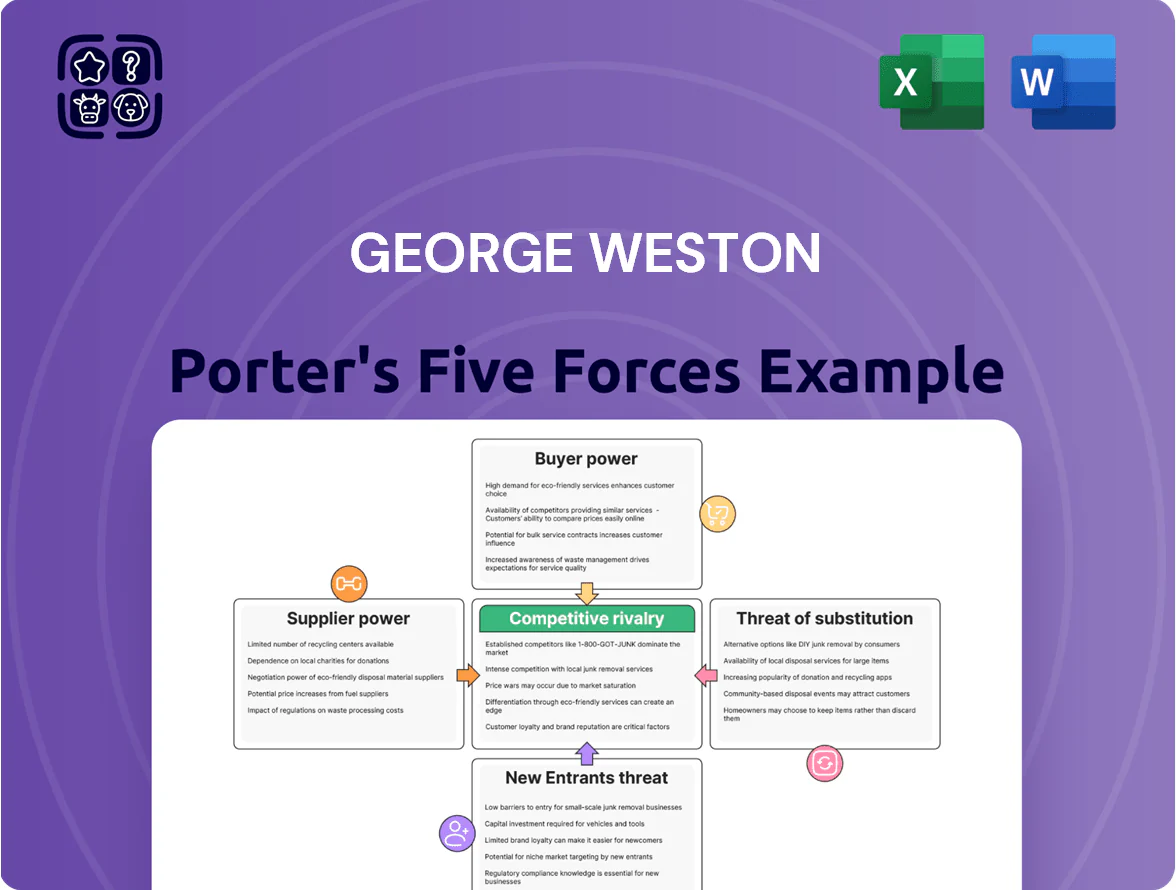

George Weston Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

George Weston faces moderate supplier power and high buyer sensitivity in grocery retail, balanced by strong brand scale but rising private-label and online substitutes; barriers to entry are significant yet niche disruptors pose localized threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore George Weston’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated Multi-National Brand Power

Vertical Integration through Private Labels

George Weston reduces supplier power by scaling President's Choice and No Name private labels—these accounted for about 28% of Loblaw grocery sales in FY2024, giving Weston direct sourcing control and higher margins.

Logistics and Input Cost Volatility

Suppliers of fuel and staples hold moderate power over George Weston because these inputs are essential; in 2025 fuel added ~4–6% to operating costs and wheat/soy price spikes raised raw material costs by ~8% year-over-year.

Global supply-chain disruption and climate-driven crop shifts let specialized suppliers pass costs through, with regional yield drops up to 12% in 2024–25.

George Weston leverages scale and long-term contracts covering ~60% of purchases, cutting short-term volatility, but systemic food-supply inflation (CPI food +9% in 2024) still pressures margins.

Real Estate Construction and Maintenance Costs

Choice Properties REIT makes George Weston a major buyer of construction and property management; supplier leverage rises when labour and material supply tighten in Canada.

In 2024 Canada construction wage growth hit about 4.5% and material costs rose ~6% year-over-year, while Bank of Canada policy kept mortgage-linked rates elevated, all boosting contractor pricing power.

- Large buyer but concentrated supplier risk

- 2024: construction wages +4.5%, materials +6%

- High rates raise financing costs for projects

- Specialized contractors gain pricing leverage

Regulatory Oversight on Supplier Relations

The Canadian Grocery Code of Conduct, strengthened by 2025, standardizes retailer-supplier terms and bars arbitrary fees or retroactive price cuts, limiting practices once used by major chains like Loblaw.

By reducing unilateral cost-shifting, the code shifts bargaining power modestly toward suppliers; small/medium suppliers (≈75% of Canadian food producers) see lower dispute rates and improved payment terms.

Weston/Loblaw scale tempers supplier power amid inflation, crop shocks and Grocery Code

Suppliers hold moderate power: national brands drove ~38% of Loblaw 2024 food sales, but Weston’s private labels (28% of sales in FY2024) and Weston’s C$50bn+ scale cut supplier margins; long-term contracts cover ~60% purchases. 2024–25 shocks (food CPI +9%, fuel +4–6% operating cost, regional crop yield drops up to 12%) raise pass-through risk; 2025 Grocery Code eases small supplier bargaining.

| Metric | Value |

|---|---|

| National brand share (Loblaw 2024) | 38% |

| Private-label share (Weston FY2024) | 28% |

| Scale (Weston retail sales 2024) | C$50bn+ |

| Contracts covering purchases | 60% |

| Food CPI (2024) | +9% |

| Fuel impact on costs (2025) | +4–6% |

| Regional crop yield drops (2024–25) | up to 12% |

What is included in the product

Tailored Porter's Five Forces analysis for George Weston that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive trends affecting its market position.

Concise Porter's Five Forces snapshot for George Weston—quickly pinpoint competitive pressures and strategic levers to ease decision-making under shifting market conditions.

Customers Bargaining Power

High Price Sensitivity in Grocery Retail

Canadian consumers in 2025 remain value-driven after repeated inflation, so price sensitivity is high and customer bargaining power strong.

Shoppers switch weekly based on flyers and promos; grocery price promotions rose 8% year-over-year in 2024, boosting switch rates.

George Weston must keep investing in No Frills—which accounted for about 20% of Loblaw’s 2024 banner sales—to retain cost-focused buyers.

Loyalty Program Ecosystem Integration

The PC Optimum loyalty program raises switching costs by bundling personalized discounts and points redeemable across Loblaw grocery, Shoppers Drug Mart pharmacy, and Mobil gas, creating a closed-loop ecosystem that weakens customer bargaining power.

In 2024 Loblaw reported over 23 million active PC Optimum members, and personalized offers drove a reported 4-6% uplift in basket size, helping sustain footfall despite price competition.

PC Optimum’s data-driven targeting improves demand prediction and retention, so even when rivals cut prices George Weston sustains volume and margins by steering repeat purchases.

Growth of E-commerce and Comparison Shopping

The rise of e-commerce and price‑comparison apps lets shoppers find lowest prices in minutes, raising customer bargaining power and forcing George Weston to keep price parity across channels.

Customers skip store visits, so Weston faces slimmer margins; online grocery price transparency grew 28% in Canada 2023–24, increasing price sensitivity.

Weston’s investments in PC Express and home delivery—PC Express had ~1,300 pickup sites by end‑2024—aim to match convenience and retain customers.

Demand for Health and Sustainability Transparency

- 72% of Canadian shoppers consider sustainability

- 2024 organic sales growth: Loblaw +8%

- Risk: brand erosion, share loss to specialty retailers

- Action: prioritize organic, local, ethical sourcing

Pharmacy and Healthcare Stickiness

Customer power in the Shoppers Drug Mart segment is muted versus grocery because prescriptions are essential; in 2024 prescriptions accounted for ~45% of SDM sales, raising switching costs through regulated dispensing and professional services.

Regulation and in-store pharmacist care lock in customers, but online pharmacies and mail-order grew ~12% YoY in 2024, creating a rising alternative the company must counter.

- Prescriptions ~45% of SDM sales (2024)

- Online/mail-order pharmacy growth ~12% YoY (2024)

- Higher switching costs via regulated dispensing and pharmacist trust

High customer price power: promos, online transparency rise despite loyalty and Rx stickiness

Customer bargaining power is high: price sensitivity rose after inflation, promotions up 8% in 2024, and online price transparency +28% (2023–24) boost switching. Loyalty (23m PC Optimum members in 2024) and No Frills (≈20% of Loblaw banner sales, 2024) curb power; SDM prescriptions (~45% of sales, 2024) raise switching costs, while online pharmacy growth ~12% YoY adds pressure.

| Metric | 2024 |

|---|---|

| PC Optimum members | 23m+ |

| Promo growth | +8% YoY |

| Online price transparency | +28% (2023–24) |

| No Frills share | ~20% banner sales |

| SDM prescriptions | ~45% sales |

| Online pharmacy growth | ~12% YoY |

Preview the Actual Deliverable

George Weston Porter's Five Forces Analysis

This preview shows the exact George Weston Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples. The document displayed is the fully formatted, ready-to-use file you’ll be able to download the moment you buy. It contains the complete competitive assessment, implications for strategy, and concise conclusions tailored for decision-makers. What you see here is precisely what you’ll get.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

George Weston faces moderate supplier power and high buyer sensitivity in grocery retail, balanced by strong brand scale but rising private-label and online substitutes; barriers to entry are significant yet niche disruptors pose localized threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore George Weston’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated Multi-National Brand Power

Vertical Integration through Private Labels

George Weston reduces supplier power by scaling President's Choice and No Name private labels—these accounted for about 28% of Loblaw grocery sales in FY2024, giving Weston direct sourcing control and higher margins.

Logistics and Input Cost Volatility

Suppliers of fuel and staples hold moderate power over George Weston because these inputs are essential; in 2025 fuel added ~4–6% to operating costs and wheat/soy price spikes raised raw material costs by ~8% year-over-year.

Global supply-chain disruption and climate-driven crop shifts let specialized suppliers pass costs through, with regional yield drops up to 12% in 2024–25.

George Weston leverages scale and long-term contracts covering ~60% of purchases, cutting short-term volatility, but systemic food-supply inflation (CPI food +9% in 2024) still pressures margins.

Real Estate Construction and Maintenance Costs

Choice Properties REIT makes George Weston a major buyer of construction and property management; supplier leverage rises when labour and material supply tighten in Canada.

In 2024 Canada construction wage growth hit about 4.5% and material costs rose ~6% year-over-year, while Bank of Canada policy kept mortgage-linked rates elevated, all boosting contractor pricing power.

- Large buyer but concentrated supplier risk

- 2024: construction wages +4.5%, materials +6%

- High rates raise financing costs for projects

- Specialized contractors gain pricing leverage

Regulatory Oversight on Supplier Relations

The Canadian Grocery Code of Conduct, strengthened by 2025, standardizes retailer-supplier terms and bars arbitrary fees or retroactive price cuts, limiting practices once used by major chains like Loblaw.

By reducing unilateral cost-shifting, the code shifts bargaining power modestly toward suppliers; small/medium suppliers (≈75% of Canadian food producers) see lower dispute rates and improved payment terms.

Weston/Loblaw scale tempers supplier power amid inflation, crop shocks and Grocery Code

Suppliers hold moderate power: national brands drove ~38% of Loblaw 2024 food sales, but Weston’s private labels (28% of sales in FY2024) and Weston’s C$50bn+ scale cut supplier margins; long-term contracts cover ~60% purchases. 2024–25 shocks (food CPI +9%, fuel +4–6% operating cost, regional crop yield drops up to 12%) raise pass-through risk; 2025 Grocery Code eases small supplier bargaining.

| Metric | Value |

|---|---|

| National brand share (Loblaw 2024) | 38% |

| Private-label share (Weston FY2024) | 28% |

| Scale (Weston retail sales 2024) | C$50bn+ |

| Contracts covering purchases | 60% |

| Food CPI (2024) | +9% |

| Fuel impact on costs (2025) | +4–6% |

| Regional crop yield drops (2024–25) | up to 12% |

What is included in the product

Tailored Porter's Five Forces analysis for George Weston that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive trends affecting its market position.

Concise Porter's Five Forces snapshot for George Weston—quickly pinpoint competitive pressures and strategic levers to ease decision-making under shifting market conditions.

Customers Bargaining Power

High Price Sensitivity in Grocery Retail

Canadian consumers in 2025 remain value-driven after repeated inflation, so price sensitivity is high and customer bargaining power strong.

Shoppers switch weekly based on flyers and promos; grocery price promotions rose 8% year-over-year in 2024, boosting switch rates.

George Weston must keep investing in No Frills—which accounted for about 20% of Loblaw’s 2024 banner sales—to retain cost-focused buyers.

Loyalty Program Ecosystem Integration

The PC Optimum loyalty program raises switching costs by bundling personalized discounts and points redeemable across Loblaw grocery, Shoppers Drug Mart pharmacy, and Mobil gas, creating a closed-loop ecosystem that weakens customer bargaining power.

In 2024 Loblaw reported over 23 million active PC Optimum members, and personalized offers drove a reported 4-6% uplift in basket size, helping sustain footfall despite price competition.

PC Optimum’s data-driven targeting improves demand prediction and retention, so even when rivals cut prices George Weston sustains volume and margins by steering repeat purchases.

Growth of E-commerce and Comparison Shopping

The rise of e-commerce and price‑comparison apps lets shoppers find lowest prices in minutes, raising customer bargaining power and forcing George Weston to keep price parity across channels.

Customers skip store visits, so Weston faces slimmer margins; online grocery price transparency grew 28% in Canada 2023–24, increasing price sensitivity.

Weston’s investments in PC Express and home delivery—PC Express had ~1,300 pickup sites by end‑2024—aim to match convenience and retain customers.

Demand for Health and Sustainability Transparency

- 72% of Canadian shoppers consider sustainability

- 2024 organic sales growth: Loblaw +8%

- Risk: brand erosion, share loss to specialty retailers

- Action: prioritize organic, local, ethical sourcing

Pharmacy and Healthcare Stickiness

Customer power in the Shoppers Drug Mart segment is muted versus grocery because prescriptions are essential; in 2024 prescriptions accounted for ~45% of SDM sales, raising switching costs through regulated dispensing and professional services.

Regulation and in-store pharmacist care lock in customers, but online pharmacies and mail-order grew ~12% YoY in 2024, creating a rising alternative the company must counter.

- Prescriptions ~45% of SDM sales (2024)

- Online/mail-order pharmacy growth ~12% YoY (2024)

- Higher switching costs via regulated dispensing and pharmacist trust

High customer price power: promos, online transparency rise despite loyalty and Rx stickiness

Customer bargaining power is high: price sensitivity rose after inflation, promotions up 8% in 2024, and online price transparency +28% (2023–24) boost switching. Loyalty (23m PC Optimum members in 2024) and No Frills (≈20% of Loblaw banner sales, 2024) curb power; SDM prescriptions (~45% of sales, 2024) raise switching costs, while online pharmacy growth ~12% YoY adds pressure.

| Metric | 2024 |

|---|---|

| PC Optimum members | 23m+ |

| Promo growth | +8% YoY |

| Online price transparency | +28% (2023–24) |

| No Frills share | ~20% banner sales |

| SDM prescriptions | ~45% sales |

| Online pharmacy growth | ~12% YoY |

Preview the Actual Deliverable

George Weston Porter's Five Forces Analysis

This preview shows the exact George Weston Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples. The document displayed is the fully formatted, ready-to-use file you’ll be able to download the moment you buy. It contains the complete competitive assessment, implications for strategy, and concise conclusions tailored for decision-makers. What you see here is precisely what you’ll get.