TCNS Clothing PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of TCNS Clothing—identifying regulatory, economic, social, technological, and environmental forces shaping its growth and risks; ideal for investors, consultants, and managers. Purchase the full report for a complete, actionable breakdown with ready-to-use insights and templates to inform decisions and strengthen your competitive position.

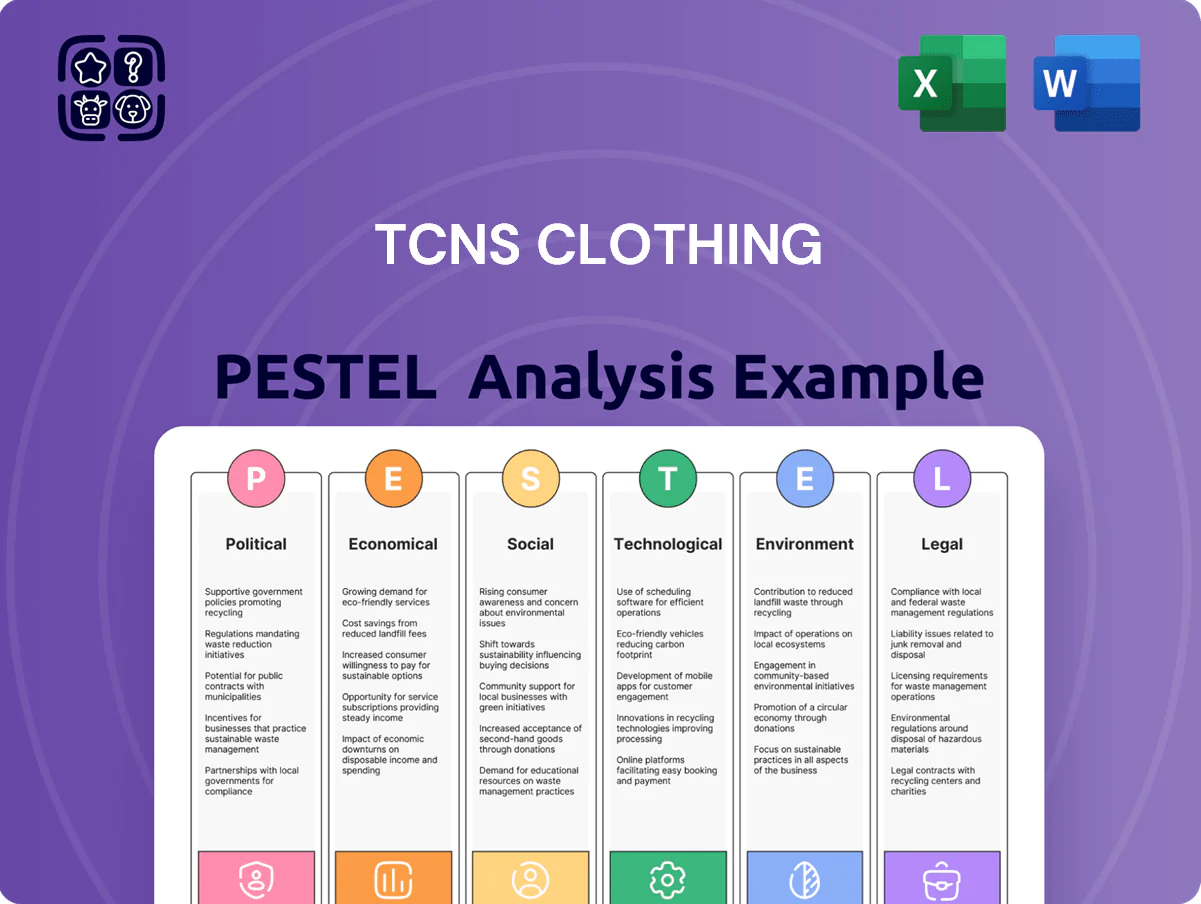

Political factors

Aditya Birla Fashion and Retail (ABFRL) ownership

Following ABFRL’s acquisition completed in 2021, TCNS Clothing now aligns political lobbying and governance with a conglomerate reporting consolidated FY2024 revenue of INR 21,318 crore, streamlining engagement with ministries on textile policy and GST issues; ABFRL’s market influence has aided regulatory predictability for W and Aurelia, supporting steady retail expansion across 1,650+ stores and bolstering investor confidence amid sector reforms.

Government focus on 'Make in India'

The Production Linked Incentive scheme for textiles, allocating about INR 10,683 crore through 2024, directly benefits TCNS Clothing by subsidizing capex and boosting local value addition; as a leading Indian ethnic wear player it can access PLI-linked manufacturing clusters and infrastructure, enhancing gross margins and export readiness—India’s textile exports rose 19% to USD 55.9 billion in FY2023-24, improving market opportunity for TCNS’s domestic and international growth.

Foreign Direct Investment (FDI) policies in retail

Ongoing adjustments to FDI norms in multi-brand and single-brand retail affect TCNS by shaping entry terms for global players in Indian ethnic wear; policy tweaks since 2024 kept single-brand FDI at 100% with conditions, while multi-brand remains restricted, limiting direct competition from big-box foreign retailers. The political landscape through late 2025 favors domestic-heavy firms, with protective measures and route-to-market rules that supported a 7–9% annual growth in organised ethnic retail in 2024–25. Regulations mandating local sourcing and investment thresholds slow the pace at which global brands can scale in the traditional wear segment, influencing TCNS expansion strategy and market share dynamics.

Trade agreements and export incentives

Bilateral trade agreements through 2024–25, including India-UAE CEPA expansion and ASEAN-India tariff concessions, enable TCNS to target ~15–20% revenue growth from Middle East and Southeast Asia; exports to these regions rose 12% in FY2024. Political stability and diplomatic ties affect store rollouts and logistics costs—instability can raise freight/insurance by 5–10%. Recent export duty cuts on RMG in 2024 improved margins by ~80–120 bps.

- Target regions: Middle East, Southeast Asia — +12% exports FY2024

- Projected international revenue growth: 15–20%

- Logistics cost risk if instability: +5–10%

- Export duty cuts 2024: margin +80–120 bps

State-level labor law reforms

State-level labor law reforms in India, including consolidation into four labour codes since 2020, materially affect TCNS Clothing’s 400+ stores and multiple manufacturing units across states; changes increasing flexible hiring can reduce hourly labor costs by an estimated 5–8% but may raise compliance monitoring expenses.

Implementation of industrial flexibility provisions impacts workforce strategies—contract staffing rose ~12% in Indian retail in 2023—altering payroll mix and benefits liabilities for TCNS.

Stable state governments (e.g., Gujarat, Karnataka) correlate with fewer supply disruptions; states with frequent industrial actions saw inventory turnover slow by ~6% in 2022, risking retail revenue volatility.

- 400+ stores and multiple manufacturing sites across states

- Potential 5–8% reduction in hourly labor costs from flexible hiring

- Contract staffing up ~12% in retail (2023)

- Industrial actions linked to ~6% slower inventory turnover (2022)

Post‑ABFRL consolidation & PLI boost propel 7–9% ethnic retail growth, exports +12%

Post-ABFRL consolidation improves regulatory access and predictability; PLI textiles (INR 10,683 crore) raises capex subsidies; FDI rules favor domestic players sustaining 7–9% organised ethnic retail growth (2024–25); trade deals/exports (+12% FY2024) target 15–20% intl revenue; labour code reforms lower hourly costs 5–8% but increase compliance.

| Metric | Value |

|---|---|

| ABFRL FY2024 revenue | INR 21,318 cr |

| PLI allocation | INR 10,683 cr |

| Ethnic retail growth | 7–9% (2024–25) |

| Exports FY2024 | +12% |

| Labour cost impact | -5–8% |

What is included in the product

Explores how external macro-environmental factors uniquely affect TCNS Clothing across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications tailored to its Indian and global apparel markets to inform strategy, risk mitigation, and investor communications.

A concise, shareable TCNS Clothing PESTLE summary that’s visually segmented for quick interpretation, ideal for meetings, slide decks, and cross-team alignment while allowing note-taking for region- or business-specific context.

Economic factors

Recovery in discretionary consumer spending

By end-2025 India’s GDP growth normalised around 6.8%, fueling a rebound in urban middle-class consumption; retail discretionary spending rose ~9% YoY in FY25, lifting demand for lifestyle and fashion. TCNS brands W and Aurelia captured this uptick as urban women increased spend on branded ethnic wear for work and social occasions, supporting a shift toward higher average selling prices. The trend underpins TCNS’s premiumisation strategy, aiding margin expansion and higher ASPs.

Inflationary pressure on raw materials

Fluctuations in cotton, silk and synthetic fibre prices—cotton up ~18% in 2024 vs 2023, benchmark polyester resin rising ~12%—pressure TCNS Clothing’s cost base, forcing margin-tight choices in the ethnic wear segment. Rising input costs must be balanced against consumer price sensitivity after discretionary spends slowed in FY24; losing a 1–2% price competitiveness risks market-share erosion. Global commodity volatility makes advanced procurement, supplier diversification and hedging essential to protect FY25 gross margins.

Growth of the organized retail sector

The shift from unorganized boutiques to organized retail boosts TCNS, where organized retail in India reached ~17% of overall retail in 2024 and is projected to hit ~22% by 2027; TCNS’s ~650 EBOs and 2,500 MBOs (2025) capitalize on mall and branded-outlet traffic, increasing market share for Aurelia and Wishful and supporting compounded revenue growth—TCNS reported 18% retail channel revenue growth in FY2024, reflecting this structural tailwind.

E-commerce and omnichannel integration costs

Maintaining TCNS Clothing’s digital presence demands significant investment in platforms, IT and last-mile delivery—e-commerce and logistics capex rose industry-wide ~12–15% in 2024, with fashion return rates near 20–30% eroding margins.

Online channels now drive ~40–55% of apparel sales for comparable Indian brands in 2024–25, but elevated customer acquisition costs (often INR 400–800 per order) and returns compress profitability, forcing trade-offs between store expansion and digital spend.

- E-commerce share: ~40–55% of apparel sales (2024–25)

- Return rates: 20–30% in fashion (2024)

- Customer acquisition cost: ~INR 400–800/order (2024)

- Industry digital/logistics capex growth: ~12–15% (2024)

Interest rate environment and capital cost

Prevailing RBI policy rates — repo at 6.5% (Dec 2025) — raise TCNS’s borrowing costs for expansion and inventory; ABFRL backing secures lower spreads, improving access to ~8–9% effective borrowing versus standalone rates above 10% for peers.

Higher rates increase project discount rates, reducing NPV of store openings and omnichannel investments; elevated consumer credit costs can cut demand for premium lines like Wishful, where average ticket is ~₹2,500–3,500.

- Repo rate: 6.5% (Dec 2025)

- Estimated TCNS effective borrowing: ~8–9%

- Wishful avg ticket: ₹2,500–3,500

- Higher rates → lower NPV, weaker premium demand

Robust India demand lifts TCNS despite rising cotton costs and higher e‑commerce mix

Economic tailwinds: India GDP ~6.8% (2025) and retail discretionary +9% (FY25) boosted branded ethnic demand; cotton +18% (2024), polyester resin +12% raised input costs; organized retail ~17% (2024) to ~22% (2027) aided TCNS’s 650 EBOs/2,500 MBOs; e-commerce 40–55% share (2024–25) with CAC INR 400–800 and return rates 20–30%; repo 6.5% (Dec‑2025), TCNS borrowing ~8–9%.

| Metric | Value |

|---|---|

| GDP growth (2025) | 6.8% |

| Retail discretionary (FY25) | +9% YoY |

| Cotton (2024) | +18% |

| E‑commerce share | 40–55% |

Same Document Delivered

TCNS Clothing PESTLE Analysis

The preview shown here is the exact TCNS Clothing PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The file you’re seeing now is the final version, with no placeholders or teasers, delivered exactly as shown. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. Don’t just imagine what you’re getting—this is the real, finished file you’ll own upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of TCNS Clothing—identifying regulatory, economic, social, technological, and environmental forces shaping its growth and risks; ideal for investors, consultants, and managers. Purchase the full report for a complete, actionable breakdown with ready-to-use insights and templates to inform decisions and strengthen your competitive position.

Political factors

Aditya Birla Fashion and Retail (ABFRL) ownership

Following ABFRL’s acquisition completed in 2021, TCNS Clothing now aligns political lobbying and governance with a conglomerate reporting consolidated FY2024 revenue of INR 21,318 crore, streamlining engagement with ministries on textile policy and GST issues; ABFRL’s market influence has aided regulatory predictability for W and Aurelia, supporting steady retail expansion across 1,650+ stores and bolstering investor confidence amid sector reforms.

Government focus on 'Make in India'

The Production Linked Incentive scheme for textiles, allocating about INR 10,683 crore through 2024, directly benefits TCNS Clothing by subsidizing capex and boosting local value addition; as a leading Indian ethnic wear player it can access PLI-linked manufacturing clusters and infrastructure, enhancing gross margins and export readiness—India’s textile exports rose 19% to USD 55.9 billion in FY2023-24, improving market opportunity for TCNS’s domestic and international growth.

Foreign Direct Investment (FDI) policies in retail

Ongoing adjustments to FDI norms in multi-brand and single-brand retail affect TCNS by shaping entry terms for global players in Indian ethnic wear; policy tweaks since 2024 kept single-brand FDI at 100% with conditions, while multi-brand remains restricted, limiting direct competition from big-box foreign retailers. The political landscape through late 2025 favors domestic-heavy firms, with protective measures and route-to-market rules that supported a 7–9% annual growth in organised ethnic retail in 2024–25. Regulations mandating local sourcing and investment thresholds slow the pace at which global brands can scale in the traditional wear segment, influencing TCNS expansion strategy and market share dynamics.

Trade agreements and export incentives

Bilateral trade agreements through 2024–25, including India-UAE CEPA expansion and ASEAN-India tariff concessions, enable TCNS to target ~15–20% revenue growth from Middle East and Southeast Asia; exports to these regions rose 12% in FY2024. Political stability and diplomatic ties affect store rollouts and logistics costs—instability can raise freight/insurance by 5–10%. Recent export duty cuts on RMG in 2024 improved margins by ~80–120 bps.

- Target regions: Middle East, Southeast Asia — +12% exports FY2024

- Projected international revenue growth: 15–20%

- Logistics cost risk if instability: +5–10%

- Export duty cuts 2024: margin +80–120 bps

State-level labor law reforms

State-level labor law reforms in India, including consolidation into four labour codes since 2020, materially affect TCNS Clothing’s 400+ stores and multiple manufacturing units across states; changes increasing flexible hiring can reduce hourly labor costs by an estimated 5–8% but may raise compliance monitoring expenses.

Implementation of industrial flexibility provisions impacts workforce strategies—contract staffing rose ~12% in Indian retail in 2023—altering payroll mix and benefits liabilities for TCNS.

Stable state governments (e.g., Gujarat, Karnataka) correlate with fewer supply disruptions; states with frequent industrial actions saw inventory turnover slow by ~6% in 2022, risking retail revenue volatility.

- 400+ stores and multiple manufacturing sites across states

- Potential 5–8% reduction in hourly labor costs from flexible hiring

- Contract staffing up ~12% in retail (2023)

- Industrial actions linked to ~6% slower inventory turnover (2022)

Post‑ABFRL consolidation & PLI boost propel 7–9% ethnic retail growth, exports +12%

Post-ABFRL consolidation improves regulatory access and predictability; PLI textiles (INR 10,683 crore) raises capex subsidies; FDI rules favor domestic players sustaining 7–9% organised ethnic retail growth (2024–25); trade deals/exports (+12% FY2024) target 15–20% intl revenue; labour code reforms lower hourly costs 5–8% but increase compliance.

| Metric | Value |

|---|---|

| ABFRL FY2024 revenue | INR 21,318 cr |

| PLI allocation | INR 10,683 cr |

| Ethnic retail growth | 7–9% (2024–25) |

| Exports FY2024 | +12% |

| Labour cost impact | -5–8% |

What is included in the product

Explores how external macro-environmental factors uniquely affect TCNS Clothing across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications tailored to its Indian and global apparel markets to inform strategy, risk mitigation, and investor communications.

A concise, shareable TCNS Clothing PESTLE summary that’s visually segmented for quick interpretation, ideal for meetings, slide decks, and cross-team alignment while allowing note-taking for region- or business-specific context.

Economic factors

Recovery in discretionary consumer spending

By end-2025 India’s GDP growth normalised around 6.8%, fueling a rebound in urban middle-class consumption; retail discretionary spending rose ~9% YoY in FY25, lifting demand for lifestyle and fashion. TCNS brands W and Aurelia captured this uptick as urban women increased spend on branded ethnic wear for work and social occasions, supporting a shift toward higher average selling prices. The trend underpins TCNS’s premiumisation strategy, aiding margin expansion and higher ASPs.

Inflationary pressure on raw materials

Fluctuations in cotton, silk and synthetic fibre prices—cotton up ~18% in 2024 vs 2023, benchmark polyester resin rising ~12%—pressure TCNS Clothing’s cost base, forcing margin-tight choices in the ethnic wear segment. Rising input costs must be balanced against consumer price sensitivity after discretionary spends slowed in FY24; losing a 1–2% price competitiveness risks market-share erosion. Global commodity volatility makes advanced procurement, supplier diversification and hedging essential to protect FY25 gross margins.

Growth of the organized retail sector

The shift from unorganized boutiques to organized retail boosts TCNS, where organized retail in India reached ~17% of overall retail in 2024 and is projected to hit ~22% by 2027; TCNS’s ~650 EBOs and 2,500 MBOs (2025) capitalize on mall and branded-outlet traffic, increasing market share for Aurelia and Wishful and supporting compounded revenue growth—TCNS reported 18% retail channel revenue growth in FY2024, reflecting this structural tailwind.

E-commerce and omnichannel integration costs

Maintaining TCNS Clothing’s digital presence demands significant investment in platforms, IT and last-mile delivery—e-commerce and logistics capex rose industry-wide ~12–15% in 2024, with fashion return rates near 20–30% eroding margins.

Online channels now drive ~40–55% of apparel sales for comparable Indian brands in 2024–25, but elevated customer acquisition costs (often INR 400–800 per order) and returns compress profitability, forcing trade-offs between store expansion and digital spend.

- E-commerce share: ~40–55% of apparel sales (2024–25)

- Return rates: 20–30% in fashion (2024)

- Customer acquisition cost: ~INR 400–800/order (2024)

- Industry digital/logistics capex growth: ~12–15% (2024)

Interest rate environment and capital cost

Prevailing RBI policy rates — repo at 6.5% (Dec 2025) — raise TCNS’s borrowing costs for expansion and inventory; ABFRL backing secures lower spreads, improving access to ~8–9% effective borrowing versus standalone rates above 10% for peers.

Higher rates increase project discount rates, reducing NPV of store openings and omnichannel investments; elevated consumer credit costs can cut demand for premium lines like Wishful, where average ticket is ~₹2,500–3,500.

- Repo rate: 6.5% (Dec 2025)

- Estimated TCNS effective borrowing: ~8–9%

- Wishful avg ticket: ₹2,500–3,500

- Higher rates → lower NPV, weaker premium demand

Robust India demand lifts TCNS despite rising cotton costs and higher e‑commerce mix

Economic tailwinds: India GDP ~6.8% (2025) and retail discretionary +9% (FY25) boosted branded ethnic demand; cotton +18% (2024), polyester resin +12% raised input costs; organized retail ~17% (2024) to ~22% (2027) aided TCNS’s 650 EBOs/2,500 MBOs; e-commerce 40–55% share (2024–25) with CAC INR 400–800 and return rates 20–30%; repo 6.5% (Dec‑2025), TCNS borrowing ~8–9%.

| Metric | Value |

|---|---|

| GDP growth (2025) | 6.8% |

| Retail discretionary (FY25) | +9% YoY |

| Cotton (2024) | +18% |

| E‑commerce share | 40–55% |

Same Document Delivered

TCNS Clothing PESTLE Analysis

The preview shown here is the exact TCNS Clothing PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The file you’re seeing now is the final version, with no placeholders or teasers, delivered exactly as shown. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. Don’t just imagine what you’re getting—this is the real, finished file you’ll own upon checkout.