Western Union Porter's Five Forces Analysis

From Overview to Strategy Blueprint

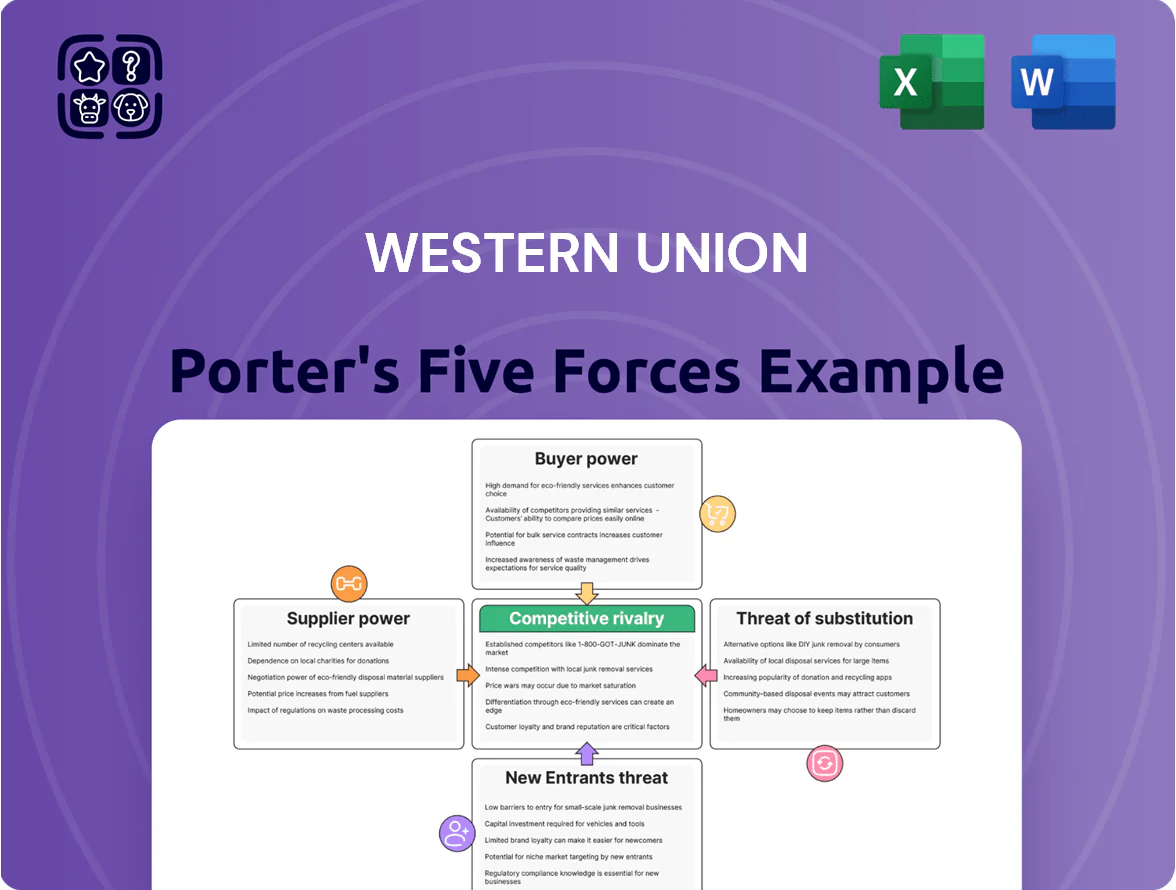

Western Union faces moderate buyer power and substitution risk from fintech and digital wallets, while regulatory complexity and global agent networks shape supplier and rivalry dynamics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Western Union’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Retail Agent Network Partners

Western Union depends on ~500,000 third-party agent locations globally (2025), including post offices, banks, and retail outlets, to serve cash transactions for the unbanked.

Large retail chains wield negotiation power—able to switch to MoneyGram or Ria—forcing WU to offer higher commissions that squeeze margins.

By end-2025 digital payments rose 8% y/y, slightly lowering agent leverage, but physical points remain vital for ~25% of transfers, so WU must balance commission cuts against footprint risk.

Technology and Cloud Infrastructure Providers

As Western Union finishes its digital-first shift, reliance on cloud providers and niche software vendors has grown; AWS, Microsoft Azure, and Google Cloud together held ~62% global IaaS market share in 2024, increasing supplier influence.

These suppliers deliver real-time transaction engines, security stacks, and mobile hosting that support Western Union’s ~$1.7B annual digital money-transfer volume in 2024.

Switching cloud architectures risks high migration costs and downtime, so bargaining power is moderate despite not absolute control.

Western Union reduces lock-in by running multi-cloud deployments and adding proprietary middleware and APIs to retain portability and control.

Banking and Liquidity Partners

To move funds cross-border, Western Union depends on a complex web of correspondent banks and local liquidity providers that supply settlement rails and cash at 200,000+ payout locations across 200+ countries as of 2025.

Regulatory tightening and bank de-risking since 2018 increased partner leverage on fees and compliance, raising correspondent costs by an estimated mid-single-digit percent for global money transfer firms in 2024.

Western Union counters this by diversifying across jurisdictions and maintaining hundreds of banking relationships and alternative liquidity arrangements to limit single-counterparty exposure and preserve payout coverage.

Compliance and Regulatory Data Vendors

Compliance vendors are indispensable for Western Union because global AML (anti-money laundering) and KYC (know your customer) rules require specialized screening databases and tools; failure risks fines—e.g., 2017–2024 banks paid over $26 billion in AML fines—so WU tolerates little vendor risk.

That low switching tolerance creates a tight market where top vendors charge premiums; industry pricing shows 10–30% annual fee increases for real-time screening and sanctions data in 2023–2024.

- Essential: AML/KYC data prevents licensing loss

- Risk: heavy fines drive low vendor switching

- Market: specialized suppliers command 10–30% price premiums

Telecommunications and Connectivity Providers

- Key risk: single-provider outages halt transactions

- 2024 stat: ~80% market share held by top 2 telcos in some markets

- Mitigation: SLAs, partnerships, traffic prioritization

Suppliers wield leverage—WU offsets costs and outage risks with multi‑cloud, banks & SLAs

Suppliers exert moderate-to-high bargaining power: 500k agents (2025) and 200k payout partners give footprint leverage, cloud providers (AWS/Azure/GCP ~62% IaaS 2024) and AML vendors (10–30% fee rises 2023–24) raise costs, and telco concentration (MTN/Airtel ~80% in Nigeria 2024) risks outages; WU counters with multi-cloud, diversified banking ties, SLAs, and proprietary middleware.

| Item | Metric |

|---|---|

| Agent locations | ~500,000 (2025) |

| Payout partners | 200,000+ (2025) |

| IaaS share | 62% AWS/Azure/GCP (2024) |

| AML vendor inflation | 10–30% (2023–24) |

| Telco conc. | ~80% top2 (Nigeria 2024) |

What is included in the product

Tailored Porter's Five Forces analysis of Western Union, revealing competitive intensity, buyer and supplier power, threat of substitutes and entrants, and strategic levers that protect or erode its remittance-market position.

A concise Porter's Five Forces snapshot for Western Union—clarifies competitive pressures and regulatory risks at a glance, ready to drop into investor decks or strategy memos.

Customers Bargaining Power

High Price Sensitivity in Remittance Corridors

Migrant workers—Western Union’s core customers—are highly price sensitive to fees and FX margins; in 2024 remittance flows hit $715 billion globally, with US-to-Mexico and Europe-to-India among the largest corridors.

By 2025 realtime price-comparison sites show spreads across providers; a 1% lower margin can shift millions in monthly volume, forcing WU to match rates to retain customers.

Low Switching Costs for Digital Users

With mobile finance apps maturing, switching from Western Union to a digital-first rival takes minutes—download, ID check, and a transfer—often boosted by first-time-free offers; in 2024, global remittance app downloads rose 18% and promo-driven activations climbed 22%. This near-zero friction forces Western Union to compete on UX and speed, not inertia, as brand loyalty yields to immediate utility and lower fees, squeezing margins on core transfer volumes.

Demand for Integrated Financial Ecosystems

Modern consumers now want integrated wallets, bill pay, and debit-card features alongside transfers; 2024 surveys show 62% of cross-border remitters prefer bundled financial services, boosting customer leverage over product roadmaps.

If Western Union lags, users will shift to neobanks—Chime, Revolut, Wise—where cross-border transfers are secondary; Wise grew to 10.2M active customers by 2024, illustrating migration risk.

That pressure forces Western Union to raise R&D spending—management increased tech investment to $280M in FY2023—to build a holistic ecosystem or lose share to digital-first rivals.

Influence of Small and Medium Enterprises

Western Union’s B2B segment faces high customer bargaining power: SMEs executing large monthly flows (often $100k–$5M) can push for bespoke FX margins and fee cuts by shifting payroll or supplier payments to commercial FX brokers.

These firms’ high lifetime value—commercial remittances made up ~18% of global revenue in 2024 for major money-transfer providers—gives SMEs leverage over SLAs and pricing.

Western Union counters with dedicated account managers, bespoke APIs, and tiered digital pricing to retain clients and protect margins.

- SME flows: $100k–$5M+/month

- Commercial remittances ≈18% revenue (2024)

- Leverage: negotiate FX spreads, SLAs

- WU response: account managers, APIs, tiered pricing

Impact of Digital Literacy and Mobile Adoption

As global digital literacy and smartphone adoption rose—smartphone users hit 6.6 billion in 2025—customers shift from costly cash-to-cash to cheaper digital-to-digital transfers, giving them access to fintech rivals that don’t need agents.

Western Union must cannibalize its high-margin retail flows—retail transaction value fell 9% in 2024—to offer lower-cost digital alternatives, shifting bargaining power to tech-savvy customers.

- Smartphone users: 6.6B (2025)

- WU retail value decline: −9% (2024)

- Digital alternatives: many agent-free fintechs

- Power shift: provider → consumer

Customers Demand Low-Fee, Tech-First Transfers—WU Faces R&D Spike to Defend Volume

Customers hold strong bargaining power: price-sensitive remitters (global remittances $715B in 2024) and tech-savvy users (6.6B smartphones in 2025) shift to low-fee apps; SMEs with $100k–$5M+/mo flows (~18% commercial share) demand bespoke FX/SLAs, forcing WU into higher R&D ($280M FY2023) and digital cannibalization to protect volume.

| Metric | Value |

|---|---|

| Global remittances (2024) | $715B |

| Smartphone users (2025) | 6.6B |

| Wise active users (2024) | 10.2M |

| WU tech spend (FY2023) | $280M |

Same Document Delivered

Western Union Porter's Five Forces Analysis

This preview shows the exact Western Union Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples—fully formatted, professionally written, and ready to download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Western Union faces moderate buyer power and substitution risk from fintech and digital wallets, while regulatory complexity and global agent networks shape supplier and rivalry dynamics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Western Union’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Retail Agent Network Partners

Western Union depends on ~500,000 third-party agent locations globally (2025), including post offices, banks, and retail outlets, to serve cash transactions for the unbanked.

Large retail chains wield negotiation power—able to switch to MoneyGram or Ria—forcing WU to offer higher commissions that squeeze margins.

By end-2025 digital payments rose 8% y/y, slightly lowering agent leverage, but physical points remain vital for ~25% of transfers, so WU must balance commission cuts against footprint risk.

Technology and Cloud Infrastructure Providers

As Western Union finishes its digital-first shift, reliance on cloud providers and niche software vendors has grown; AWS, Microsoft Azure, and Google Cloud together held ~62% global IaaS market share in 2024, increasing supplier influence.

These suppliers deliver real-time transaction engines, security stacks, and mobile hosting that support Western Union’s ~$1.7B annual digital money-transfer volume in 2024.

Switching cloud architectures risks high migration costs and downtime, so bargaining power is moderate despite not absolute control.

Western Union reduces lock-in by running multi-cloud deployments and adding proprietary middleware and APIs to retain portability and control.

Banking and Liquidity Partners

To move funds cross-border, Western Union depends on a complex web of correspondent banks and local liquidity providers that supply settlement rails and cash at 200,000+ payout locations across 200+ countries as of 2025.

Regulatory tightening and bank de-risking since 2018 increased partner leverage on fees and compliance, raising correspondent costs by an estimated mid-single-digit percent for global money transfer firms in 2024.

Western Union counters this by diversifying across jurisdictions and maintaining hundreds of banking relationships and alternative liquidity arrangements to limit single-counterparty exposure and preserve payout coverage.

Compliance and Regulatory Data Vendors

Compliance vendors are indispensable for Western Union because global AML (anti-money laundering) and KYC (know your customer) rules require specialized screening databases and tools; failure risks fines—e.g., 2017–2024 banks paid over $26 billion in AML fines—so WU tolerates little vendor risk.

That low switching tolerance creates a tight market where top vendors charge premiums; industry pricing shows 10–30% annual fee increases for real-time screening and sanctions data in 2023–2024.

- Essential: AML/KYC data prevents licensing loss

- Risk: heavy fines drive low vendor switching

- Market: specialized suppliers command 10–30% price premiums

Telecommunications and Connectivity Providers

- Key risk: single-provider outages halt transactions

- 2024 stat: ~80% market share held by top 2 telcos in some markets

- Mitigation: SLAs, partnerships, traffic prioritization

Suppliers wield leverage—WU offsets costs and outage risks with multi‑cloud, banks & SLAs

Suppliers exert moderate-to-high bargaining power: 500k agents (2025) and 200k payout partners give footprint leverage, cloud providers (AWS/Azure/GCP ~62% IaaS 2024) and AML vendors (10–30% fee rises 2023–24) raise costs, and telco concentration (MTN/Airtel ~80% in Nigeria 2024) risks outages; WU counters with multi-cloud, diversified banking ties, SLAs, and proprietary middleware.

| Item | Metric |

|---|---|

| Agent locations | ~500,000 (2025) |

| Payout partners | 200,000+ (2025) |

| IaaS share | 62% AWS/Azure/GCP (2024) |

| AML vendor inflation | 10–30% (2023–24) |

| Telco conc. | ~80% top2 (Nigeria 2024) |

What is included in the product

Tailored Porter's Five Forces analysis of Western Union, revealing competitive intensity, buyer and supplier power, threat of substitutes and entrants, and strategic levers that protect or erode its remittance-market position.

A concise Porter's Five Forces snapshot for Western Union—clarifies competitive pressures and regulatory risks at a glance, ready to drop into investor decks or strategy memos.

Customers Bargaining Power

High Price Sensitivity in Remittance Corridors

Migrant workers—Western Union’s core customers—are highly price sensitive to fees and FX margins; in 2024 remittance flows hit $715 billion globally, with US-to-Mexico and Europe-to-India among the largest corridors.

By 2025 realtime price-comparison sites show spreads across providers; a 1% lower margin can shift millions in monthly volume, forcing WU to match rates to retain customers.

Low Switching Costs for Digital Users

With mobile finance apps maturing, switching from Western Union to a digital-first rival takes minutes—download, ID check, and a transfer—often boosted by first-time-free offers; in 2024, global remittance app downloads rose 18% and promo-driven activations climbed 22%. This near-zero friction forces Western Union to compete on UX and speed, not inertia, as brand loyalty yields to immediate utility and lower fees, squeezing margins on core transfer volumes.

Demand for Integrated Financial Ecosystems

Modern consumers now want integrated wallets, bill pay, and debit-card features alongside transfers; 2024 surveys show 62% of cross-border remitters prefer bundled financial services, boosting customer leverage over product roadmaps.

If Western Union lags, users will shift to neobanks—Chime, Revolut, Wise—where cross-border transfers are secondary; Wise grew to 10.2M active customers by 2024, illustrating migration risk.

That pressure forces Western Union to raise R&D spending—management increased tech investment to $280M in FY2023—to build a holistic ecosystem or lose share to digital-first rivals.

Influence of Small and Medium Enterprises

Western Union’s B2B segment faces high customer bargaining power: SMEs executing large monthly flows (often $100k–$5M) can push for bespoke FX margins and fee cuts by shifting payroll or supplier payments to commercial FX brokers.

These firms’ high lifetime value—commercial remittances made up ~18% of global revenue in 2024 for major money-transfer providers—gives SMEs leverage over SLAs and pricing.

Western Union counters with dedicated account managers, bespoke APIs, and tiered digital pricing to retain clients and protect margins.

- SME flows: $100k–$5M+/month

- Commercial remittances ≈18% revenue (2024)

- Leverage: negotiate FX spreads, SLAs

- WU response: account managers, APIs, tiered pricing

Impact of Digital Literacy and Mobile Adoption

As global digital literacy and smartphone adoption rose—smartphone users hit 6.6 billion in 2025—customers shift from costly cash-to-cash to cheaper digital-to-digital transfers, giving them access to fintech rivals that don’t need agents.

Western Union must cannibalize its high-margin retail flows—retail transaction value fell 9% in 2024—to offer lower-cost digital alternatives, shifting bargaining power to tech-savvy customers.

- Smartphone users: 6.6B (2025)

- WU retail value decline: −9% (2024)

- Digital alternatives: many agent-free fintechs

- Power shift: provider → consumer

Customers Demand Low-Fee, Tech-First Transfers—WU Faces R&D Spike to Defend Volume

Customers hold strong bargaining power: price-sensitive remitters (global remittances $715B in 2024) and tech-savvy users (6.6B smartphones in 2025) shift to low-fee apps; SMEs with $100k–$5M+/mo flows (~18% commercial share) demand bespoke FX/SLAs, forcing WU into higher R&D ($280M FY2023) and digital cannibalization to protect volume.

| Metric | Value |

|---|---|

| Global remittances (2024) | $715B |

| Smartphone users (2025) | 6.6B |

| Wise active users (2024) | 10.2M |

| WU tech spend (FY2023) | $280M |

Same Document Delivered

Western Union Porter's Five Forces Analysis

This preview shows the exact Western Union Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples—fully formatted, professionally written, and ready to download and use the moment you buy.