Wharf (Holdings) SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Wharf (Holdings) balances a diversified property and logistics portfolio with strong cash flows and strategic Hong Kong assets, yet faces cyclical property headwinds, regulatory risks, and regional competition; our full SWOT unpacks these dynamics with data-driven insights and tactical recommendations. Discover the complete picture—purchase the full SWOT analysis for a professionally formatted Word report and editable Excel tools to plan, pitch, or invest with confidence.

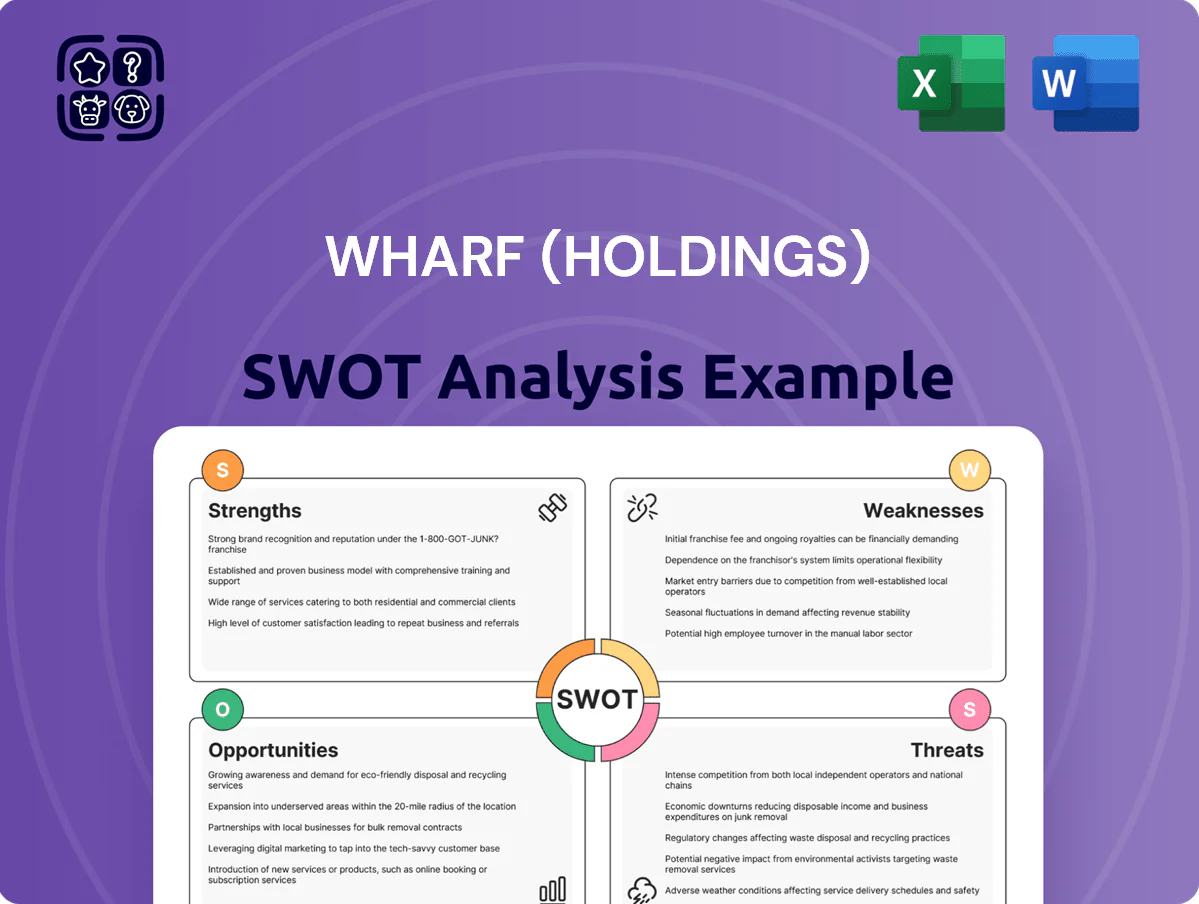

Strengths

Prime Real Estate Asset Portfolio

Wharf Holdings owns an iconic portfolio of commercial properties in Hong Kong and Mainland China, including Harbour City and Times Square, delivering recurring rental income—HK$17.4 billion in rental revenue in FY2024—and >85% occupancy with blue-chip tenants; these flagship malls and Grade-A offices in core districts create a location-based moat that supported NAV resilience, with investment property valuation up 4.2% to HK$245.8 billion as of Dec 31, 2024.

Strong Financial Liquidity and Balance Sheet

The group closed 2025 with net gearing around 18% and HK$28.6 billion in cash and equivalents, reflecting disciplined liability management and ample liquidity. This balance-sheet strength helps Wharf (Holdings) absorb market shocks and fund strategic acquisitions without heavy new borrowing. Investors in capital-intensive property value the stability those metrics signal.

Strategic Logistics Infrastructure Ownership

Through its interest in Modern Terminals, Wharf (Holdings) anchors container operations in the Pearl River Delta, handling ~4.2 million TEU p.a. across Hong Kong and Shenzhen in 2024, per company filings.

This logistics arm generated HKD 4.1bn EBITDA in FY2024, offering revenue less tied to cyclical property prices and acting as a natural hedge.

Established operational expertise and deep-water berths (up to 16m draft) keep Wharf a preferred hub for major international shipping lines.

Established Luxury Hospitality Brands

- Niccolo & Marco Polo: premium brands in Asia

- RevPAR (2024): ~HKD 1,450 at flagship hotels

- FY2024 hotel revenue growth: +28%

- Occupancy resilience vs mid-market: ~+10–15ppt

Prudent Capital Allocation and Investment Strategy

Management’s conservative capital allocation has driven steady dividend streams—Wharf (Holdings) reported HKD 5.6 billion in investment income in 2024—while holding diversified long-term stakes (Harbour City, i-CABLE, Wharf T&T) that support NAV uplift and upside through capital gains.

This diversified investment mix reduces reliance on cyclical property sales, stabilizes cash flow, and preserves balance-sheet flexibility for opportunistic acquisitions.

- 2024 investment income: HKD 5.6B

- Key strategic assets: Harbour City, i-CABLE, Wharf T&T

- Dividend support + capital gains potential

- Lower pure-play property risk

Wharf: Iconic HK assets, strong cashflow, low leverage and diversified logistics & hotels

Wharf (Holdings) combines an iconic HK/China property portfolio (Harbour City, Times Square) with steady rental income (HK$17.4bn FY2024), low net gearing (~18% end-2025) and HK$28.6bn cash, plus a logistics arm (~4.2m TEU, HK$4.1bn EBITDA FY2024) and premium hotels (Niccolo RevPAR ~HKD1,450 2024) that diversify cash flow and protect NAV.

| Metric | Value |

|---|---|

| Rental revenue FY2024 | HK$17.4bn |

| Investment property value (Dec 31, 2024) | HK$245.8bn |

| Net gearing (end-2025) | ~18% |

| Cash & equivalents | HK$28.6bn |

| Modern Terminals throughput 2024 | ~4.2m TEU |

| Logistics EBITDA FY2024 | HK$4.1bn |

| Niccolo RevPAR 2024 | HKD1,450 |

What is included in the product

Provides a concise SWOT overview of Wharf (Holdings), outlining its core strengths, operational weaknesses, market opportunities, and external threats to clarify strategic positioning and future prospects.

Delivers a concise Wharf (Holdings) SWOT matrix for quick strategic alignment, ideal for executives needing a snapshot of strengths, weaknesses, opportunities, and threats.

Weaknesses

Heavy Geographic Concentration in Greater China

Wharf (Holdings) concentrates over 85% of its 2024 revenue and NAV in Hong Kong and Mainland China, so regional GDP contraction or property cooling directly hits cash flow and asset values.

Unlike global peers, Wharf has minimal overseas revenue—less than 5%—limiting natural hedges against China-specific shocks.

This geographic focus increases exposure to Chinese regulatory actions; for example, 2023–24 property-policy tightening trimmed comparable rental income growth to under 2%.

Exposure to Volatile Mainland Property Markets

Sensitivity to Non-Cash Asset Revaluations

Wharf’s reported net profit often swings due to fair value changes on its investment property portfolio; in FY2024 the company booked HKD -4.1bn revaluation losses that cut reported profit but left operating cash flow largely intact. In 2022–24 higher global rates and a HK property correction increased write-down frequency, creating volatile quarterly earnings that can mask recurring retail and leasing cash returns. This accounting noise complicates valuation for retail investors.

High Capital Intensity of Core Operations

- Large upfront CapEx: HKD 8.3B in 2024

- Long payback: property cycles 5–10 years

- Net debt: HKD 38.5B (FY2024)

- Reinvestment need: ongoing asset upgrades

Limited Revenue Diversification Outside Core Sectors

- ~70% recurring EBITDA from property/logistics (FY2024)

- communications/media <10% of revenue

- ~HKD 2bn M&A spend since 2022

- 10% property EBIT drop → ~7% group EBIT impact

High HK/China concentration, heavy debt & CapEx risk; property slump could hit group EBIT

Heavy Hong Kong/China concentration (>85% revenue/NAV FY2024) and minimal overseas revenue (<5%) raise macro, policy and demand risk; FY2024 revaluation loss HKD -4.1bn added earnings volatility while net debt was HKD 38.5bn. Large CapEx (HKD 8.3bn 2024) and long payback (5–10 yrs) squeeze cashflow; ~70% recurring EBITDA from property/logistics leaves group sensitive to a 10% property EBIT drop (~7% group EBIT impact).

| Metric | Value |

|---|---|

| Revenue/NAV concentration HK/China | >85% (FY2024) |

| Overseas revenue | <5% |

| Revaluation loss | HKD -4.1bn (FY2024) |

| Net debt | HKD 38.5bn (End-2024) |

| CapEx | HKD 8.3bn (2024) |

| Recurring EBITDA from property/logistics | ~70% (FY2024) |

| Property EBIT sensitivity | 10% drop → ~7% group EBIT |

Full Version Awaits

Wharf (Holdings) SWOT Analysis

This is a real excerpt from the complete Wharf (Holdings) SWOT analysis you’ll receive upon purchase—no surprises, just professional quality and ready-to-use insights.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Wharf (Holdings) balances a diversified property and logistics portfolio with strong cash flows and strategic Hong Kong assets, yet faces cyclical property headwinds, regulatory risks, and regional competition; our full SWOT unpacks these dynamics with data-driven insights and tactical recommendations. Discover the complete picture—purchase the full SWOT analysis for a professionally formatted Word report and editable Excel tools to plan, pitch, or invest with confidence.

Strengths

Prime Real Estate Asset Portfolio

Wharf Holdings owns an iconic portfolio of commercial properties in Hong Kong and Mainland China, including Harbour City and Times Square, delivering recurring rental income—HK$17.4 billion in rental revenue in FY2024—and >85% occupancy with blue-chip tenants; these flagship malls and Grade-A offices in core districts create a location-based moat that supported NAV resilience, with investment property valuation up 4.2% to HK$245.8 billion as of Dec 31, 2024.

Strong Financial Liquidity and Balance Sheet

The group closed 2025 with net gearing around 18% and HK$28.6 billion in cash and equivalents, reflecting disciplined liability management and ample liquidity. This balance-sheet strength helps Wharf (Holdings) absorb market shocks and fund strategic acquisitions without heavy new borrowing. Investors in capital-intensive property value the stability those metrics signal.

Strategic Logistics Infrastructure Ownership

Through its interest in Modern Terminals, Wharf (Holdings) anchors container operations in the Pearl River Delta, handling ~4.2 million TEU p.a. across Hong Kong and Shenzhen in 2024, per company filings.

This logistics arm generated HKD 4.1bn EBITDA in FY2024, offering revenue less tied to cyclical property prices and acting as a natural hedge.

Established operational expertise and deep-water berths (up to 16m draft) keep Wharf a preferred hub for major international shipping lines.

Established Luxury Hospitality Brands

- Niccolo & Marco Polo: premium brands in Asia

- RevPAR (2024): ~HKD 1,450 at flagship hotels

- FY2024 hotel revenue growth: +28%

- Occupancy resilience vs mid-market: ~+10–15ppt

Prudent Capital Allocation and Investment Strategy

Management’s conservative capital allocation has driven steady dividend streams—Wharf (Holdings) reported HKD 5.6 billion in investment income in 2024—while holding diversified long-term stakes (Harbour City, i-CABLE, Wharf T&T) that support NAV uplift and upside through capital gains.

This diversified investment mix reduces reliance on cyclical property sales, stabilizes cash flow, and preserves balance-sheet flexibility for opportunistic acquisitions.

- 2024 investment income: HKD 5.6B

- Key strategic assets: Harbour City, i-CABLE, Wharf T&T

- Dividend support + capital gains potential

- Lower pure-play property risk

Wharf: Iconic HK assets, strong cashflow, low leverage and diversified logistics & hotels

Wharf (Holdings) combines an iconic HK/China property portfolio (Harbour City, Times Square) with steady rental income (HK$17.4bn FY2024), low net gearing (~18% end-2025) and HK$28.6bn cash, plus a logistics arm (~4.2m TEU, HK$4.1bn EBITDA FY2024) and premium hotels (Niccolo RevPAR ~HKD1,450 2024) that diversify cash flow and protect NAV.

| Metric | Value |

|---|---|

| Rental revenue FY2024 | HK$17.4bn |

| Investment property value (Dec 31, 2024) | HK$245.8bn |

| Net gearing (end-2025) | ~18% |

| Cash & equivalents | HK$28.6bn |

| Modern Terminals throughput 2024 | ~4.2m TEU |

| Logistics EBITDA FY2024 | HK$4.1bn |

| Niccolo RevPAR 2024 | HKD1,450 |

What is included in the product

Provides a concise SWOT overview of Wharf (Holdings), outlining its core strengths, operational weaknesses, market opportunities, and external threats to clarify strategic positioning and future prospects.

Delivers a concise Wharf (Holdings) SWOT matrix for quick strategic alignment, ideal for executives needing a snapshot of strengths, weaknesses, opportunities, and threats.

Weaknesses

Heavy Geographic Concentration in Greater China

Wharf (Holdings) concentrates over 85% of its 2024 revenue and NAV in Hong Kong and Mainland China, so regional GDP contraction or property cooling directly hits cash flow and asset values.

Unlike global peers, Wharf has minimal overseas revenue—less than 5%—limiting natural hedges against China-specific shocks.

This geographic focus increases exposure to Chinese regulatory actions; for example, 2023–24 property-policy tightening trimmed comparable rental income growth to under 2%.

Exposure to Volatile Mainland Property Markets

Sensitivity to Non-Cash Asset Revaluations

Wharf’s reported net profit often swings due to fair value changes on its investment property portfolio; in FY2024 the company booked HKD -4.1bn revaluation losses that cut reported profit but left operating cash flow largely intact. In 2022–24 higher global rates and a HK property correction increased write-down frequency, creating volatile quarterly earnings that can mask recurring retail and leasing cash returns. This accounting noise complicates valuation for retail investors.

High Capital Intensity of Core Operations

- Large upfront CapEx: HKD 8.3B in 2024

- Long payback: property cycles 5–10 years

- Net debt: HKD 38.5B (FY2024)

- Reinvestment need: ongoing asset upgrades

Limited Revenue Diversification Outside Core Sectors

- ~70% recurring EBITDA from property/logistics (FY2024)

- communications/media <10% of revenue

- ~HKD 2bn M&A spend since 2022

- 10% property EBIT drop → ~7% group EBIT impact

High HK/China concentration, heavy debt & CapEx risk; property slump could hit group EBIT

Heavy Hong Kong/China concentration (>85% revenue/NAV FY2024) and minimal overseas revenue (<5%) raise macro, policy and demand risk; FY2024 revaluation loss HKD -4.1bn added earnings volatility while net debt was HKD 38.5bn. Large CapEx (HKD 8.3bn 2024) and long payback (5–10 yrs) squeeze cashflow; ~70% recurring EBITDA from property/logistics leaves group sensitive to a 10% property EBIT drop (~7% group EBIT impact).

| Metric | Value |

|---|---|

| Revenue/NAV concentration HK/China | >85% (FY2024) |

| Overseas revenue | <5% |

| Revaluation loss | HKD -4.1bn (FY2024) |

| Net debt | HKD 38.5bn (End-2024) |

| CapEx | HKD 8.3bn (2024) |

| Recurring EBITDA from property/logistics | ~70% (FY2024) |

| Property EBIT sensitivity | 10% drop → ~7% group EBIT |

Full Version Awaits

Wharf (Holdings) SWOT Analysis

This is a real excerpt from the complete Wharf (Holdings) SWOT analysis you’ll receive upon purchase—no surprises, just professional quality and ready-to-use insights.