Westpac Bank Boston Consulting Group Matrix

Unlock Strategic Clarity

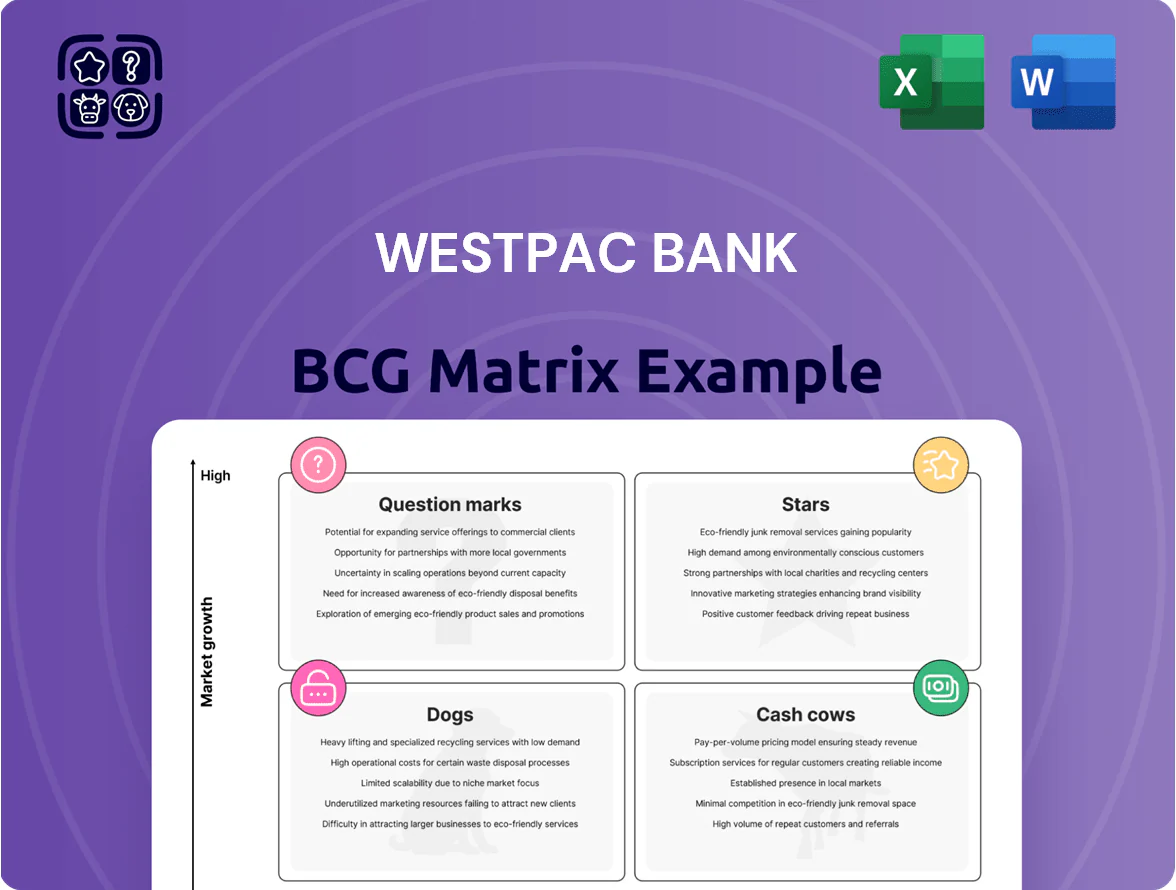

Westpac’s BCG Matrix snapshot highlights where its business lines—retail banking, institutional services, wealth management, and payments—sit amid market growth and relative share, revealing potential Stars to scale and Cash Cows to optimize. This preview teases quadrant placements and strategic implications but stops short of the full, data-rich picture. Purchase the full BCG Matrix to get quadrant-by-quadrant analysis, actionable recommendations, and downloadable Word + Excel files to guide capital allocation and growth decisions.

Stars

Next-Gen Digital Banking UNITE

Next-Gen Digital Banking UNITE sits in Stars: high-growth as Australian mobile banking users hit 85% of adults in 2024 and app sessions grew 22% year-on-year to Q3 2025, driving rapid demand for mobile-first services.

Westpac holds ~15% of ANZ retail digital market share (2025 RFI estimates) but must invest ~A$1.2–1.5bn annually in development and cybersecurity to match neobanks and Big Tech.

UNITE consumes substantial capital for cloud, APIs, and AI-driven automation yet targets 18–34-year-olds who represent 40% of digital deposit growth; success secures Westpac’s leadership in decentralized, automated finance.

Sustainable Finance and ESG Lending

Westpac leads Australia’s green bond and sustainability-linked loan market, underwriting A$12.4bn in green financing through 2024 as corporates push toward a 2050 net-zero goal.

The bank holds a top-quartile market share in ESG lending, financing large renewable projects and infrastructure with specialized teams for project structuring.

Growth rates exceed 25% CAGR (2021–24), but verification and ESG risk assessment raise operational costs by an estimated 130–180 basis points.

As the market matures, Westpac expects these green portfolios to become primary institutional profit drivers, targeting a 15–20% ROE contribution by 2027.

New Zealand Banking Operations

New Zealand Banking Operations is a Star: Westpac NZ holds ~27% market share in NZ retail deposits (2024 RBNZ data) and posted ~4–6% annual revenue growth in 2023–24, outpacing Australia’s single-digit retail growth.

The unit captures retail and SME growth where Westpac is one of NZ’s big four, requiring ongoing capital for RBNZ liquidity/T1 requirements and ~NZD 200–300m tech investment through 2025 to stay competitive.

If Westpac sustains leadership, NZ will remain a key growth engine, contributing ~10–12% of group statutory profit in FY2024 and supporting group expansion into Pacific markets.

SME Digital Lending Solutions

SME Digital Lending Solutions is a Star: Westpac is scaling automated SME loans, growing at ~18% YoY in 2024 and originating ~A$4.2bn in digital SME credit that year, outpacing branch volumes.

By using analytics and open-data scoring, approval times fell to <48 hours for many cases, letting Westpac win share from regional banks and non-bank lenders while spending heavily on tech and marketing.

High promo and capex are needed to convert SME owners from fintechs; if adoption continues, these tools could reshape commercial banking and lift SME NIMs long-term.

- 2024 digital SME originations A$4.2bn

- ~18% YoY growth in 2024

- Approval times reduced to <48 hours

- High promotional/tech spend required

Institutional Infrastructure Finance

Westpac's institutional arm leads financing for Asia-Pacific infrastructure, underwriting about A$18bn in projects in 2024, notably transport and energy-transition deals where government spending rose 12% YoY.

These mandates capture a large share of high-value assignments but demand heavy specialist teams and capital, consuming significant cash—projected A$2.4bn in deployed capital and A$150–220m annual operating costs.

This segment sustains Westpac's top-tier institutional reputation, winning 28% of competitive mandates in 2024 and positioning the bank for pipeline growth as public infrastructure budgets expand.

- 2024 project finance: ~A$18bn

- Deployed capital est.: A$2.4bn

- Annual ops cost est.: A$150–220m

- Market share of mandates: 28% in 2024

High‑capex Growth: UNITE, NZ, SME & Green/Infra Target Major Market Shares

Stars: UNITE, NZ Banking, SME Digital Lending, Green & Infra finance are high-growth, high-share units needing heavy capex (A$1.2–1.5bn pa for UNITE; NZ tech NZD200–300m to 2025; SME originations A$4.2bn in 2024), with targets: UNITE capture ~15% digital share, NZ ~27% deposit share, infra A$18bn project finance (2024).

| Unit | 2024–25 |

|---|---|

| UNITE | A$1.2–1.5bn capex; 15% digital share |

| NZ | 27% deposits; NZD200–300m tech |

| SME | A$4.2bn originations; 18% YoY |

| Infra/Green | A$18bn projects; A$12.4bn green underwritings |

What is included in the product

Comprehensive BCG analysis of Westpac’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Westpac BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

Australian Residential Mortgages

The Australian home loan portfolio is Westpac’s bedrock, holding roughly 17% of the market and about AUD 300bn in outstanding mortgages as of 30 Sep 2025, producing steady net interest income despite housing growth slowing to ~2–3% annually.

With core servicing infrastructure in place, incremental capex is low so mortgage cashflows fund dividends and seed higher-growth digital initiatives, supporting liquidity ratios—APRA CET1 ~12.5% in 2025—while maintaining credit quality.

Retail Deposit Accounts

Westpac’s retail deposit accounts are a cash cow: as of Sep 30, 2025 retail deposits stood at A$283.4bn, reflecting dominant market share in a low-growth Australian market.

They supply low-cost funding—retail deposit cost ~1.1% in FY25—fueling mortgage and business lending and cutting reliance on costly wholesale debt.

Brand scale keeps marketing spend low for basic savings; steady deposits keep LCR and NSFR comfortably above APRA minima, avoiding expensive external funding.

Standard Commercial Banking

Standard commercial banking—Westpac’s traditional business banking for established firms—is a cash cow: mature segment, high market share (estimated ~18% of Australian business deposits in 2024) and predictable returns.

Long-term client relationships need little new infrastructure or heavy promotion, keeping cost-to-income low; 2024 business lending NIMs stayed near 2.1%, supporting margins.

High profit margins on established loans and overdrafts generated substantial free cash flow—Westpac’s 2024 net interest income was A$14.2bn—so this segment cushions corporate health in volatile markets.

Credit Card Portfolios

Westpac holds a leading share in Australia’s mature credit card market—about 15% of outstanding cards and NZ$45bn+ in receivables as of FY2024—delivering high interest and fee margins despite slowing card volume growth due to digital wallets and BNPL.

Investment focuses on maintenance, fraud prevention, and compliance; cash flows from cards fund R&D into payment tech and mobile solutions rather than market-share expansion.

- ~15% market share; NZ$45bn+ receivables (FY2024)

- High net interest and fee margins; core cash cow

- Capex shifted to fraud/security and maintenance

- Proceeds funneled to digital payments R&D

Transactional Banking Services

Westpac’s transactional banking services—everyday accounts and payments for ~9 million customers—generate steady fee income with low growth, aligning them as Cash Cows in the BCG matrix.

As a market leader, Westpac processes high transaction volumes through established clearing rails; fixed-cost operations mean higher margins as usage rises (FY2024 payment volumes up ~3.5%).

These services boost retention and delivered stable operating cash flow—Westpac reported cash earnings of A$3.9bn in FY2024—funding strategic investments across the group.

- Millions of retail customers (~9m)

- Low growth, steady fees

- High volumes → margin leverage

- FY2024 cash earnings A$3.9bn

Westpac’s Cash Cows: A$300bn Mortgages, A$283bn Deposits & Strong Retail Earnings

Westpac’s Cash Cows: Australian mortgages (A$300bn, ~17% share, NII stable), retail deposits (A$283.4bn, cost ~1.1%, supports LCR/NSFR), business banking (~18% deposits, NIM ~2.1%), credit cards (~15% share, NZ$45bn receivables), transactional accounts (~9m customers, FY24 cash earnings A$3.9bn).

| Segment | Size | Yield/Cost |

|---|---|---|

| Mortgages | A$300bn | — |

| Retail deposits | A$283.4bn | 1.1% |

| Cards | NZ$45bn | — |

What You See Is What You Get

Westpac Bank BCG Matrix

The file you're previewing is the exact Westpac BCG Matrix report you'll receive after purchase—no watermarks or demo content, just the fully formatted, ready-to-use strategic analysis crafted for clarity and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Westpac’s BCG Matrix snapshot highlights where its business lines—retail banking, institutional services, wealth management, and payments—sit amid market growth and relative share, revealing potential Stars to scale and Cash Cows to optimize. This preview teases quadrant placements and strategic implications but stops short of the full, data-rich picture. Purchase the full BCG Matrix to get quadrant-by-quadrant analysis, actionable recommendations, and downloadable Word + Excel files to guide capital allocation and growth decisions.

Stars

Next-Gen Digital Banking UNITE

Next-Gen Digital Banking UNITE sits in Stars: high-growth as Australian mobile banking users hit 85% of adults in 2024 and app sessions grew 22% year-on-year to Q3 2025, driving rapid demand for mobile-first services.

Westpac holds ~15% of ANZ retail digital market share (2025 RFI estimates) but must invest ~A$1.2–1.5bn annually in development and cybersecurity to match neobanks and Big Tech.

UNITE consumes substantial capital for cloud, APIs, and AI-driven automation yet targets 18–34-year-olds who represent 40% of digital deposit growth; success secures Westpac’s leadership in decentralized, automated finance.

Sustainable Finance and ESG Lending

Westpac leads Australia’s green bond and sustainability-linked loan market, underwriting A$12.4bn in green financing through 2024 as corporates push toward a 2050 net-zero goal.

The bank holds a top-quartile market share in ESG lending, financing large renewable projects and infrastructure with specialized teams for project structuring.

Growth rates exceed 25% CAGR (2021–24), but verification and ESG risk assessment raise operational costs by an estimated 130–180 basis points.

As the market matures, Westpac expects these green portfolios to become primary institutional profit drivers, targeting a 15–20% ROE contribution by 2027.

New Zealand Banking Operations

New Zealand Banking Operations is a Star: Westpac NZ holds ~27% market share in NZ retail deposits (2024 RBNZ data) and posted ~4–6% annual revenue growth in 2023–24, outpacing Australia’s single-digit retail growth.

The unit captures retail and SME growth where Westpac is one of NZ’s big four, requiring ongoing capital for RBNZ liquidity/T1 requirements and ~NZD 200–300m tech investment through 2025 to stay competitive.

If Westpac sustains leadership, NZ will remain a key growth engine, contributing ~10–12% of group statutory profit in FY2024 and supporting group expansion into Pacific markets.

SME Digital Lending Solutions

SME Digital Lending Solutions is a Star: Westpac is scaling automated SME loans, growing at ~18% YoY in 2024 and originating ~A$4.2bn in digital SME credit that year, outpacing branch volumes.

By using analytics and open-data scoring, approval times fell to <48 hours for many cases, letting Westpac win share from regional banks and non-bank lenders while spending heavily on tech and marketing.

High promo and capex are needed to convert SME owners from fintechs; if adoption continues, these tools could reshape commercial banking and lift SME NIMs long-term.

- 2024 digital SME originations A$4.2bn

- ~18% YoY growth in 2024

- Approval times reduced to <48 hours

- High promotional/tech spend required

Institutional Infrastructure Finance

Westpac's institutional arm leads financing for Asia-Pacific infrastructure, underwriting about A$18bn in projects in 2024, notably transport and energy-transition deals where government spending rose 12% YoY.

These mandates capture a large share of high-value assignments but demand heavy specialist teams and capital, consuming significant cash—projected A$2.4bn in deployed capital and A$150–220m annual operating costs.

This segment sustains Westpac's top-tier institutional reputation, winning 28% of competitive mandates in 2024 and positioning the bank for pipeline growth as public infrastructure budgets expand.

- 2024 project finance: ~A$18bn

- Deployed capital est.: A$2.4bn

- Annual ops cost est.: A$150–220m

- Market share of mandates: 28% in 2024

High‑capex Growth: UNITE, NZ, SME & Green/Infra Target Major Market Shares

Stars: UNITE, NZ Banking, SME Digital Lending, Green & Infra finance are high-growth, high-share units needing heavy capex (A$1.2–1.5bn pa for UNITE; NZ tech NZD200–300m to 2025; SME originations A$4.2bn in 2024), with targets: UNITE capture ~15% digital share, NZ ~27% deposit share, infra A$18bn project finance (2024).

| Unit | 2024–25 |

|---|---|

| UNITE | A$1.2–1.5bn capex; 15% digital share |

| NZ | 27% deposits; NZD200–300m tech |

| SME | A$4.2bn originations; 18% YoY |

| Infra/Green | A$18bn projects; A$12.4bn green underwritings |

What is included in the product

Comprehensive BCG analysis of Westpac’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Westpac BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

Australian Residential Mortgages

The Australian home loan portfolio is Westpac’s bedrock, holding roughly 17% of the market and about AUD 300bn in outstanding mortgages as of 30 Sep 2025, producing steady net interest income despite housing growth slowing to ~2–3% annually.

With core servicing infrastructure in place, incremental capex is low so mortgage cashflows fund dividends and seed higher-growth digital initiatives, supporting liquidity ratios—APRA CET1 ~12.5% in 2025—while maintaining credit quality.

Retail Deposit Accounts

Westpac’s retail deposit accounts are a cash cow: as of Sep 30, 2025 retail deposits stood at A$283.4bn, reflecting dominant market share in a low-growth Australian market.

They supply low-cost funding—retail deposit cost ~1.1% in FY25—fueling mortgage and business lending and cutting reliance on costly wholesale debt.

Brand scale keeps marketing spend low for basic savings; steady deposits keep LCR and NSFR comfortably above APRA minima, avoiding expensive external funding.

Standard Commercial Banking

Standard commercial banking—Westpac’s traditional business banking for established firms—is a cash cow: mature segment, high market share (estimated ~18% of Australian business deposits in 2024) and predictable returns.

Long-term client relationships need little new infrastructure or heavy promotion, keeping cost-to-income low; 2024 business lending NIMs stayed near 2.1%, supporting margins.

High profit margins on established loans and overdrafts generated substantial free cash flow—Westpac’s 2024 net interest income was A$14.2bn—so this segment cushions corporate health in volatile markets.

Credit Card Portfolios

Westpac holds a leading share in Australia’s mature credit card market—about 15% of outstanding cards and NZ$45bn+ in receivables as of FY2024—delivering high interest and fee margins despite slowing card volume growth due to digital wallets and BNPL.

Investment focuses on maintenance, fraud prevention, and compliance; cash flows from cards fund R&D into payment tech and mobile solutions rather than market-share expansion.

- ~15% market share; NZ$45bn+ receivables (FY2024)

- High net interest and fee margins; core cash cow

- Capex shifted to fraud/security and maintenance

- Proceeds funneled to digital payments R&D

Transactional Banking Services

Westpac’s transactional banking services—everyday accounts and payments for ~9 million customers—generate steady fee income with low growth, aligning them as Cash Cows in the BCG matrix.

As a market leader, Westpac processes high transaction volumes through established clearing rails; fixed-cost operations mean higher margins as usage rises (FY2024 payment volumes up ~3.5%).

These services boost retention and delivered stable operating cash flow—Westpac reported cash earnings of A$3.9bn in FY2024—funding strategic investments across the group.

- Millions of retail customers (~9m)

- Low growth, steady fees

- High volumes → margin leverage

- FY2024 cash earnings A$3.9bn

Westpac’s Cash Cows: A$300bn Mortgages, A$283bn Deposits & Strong Retail Earnings

Westpac’s Cash Cows: Australian mortgages (A$300bn, ~17% share, NII stable), retail deposits (A$283.4bn, cost ~1.1%, supports LCR/NSFR), business banking (~18% deposits, NIM ~2.1%), credit cards (~15% share, NZ$45bn receivables), transactional accounts (~9m customers, FY24 cash earnings A$3.9bn).

| Segment | Size | Yield/Cost |

|---|---|---|

| Mortgages | A$300bn | — |

| Retail deposits | A$283.4bn | 1.1% |

| Cards | NZ$45bn | — |

What You See Is What You Get

Westpac Bank BCG Matrix

The file you're previewing is the exact Westpac BCG Matrix report you'll receive after purchase—no watermarks or demo content, just the fully formatted, ready-to-use strategic analysis crafted for clarity and decision-making.