George Weston SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

George Weston’s diversified footprint—spanning grocery, food processing, and real estate—anchors resilient cashflows, but competitive retail pressures and supply-chain risks test margins and expansion plans.

Our full SWOT analysis unpacks strategic levers, financial context, and operational vulnerabilities with actionable recommendations tailored for investors, advisors, and managers.

Purchase the complete, editable SWOT report (Word + Excel) to convert insights into decisions—plan, pitch, or invest with confidence.

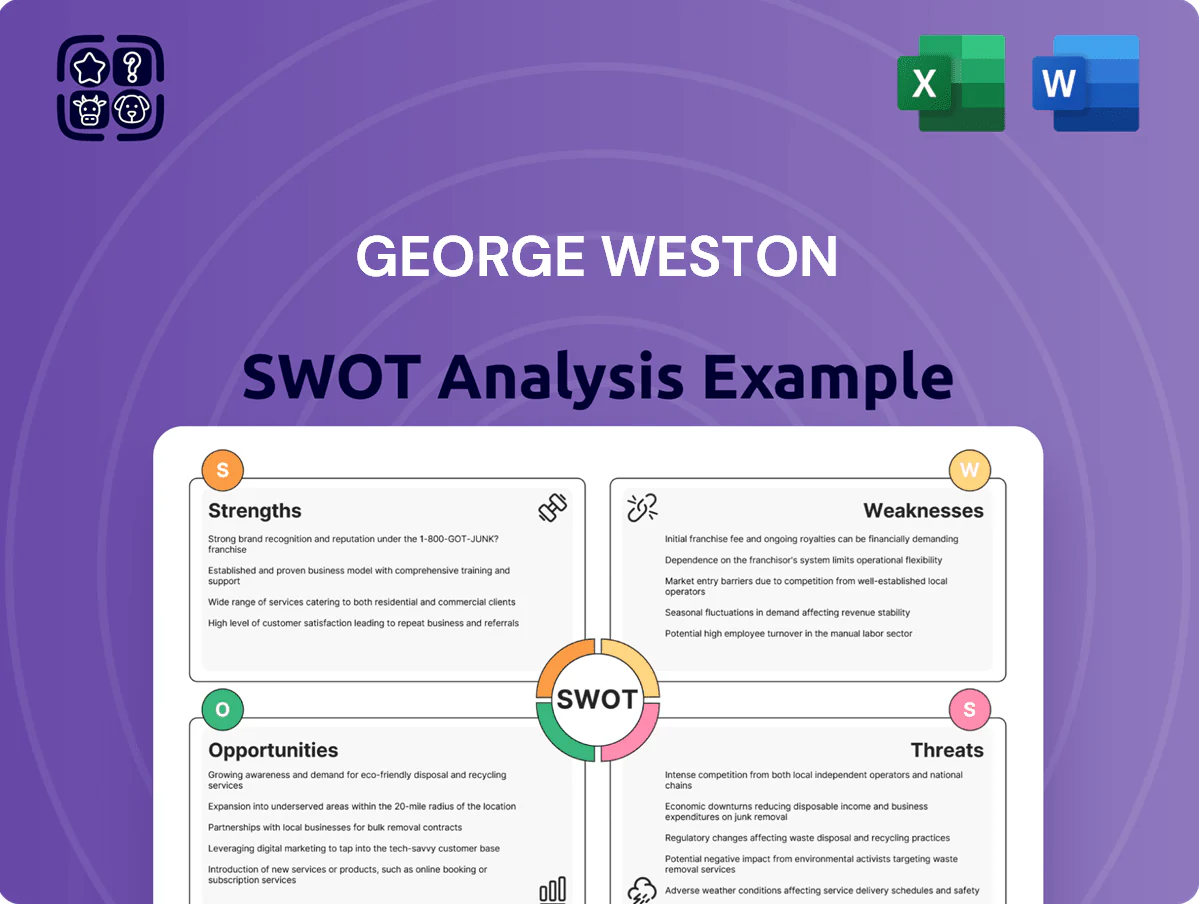

Strengths

Dominant Market Leadership through Loblaw

George Weston holds a 62.5% voting interest in Loblaw Companies Limited, Canada’s largest food and drug retailer with about 1,300 supermarkets and 2,600 pharmacies as of FY2024, giving Weston unmatched scale in procurement and distribution.

That network drove Loblaw to CAD 56.2 billion in 2024 revenue, providing Weston a steady, sizeable cash flow and a cost advantage versus regional rivals through national buying power and logistics.

Strategic Real Estate Integration

Through its 64% stake in Choice Properties REIT (as of Dec 31, 2024), George Weston controls a 2,800+ property portfolio valued at roughly CAD 15.6 billion, many anchored by Loblaw stores, yielding occupancy >98% and stabilized rental income that held up in 2023–24.

Powerful Private Label Brand Equity

George Weston’s private labels, led by President’s Choice and No Name, are among Canada’s most trusted, generating higher gross margins (about 6–8 percentage points above national brands) and driving Loblaws’ 2024 private-label penetration of ~40% of food sales; this boosts profitability while giving value-conscious shoppers cheaper alternatives, deepening loyalty and differentiating the retail mix versus competitors like Walmart and Costco.

Robust PC Optimum Loyalty Ecosystem

The PC Optimum program, with over 23 million members as of Dec 31, 2024, gives George Weston a vast consumer-data asset that fuels targeted marketing and personalized offers across Loblaw grocery, Shoppers Drug Mart pharmacy, and PC Financial services.

That data drives higher basket sizes and frequency—Loblaw reported Q4 2024 same-store sales growth of 3.6%—and creates strong switching costs as members earn and redeem points within the Weston network.

- 23M+ members (Dec 31, 2024)

- Drives personalized promos across grocery, pharmacy, finance

- Supports 3.6% Q4 2024 same-store sales growth (Loblaw)

- High switching cost via cross-network rewards

Resilient Financial Services Segment

- 5M+ PC Optimum members

- 1,500+ retail locations

- Lower acquisition cost vs. big banks

- Mid-single-digit boost to non-grocery revenue (2024)

Weston: Dominant scale—CAD56B Loblaw, 23M members, 40% private-label lift

Weston’s 62.5% stake in Loblaw (≈1,300 supermarkets, 2,600 pharmacies) and CAD56.2B Loblaw 2024 revenue deliver scale, procurement savings, and steady cash flow; Choice Properties (64% stake, ~2,800 properties, CAD15.6B value) supplies >98% occupancy and stable rents; strong private labels (PC, No Name ~40% food penetration) boost margins ~6–8pp; PC Optimum 23M members and PC Financial (5M users) raise basket size and cross-sell.

| Metric | Value (2024) |

|---|---|

| Loblaw revenue | CAD56.2B |

| Supermarkets / Pharmacies | 1,300 / 2,600 |

| PC Optimum members | 23M+ |

| Choice Properties value | CAD15.6B |

| Private-label penetration | ~40% |

What is included in the product

Provides a concise SWOT framework outlining George Weston’s core strengths, operational weaknesses, market opportunities, and external threats to evaluate its strategic position and future prospects.

Provides a concise SWOT matrix for George Weston to quickly align strategies and communicate competitive positioning to executives and stakeholders.

Weaknesses

Significant Revenue Concentration Risk

George Weston’s 2024 revenue remains heavily tied to Loblaw Companies, which accounted for about 88% of consolidated revenue (C$54.2bn of C$61.6bn in FY2024), exposing Weston to Canadian grocery and pharmacy cycles.

Limited international footprint means a Canadian GDP decline or a 1% drop in grocery volumes could shave several hundred million from EBITDA; localized shocks hit group cash flow directly.

Public Relations and Reputational Challenges

High Debt Levels and Capital Intensity

Managing a massive real estate portfolio and a nationwide retail network forces George Weston Limited (parent of Loblaw) into heavy capital spending and debt: consolidated long-term debt stood at CAD 9.1 billion as of Oct 31, 2024, constraining cash flow for M&A and rapid pivots.

High leverage reduces financial flexibility and raises refinancing risk; net debt/EBITDA was about 2.8x in FY2024, limiting aggressive acquisitions.

Rising rates raise REIT servicing costs—Wesminster Reit-related obligations and higher coupon debt lifted interest expense by ~12% year-over-year in 2024, squeezing net income.

Thin Operating Margins in Retail

George Weston faces thin retail operating margins—Canada’s grocery sector median EBIT margin was about 2.6% in 2024, leaving little room for error.

Weston must trim supply-chain and labour costs to compete with low-cost rivals like Walmart; a 1% rise in wages or 5% commodity inflation could cut earnings-per-share materially.

Even brief logistics disruptions or commodity spikes (2024 wheat up ~20% YoY) can disproportionately hit net income.

- 2024 median grocery EBIT ~2.6%

- Wheat +20% YoY (2024)

- 1% wage rise risks EPS pressure

Exposure to Canadian Regulatory Environment

- 2024 revenue: CAD 53.5B

- Regulatory risk: proposed grocery codes, Competition Bureau probes

- Higher legal/compliance costs: tens of millions/year

- Possible delays: expansion and M&A timelines extended by quarters

Weston risk: Loblaw concentration, rising debt and shrinking grocery margins

Heavy reliance on Loblaw (≈88% of Weston FY2024 revenue, C$54.2bn/ C$61.6bn) concentrates cash‑flow risk in Canadian grocery cycles; net debt/EBITDA ~2.8x (FY2024) limits M&A; SG&A C$4.2bn and rising interest expense (+12% YoY 2024) squeeze free cash flow; regulatory, reputational and margin pressure (median grocery EBIT ~2.6% 2024) raise earnings vulnerability.

| Metric | Value (2024) |

|---|---|

| Loblaw share of revenue | ≈88% (C$54.2bn of C$61.6bn) |

| Net debt / EBITDA | ~2.8x |

| SG&A | C$4.2bn |

| Long‑term debt | C$9.1bn |

| Interest expense change | +12% YoY |

| Median grocery EBIT | ~2.6% |

Same Document Delivered

George Weston SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

George Weston’s diversified footprint—spanning grocery, food processing, and real estate—anchors resilient cashflows, but competitive retail pressures and supply-chain risks test margins and expansion plans.

Our full SWOT analysis unpacks strategic levers, financial context, and operational vulnerabilities with actionable recommendations tailored for investors, advisors, and managers.

Purchase the complete, editable SWOT report (Word + Excel) to convert insights into decisions—plan, pitch, or invest with confidence.

Strengths

Dominant Market Leadership through Loblaw

George Weston holds a 62.5% voting interest in Loblaw Companies Limited, Canada’s largest food and drug retailer with about 1,300 supermarkets and 2,600 pharmacies as of FY2024, giving Weston unmatched scale in procurement and distribution.

That network drove Loblaw to CAD 56.2 billion in 2024 revenue, providing Weston a steady, sizeable cash flow and a cost advantage versus regional rivals through national buying power and logistics.

Strategic Real Estate Integration

Through its 64% stake in Choice Properties REIT (as of Dec 31, 2024), George Weston controls a 2,800+ property portfolio valued at roughly CAD 15.6 billion, many anchored by Loblaw stores, yielding occupancy >98% and stabilized rental income that held up in 2023–24.

Powerful Private Label Brand Equity

George Weston’s private labels, led by President’s Choice and No Name, are among Canada’s most trusted, generating higher gross margins (about 6–8 percentage points above national brands) and driving Loblaws’ 2024 private-label penetration of ~40% of food sales; this boosts profitability while giving value-conscious shoppers cheaper alternatives, deepening loyalty and differentiating the retail mix versus competitors like Walmart and Costco.

Robust PC Optimum Loyalty Ecosystem

The PC Optimum program, with over 23 million members as of Dec 31, 2024, gives George Weston a vast consumer-data asset that fuels targeted marketing and personalized offers across Loblaw grocery, Shoppers Drug Mart pharmacy, and PC Financial services.

That data drives higher basket sizes and frequency—Loblaw reported Q4 2024 same-store sales growth of 3.6%—and creates strong switching costs as members earn and redeem points within the Weston network.

- 23M+ members (Dec 31, 2024)

- Drives personalized promos across grocery, pharmacy, finance

- Supports 3.6% Q4 2024 same-store sales growth (Loblaw)

- High switching cost via cross-network rewards

Resilient Financial Services Segment

- 5M+ PC Optimum members

- 1,500+ retail locations

- Lower acquisition cost vs. big banks

- Mid-single-digit boost to non-grocery revenue (2024)

Weston: Dominant scale—CAD56B Loblaw, 23M members, 40% private-label lift

Weston’s 62.5% stake in Loblaw (≈1,300 supermarkets, 2,600 pharmacies) and CAD56.2B Loblaw 2024 revenue deliver scale, procurement savings, and steady cash flow; Choice Properties (64% stake, ~2,800 properties, CAD15.6B value) supplies >98% occupancy and stable rents; strong private labels (PC, No Name ~40% food penetration) boost margins ~6–8pp; PC Optimum 23M members and PC Financial (5M users) raise basket size and cross-sell.

| Metric | Value (2024) |

|---|---|

| Loblaw revenue | CAD56.2B |

| Supermarkets / Pharmacies | 1,300 / 2,600 |

| PC Optimum members | 23M+ |

| Choice Properties value | CAD15.6B |

| Private-label penetration | ~40% |

What is included in the product

Provides a concise SWOT framework outlining George Weston’s core strengths, operational weaknesses, market opportunities, and external threats to evaluate its strategic position and future prospects.

Provides a concise SWOT matrix for George Weston to quickly align strategies and communicate competitive positioning to executives and stakeholders.

Weaknesses

Significant Revenue Concentration Risk

George Weston’s 2024 revenue remains heavily tied to Loblaw Companies, which accounted for about 88% of consolidated revenue (C$54.2bn of C$61.6bn in FY2024), exposing Weston to Canadian grocery and pharmacy cycles.

Limited international footprint means a Canadian GDP decline or a 1% drop in grocery volumes could shave several hundred million from EBITDA; localized shocks hit group cash flow directly.

Public Relations and Reputational Challenges

High Debt Levels and Capital Intensity

Managing a massive real estate portfolio and a nationwide retail network forces George Weston Limited (parent of Loblaw) into heavy capital spending and debt: consolidated long-term debt stood at CAD 9.1 billion as of Oct 31, 2024, constraining cash flow for M&A and rapid pivots.

High leverage reduces financial flexibility and raises refinancing risk; net debt/EBITDA was about 2.8x in FY2024, limiting aggressive acquisitions.

Rising rates raise REIT servicing costs—Wesminster Reit-related obligations and higher coupon debt lifted interest expense by ~12% year-over-year in 2024, squeezing net income.

Thin Operating Margins in Retail

George Weston faces thin retail operating margins—Canada’s grocery sector median EBIT margin was about 2.6% in 2024, leaving little room for error.

Weston must trim supply-chain and labour costs to compete with low-cost rivals like Walmart; a 1% rise in wages or 5% commodity inflation could cut earnings-per-share materially.

Even brief logistics disruptions or commodity spikes (2024 wheat up ~20% YoY) can disproportionately hit net income.

- 2024 median grocery EBIT ~2.6%

- Wheat +20% YoY (2024)

- 1% wage rise risks EPS pressure

Exposure to Canadian Regulatory Environment

- 2024 revenue: CAD 53.5B

- Regulatory risk: proposed grocery codes, Competition Bureau probes

- Higher legal/compliance costs: tens of millions/year

- Possible delays: expansion and M&A timelines extended by quarters

Weston risk: Loblaw concentration, rising debt and shrinking grocery margins

Heavy reliance on Loblaw (≈88% of Weston FY2024 revenue, C$54.2bn/ C$61.6bn) concentrates cash‑flow risk in Canadian grocery cycles; net debt/EBITDA ~2.8x (FY2024) limits M&A; SG&A C$4.2bn and rising interest expense (+12% YoY 2024) squeeze free cash flow; regulatory, reputational and margin pressure (median grocery EBIT ~2.6% 2024) raise earnings vulnerability.

| Metric | Value (2024) |

|---|---|

| Loblaw share of revenue | ≈88% (C$54.2bn of C$61.6bn) |

| Net debt / EBITDA | ~2.8x |

| SG&A | C$4.2bn |

| Long‑term debt | C$9.1bn |

| Interest expense change | +12% YoY |

| Median grocery EBIT | ~2.6% |

Same Document Delivered

George Weston SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.