West Fraser Boston Consulting Group Matrix

Download Your Competitive Advantage

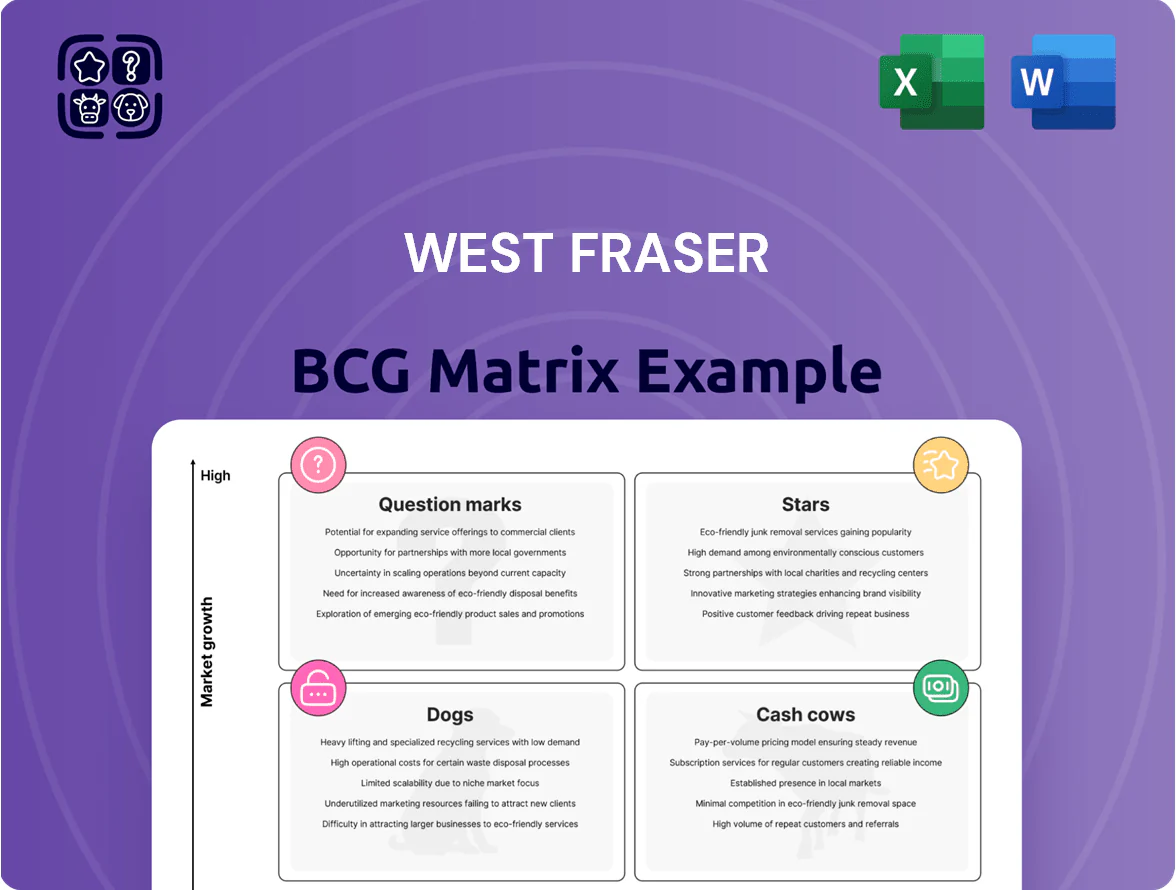

West Fraser’s BCG Matrix preview highlights how its core segments—lumber, plywood, and pulp—stack up across market growth and relative share, revealing where cash generation and reinvestment should focus; however, this snapshot is only the start. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and editable Word and Excel files that turn insight into action and save you hours of analysis.

Stars

North American OSB Market Leadership

West Fraser holds leading North American OSB market share, about 26% in 2024, and demand stayed strong into 2025 with US housing starts averaging ~1.4M annualized through Q3 2025, supporting sustained panel consumption.

OSB needs heavy capital: West Fraser invested C$450M in OSB capacity and tech upgrades in 2024–25 to cut costs and raise output by ~400k mmbf/year.

High share plus rising green building rules and a 2025 OSB price premium near US$25/mbf over plywood make OSB West Fraser’s main growth engine.

Mass Timber and CLT Expansion

Mass timber and Cross-Laminated Timber (CLT) demand is rising with global mass timber market projected to reach US$11.3B by 2030 (CAGR ~10.2%); West Fraser has allocated roughly CAD 250M since 2021 into CLT and engineered-wood capacity to seize commercial-build share.

These divisions burn significant cash for R&D and specialized plants—CapEx for engineered-wood rose to CAD 180M in FY2024—pressuring near-term margins but positioning West Fraser as a leader in high-density sustainable architecture.

Southern United States Production Capacity

Strategic acquisitions and mill modernizations in the Southern US have placed West Fraser in a high-growth, high-market-share region; the company reported US lumber shipments of ~2.1 billion board feet in 2024 from Southern mills, up 8% year-over-year.

Proximity to 60+ million acres of private timberlands and rising Sun Belt housing starts (1.3M in 2024) gives West Fraser a cost and supply edge that demands ongoing capital reinvestment—capital expenditures for 2024: CAD 515 million.

High-volume, high-demand dynamics make this segment a lead performer in the corporate portfolio, contributing roughly 35% of consolidated operating income in 2024 and justifying continued capacity upgrades.

Engineered Wood Product Innovation

Engineered wood products for industrial use are growing ~12% CAGR 2021–25, displacing steel/concrete in mid-rise and modular projects; West Fraser (TSX: WFG) held an estimated 18–22% share of this niche by 2025 by using integrated mills and FSC/PEFC certifications.

Ongoing marketing and distribution push needed as cross-laminated timber (CLT) and mass timber makers raised global capacity ~30% in 2024; West Fraser must sustain premium placement to defend margins.

- 12% CAGR 2021–25

- 18–22% market share (2025)

- 30% global capacity increase (2024)

- FSC/PEFC certified supply chain

Sustainable Structural Panels

West Fraser’s eco-certified structural panels sit in the Stars quadrant: rising demand from tighter 2026 builder regs pushes global market growth ~8–10% CAGR and West Fraser’s estimated market share >25% in North America, driven by 7.2M hectares of forest tenure and FSC/PEFC validations.

These panels are high-growth and capital-intensive; West Fraser increased 2024–25 capex to ~US$800M to expand OSB/MDF lines and must keep investing to meet ESG (Scope 1–3) compliance for exports to EU/UK.

- Market growth: ~8–10% CAGR to 2028

- Company share: >25% North America

- Forest tenure: 7.2M hectares

- Capex 2024–25: ~US$800M

- Certifications: FSC, PEFC; ESG targets ongoing

West Fraser: OSB/Engineered-Wood Powerhouse—>25% NA OSB, 8–12% growth, $800M capex

West Fraser’s Stars: OSB/engineered-wood >25% NA share (2025), market growth ~8–10% CAGR to 2028, 2024–25 capex ~US$800M, contributed ~35% operating income (2024); engineered-wood CAGR ~12% (2021–25), CLT/MLT investments ~CAD250M since 2021, forest tenure 7.2M ha, certifications FSC/PEFC.

| Metric | Value |

|---|---|

| NA share (OSB) | >25% (2025) |

| Market CAGR | 8–10% to 2028 |

| CapEx 2024–25 | ~US$800M |

What is included in the product

Comprehensive BCG Matrix for West Fraser outlining Stars, Cash Cows, Question Marks, and Dogs with strategic investment recommendations.

One-page BCG Matrix placing West Fraser business units in quadrants for quick strategic clarity.

Cash Cows

Canadian SPF Lumber Operations

Canadian SPF (spruce-pine-fir) lumber is a cash cow for West Fraser: the company held roughly 18% of North American SPF capacity in 2024 and ran mills at ~88% utilization, producing stable EBITDA margins near 22% in FY2024.

Growth has plateaued, so low incremental marketing spend preserves free cash flow—West Fraser generated C$1.1bn FCF in FY2024, largely from lumber operations.

That cash funds expansion in bio-products—investments of C$300m+ since 2022—and supports C$0.75 per-share dividends and opportunistic buybacks.

Southern Yellow Pine Lumber

Southern Yellow Pine lumber is a high-market-share product for West Fraser in a mature North American building market, accounting for roughly 12–15% of company shipments in 2024 and supporting stable pricing versus soft commodity grades.

Mill efficiency and scale push EBITDA margins near 18–22% in 2024 for this segment, producing steady cash flow that cushions commodity swings.

West Fraser used proceeds from Southern Yellow Pine operations to pay down about $350m of net debt in 2024 and to fund the $200m strategic veneer and engineered-wood acquisition closed in Nov 2024.

Wood Chip and Residual Supply

West Fraser’s wood chip and residual supply is a low-growth, high-stability cash cow: in 2024 wood products residuals generated roughly CAD 420m in segment EBITDA-contribution-equivalent, with chip volumes ~4.1 million green tonnes—making West Fraser a primary supplier to pulp and energy markets.

Little incremental capex is needed beyond existing sawmills; residual recovery adds ~5–8% margin uplift per mill and delivered steady free cash flow, funding capex and dividends—chips are milked to support higher-growth units.

Established Plywood Manufacturing

West Fraser’s established plywood division operates in a mature North American market with high barriers to entry and few large competitors; in 2024 plywood revenue was about US$1.1bn, maintaining steady market share and ~12% operating margin.

Decades of process optimization let the unit generate free cash flow exceeding capex needs, producing roughly US$120m FCF in 2024 and stabilizing West Fraser’s balance sheet versus volatile specialty wood investments.

- 2024 plywood revenue ~US$1.1bn

- Operating margin ~12%

- 2024 free cash flow ~US$120m

- Mature market, high entry barriers

- Provides balance-sheet stability

Integrated Forest Management Services

Integrated Forest Management Services at West Fraser is a cash cow: mature operations cover over 6.5 million hectares of tenure (Canada and US) with ~30% company-market share in key regions, delivering low-cost fiber and stable margins around 12–15% EBITDA in 2024.

Timberland growth is constrained by zoning and policy, but operational efficiency—harvest productivity gains ~5% since 2020—provides predictable cash flow that funds R&D on engineered wood and waste-to-energy projects.

- 6.5M ha tenure; ~30% regional share

- 12–15% EBITDA (2024)

- 5% productivity gain since 2020

- Stable cash funds R&D for engineered wood

West Fraser's cash cows drive C$1.1B FCF, C$350M debt paydown and growth capex

West Fraser’s cash cows—Canadian SPF, Southern Yellow Pine, wood chips/residuals, plywood, and forest management—generated steady margins (SPF ~22%, SYP 18–22%, chips/residuals eq. CAD420m EBITDA, plywood ~12%, timberland 12–15%) and funded C$1.1bn FCF in FY2024, C$300m+ bio-products capex since 2022, C$350m net-debt paydown and C$0.75/sh dividends.

| Unit | 2024 Key |

|---|---|

| SPF | 18% NA capacity, 88% util, 22% EBITDA |

| SYP | 12–15% shipments, 18–22% EBITDA |

| Chips | CAD420m equiv EBITDA, 4.1Mt |

| Plywood | US$1.1bn rev, 12% op margin |

| Timberland | 6.5M ha, 12–15% EBITDA |

What You See Is What You Get

West Fraser BCG Matrix

The file you're previewing on this page is the exact West Fraser BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the final, fully formatted analysis ready for presentation or integration into your planning documents.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

West Fraser’s BCG Matrix preview highlights how its core segments—lumber, plywood, and pulp—stack up across market growth and relative share, revealing where cash generation and reinvestment should focus; however, this snapshot is only the start. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and editable Word and Excel files that turn insight into action and save you hours of analysis.

Stars

North American OSB Market Leadership

West Fraser holds leading North American OSB market share, about 26% in 2024, and demand stayed strong into 2025 with US housing starts averaging ~1.4M annualized through Q3 2025, supporting sustained panel consumption.

OSB needs heavy capital: West Fraser invested C$450M in OSB capacity and tech upgrades in 2024–25 to cut costs and raise output by ~400k mmbf/year.

High share plus rising green building rules and a 2025 OSB price premium near US$25/mbf over plywood make OSB West Fraser’s main growth engine.

Mass Timber and CLT Expansion

Mass timber and Cross-Laminated Timber (CLT) demand is rising with global mass timber market projected to reach US$11.3B by 2030 (CAGR ~10.2%); West Fraser has allocated roughly CAD 250M since 2021 into CLT and engineered-wood capacity to seize commercial-build share.

These divisions burn significant cash for R&D and specialized plants—CapEx for engineered-wood rose to CAD 180M in FY2024—pressuring near-term margins but positioning West Fraser as a leader in high-density sustainable architecture.

Southern United States Production Capacity

Strategic acquisitions and mill modernizations in the Southern US have placed West Fraser in a high-growth, high-market-share region; the company reported US lumber shipments of ~2.1 billion board feet in 2024 from Southern mills, up 8% year-over-year.

Proximity to 60+ million acres of private timberlands and rising Sun Belt housing starts (1.3M in 2024) gives West Fraser a cost and supply edge that demands ongoing capital reinvestment—capital expenditures for 2024: CAD 515 million.

High-volume, high-demand dynamics make this segment a lead performer in the corporate portfolio, contributing roughly 35% of consolidated operating income in 2024 and justifying continued capacity upgrades.

Engineered Wood Product Innovation

Engineered wood products for industrial use are growing ~12% CAGR 2021–25, displacing steel/concrete in mid-rise and modular projects; West Fraser (TSX: WFG) held an estimated 18–22% share of this niche by 2025 by using integrated mills and FSC/PEFC certifications.

Ongoing marketing and distribution push needed as cross-laminated timber (CLT) and mass timber makers raised global capacity ~30% in 2024; West Fraser must sustain premium placement to defend margins.

- 12% CAGR 2021–25

- 18–22% market share (2025)

- 30% global capacity increase (2024)

- FSC/PEFC certified supply chain

Sustainable Structural Panels

West Fraser’s eco-certified structural panels sit in the Stars quadrant: rising demand from tighter 2026 builder regs pushes global market growth ~8–10% CAGR and West Fraser’s estimated market share >25% in North America, driven by 7.2M hectares of forest tenure and FSC/PEFC validations.

These panels are high-growth and capital-intensive; West Fraser increased 2024–25 capex to ~US$800M to expand OSB/MDF lines and must keep investing to meet ESG (Scope 1–3) compliance for exports to EU/UK.

- Market growth: ~8–10% CAGR to 2028

- Company share: >25% North America

- Forest tenure: 7.2M hectares

- Capex 2024–25: ~US$800M

- Certifications: FSC, PEFC; ESG targets ongoing

West Fraser: OSB/Engineered-Wood Powerhouse—>25% NA OSB, 8–12% growth, $800M capex

West Fraser’s Stars: OSB/engineered-wood >25% NA share (2025), market growth ~8–10% CAGR to 2028, 2024–25 capex ~US$800M, contributed ~35% operating income (2024); engineered-wood CAGR ~12% (2021–25), CLT/MLT investments ~CAD250M since 2021, forest tenure 7.2M ha, certifications FSC/PEFC.

| Metric | Value |

|---|---|

| NA share (OSB) | >25% (2025) |

| Market CAGR | 8–10% to 2028 |

| CapEx 2024–25 | ~US$800M |

What is included in the product

Comprehensive BCG Matrix for West Fraser outlining Stars, Cash Cows, Question Marks, and Dogs with strategic investment recommendations.

One-page BCG Matrix placing West Fraser business units in quadrants for quick strategic clarity.

Cash Cows

Canadian SPF Lumber Operations

Canadian SPF (spruce-pine-fir) lumber is a cash cow for West Fraser: the company held roughly 18% of North American SPF capacity in 2024 and ran mills at ~88% utilization, producing stable EBITDA margins near 22% in FY2024.

Growth has plateaued, so low incremental marketing spend preserves free cash flow—West Fraser generated C$1.1bn FCF in FY2024, largely from lumber operations.

That cash funds expansion in bio-products—investments of C$300m+ since 2022—and supports C$0.75 per-share dividends and opportunistic buybacks.

Southern Yellow Pine Lumber

Southern Yellow Pine lumber is a high-market-share product for West Fraser in a mature North American building market, accounting for roughly 12–15% of company shipments in 2024 and supporting stable pricing versus soft commodity grades.

Mill efficiency and scale push EBITDA margins near 18–22% in 2024 for this segment, producing steady cash flow that cushions commodity swings.

West Fraser used proceeds from Southern Yellow Pine operations to pay down about $350m of net debt in 2024 and to fund the $200m strategic veneer and engineered-wood acquisition closed in Nov 2024.

Wood Chip and Residual Supply

West Fraser’s wood chip and residual supply is a low-growth, high-stability cash cow: in 2024 wood products residuals generated roughly CAD 420m in segment EBITDA-contribution-equivalent, with chip volumes ~4.1 million green tonnes—making West Fraser a primary supplier to pulp and energy markets.

Little incremental capex is needed beyond existing sawmills; residual recovery adds ~5–8% margin uplift per mill and delivered steady free cash flow, funding capex and dividends—chips are milked to support higher-growth units.

Established Plywood Manufacturing

West Fraser’s established plywood division operates in a mature North American market with high barriers to entry and few large competitors; in 2024 plywood revenue was about US$1.1bn, maintaining steady market share and ~12% operating margin.

Decades of process optimization let the unit generate free cash flow exceeding capex needs, producing roughly US$120m FCF in 2024 and stabilizing West Fraser’s balance sheet versus volatile specialty wood investments.

- 2024 plywood revenue ~US$1.1bn

- Operating margin ~12%

- 2024 free cash flow ~US$120m

- Mature market, high entry barriers

- Provides balance-sheet stability

Integrated Forest Management Services

Integrated Forest Management Services at West Fraser is a cash cow: mature operations cover over 6.5 million hectares of tenure (Canada and US) with ~30% company-market share in key regions, delivering low-cost fiber and stable margins around 12–15% EBITDA in 2024.

Timberland growth is constrained by zoning and policy, but operational efficiency—harvest productivity gains ~5% since 2020—provides predictable cash flow that funds R&D on engineered wood and waste-to-energy projects.

- 6.5M ha tenure; ~30% regional share

- 12–15% EBITDA (2024)

- 5% productivity gain since 2020

- Stable cash funds R&D for engineered wood

West Fraser's cash cows drive C$1.1B FCF, C$350M debt paydown and growth capex

West Fraser’s cash cows—Canadian SPF, Southern Yellow Pine, wood chips/residuals, plywood, and forest management—generated steady margins (SPF ~22%, SYP 18–22%, chips/residuals eq. CAD420m EBITDA, plywood ~12%, timberland 12–15%) and funded C$1.1bn FCF in FY2024, C$300m+ bio-products capex since 2022, C$350m net-debt paydown and C$0.75/sh dividends.

| Unit | 2024 Key |

|---|---|

| SPF | 18% NA capacity, 88% util, 22% EBITDA |

| SYP | 12–15% shipments, 18–22% EBITDA |

| Chips | CAD420m equiv EBITDA, 4.1Mt |

| Plywood | US$1.1bn rev, 12% op margin |

| Timberland | 6.5M ha, 12–15% EBITDA |

What You See Is What You Get

West Fraser BCG Matrix

The file you're previewing on this page is the exact West Fraser BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the final, fully formatted analysis ready for presentation or integration into your planning documents.