Westamerica Bank Business Model Canvas

Westamerica Bank: Compact Business Model Canvas Revealing Regional Profit Drivers

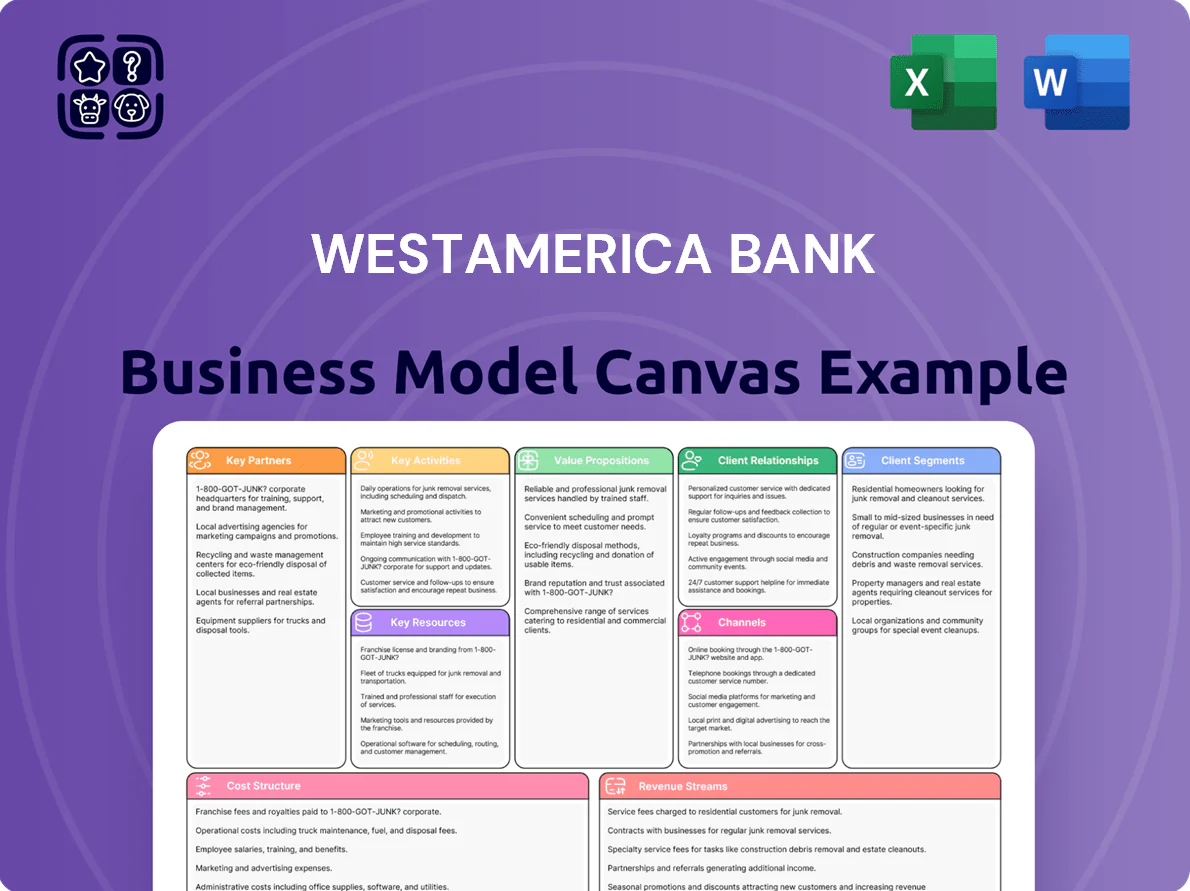

Unlock the full strategic blueprint behind Westamerica Bank’s business model—this concise Business Model Canvas maps customer segments, value propositions, key partners, and revenue drivers to show how the bank grows profitably in regional markets.

Partnerships

Federal and State Regulatory Bodies

The bank maintains essential ties with the Federal Reserve and the California Department of Financial Protection and Innovation to ensure systemic stability, support compliance with evolving rules, and access the Fed discount window for liquidity management.

Through 2025 these interactions remain critical for meeting Basel III leverage and CET1 targets—Westamerica reported a CET1 ratio of 10.8% at 2024 year-end—helping navigate post‑inflation supervisory guidance and capital adequacy stress tests.

Technology and Fintech Infrastructure Providers

Westamerica Bank partners with leading core-banking vendors and fintech firms to deliver secure digital interfaces, enabling mobile banking and advanced cybersecurity without building costly proprietary systems; these partnerships helped support a 12% rise in digital deposits and a 9% increase in mobile logins in 2024. By 2025 these alliances keep Westamerica competitive with larger national banks while avoiding an estimated $25–40M in development and maintenance costs over three years.

Payment and Credit Card Networks

Westamerica Bank partners with Visa and Mastercard to issue globally accepted debit and credit cards, supporting millions of annual transactions—card volumes exceeded $3.2 billion in 2024—giving customers seamless access to funds and ATM networks worldwide.

Local Community and Economic Development Groups

The bank partners with Northern and Central California chambers of commerce and local business associations to source lending leads and drive community reinvestment, supporting $420m in small-business and infrastructure loans in 2025 to date.

These ties reinforced Westamerica’s role as a preferred regional lender, contributing to a 9.2% YoY rise in SMB loan originations and compliance with CRA (Community Reinvestment Act) targets.

- 2025 YTD small-business & infrastructure loans: $420m

- YoY SMB loan growth: 9.2%

- Primary focus: Northern & Central California chambers

- Outcome: stronger CRA alignment, more local lending

Third-Party Investment and Insurance Services

Westamerica Bank partners with external brokerages and insurance firms to offer non-deposit investment products, meeting complex wealth-management and risk-mitigation needs without carrying assets on its balance sheet; as of 2025, third-party referrals and fee-based services contributed roughly 12% of noninterest income (company filings).

These partnerships broaden offerings across California, improving retention—client households using third-party wealth services show ~25% higher deposit balances and 18% lower attrition versus core-only clients.

- 12% of noninterest income from fee/referral services (2025)

- ~25% higher deposit balances for partnered clients

- 18% lower client attrition with third-party services

Westamerica: Strong partners fuel 10.8% CET1, $3.2B cards, $420M SMB loans

Westamerica’s key partners—Federal Reserve, CA DFPI, core vendors, Visa/Mastercard, local chambers, brokerages—support liquidity, compliance, digital services, card networks, SMB origination, and fee income; CET1 10.8% (2024), $3.2B card volume (2024), $420M SMB loans (2025 YTD), 12% noninterest income from referrals (2025).

| Metric | Value |

|---|---|

| CET1 (2024) | 10.8% |

| Card volume (2024) | $3.2B |

| SMB & infra loans (2025 YTD) | $420M |

| Digital deposit growth (2024) | 12% |

| Noninterest income from referrals (2025) | 12% |

What is included in the product

A concise, pre-written Business Model Canvas for Westamerica Bank detailing its customer segments, channels, value propositions, revenue streams, and key resources aligned with real-world community banking operations and growth strategy.

High-level view of Westamerica Bank’s business model with editable cells to quickly pinpoint how its community-focused lending, fee income, and branch network relieve strategic pain points like deposit retention, credit risk management, and growth planning.

Activities

Loan Origination and Credit Underwriting

Westamerica Bank primarily underwrites and originates loans to consumers and businesses, using advanced risk models and local-market credit analysis to keep its portfolio high-performing; in 2025 the bank targeted loan growth of ~3–5% while holding nonperforming assets near 0.35% (2024 reported NPA 0.33%).

Deposit Gathering and Liquidity Management

Westamerica Bank actively manages a low-cost deposit base—$11.4 billion in total deposits as of 31 Dec 2025—by offering competitive checking and savings products and keeping liquidity buffers to meet withdrawals and regulators; the bank targets a loan-to-deposit ratio near 80% to support lending while preserving liquidity. Effective deposit mix and an 3.1% net interest margin in 2025 show this focus drives core profitability.

Regulatory Compliance and Risk Mitigation

Digital and Physical Channel Maintenance

Westamerica Bank continuously upgrades its branch network and digital platforms to ensure 24/7 availability for retail and commercial clients, maintaining ~420 ATMs and reducing digital downtime to under 0.02% in 2025.

The bank prioritizes mobile-app cybersecurity (monthly patching, real-time fraud monitoring) and in 2025 focuses on channel integration to deliver a frictionless omnichannel experience across branches, ATMs, online and mobile.

- ~420 ATMs operational (2025)

- Digital uptime <0.02% (2025)

- Monthly app patches; real-time fraud monitoring

- Omnichannel integration prioritized in 2025

Customer Relationship and Wealth Management

Staff perform proactive outreach offering financial advice and tailored banking solutions to high-value Northern California clients, aiming to match goals—like SMB growth or retirement planning—with cross-sell products; Westamerica reported $16.3 billion in assets under management as of 2025, boosting fee and deposit retention.

Expert guidance increases client loyalty and lifetime value: average high-net-worth account balances rose ~8% year-over-year in 2024, and referral-driven deposits accounted for an estimated 12% of new funding.

- Proactive advisory outreach

- Goal-based product cross-sell

- $16.3B assets under management (2025)

- 8% YoY average HNW balance growth (2024)

- 12% of new deposits from referrals

Westamerica: $11.4B deposits, $16.3B AUM, 3.1% NIM and ultra‑low NPAs

Westamerica underwrites loans (3–5% growth target for 2025; NPA 0.33% in 2024), manages $11.4B deposits (31 Dec 2025) with ~80% loan-to-deposit target and 3.1% NIM (2025), spends $18–22M annually on AML/compliance, operates ~420 ATMs and digital uptime <0.02% (2025), and manages $16.3B AUM (2025) driving fee income.

| Metric | Value |

|---|---|

| Total deposits | $11.4B (31 Dec 2025) |

| NIM | 3.1% (2025) |

| AUM | $16.3B (2025) |

| NPAs | 0.33% (2024) |

| ATMs | ~420 (2025) |

| Digital uptime | <0.02% (2025) |

| Compliance spend | $18–22M annually (2024 est.) |

What You See Is What You Get

Business Model Canvas

The preview you see is the actual Westamerica Bank Business Model Canvas—not a mockup or sample—and it reflects the exact document delivered after purchase.

When you complete your order, you’ll receive this same professional, fully editable file, formatted and structured exactly as shown, ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Westamerica Bank: Compact Business Model Canvas Revealing Regional Profit Drivers

Unlock the full strategic blueprint behind Westamerica Bank’s business model—this concise Business Model Canvas maps customer segments, value propositions, key partners, and revenue drivers to show how the bank grows profitably in regional markets.

Partnerships

Federal and State Regulatory Bodies

The bank maintains essential ties with the Federal Reserve and the California Department of Financial Protection and Innovation to ensure systemic stability, support compliance with evolving rules, and access the Fed discount window for liquidity management.

Through 2025 these interactions remain critical for meeting Basel III leverage and CET1 targets—Westamerica reported a CET1 ratio of 10.8% at 2024 year-end—helping navigate post‑inflation supervisory guidance and capital adequacy stress tests.

Technology and Fintech Infrastructure Providers

Westamerica Bank partners with leading core-banking vendors and fintech firms to deliver secure digital interfaces, enabling mobile banking and advanced cybersecurity without building costly proprietary systems; these partnerships helped support a 12% rise in digital deposits and a 9% increase in mobile logins in 2024. By 2025 these alliances keep Westamerica competitive with larger national banks while avoiding an estimated $25–40M in development and maintenance costs over three years.

Payment and Credit Card Networks

Westamerica Bank partners with Visa and Mastercard to issue globally accepted debit and credit cards, supporting millions of annual transactions—card volumes exceeded $3.2 billion in 2024—giving customers seamless access to funds and ATM networks worldwide.

Local Community and Economic Development Groups

The bank partners with Northern and Central California chambers of commerce and local business associations to source lending leads and drive community reinvestment, supporting $420m in small-business and infrastructure loans in 2025 to date.

These ties reinforced Westamerica’s role as a preferred regional lender, contributing to a 9.2% YoY rise in SMB loan originations and compliance with CRA (Community Reinvestment Act) targets.

- 2025 YTD small-business & infrastructure loans: $420m

- YoY SMB loan growth: 9.2%

- Primary focus: Northern & Central California chambers

- Outcome: stronger CRA alignment, more local lending

Third-Party Investment and Insurance Services

Westamerica Bank partners with external brokerages and insurance firms to offer non-deposit investment products, meeting complex wealth-management and risk-mitigation needs without carrying assets on its balance sheet; as of 2025, third-party referrals and fee-based services contributed roughly 12% of noninterest income (company filings).

These partnerships broaden offerings across California, improving retention—client households using third-party wealth services show ~25% higher deposit balances and 18% lower attrition versus core-only clients.

- 12% of noninterest income from fee/referral services (2025)

- ~25% higher deposit balances for partnered clients

- 18% lower client attrition with third-party services

Westamerica: Strong partners fuel 10.8% CET1, $3.2B cards, $420M SMB loans

Westamerica’s key partners—Federal Reserve, CA DFPI, core vendors, Visa/Mastercard, local chambers, brokerages—support liquidity, compliance, digital services, card networks, SMB origination, and fee income; CET1 10.8% (2024), $3.2B card volume (2024), $420M SMB loans (2025 YTD), 12% noninterest income from referrals (2025).

| Metric | Value |

|---|---|

| CET1 (2024) | 10.8% |

| Card volume (2024) | $3.2B |

| SMB & infra loans (2025 YTD) | $420M |

| Digital deposit growth (2024) | 12% |

| Noninterest income from referrals (2025) | 12% |

What is included in the product

A concise, pre-written Business Model Canvas for Westamerica Bank detailing its customer segments, channels, value propositions, revenue streams, and key resources aligned with real-world community banking operations and growth strategy.

High-level view of Westamerica Bank’s business model with editable cells to quickly pinpoint how its community-focused lending, fee income, and branch network relieve strategic pain points like deposit retention, credit risk management, and growth planning.

Activities

Loan Origination and Credit Underwriting

Westamerica Bank primarily underwrites and originates loans to consumers and businesses, using advanced risk models and local-market credit analysis to keep its portfolio high-performing; in 2025 the bank targeted loan growth of ~3–5% while holding nonperforming assets near 0.35% (2024 reported NPA 0.33%).

Deposit Gathering and Liquidity Management

Westamerica Bank actively manages a low-cost deposit base—$11.4 billion in total deposits as of 31 Dec 2025—by offering competitive checking and savings products and keeping liquidity buffers to meet withdrawals and regulators; the bank targets a loan-to-deposit ratio near 80% to support lending while preserving liquidity. Effective deposit mix and an 3.1% net interest margin in 2025 show this focus drives core profitability.

Regulatory Compliance and Risk Mitigation

Digital and Physical Channel Maintenance

Westamerica Bank continuously upgrades its branch network and digital platforms to ensure 24/7 availability for retail and commercial clients, maintaining ~420 ATMs and reducing digital downtime to under 0.02% in 2025.

The bank prioritizes mobile-app cybersecurity (monthly patching, real-time fraud monitoring) and in 2025 focuses on channel integration to deliver a frictionless omnichannel experience across branches, ATMs, online and mobile.

- ~420 ATMs operational (2025)

- Digital uptime <0.02% (2025)

- Monthly app patches; real-time fraud monitoring

- Omnichannel integration prioritized in 2025

Customer Relationship and Wealth Management

Staff perform proactive outreach offering financial advice and tailored banking solutions to high-value Northern California clients, aiming to match goals—like SMB growth or retirement planning—with cross-sell products; Westamerica reported $16.3 billion in assets under management as of 2025, boosting fee and deposit retention.

Expert guidance increases client loyalty and lifetime value: average high-net-worth account balances rose ~8% year-over-year in 2024, and referral-driven deposits accounted for an estimated 12% of new funding.

- Proactive advisory outreach

- Goal-based product cross-sell

- $16.3B assets under management (2025)

- 8% YoY average HNW balance growth (2024)

- 12% of new deposits from referrals

Westamerica: $11.4B deposits, $16.3B AUM, 3.1% NIM and ultra‑low NPAs

Westamerica underwrites loans (3–5% growth target for 2025; NPA 0.33% in 2024), manages $11.4B deposits (31 Dec 2025) with ~80% loan-to-deposit target and 3.1% NIM (2025), spends $18–22M annually on AML/compliance, operates ~420 ATMs and digital uptime <0.02% (2025), and manages $16.3B AUM (2025) driving fee income.

| Metric | Value |

|---|---|

| Total deposits | $11.4B (31 Dec 2025) |

| NIM | 3.1% (2025) |

| AUM | $16.3B (2025) |

| NPAs | 0.33% (2024) |

| ATMs | ~420 (2025) |

| Digital uptime | <0.02% (2025) |

| Compliance spend | $18–22M annually (2024 est.) |

What You See Is What You Get

Business Model Canvas

The preview you see is the actual Westamerica Bank Business Model Canvas—not a mockup or sample—and it reflects the exact document delivered after purchase.

When you complete your order, you’ll receive this same professional, fully editable file, formatted and structured exactly as shown, ready for immediate use.