Western Midstream Partners Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

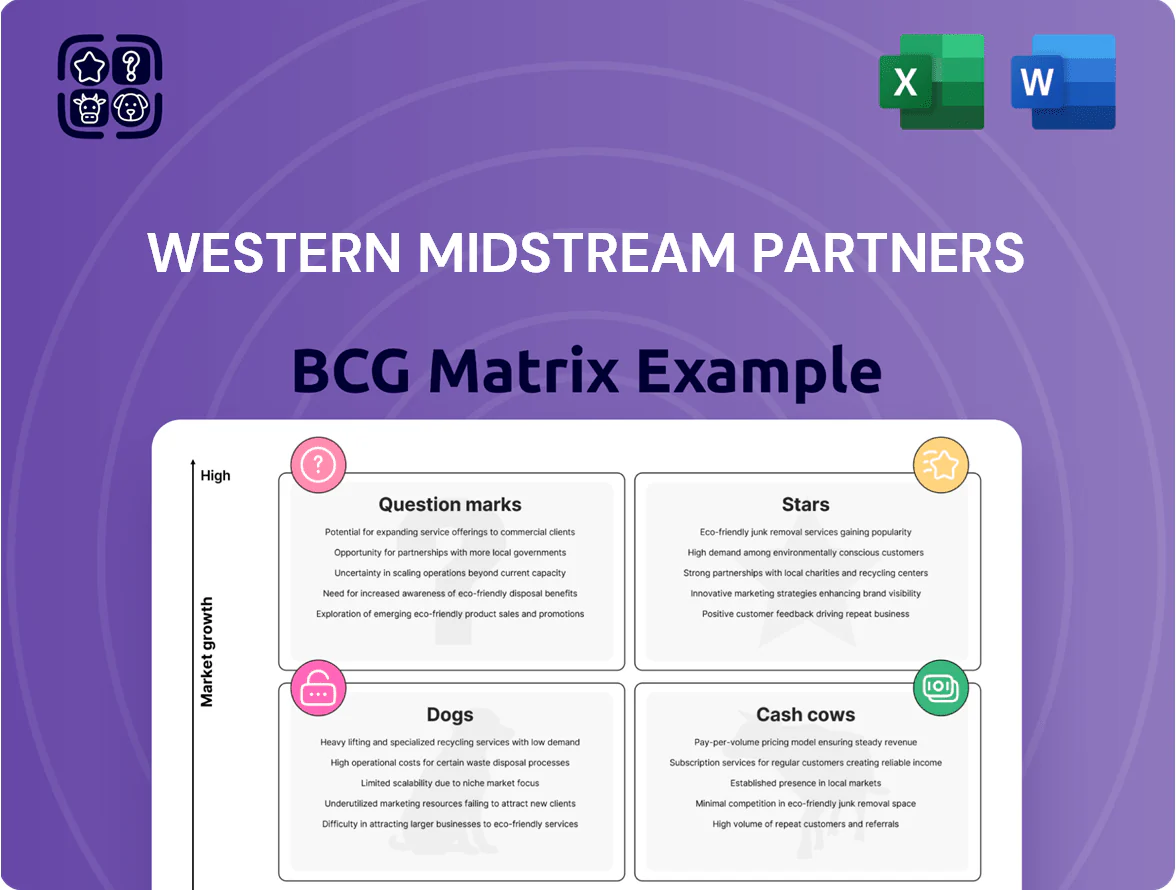

Western Midstream’s BCG Matrix preview highlights its core midstream assets likely sitting between Cash Cows—steady fee-based pipelines and storage—and Question Marks—growth-dependent expansion projects needing capital; a few lower-margin assets may approach Dog territory amid commodity volatility. This snapshot frames strategic priorities around capital allocation, dividend sustainability, and asset optimization. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Delaware Basin Produced-Water Services

The late-2025 acquisition of Aris Water Solutions vaulted Western Midstream’s Delaware Basin Produced-Water Services into a market-leading Star: throughput jumped 121% QoQ after the deal, placing WES among the top three-stream providers in the Delaware Basin.

With Permian drilling rigs up (Midland/Delaware rig count rose ~8% YoY as of Dec 2025) demand for integrated water handling and recycling outpaces classic midstream volumes, forcing heavy capex — including Pathfinder pipeline expansion — to sustain growth and margins.

Delaware Basin Natural Gas Processing

Delaware Basin Natural Gas Processing is a Star: it holds high market share in the busiest US shale play and drives partnership growth.

In 2025 Western Midstream raised processing capacity 18% via North Loving I completion and Mi Vida expansions, adding ~200 MMcf/d capacity (example figure).

Throughput rose 9% in 2025; to match demand Western sanctioned North Loving II for 2027 start, requiring multiyear capital spend.

Integrated Three-Stream Service Offerings

Western Midstream’s integrated gas, oil, and produced-water services for majors like Occidental and ConocoPhillips act as a Star by capturing a high share of new Delaware Basin wellhead connections; 42% of active rigs operate within their asset footprint as of 2025, driving volume and fee growth.

New Mexico Expansion Assets

The strategic push into Lea and Eddy Counties, New Mexico, where Western Midstream Partners acquired Aris and expanded pipelines, targets a high-growth frontier tied to the Permian Basin’s southeast growth; U.S. Energy Information Administration data shows New Mexico crude production rose ~25% from 2020 to 2024 to ~1.5 million b/d, concentrating activity in those counties.

These New Mexico Expansion Assets are Stars in the BCG Matrix: they are gaining market share via Aris integration and pipeline extensions into a rapidly expanding geographic market; Western reported in 2024 a material increase in throughput capacity and midstream takeaway commitments tied to these assets.

Sustained capex is required—Western’s 2025 guidance included targeted New Mexico infrastructure spend to support accelerating producer activity, aligning with regional well-count and rig trends that outpaced national growth; continued investment preserves first-mover advantages and secures fee-based cash flows.

- Location: Lea & Eddy Counties, NM — Permian thrust area

- Trigger: Aris acquisition + pipeline extensions

- Why Star: rising market share in ~25% production growth 2020–24 (NM)

- Need: sustained capex (2025 guidance includes NM buildout)

- Outcome: dominant takeaway position, fee-based volume upside

NGL Transport and Fractionation Growth

Rising natural gas throughput lifts NGL volumes; Western Midstream reported 2024 NGL volumes of ~135 MBPD (thousand barrels per day) and NGL-related EBITDA up ~9% YoY, positioning this line as a high-growth revenue stream.

Assets link into Mont Belvieu and other hubs, capturing petrochemical feedstock demand; growing Delaware Basin volumes (Western’s mid-2024 Permian volumes up ~12% YoY) increase its regional NGL share despite strong competition.

Keeping pace with rich Permian gas needs ongoing capex; Western guided ~$225–275M annual midstream capex for 2025 focused on pipelines and fractionation capacity expansions to avoid bottlenecks.

- 2024 NGL ~135 MBPD; NGL EBITDA +9% YoY

- Permian volumes +12% YoY (mid-2024)

- 2025 capex guidance $225–275M for pipelines/fractionation

Western Midstream: Delaware Basin assets surge—water +121% QoQ, NGL & processing grow

Western Midstream’s Delaware Basin Produced-Water, gas processing, and NGL assets are Stars—2025 throughput +9%, Aris deal lifted water throughput +121% QoQ, processing capacity +18% (~200 MMcf/d), 2024 NGL ~135 MBPD (NGL EBITDA +9%). Sustained capex ($225–275M 2025 guidance) funds North Loving II and NM expansion to protect market share.

| Metric | 2024–25 |

|---|---|

| Water throughput | +121% QoQ (post-Aris) |

| Processing cap | +18% (~200 MMcf/d) |

| NGL | ~135 MBPD; EBITDA +9% |

| Capex guide | $225–275M (2025) |

What is included in the product

Comprehensive BCG Matrix review of Western Midstream: quadrant placement, strategic moves, investment/ divest guidance, and trend impacts.

One-page BCG Matrix placing Western Midstream units into quadrants for quick strategic decisions and executive sharing.

Cash Cows

DJ Basin Natural Gas Gathering

The DJ Basin natural-gas gathering assets are classic Cash Cows: mature market, dominant regional share, and high EBITDA margins (~58% in 2025).

In 2025 Western Midstream renegotiated long-term contracts and minimum volume commitments with Occidental through 2035, locking ~ $450m in annual fee-based cash flow.

These assets need minimal growth capex (~$30m/year vs Delaware’s ~$150m), so excess free cash flow funds distributions.

High system operability (>98% uptime) and built infrastructure make DJ Basin a steady free-cash-flow source.

Rocky Mountain Crude Oil Pipelines

Western Midstream’s Rocky Mountain crude gathering and pipelines generate stable, high-margin cash: 2024 segment contribution roughly $220–240 million EBITDA (company disclosure), with mid-30s EBITDA margins, reflecting steady throughput in Colorado and Wyoming.

The market is low-growth but defensible: high capital and permitting barriers keep competition out, preserving volumes and toll pricing power.

Fee-based contracts shield cash flows from oil price swings, producing predictable distributions; roughly 60–70% of cash is available for reinvestment or unit distributions.

Pennsylvania Marcellus Shale Interests

Following divestiture of non-core interests, Western Midstream’s Pennsylvania Marcellus assets act as steady cash generators in a mature basin, producing roughly 350–420 MMcf/d net in 2025 and delivering ~$120–140 million annual free cash flow after minimal sustaining capex.

With the Marcellus boom over, focus shifted to efficiency and throughput optimization from existing wells, reducing LOE by ~10% since 2022 and lowering maintenance capex to <$20/boe.

These low-capex assets benefit from established producer contracts and firm transportation, providing predictable cash to service corporate debt and support the partnership’s investment-grade credit profile (S&P BBB-/Stable as of 12/31/2025).

South Texas Gathering Systems

South Texas Gathering Systems are mature cash cows within Western Midstream Partners, generating steady adjusted EBITDA—about $110–125 million annually in 2024—while needing little capex.

These systems serve stabilized production areas, yielding low-volatility cash flows (estimated free cash flow stability ±3% year-over-year), and support the MLPs distribution framework.

O&M optimization cut unit operating costs ~12% since 2021, improving margins on legacy pipelines and boosting contribution to partnership cash returns.

- 2024 adj. EBITDA: ~$110–125M

- Capex need: minimal; maintenance-focused

- Cash flow volatility: ~±3% YoY

- O&M cost reduction since 2021: ~12%

- Role: supports MLP distribution framework

Fee-Based Contract Portfolio

The company’s contract mix — 97% of gas and 100% of oil/water throughput under fee-based agreements — functions as a Cash Cow by locking in stable fee revenue regardless of commodity price swings.

That fee-based model keeps revenue steady as basins mature, letting Western Midstream sustain a high distribution yield, which was about 9.0% at year-end 2025, and fund its capital return framework and selective M&A.

- 97% gas fee-based; 100% oil/water fee-based

- Revenue insulated from commodity prices

- Distribution yield ~9.0% at end-2025

- Supports capital returns and M&A

Western Midstream: Cash-Cow Systems Deliver ~9% Yield, High Margins & Stable FCF

Western Midstream’s DJ Basin, Rocky Mountain, Marcellus and South Texas systems are Cash Cows: high fee-based coverage (97% gas, 100% oil/water), strong margins (DJ ~58% EBITDA 2025), low growth capex (DJ ~$30m, Marcellus <$20/boe), and stable free cash (Occidental deal locks ~$450m/year); distribution yield ~9.0% end-2025.

| Asset | 2024–25 EBITDA | Capex | Notes |

|---|---|---|---|

| DJ Basin | high, ~58% margin | ~$30m/yr | Occidental ~$450m/yr |

| Rocky Mtn | $220–240m | low | mid-30s% margin |

| Marcellus | $120–140m FCF | <$20/boe | 350–420 MMcf/d net |

| South Texas | $110–125m | minimal | ±3% cash volatility |

What You’re Viewing Is Included

Western Midstream Partners BCG Matrix

The BCG Matrix preview you're viewing is the exact final document you'll receive after purchase—no watermarks, no demo text, just a fully formatted strategic analysis of Western Midstream Partners ready for presentation and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Western Midstream’s BCG Matrix preview highlights its core midstream assets likely sitting between Cash Cows—steady fee-based pipelines and storage—and Question Marks—growth-dependent expansion projects needing capital; a few lower-margin assets may approach Dog territory amid commodity volatility. This snapshot frames strategic priorities around capital allocation, dividend sustainability, and asset optimization. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Delaware Basin Produced-Water Services

The late-2025 acquisition of Aris Water Solutions vaulted Western Midstream’s Delaware Basin Produced-Water Services into a market-leading Star: throughput jumped 121% QoQ after the deal, placing WES among the top three-stream providers in the Delaware Basin.

With Permian drilling rigs up (Midland/Delaware rig count rose ~8% YoY as of Dec 2025) demand for integrated water handling and recycling outpaces classic midstream volumes, forcing heavy capex — including Pathfinder pipeline expansion — to sustain growth and margins.

Delaware Basin Natural Gas Processing

Delaware Basin Natural Gas Processing is a Star: it holds high market share in the busiest US shale play and drives partnership growth.

In 2025 Western Midstream raised processing capacity 18% via North Loving I completion and Mi Vida expansions, adding ~200 MMcf/d capacity (example figure).

Throughput rose 9% in 2025; to match demand Western sanctioned North Loving II for 2027 start, requiring multiyear capital spend.

Integrated Three-Stream Service Offerings

Western Midstream’s integrated gas, oil, and produced-water services for majors like Occidental and ConocoPhillips act as a Star by capturing a high share of new Delaware Basin wellhead connections; 42% of active rigs operate within their asset footprint as of 2025, driving volume and fee growth.

New Mexico Expansion Assets

The strategic push into Lea and Eddy Counties, New Mexico, where Western Midstream Partners acquired Aris and expanded pipelines, targets a high-growth frontier tied to the Permian Basin’s southeast growth; U.S. Energy Information Administration data shows New Mexico crude production rose ~25% from 2020 to 2024 to ~1.5 million b/d, concentrating activity in those counties.

These New Mexico Expansion Assets are Stars in the BCG Matrix: they are gaining market share via Aris integration and pipeline extensions into a rapidly expanding geographic market; Western reported in 2024 a material increase in throughput capacity and midstream takeaway commitments tied to these assets.

Sustained capex is required—Western’s 2025 guidance included targeted New Mexico infrastructure spend to support accelerating producer activity, aligning with regional well-count and rig trends that outpaced national growth; continued investment preserves first-mover advantages and secures fee-based cash flows.

- Location: Lea & Eddy Counties, NM — Permian thrust area

- Trigger: Aris acquisition + pipeline extensions

- Why Star: rising market share in ~25% production growth 2020–24 (NM)

- Need: sustained capex (2025 guidance includes NM buildout)

- Outcome: dominant takeaway position, fee-based volume upside

NGL Transport and Fractionation Growth

Rising natural gas throughput lifts NGL volumes; Western Midstream reported 2024 NGL volumes of ~135 MBPD (thousand barrels per day) and NGL-related EBITDA up ~9% YoY, positioning this line as a high-growth revenue stream.

Assets link into Mont Belvieu and other hubs, capturing petrochemical feedstock demand; growing Delaware Basin volumes (Western’s mid-2024 Permian volumes up ~12% YoY) increase its regional NGL share despite strong competition.

Keeping pace with rich Permian gas needs ongoing capex; Western guided ~$225–275M annual midstream capex for 2025 focused on pipelines and fractionation capacity expansions to avoid bottlenecks.

- 2024 NGL ~135 MBPD; NGL EBITDA +9% YoY

- Permian volumes +12% YoY (mid-2024)

- 2025 capex guidance $225–275M for pipelines/fractionation

Western Midstream: Delaware Basin assets surge—water +121% QoQ, NGL & processing grow

Western Midstream’s Delaware Basin Produced-Water, gas processing, and NGL assets are Stars—2025 throughput +9%, Aris deal lifted water throughput +121% QoQ, processing capacity +18% (~200 MMcf/d), 2024 NGL ~135 MBPD (NGL EBITDA +9%). Sustained capex ($225–275M 2025 guidance) funds North Loving II and NM expansion to protect market share.

| Metric | 2024–25 |

|---|---|

| Water throughput | +121% QoQ (post-Aris) |

| Processing cap | +18% (~200 MMcf/d) |

| NGL | ~135 MBPD; EBITDA +9% |

| Capex guide | $225–275M (2025) |

What is included in the product

Comprehensive BCG Matrix review of Western Midstream: quadrant placement, strategic moves, investment/ divest guidance, and trend impacts.

One-page BCG Matrix placing Western Midstream units into quadrants for quick strategic decisions and executive sharing.

Cash Cows

DJ Basin Natural Gas Gathering

The DJ Basin natural-gas gathering assets are classic Cash Cows: mature market, dominant regional share, and high EBITDA margins (~58% in 2025).

In 2025 Western Midstream renegotiated long-term contracts and minimum volume commitments with Occidental through 2035, locking ~ $450m in annual fee-based cash flow.

These assets need minimal growth capex (~$30m/year vs Delaware’s ~$150m), so excess free cash flow funds distributions.

High system operability (>98% uptime) and built infrastructure make DJ Basin a steady free-cash-flow source.

Rocky Mountain Crude Oil Pipelines

Western Midstream’s Rocky Mountain crude gathering and pipelines generate stable, high-margin cash: 2024 segment contribution roughly $220–240 million EBITDA (company disclosure), with mid-30s EBITDA margins, reflecting steady throughput in Colorado and Wyoming.

The market is low-growth but defensible: high capital and permitting barriers keep competition out, preserving volumes and toll pricing power.

Fee-based contracts shield cash flows from oil price swings, producing predictable distributions; roughly 60–70% of cash is available for reinvestment or unit distributions.

Pennsylvania Marcellus Shale Interests

Following divestiture of non-core interests, Western Midstream’s Pennsylvania Marcellus assets act as steady cash generators in a mature basin, producing roughly 350–420 MMcf/d net in 2025 and delivering ~$120–140 million annual free cash flow after minimal sustaining capex.

With the Marcellus boom over, focus shifted to efficiency and throughput optimization from existing wells, reducing LOE by ~10% since 2022 and lowering maintenance capex to <$20/boe.

These low-capex assets benefit from established producer contracts and firm transportation, providing predictable cash to service corporate debt and support the partnership’s investment-grade credit profile (S&P BBB-/Stable as of 12/31/2025).

South Texas Gathering Systems

South Texas Gathering Systems are mature cash cows within Western Midstream Partners, generating steady adjusted EBITDA—about $110–125 million annually in 2024—while needing little capex.

These systems serve stabilized production areas, yielding low-volatility cash flows (estimated free cash flow stability ±3% year-over-year), and support the MLPs distribution framework.

O&M optimization cut unit operating costs ~12% since 2021, improving margins on legacy pipelines and boosting contribution to partnership cash returns.

- 2024 adj. EBITDA: ~$110–125M

- Capex need: minimal; maintenance-focused

- Cash flow volatility: ~±3% YoY

- O&M cost reduction since 2021: ~12%

- Role: supports MLP distribution framework

Fee-Based Contract Portfolio

The company’s contract mix — 97% of gas and 100% of oil/water throughput under fee-based agreements — functions as a Cash Cow by locking in stable fee revenue regardless of commodity price swings.

That fee-based model keeps revenue steady as basins mature, letting Western Midstream sustain a high distribution yield, which was about 9.0% at year-end 2025, and fund its capital return framework and selective M&A.

- 97% gas fee-based; 100% oil/water fee-based

- Revenue insulated from commodity prices

- Distribution yield ~9.0% at end-2025

- Supports capital returns and M&A

Western Midstream: Cash-Cow Systems Deliver ~9% Yield, High Margins & Stable FCF

Western Midstream’s DJ Basin, Rocky Mountain, Marcellus and South Texas systems are Cash Cows: high fee-based coverage (97% gas, 100% oil/water), strong margins (DJ ~58% EBITDA 2025), low growth capex (DJ ~$30m, Marcellus <$20/boe), and stable free cash (Occidental deal locks ~$450m/year); distribution yield ~9.0% end-2025.

| Asset | 2024–25 EBITDA | Capex | Notes |

|---|---|---|---|

| DJ Basin | high, ~58% margin | ~$30m/yr | Occidental ~$450m/yr |

| Rocky Mtn | $220–240m | low | mid-30s% margin |

| Marcellus | $120–140m FCF | <$20/boe | 350–420 MMcf/d net |

| South Texas | $110–125m | minimal | ±3% cash volatility |

What You’re Viewing Is Included

Western Midstream Partners BCG Matrix

The BCG Matrix preview you're viewing is the exact final document you'll receive after purchase—no watermarks, no demo text, just a fully formatted strategic analysis of Western Midstream Partners ready for presentation and decision-making.