Wheaton Precious Metals SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Wheaton Precious Metals blends a low-cost streaming model with strong cash flow visibility, but faces metal price volatility and geopolitical exposure; our full SWOT unpacks these dynamics with financial context and strategic implications. Discover actionable insights and an editable report to support investment or corporate strategy—purchase the complete SWOT for the full, investor-ready analysis.

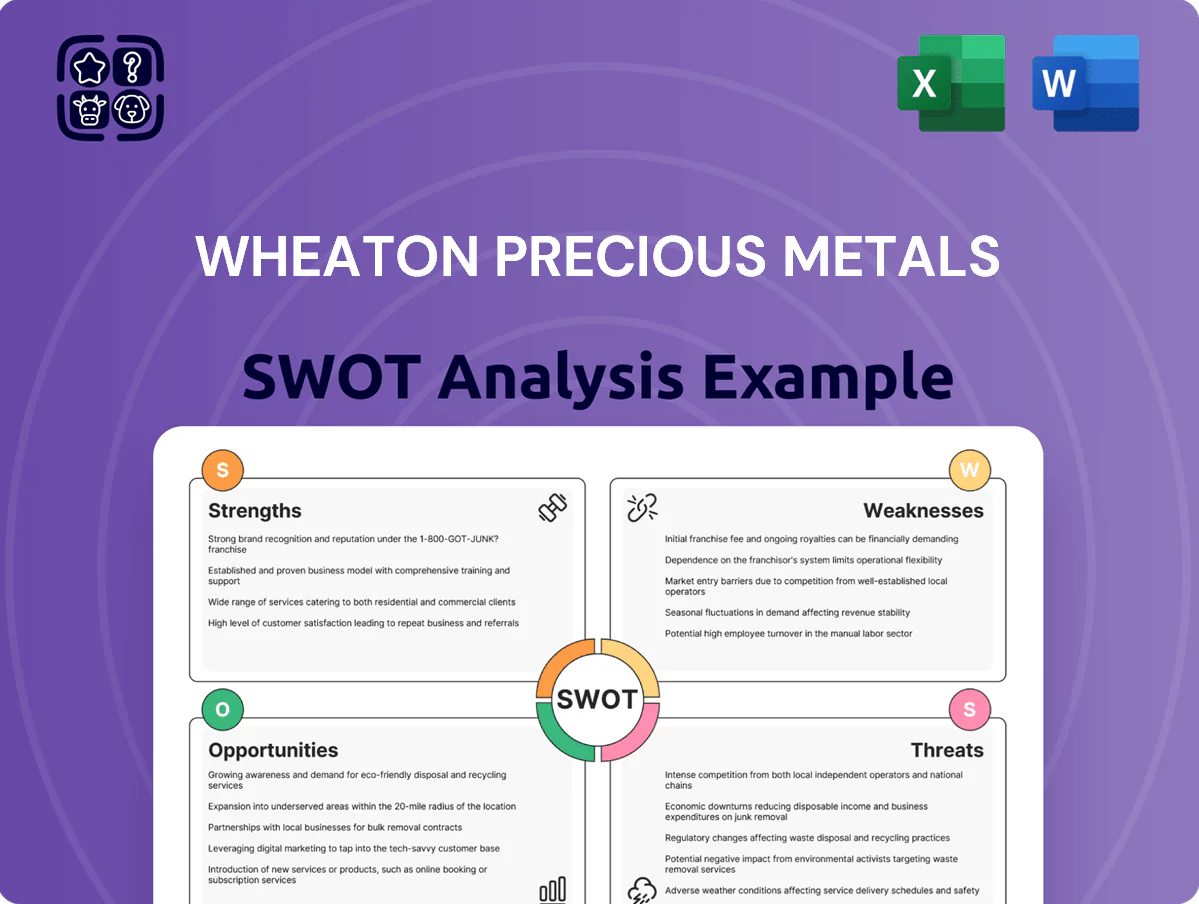

Strengths

High-Margin Business Model

Wheaton Precious Metals uses a streaming model that locks in fixed per-ounce payments well below spot prices, producing cash margins far above miners; in 2024 its adjusted operating margin was about 62%, vs ~25–30% for major producers.

Diversified Global Asset Portfolio

Wheaton Precious Metals holds a diversified portfolio of long-life streaming assets across politically stable, geologically rich jurisdictions in the Americas and Europe, covering over 40 producing and development-stage projects as of YE 2025 and supporting ~12% annual attributable payable silver and gold production growth guidance for 2025–2026.

Predictable Cash Flows and Low Overheads

Wheaton Precious Metals runs a very lean corporate model, avoiding the heavy capital expenditures miners face—2024 SG&A was about US$86m, keeping overheads low versus miners that reinvest billions. This allows ~70–80% of operating cash flow to fund dividends and new streams; in 2024 Wheaton returned US$360m in dividends and buybacks. Streaming contracts give clear visibility: 2025–2030 attributable metal production and fixed/variable payments are largely contracted, supporting predictable revenue streams.

Robust Balance Sheet and Liquidity

As of December 31, 2025, Wheaton Precious Metals (WPM) held net cash (cash minus debt) of about US$480 million and undrawn revolving credit capacity of US$750 million, giving low leverage (net debt/EBITDA ~0.2x) and quick access to capital.

This liquidity lets WPM move fast on high-value precious-metals streaming deals, often outbidding smaller peers, and cushions cash flows during commodity swings, supporting its quarterly dividend of US$0.11 per share.

- Net cash ~US$480M (Dec 31, 2025)

- Undrawn revolver US$750M

- Net debt/EBITDA ~0.2x

- Quarterly dividend US$0.11/share

Strategic ESG Integration

Wheaton Precious Metals leads the streaming sector on ESG, applying strict partner due diligence and funding community programs at mine sites, which lowers reputational and operational risk.

As of 2024, Wheaton reported 98% of streaming counterparties meeting its ESG screening and increased community investment to US$12.5m, making it more attractive to institutional investors with ESG mandates.

- 98% counterparties pass ESG screens

- US$12.5m community investment in 2024

- Lowered partner-related operational risk

- Stronger appeal to ESG-bound institutions

Wheaton: High‑margin, low‑risk streaming—$480M net cash, 40+ projects, 98% ESG pass

Wheaton’s streaming model yields high margins (2024 adj. operating margin ~62%) with long-life, diversified streams (40+ projects YE 2025) and predictable contracted cash flows; net cash ~US$480M, US$750M revolver, net debt/EBITDA ~0.2x, enabling US$360M returned in 2024 and a US$0.11/qtr dividend; strong ESG: 98% counterparties pass, US$12.5M community spend (2024).

| Metric | Value |

|---|---|

| Adj. op. margin (2024) | ~62% |

| Projects (YE 2025) | 40+ |

| Net cash (Dec 31, 2025) | US$480M |

| Undrawn revolver | US$750M |

| Net debt/EBITDA | ~0.2x |

| Returns (2024) | US$360M |

| Dividend | US$0.11/qtr |

| ESG pass rate (2024) | 98% |

| Community spend (2024) | US$12.5M |

What is included in the product

Provides a clear SWOT framework analyzing Wheaton Precious Metals’ strategic strengths, weaknesses, opportunities, and threats to assess its competitive position and future risks.

Delivers a focused SWOT summary of Wheaton Precious Metals for rapid strategic alignment and stakeholder-ready visuals.

Weaknesses

Dependency on Third-Party Operators

Wheaton Precious Metals lacks operational control because it holds streaming and royalty agreements rather than owning mines, so day-to-day production decisions rest with third-party operators.

If an operator suspends a mine—technical problems, strikes, or strategy changes—Wheaton’s attributable revenue stops immediately; in 2024 streaming cash flows showed volatility when two mid-tier operators cut output, trimming consolidated attributable silver ounces by about 9% year-over-year.

This dependency is a structural weakness versus integrated miners that can internally raise or lower production to smooth revenue and respond to price swings.

Exposure to Jurisdictional Risks

While Wheaton Precious Metals has a diversified streaming portfolio, about 60% of its attributable payable silver and gold exposure in 2024 came from projects in developing nations such as Mexico, Peru and Brazil, where legal and regulatory frameworks can be unpredictable.

Sudden changes to mining codes, royalty rules, or environmental laws—for example Peru’s 2024 draft taxation changes—can delay projects or raise operators’ costs, shrinking mined output.

Lower operator production reduces metals delivered under Wheaton’s streaming contracts, directly cutting realized volumes and pressuring recurring revenue; in 2024 a 10% production shortfall on major streams could shave roughly US$40–60m EBITDA.

Limited Influence Over Mine Life

The longevity of Wheaton Precious Metals’ revenue depends entirely on mine owners’ reserve replacement and exploration; in 2024 operators provided ~85% of production under streaming contracts but reserve additions fell 6% year-over-year, raising risk to future cashflows. If an operator cuts exploration or hits poor geology, a stream’s life can shrink below initial forecasts—Wheaton cannot compel owners to extend operations. Wheaton’s contracts offer limited remedies; economic closure or technical limits end payments once ore is exhausted, so NAV and 2025 guidance remain sensitive to counterparties’ capex choices.

Concentration in Gold and Silver

Wheaton Precious Metals remains heavily weighted to gold and silver—roughly 75% of attributable metal production in 2024 was gold and silver—which makes its share price highly sensitive to those metals’ moves.

This concentration gives strong upside in bull markets (gold +15% in 2024) but creates downside if prices stagnate or fall; a 10% gold drop cuts revenue notably.

Financials tie to macro factors like interest rates and inflation; real rates fell in 2024, boosting metal demand and Wheaton’s NAV.

- ~75% gold/silver exposure (2024)

- Gold up ~15% in 2024

- 10% metal drop → meaningful revenue hit

Vulnerability to Partner Financial Health

- Depends on partner solvency

- Deliveries can be delayed by bankruptcy

- Senior security helps, but recovery is slow

- 2024 mining bankruptcies +14% raises counterparty risk

Wheaton faces volatile revenue and legal risk as streaming shortfalls cut EBITDA $40–60m

Wheaton’s streaming model lacks operational control, making revenue volatile when operators cut output—2024 attributable silver ounces fell ~9%, and a 10% production shortfall could trim ~US$40–60m EBITDA.

About 60% of 2024 payable metals came from Mexico, Peru and Brazil, where rule changes (eg Peru 2024 tax draft) raise legal risk; mining bankruptcies rose ~14% in 2024, boosting counterparty risk.

| Metric | 2024 |

|---|---|

| Attributable silver change | -9% |

| Gold/silver share of metals | ~75% |

| Payable metals from developing nations | ~60% |

| Mining bankruptcies change | +14% |

| 10% shortfall EBITDA impact | US$40–60m |

Same Document Delivered

Wheaton Precious Metals SWOT Analysis

This is the actual Wheaton Precious Metals SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Wheaton Precious Metals blends a low-cost streaming model with strong cash flow visibility, but faces metal price volatility and geopolitical exposure; our full SWOT unpacks these dynamics with financial context and strategic implications. Discover actionable insights and an editable report to support investment or corporate strategy—purchase the complete SWOT for the full, investor-ready analysis.

Strengths

High-Margin Business Model

Wheaton Precious Metals uses a streaming model that locks in fixed per-ounce payments well below spot prices, producing cash margins far above miners; in 2024 its adjusted operating margin was about 62%, vs ~25–30% for major producers.

Diversified Global Asset Portfolio

Wheaton Precious Metals holds a diversified portfolio of long-life streaming assets across politically stable, geologically rich jurisdictions in the Americas and Europe, covering over 40 producing and development-stage projects as of YE 2025 and supporting ~12% annual attributable payable silver and gold production growth guidance for 2025–2026.

Predictable Cash Flows and Low Overheads

Wheaton Precious Metals runs a very lean corporate model, avoiding the heavy capital expenditures miners face—2024 SG&A was about US$86m, keeping overheads low versus miners that reinvest billions. This allows ~70–80% of operating cash flow to fund dividends and new streams; in 2024 Wheaton returned US$360m in dividends and buybacks. Streaming contracts give clear visibility: 2025–2030 attributable metal production and fixed/variable payments are largely contracted, supporting predictable revenue streams.

Robust Balance Sheet and Liquidity

As of December 31, 2025, Wheaton Precious Metals (WPM) held net cash (cash minus debt) of about US$480 million and undrawn revolving credit capacity of US$750 million, giving low leverage (net debt/EBITDA ~0.2x) and quick access to capital.

This liquidity lets WPM move fast on high-value precious-metals streaming deals, often outbidding smaller peers, and cushions cash flows during commodity swings, supporting its quarterly dividend of US$0.11 per share.

- Net cash ~US$480M (Dec 31, 2025)

- Undrawn revolver US$750M

- Net debt/EBITDA ~0.2x

- Quarterly dividend US$0.11/share

Strategic ESG Integration

Wheaton Precious Metals leads the streaming sector on ESG, applying strict partner due diligence and funding community programs at mine sites, which lowers reputational and operational risk.

As of 2024, Wheaton reported 98% of streaming counterparties meeting its ESG screening and increased community investment to US$12.5m, making it more attractive to institutional investors with ESG mandates.

- 98% counterparties pass ESG screens

- US$12.5m community investment in 2024

- Lowered partner-related operational risk

- Stronger appeal to ESG-bound institutions

Wheaton: High‑margin, low‑risk streaming—$480M net cash, 40+ projects, 98% ESG pass

Wheaton’s streaming model yields high margins (2024 adj. operating margin ~62%) with long-life, diversified streams (40+ projects YE 2025) and predictable contracted cash flows; net cash ~US$480M, US$750M revolver, net debt/EBITDA ~0.2x, enabling US$360M returned in 2024 and a US$0.11/qtr dividend; strong ESG: 98% counterparties pass, US$12.5M community spend (2024).

| Metric | Value |

|---|---|

| Adj. op. margin (2024) | ~62% |

| Projects (YE 2025) | 40+ |

| Net cash (Dec 31, 2025) | US$480M |

| Undrawn revolver | US$750M |

| Net debt/EBITDA | ~0.2x |

| Returns (2024) | US$360M |

| Dividend | US$0.11/qtr |

| ESG pass rate (2024) | 98% |

| Community spend (2024) | US$12.5M |

What is included in the product

Provides a clear SWOT framework analyzing Wheaton Precious Metals’ strategic strengths, weaknesses, opportunities, and threats to assess its competitive position and future risks.

Delivers a focused SWOT summary of Wheaton Precious Metals for rapid strategic alignment and stakeholder-ready visuals.

Weaknesses

Dependency on Third-Party Operators

Wheaton Precious Metals lacks operational control because it holds streaming and royalty agreements rather than owning mines, so day-to-day production decisions rest with third-party operators.

If an operator suspends a mine—technical problems, strikes, or strategy changes—Wheaton’s attributable revenue stops immediately; in 2024 streaming cash flows showed volatility when two mid-tier operators cut output, trimming consolidated attributable silver ounces by about 9% year-over-year.

This dependency is a structural weakness versus integrated miners that can internally raise or lower production to smooth revenue and respond to price swings.

Exposure to Jurisdictional Risks

While Wheaton Precious Metals has a diversified streaming portfolio, about 60% of its attributable payable silver and gold exposure in 2024 came from projects in developing nations such as Mexico, Peru and Brazil, where legal and regulatory frameworks can be unpredictable.

Sudden changes to mining codes, royalty rules, or environmental laws—for example Peru’s 2024 draft taxation changes—can delay projects or raise operators’ costs, shrinking mined output.

Lower operator production reduces metals delivered under Wheaton’s streaming contracts, directly cutting realized volumes and pressuring recurring revenue; in 2024 a 10% production shortfall on major streams could shave roughly US$40–60m EBITDA.

Limited Influence Over Mine Life

The longevity of Wheaton Precious Metals’ revenue depends entirely on mine owners’ reserve replacement and exploration; in 2024 operators provided ~85% of production under streaming contracts but reserve additions fell 6% year-over-year, raising risk to future cashflows. If an operator cuts exploration or hits poor geology, a stream’s life can shrink below initial forecasts—Wheaton cannot compel owners to extend operations. Wheaton’s contracts offer limited remedies; economic closure or technical limits end payments once ore is exhausted, so NAV and 2025 guidance remain sensitive to counterparties’ capex choices.

Concentration in Gold and Silver

Wheaton Precious Metals remains heavily weighted to gold and silver—roughly 75% of attributable metal production in 2024 was gold and silver—which makes its share price highly sensitive to those metals’ moves.

This concentration gives strong upside in bull markets (gold +15% in 2024) but creates downside if prices stagnate or fall; a 10% gold drop cuts revenue notably.

Financials tie to macro factors like interest rates and inflation; real rates fell in 2024, boosting metal demand and Wheaton’s NAV.

- ~75% gold/silver exposure (2024)

- Gold up ~15% in 2024

- 10% metal drop → meaningful revenue hit

Vulnerability to Partner Financial Health

- Depends on partner solvency

- Deliveries can be delayed by bankruptcy

- Senior security helps, but recovery is slow

- 2024 mining bankruptcies +14% raises counterparty risk

Wheaton faces volatile revenue and legal risk as streaming shortfalls cut EBITDA $40–60m

Wheaton’s streaming model lacks operational control, making revenue volatile when operators cut output—2024 attributable silver ounces fell ~9%, and a 10% production shortfall could trim ~US$40–60m EBITDA.

About 60% of 2024 payable metals came from Mexico, Peru and Brazil, where rule changes (eg Peru 2024 tax draft) raise legal risk; mining bankruptcies rose ~14% in 2024, boosting counterparty risk.

| Metric | 2024 |

|---|---|

| Attributable silver change | -9% |

| Gold/silver share of metals | ~75% |

| Payable metals from developing nations | ~60% |

| Mining bankruptcies change | +14% |

| 10% shortfall EBITDA impact | US$40–60m |

Same Document Delivered

Wheaton Precious Metals SWOT Analysis

This is the actual Wheaton Precious Metals SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version.