Western Alliance Bancorp. Business Model Canvas

Western Alliance Bancorp: Complete Business Model Canvas & Growth Blueprint

Unlock the full strategic blueprint behind Western Alliance Bancorp.’s business model—see how it serves niche commercial clients, leverages digital lending and treasury services, and balances fee income with interest margins to drive growth.

Purchase the complete Business Model Canvas for a section-by-section, editable Word and Excel file that reveals partnerships, cost structure, and revenue levers—perfect for investors, analysts, and strategists seeking actionable insights.

Partnerships

FinTech and Technology Integration Partners

Collaborations with FinTechs let Western Alliance Bancorp offer modern digital platforms and treasury-management tools—reducing tech spend vs. in-house build and matching national banks; in 2024 WA Bancorp reported 12% of deposits serviced via digital channels, up from 8% in 2022. By 2025 integrations emphasize AI-driven analytics and automated compliance monitoring, cutting manual review time by an estimated 30% and lowering compliance costs per loan by ~15%.

Mortgage Aggregator and Correspondent Networks

Through AmeriHome Mortgage, Western Alliance maintains extensive correspondent and aggregator ties with mortgage originators and institutional investors, channeling roughly $24.5 billion of mortgage production into servicing and securitization in 2024 and supporting a non-interest income stream that was 32% of total revenue in FY2024.

Regulatory and Compliance Agencies

Ongoing cooperation with the Federal Reserve and Arizona, California and Nevada state banking regulators keeps Western Alliance Bancorp compliant with evolving capital rules; as of Q4 2025 the bank reported a CET1 ratio of 11.8%, meeting Fed stress expectations and preserving its charter. These ties protect its market reputation and, through proactive engagement since post-2023 rule changes, reduce remediation costs and supervisory actions.

Industry-Specific Professional Associations

Partnerships with Life Sciences, Technology, and HOA associations give Western Alliance Bancorp sector-specific deal flow and market insight, driving 28% higher commercial originations in targeted niches in 2024 versus non-specialty segments.

These alliances boost lead generation and thought leadership, yield higher-value clients (average commercial deposit size +42% in 2024), and create networking pipelines for CRE and specialized lending.

- 28% higher originations (2024)

- +42% average deposit size (2024)

- Stronger CRE and specialized lending pipelines

Community and Economic Development Groups

Engaging local community and economic development groups helps Western Alliance Bancorp meet Community Reinvestment Act goals and boosts regional brand presence across Arizona and Nevada, where the bank held about $62.3 billion in loans and $56.1 billion in deposits at year-end 2024.

These partnerships surface $-sized lending prospects in small business and affordable housing, improve goodwill in core markets, and help retain a stable local deposit base—44% of deposits in 2024 came from core-state customers.

- Supports CRA compliance

- Drives local lending deals

- Builds goodwill in AZ/NV

- Stabilizes core deposits (44% in 2024)

Partnership-driven fintech & mortgage growth: $24.5B production, 12% digital deposits

Key partnerships supply digital fintech platforms (12% digital deposits in 2024), mortgage channels via AmeriHome (≈$24.5B production, non‑interest income 32% FY2024), regulator engagement supporting CET1 11.8% (Q4 2025), sector associations driving +28% originations and +42% avg commercial deposit (2024), and community groups stabilizing core deposits (44% in 2024).

| Metric | Value |

|---|---|

| Digital deposits (2024) | 12% |

| Mortgage production (2024) | $24.5B |

| Non‑interest income (FY2024) | 32% |

| CET1 (Q4 2025) | 11.8% |

| Sector originations uplift (2024) | +28% |

| Avg commercial deposit lift (2024) | +42% |

| Core-state deposits (2024) | 44% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Western Alliance Bancorp outlining customer segments, channels, value propositions, revenue streams, key resources, activities, partnerships, cost structure, and risk factors aligned with the bank’s commercial and specialty finance strategy.

Organized into nine BMC blocks with competitive advantage analysis, SWOT-linked insights, and polished narrative suitable for presentations, investor discussions, and strategic decision-making.

High-level view of Western Alliance Bancorp’s business model with editable cells — quickly identify core components like commercial lending, treasury services, and specialty banking with a one-page snapshot tailored for collaboration.

Activities

Specialized Commercial Lending Operations

Western Alliance Bancorp focuses on tailored credit solutions for mid-market firms and niche industries, using rigorous underwriting and sector-specific risk assessment to keep nonperforming loans low (0.45% NPLs at Q4 2025) and maintain CET1 capital above 10.5%. By end-2025, specialized commercial lending drove asset growth, lifting total loans to $60.2 billion, up 18% year-over-year.

Comprehensive Treasury Management Services

Managing liquidity and cash flow for commercial clients is a core operation at Western Alliance Bancorp, which held $65.6 billion in total assets and $37.2 billion in deposits as of 12/31/2025; the bank runs platforms for electronic payments, fraud prevention, and automated reconciliation that processed billions in ACH and wire volume in 2025, driving higher deposit retention and deeper, stickier commercial relationships.

Mortgage Servicing and Secondary Market Activities

Through its national mortgage platform, Western Alliance Bancorp manages collection and administration of residential loans, originating about $5.2B in mortgages in 2024 and servicing roughly $28B in unpaid principal balance as of 12/31/2024. Key activities: loan acquisition, hedging interest-rate risk via TBA and interest-rate swaps, and selling mortgage-backed securities in the secondary market, generating counter-cyclical fee and trading income that offset deposit margin pressure.

Risk Management and Regulatory Compliance

Continuous monitoring of credit, market, and operational risks is non-negotiable at Western Alliance Bancorp, including monthly stress tests and daily liquidity tracking; the bank reported a CET1 ratio of 12.8% and LCR (liquidity coverage ratio) above 110% in 2025.

Compliance covers AML (anti-money laundering) rules and automated federal reporting using advanced software that reduced manual report time by ~60% in 2025.

- Monthly stress tests

- Daily liquidity tracking (LCR >110%)

- CET1 ratio 12.8% (2025)

- AML compliance automated

- Reporting time cut ~60% (2025)

Strategic Deposit Acquisition and Diversification

Western Alliance actively manages its liability mix to keep funding stable and low-cost, shifting toward granular deposits—notably homeowner association (HOA) and property management accounts—which made up roughly 18% of total deposits in 2024, lowering reliance on wholesale funding from 22% in 2022 to ~12% by Q4 2024.

- Target: HOA/property management niches

- 2024: granular deposits ≈ 18% of deposits

- Wholesale funding cut to ~12% by Q4 2024

- Result: improved liquidity coverage and cost control

Western Alliance: Strong growth, low NPLs (0.45%) and CET1 12.8%—loans $60.2B

Western Alliance runs specialized commercial lending, mortgage origination/servicing, and payment platforms, keeping NPLs low (0.45% Q4 2025), CET1 at 12.8% (2025), loans $60.2B (+18% YoY 2025), assets $65.6B and deposits $37.2B (12/31/2025), while shifting deposits to granular sources (HOA ~18% of deposits 2024) and cutting wholesale funding to ~12% (Q4 2024).

| Metric | Date | Value |

|---|---|---|

| NPLs | Q4 2025 | 0.45% |

| CET1 | 2025 | 12.8% |

| Total loans | 12/31/2025 | $60.2B |

| Assets | 12/31/2025 | $65.6B |

| Deposits | 12/31/2025 | $37.2B |

| Mortgage originations | 2024 | $5.2B |

| HOA deposits | 2024 | ~18% |

| Wholesale funding | Q4 2024 | ~12% |

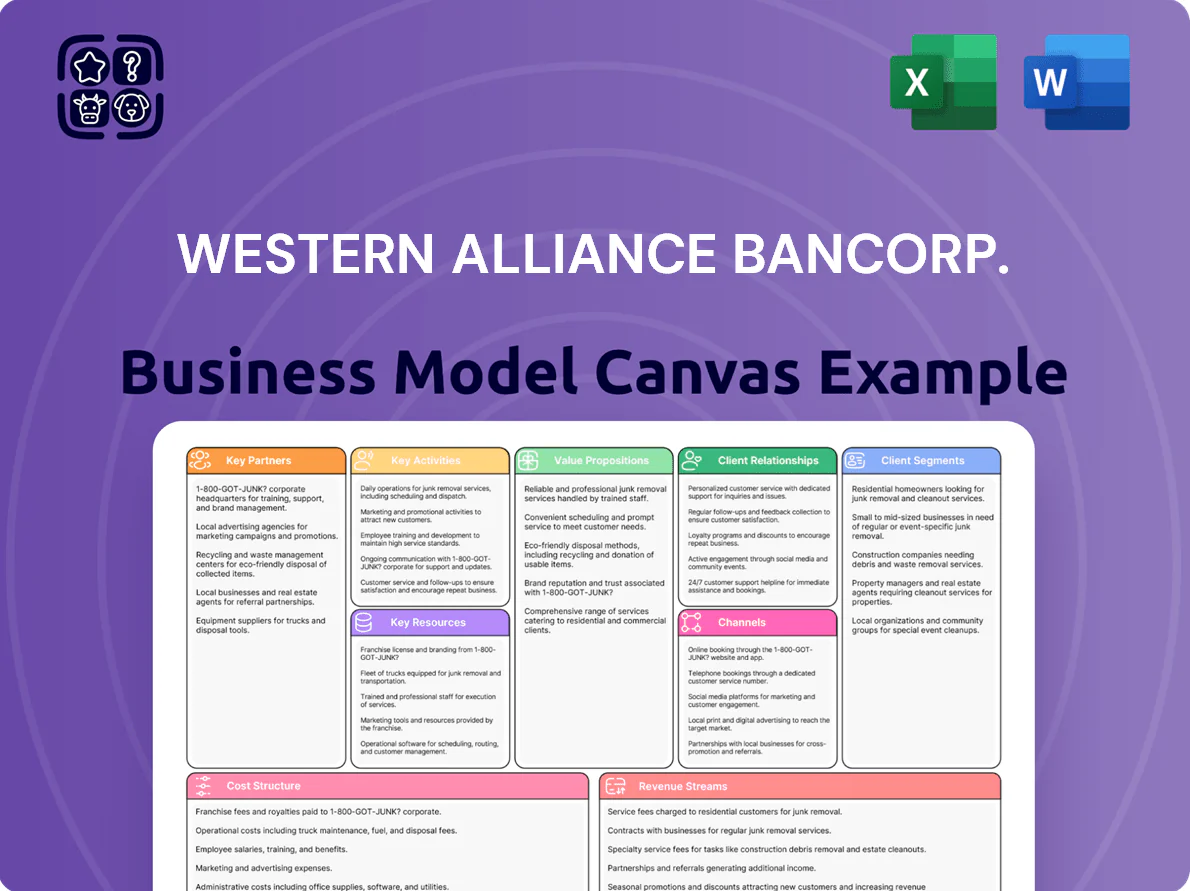

What You See Is What You Get

Business Model Canvas

The Business Model Canvas preview shown here is the exact section from the final Western Alliance Bancorp document—you’re not viewing a mockup or sample; it’s the real deliverable you’ll receive after purchase.

Upon completion of your order, you’ll get the same comprehensive file, fully formatted and ready-to-edit in Word and Excel, with all canvas blocks, value propositions, revenue streams, and cost structures included.

No placeholders or missing pages—what you see is what you’ll download: a professional, complete Business Model Canvas for Western Alliance Bancorp, instantly accessible and ready for presentation or analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Western Alliance Bancorp: Complete Business Model Canvas & Growth Blueprint

Unlock the full strategic blueprint behind Western Alliance Bancorp.’s business model—see how it serves niche commercial clients, leverages digital lending and treasury services, and balances fee income with interest margins to drive growth.

Purchase the complete Business Model Canvas for a section-by-section, editable Word and Excel file that reveals partnerships, cost structure, and revenue levers—perfect for investors, analysts, and strategists seeking actionable insights.

Partnerships

FinTech and Technology Integration Partners

Collaborations with FinTechs let Western Alliance Bancorp offer modern digital platforms and treasury-management tools—reducing tech spend vs. in-house build and matching national banks; in 2024 WA Bancorp reported 12% of deposits serviced via digital channels, up from 8% in 2022. By 2025 integrations emphasize AI-driven analytics and automated compliance monitoring, cutting manual review time by an estimated 30% and lowering compliance costs per loan by ~15%.

Mortgage Aggregator and Correspondent Networks

Through AmeriHome Mortgage, Western Alliance maintains extensive correspondent and aggregator ties with mortgage originators and institutional investors, channeling roughly $24.5 billion of mortgage production into servicing and securitization in 2024 and supporting a non-interest income stream that was 32% of total revenue in FY2024.

Regulatory and Compliance Agencies

Ongoing cooperation with the Federal Reserve and Arizona, California and Nevada state banking regulators keeps Western Alliance Bancorp compliant with evolving capital rules; as of Q4 2025 the bank reported a CET1 ratio of 11.8%, meeting Fed stress expectations and preserving its charter. These ties protect its market reputation and, through proactive engagement since post-2023 rule changes, reduce remediation costs and supervisory actions.

Industry-Specific Professional Associations

Partnerships with Life Sciences, Technology, and HOA associations give Western Alliance Bancorp sector-specific deal flow and market insight, driving 28% higher commercial originations in targeted niches in 2024 versus non-specialty segments.

These alliances boost lead generation and thought leadership, yield higher-value clients (average commercial deposit size +42% in 2024), and create networking pipelines for CRE and specialized lending.

- 28% higher originations (2024)

- +42% average deposit size (2024)

- Stronger CRE and specialized lending pipelines

Community and Economic Development Groups

Engaging local community and economic development groups helps Western Alliance Bancorp meet Community Reinvestment Act goals and boosts regional brand presence across Arizona and Nevada, where the bank held about $62.3 billion in loans and $56.1 billion in deposits at year-end 2024.

These partnerships surface $-sized lending prospects in small business and affordable housing, improve goodwill in core markets, and help retain a stable local deposit base—44% of deposits in 2024 came from core-state customers.

- Supports CRA compliance

- Drives local lending deals

- Builds goodwill in AZ/NV

- Stabilizes core deposits (44% in 2024)

Partnership-driven fintech & mortgage growth: $24.5B production, 12% digital deposits

Key partnerships supply digital fintech platforms (12% digital deposits in 2024), mortgage channels via AmeriHome (≈$24.5B production, non‑interest income 32% FY2024), regulator engagement supporting CET1 11.8% (Q4 2025), sector associations driving +28% originations and +42% avg commercial deposit (2024), and community groups stabilizing core deposits (44% in 2024).

| Metric | Value |

|---|---|

| Digital deposits (2024) | 12% |

| Mortgage production (2024) | $24.5B |

| Non‑interest income (FY2024) | 32% |

| CET1 (Q4 2025) | 11.8% |

| Sector originations uplift (2024) | +28% |

| Avg commercial deposit lift (2024) | +42% |

| Core-state deposits (2024) | 44% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Western Alliance Bancorp outlining customer segments, channels, value propositions, revenue streams, key resources, activities, partnerships, cost structure, and risk factors aligned with the bank’s commercial and specialty finance strategy.

Organized into nine BMC blocks with competitive advantage analysis, SWOT-linked insights, and polished narrative suitable for presentations, investor discussions, and strategic decision-making.

High-level view of Western Alliance Bancorp’s business model with editable cells — quickly identify core components like commercial lending, treasury services, and specialty banking with a one-page snapshot tailored for collaboration.

Activities

Specialized Commercial Lending Operations

Western Alliance Bancorp focuses on tailored credit solutions for mid-market firms and niche industries, using rigorous underwriting and sector-specific risk assessment to keep nonperforming loans low (0.45% NPLs at Q4 2025) and maintain CET1 capital above 10.5%. By end-2025, specialized commercial lending drove asset growth, lifting total loans to $60.2 billion, up 18% year-over-year.

Comprehensive Treasury Management Services

Managing liquidity and cash flow for commercial clients is a core operation at Western Alliance Bancorp, which held $65.6 billion in total assets and $37.2 billion in deposits as of 12/31/2025; the bank runs platforms for electronic payments, fraud prevention, and automated reconciliation that processed billions in ACH and wire volume in 2025, driving higher deposit retention and deeper, stickier commercial relationships.

Mortgage Servicing and Secondary Market Activities

Through its national mortgage platform, Western Alliance Bancorp manages collection and administration of residential loans, originating about $5.2B in mortgages in 2024 and servicing roughly $28B in unpaid principal balance as of 12/31/2024. Key activities: loan acquisition, hedging interest-rate risk via TBA and interest-rate swaps, and selling mortgage-backed securities in the secondary market, generating counter-cyclical fee and trading income that offset deposit margin pressure.

Risk Management and Regulatory Compliance

Continuous monitoring of credit, market, and operational risks is non-negotiable at Western Alliance Bancorp, including monthly stress tests and daily liquidity tracking; the bank reported a CET1 ratio of 12.8% and LCR (liquidity coverage ratio) above 110% in 2025.

Compliance covers AML (anti-money laundering) rules and automated federal reporting using advanced software that reduced manual report time by ~60% in 2025.

- Monthly stress tests

- Daily liquidity tracking (LCR >110%)

- CET1 ratio 12.8% (2025)

- AML compliance automated

- Reporting time cut ~60% (2025)

Strategic Deposit Acquisition and Diversification

Western Alliance actively manages its liability mix to keep funding stable and low-cost, shifting toward granular deposits—notably homeowner association (HOA) and property management accounts—which made up roughly 18% of total deposits in 2024, lowering reliance on wholesale funding from 22% in 2022 to ~12% by Q4 2024.

- Target: HOA/property management niches

- 2024: granular deposits ≈ 18% of deposits

- Wholesale funding cut to ~12% by Q4 2024

- Result: improved liquidity coverage and cost control

Western Alliance: Strong growth, low NPLs (0.45%) and CET1 12.8%—loans $60.2B

Western Alliance runs specialized commercial lending, mortgage origination/servicing, and payment platforms, keeping NPLs low (0.45% Q4 2025), CET1 at 12.8% (2025), loans $60.2B (+18% YoY 2025), assets $65.6B and deposits $37.2B (12/31/2025), while shifting deposits to granular sources (HOA ~18% of deposits 2024) and cutting wholesale funding to ~12% (Q4 2024).

| Metric | Date | Value |

|---|---|---|

| NPLs | Q4 2025 | 0.45% |

| CET1 | 2025 | 12.8% |

| Total loans | 12/31/2025 | $60.2B |

| Assets | 12/31/2025 | $65.6B |

| Deposits | 12/31/2025 | $37.2B |

| Mortgage originations | 2024 | $5.2B |

| HOA deposits | 2024 | ~18% |

| Wholesale funding | Q4 2024 | ~12% |

What You See Is What You Get

Business Model Canvas

The Business Model Canvas preview shown here is the exact section from the final Western Alliance Bancorp document—you’re not viewing a mockup or sample; it’s the real deliverable you’ll receive after purchase.

Upon completion of your order, you’ll get the same comprehensive file, fully formatted and ready-to-edit in Word and Excel, with all canvas blocks, value propositions, revenue streams, and cost structures included.

No placeholders or missing pages—what you see is what you’ll download: a professional, complete Business Model Canvas for Western Alliance Bancorp, instantly accessible and ready for presentation or analysis.