WeWork Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

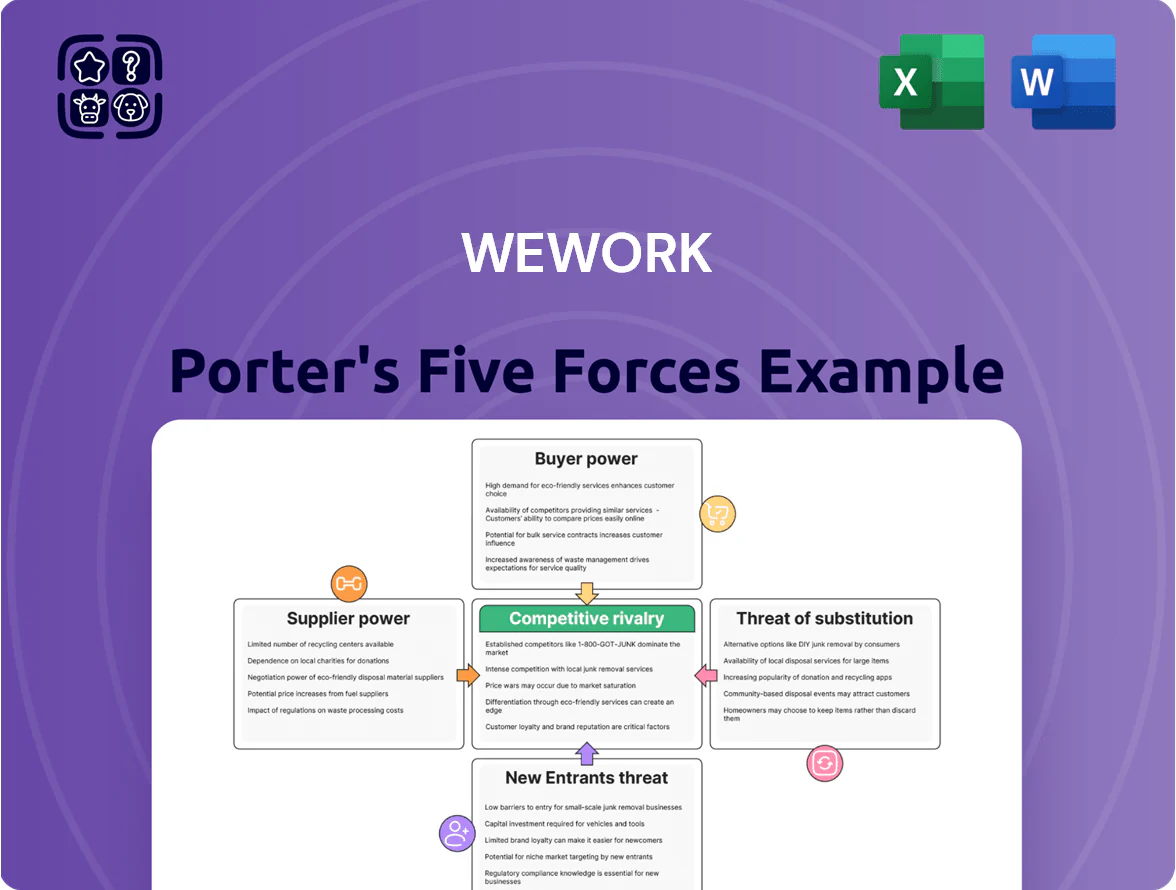

WeWork faces intense competitive rivalry from traditional landlords and flexible workspace rivals, moderate buyer power driven by corporate clients, and evolving substitute threats as remote work habits shift demand; supplier power and regulatory risks add complexity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WeWork’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Commercial Real Estate Owners

Major landlords and REITs control Tier-A offices in NYC, London, SF and others, giving them pricing power critical to WeWork’s urban-focused model.

By late 2025 WeWork had renegotiated or exited roughly 40% of its leases, but still depends on a small set of landlords in ~20 global markets.

This concentration lets suppliers push higher rents, stricter escalation clauses, or larger security deposits—sometimes 3–6 months or more at renewal.

Fixed Long-term Lease Obligations

The mismatch between WeWork’s long-term lease liabilities—about $6.5B in operating lease commitments as of Dec 31, 2024—and member revenue that can shift quarter-to-quarter gives landlords outsized leverage over costs.

Even after moving toward management agreements, a large share of locations remain under fixed leases that are costly to renegotiate and bind cash flow.

These fixed rents compress margins: a 10–20% occupancy drop can swing adjusted EBITDA by double digits because lease obligations stay constant.

Specialized Infrastructure and Utility Providers

Specialized vendors for high-speed internet, HVAC, and premium finishes are vital to WeWork’s premium brand; switching costs are high—industry estimates show enterprise-grade fiber installs cost $40k–$120k per site (2024 US avg).

Dependence on specific tech partners for proprietary building management software raises supplier leverage; 2023 surveys find 62% of flexible-office operators cite vendor lock-in as a top operational risk.

These suppliers can demand higher margins and tighter SLAs, and disruptions or price hikes would directly hit occupancy NPS and could raise operating costs by 3–7% annually.

Impact of Debt and Financial Creditors

Financial institutions and institutional investors supplying capital to WeWork wield strong control over operations; post-restructuring into 2025 creditors held roughly $3.5bn in secured claims and imposed tight covenants tied to EBITDA and leverage ratios.

These lenders set performance targets that steer asset sales, lease renegotiations, and cash allocation; their board-level influence and veto rights make them de facto gatekeepers of strategy.

- ~$3.5bn secured claims (2025)

- EBITDA covenants drive cost cuts

- Debt holders hold governance vetoes

Geographic Scarcity of Prime Real Estate

In London, New York, and Tokyo the stock of large-floorplate offices is tight—central London saw vacancy fall to ~5.6% in H2 2024, Manhattan to ~6.0% by Q3 2024, and Tokyo CBD to ~3–4% in 2024—so landlords can pick tenants and often prefer legacy corporates over flexible providers like WeWork.

That scarcity means WeWork accepts higher rents, shorter renewals, and stricter fit-out rules to keep flagship locations, squeezing margins and raising churn risk.

- Vacancy: London ~5.6%, Manhattan ~6.0%, Tokyo ~3–4% (2024)

- Result: landlords selective; prefer corporates

- Impact: higher rents, tougher lease terms, margin pressure

Suppliers’ stronghold: $6.5B leases, $3.5B debt & costly vendor lock‑in squeeze WeWork

Suppliers—major landlords, REITs, specialized vendors, and creditors—hold strong leverage over WeWork via concentrated urban office supply, long-term lease liabilities (~$6.5B operating lease commitments, Dec 31, 2024), costly vendor lock-in (fiber installs $40k–$120k/site 2024), and creditor covenants (~$3.5B secured claims, 2025) that compress margins and limit strategic flexibility.

| Supplier | Key stat |

|---|---|

| Leases | $6.5B commitments (2024) |

| Creditors | $3.5B secured (2025) |

| Vendors | Fiber $40k–$120k/site (2024) |

What is included in the product

Tailored exclusively for WeWork, this Porter’s Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, and substitutes that shape its pricing, profitability, and strategic vulnerabilities.

Compact Porter's Five Forces snapshot tailored for WeWork—quickly spot bargaining power, rivalry, and disruption risks to steer leasing, pricing, and expansion choices.

Customers Bargaining Power

Low Switching Costs for Individual Members

Freelancers and small startups can switch to rival coworking spaces or back home with almost no cost, as ~70% of WeWork memberships were month-to-month by 2024, letting members exit when better deals appear; this churn pressure pushed WeWork to spend on retention—community events, networking, and perks—contributing to roughly 8–10% of revenue directed to member experience in 2023–2024 to defend occupancy rates.

High Price Sensitivity in the SME Segment

Small and medium enterprises view office space as a major overhead and are highly price-sensitive; in 2025 surveys 62% of SMEs ranked rent cuts among top two cost priorities. In a post-2025 cost-optimization environment SMEs routinely compare per-desk rates across providers, driving churn when WeWork raises fees. The surge of budget coworking—over 1,200 new low-cost centers in 2024–25—caps pricing power and forces WeWork to compete on flexible terms instead of higher margins.

Volume Leverage of Enterprise Clients

Large enterprise clients leasing entire floors or multiple suites wield strong bargaining power, often securing bespoke pricing and build-outs; in 2024 enterprises accounted for about 28% of WeWork’s revenue, boosting their leverage.

These clients trade longer-term stability—median enterprise lease length ~36 months—for deep discounts and specialized services, pushing average rent concessions in 2024 toward 15–25%.

Their credible threat to revert to direct traditional leases gives them an upper hand in negotiations, pressuring WeWork’s margins and capital expenditure on customizations.

Abundance of Information and Price Transparency

- 68% of searches start online (JLL 2024)

- Buyers secure 5–15% concessions

- 42% renewals include matched offers (2024)

Shift Toward Permanent Hybrid Work Preferences

The shift to permanent hybrid work gives WeWork customers strong bargaining power: 62% of U.S. knowledge workers (2024 Gallup) prefer hybrid, driving demand for smaller footprints and usage-based billing, cutting average desk occupancy from 70% to ~40% and pressuring revenue per seat.

WeWork must offer on-demand access, credit-based systems, and dynamic pricing or face churn and lower lease yield; Q4 2024 flexible revenues grew but margin pressures persist.

- 62% prefer hybrid (Gallup 2024)

- Average desk occupancy ~40%

- Demand for usage billing up; smaller footprints

- WeWork flexible revenue up in Q4 2024, margins compressed

Customers Command Prices: High MRR churn, deep concessions drive 8–10% retention costs

Customers hold high bargaining power: 70% month-to-month members (2024) and 62% SMEs prioritizing rent cuts (2025) drive churn and force WeWork into ~8–10% revenue spending on retention; enterprises (28% revenue, median 36-month lease) extract 15–25% concessions, while online search transparency (68% searches, JLL 2024) yields typical 5–15% negotiated discounts.

| Metric | Value |

|---|---|

| Month-to-month share (2024) | 70% |

| Enterprise revenue share (2024) | 28% |

| Enterprise concession (2024) | 15–25% |

| Retention spend (2023–24) | 8–10% of revenue |

| Online search share (JLL 2024) | 68% |

| Negotiated discounts | 5–15% |

Same Document Delivered

WeWork Porter's Five Forces Analysis

This preview shows the exact WeWork Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for download the moment you purchase; no samples or placeholders, just the complete document.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

WeWork faces intense competitive rivalry from traditional landlords and flexible workspace rivals, moderate buyer power driven by corporate clients, and evolving substitute threats as remote work habits shift demand; supplier power and regulatory risks add complexity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WeWork’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Commercial Real Estate Owners

Major landlords and REITs control Tier-A offices in NYC, London, SF and others, giving them pricing power critical to WeWork’s urban-focused model.

By late 2025 WeWork had renegotiated or exited roughly 40% of its leases, but still depends on a small set of landlords in ~20 global markets.

This concentration lets suppliers push higher rents, stricter escalation clauses, or larger security deposits—sometimes 3–6 months or more at renewal.

Fixed Long-term Lease Obligations

The mismatch between WeWork’s long-term lease liabilities—about $6.5B in operating lease commitments as of Dec 31, 2024—and member revenue that can shift quarter-to-quarter gives landlords outsized leverage over costs.

Even after moving toward management agreements, a large share of locations remain under fixed leases that are costly to renegotiate and bind cash flow.

These fixed rents compress margins: a 10–20% occupancy drop can swing adjusted EBITDA by double digits because lease obligations stay constant.

Specialized Infrastructure and Utility Providers

Specialized vendors for high-speed internet, HVAC, and premium finishes are vital to WeWork’s premium brand; switching costs are high—industry estimates show enterprise-grade fiber installs cost $40k–$120k per site (2024 US avg).

Dependence on specific tech partners for proprietary building management software raises supplier leverage; 2023 surveys find 62% of flexible-office operators cite vendor lock-in as a top operational risk.

These suppliers can demand higher margins and tighter SLAs, and disruptions or price hikes would directly hit occupancy NPS and could raise operating costs by 3–7% annually.

Impact of Debt and Financial Creditors

Financial institutions and institutional investors supplying capital to WeWork wield strong control over operations; post-restructuring into 2025 creditors held roughly $3.5bn in secured claims and imposed tight covenants tied to EBITDA and leverage ratios.

These lenders set performance targets that steer asset sales, lease renegotiations, and cash allocation; their board-level influence and veto rights make them de facto gatekeepers of strategy.

- ~$3.5bn secured claims (2025)

- EBITDA covenants drive cost cuts

- Debt holders hold governance vetoes

Geographic Scarcity of Prime Real Estate

In London, New York, and Tokyo the stock of large-floorplate offices is tight—central London saw vacancy fall to ~5.6% in H2 2024, Manhattan to ~6.0% by Q3 2024, and Tokyo CBD to ~3–4% in 2024—so landlords can pick tenants and often prefer legacy corporates over flexible providers like WeWork.

That scarcity means WeWork accepts higher rents, shorter renewals, and stricter fit-out rules to keep flagship locations, squeezing margins and raising churn risk.

- Vacancy: London ~5.6%, Manhattan ~6.0%, Tokyo ~3–4% (2024)

- Result: landlords selective; prefer corporates

- Impact: higher rents, tougher lease terms, margin pressure

Suppliers’ stronghold: $6.5B leases, $3.5B debt & costly vendor lock‑in squeeze WeWork

Suppliers—major landlords, REITs, specialized vendors, and creditors—hold strong leverage over WeWork via concentrated urban office supply, long-term lease liabilities (~$6.5B operating lease commitments, Dec 31, 2024), costly vendor lock-in (fiber installs $40k–$120k/site 2024), and creditor covenants (~$3.5B secured claims, 2025) that compress margins and limit strategic flexibility.

| Supplier | Key stat |

|---|---|

| Leases | $6.5B commitments (2024) |

| Creditors | $3.5B secured (2025) |

| Vendors | Fiber $40k–$120k/site (2024) |

What is included in the product

Tailored exclusively for WeWork, this Porter’s Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, and substitutes that shape its pricing, profitability, and strategic vulnerabilities.

Compact Porter's Five Forces snapshot tailored for WeWork—quickly spot bargaining power, rivalry, and disruption risks to steer leasing, pricing, and expansion choices.

Customers Bargaining Power

Low Switching Costs for Individual Members

Freelancers and small startups can switch to rival coworking spaces or back home with almost no cost, as ~70% of WeWork memberships were month-to-month by 2024, letting members exit when better deals appear; this churn pressure pushed WeWork to spend on retention—community events, networking, and perks—contributing to roughly 8–10% of revenue directed to member experience in 2023–2024 to defend occupancy rates.

High Price Sensitivity in the SME Segment

Small and medium enterprises view office space as a major overhead and are highly price-sensitive; in 2025 surveys 62% of SMEs ranked rent cuts among top two cost priorities. In a post-2025 cost-optimization environment SMEs routinely compare per-desk rates across providers, driving churn when WeWork raises fees. The surge of budget coworking—over 1,200 new low-cost centers in 2024–25—caps pricing power and forces WeWork to compete on flexible terms instead of higher margins.

Volume Leverage of Enterprise Clients

Large enterprise clients leasing entire floors or multiple suites wield strong bargaining power, often securing bespoke pricing and build-outs; in 2024 enterprises accounted for about 28% of WeWork’s revenue, boosting their leverage.

These clients trade longer-term stability—median enterprise lease length ~36 months—for deep discounts and specialized services, pushing average rent concessions in 2024 toward 15–25%.

Their credible threat to revert to direct traditional leases gives them an upper hand in negotiations, pressuring WeWork’s margins and capital expenditure on customizations.

Abundance of Information and Price Transparency

- 68% of searches start online (JLL 2024)

- Buyers secure 5–15% concessions

- 42% renewals include matched offers (2024)

Shift Toward Permanent Hybrid Work Preferences

The shift to permanent hybrid work gives WeWork customers strong bargaining power: 62% of U.S. knowledge workers (2024 Gallup) prefer hybrid, driving demand for smaller footprints and usage-based billing, cutting average desk occupancy from 70% to ~40% and pressuring revenue per seat.

WeWork must offer on-demand access, credit-based systems, and dynamic pricing or face churn and lower lease yield; Q4 2024 flexible revenues grew but margin pressures persist.

- 62% prefer hybrid (Gallup 2024)

- Average desk occupancy ~40%

- Demand for usage billing up; smaller footprints

- WeWork flexible revenue up in Q4 2024, margins compressed

Customers Command Prices: High MRR churn, deep concessions drive 8–10% retention costs

Customers hold high bargaining power: 70% month-to-month members (2024) and 62% SMEs prioritizing rent cuts (2025) drive churn and force WeWork into ~8–10% revenue spending on retention; enterprises (28% revenue, median 36-month lease) extract 15–25% concessions, while online search transparency (68% searches, JLL 2024) yields typical 5–15% negotiated discounts.

| Metric | Value |

|---|---|

| Month-to-month share (2024) | 70% |

| Enterprise revenue share (2024) | 28% |

| Enterprise concession (2024) | 15–25% |

| Retention spend (2023–24) | 8–10% of revenue |

| Online search share (JLL 2024) | 68% |

| Negotiated discounts | 5–15% |

Same Document Delivered

WeWork Porter's Five Forces Analysis

This preview shows the exact WeWork Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for download the moment you purchase; no samples or placeholders, just the complete document.