Whitehaven Coal Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

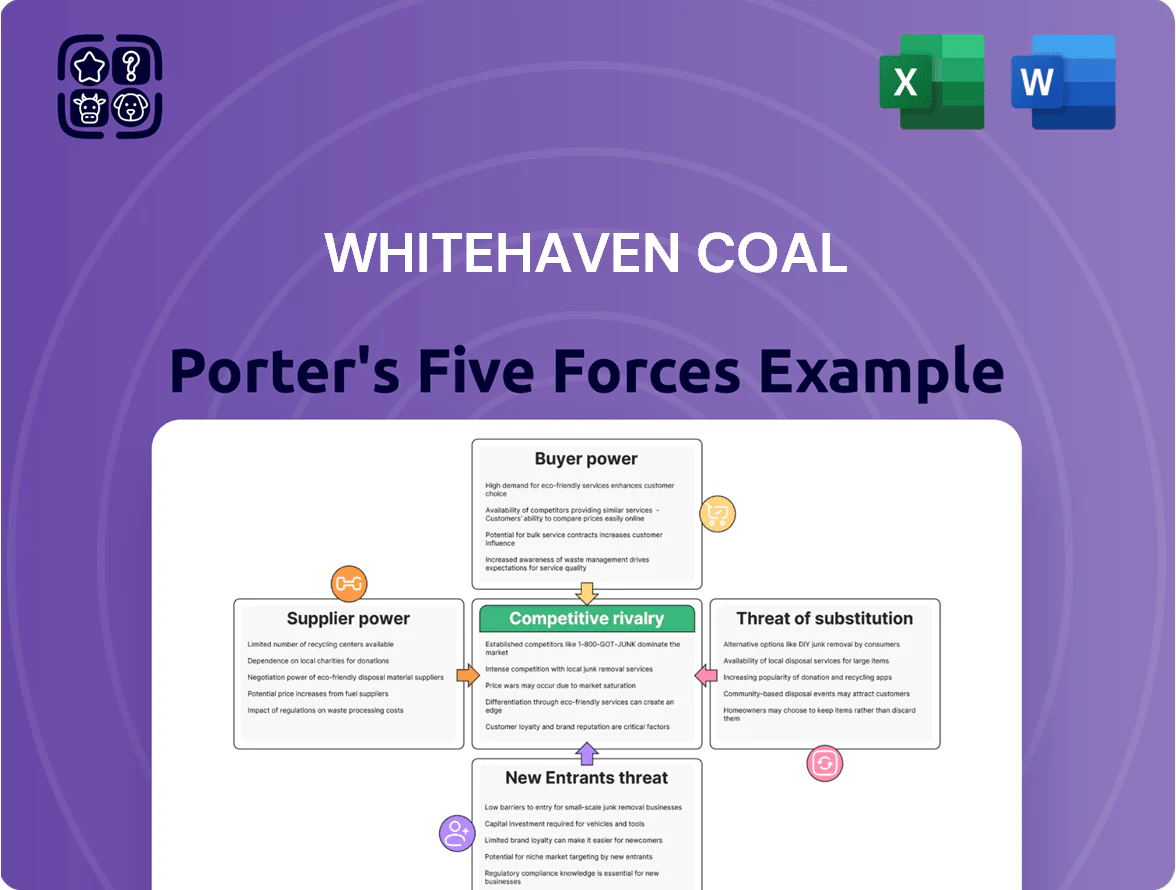

Whitehaven Coal faces intense rivalry from larger miners, regulatory and environmental pressures, and concentrated buyer power that squeeze margins, while supplier leverage and limited viable substitutes shape operational risk—this snapshot highlights critical pressures shaping strategy and valuation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Whitehaven Coal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Labor and Union Influence

The Australian mining sector faced a 2025 shortfall of ~12–15% in skilled mining engineers and technicians, tightening supplier (labor) power and raising recruitment costs for Whitehaven Coal; specialized labor scarcity pushes premium wages and contractor rates up to 18% year-on-year.

Strong unions in New South Wales and Queensland—covering ~70% of Whitehaven’s workforce—have secured enterprise bargains lifting base wages by ~7–10% in 2024–25, increasing operating costs and EBITDA pressure.

Higher labor costs plus a 4–6% probability of industrial actions in the coal belts risk production outages; a 1–3% hit to annual coal volumes would materially compress margins and cash flow.

Heavy Equipment and OEM Concentration

The supply of ultra-class haul trucks and specialized mining gear is concentrated among a few OEMs such as Caterpillar and Komatsu, giving suppliers high bargaining power; global market share for these OEMs exceeds 70% in the >100‑ton class as of 2024. Long lead times (12–24 months for new units) and multi-year parts backlogs raise dependency, and Whitehaven Coal’s fleet reliance limits price negotiation and forces capital timing tied to vendor availability.

Monopolistic Infrastructure Providers

Whitehaven Coal depends on rail and port links from Gunnedah and Bowen Basins; Australian Rail Track Corporation and major terminal operators act like natural monopolies with regulated tariffs, leaving limited alternatives.

In 2024, rail and port fees made up about 12–18% of A$ per-tonne FOB cash costs for NSW/QLD producers, so tariff rises materially cut margins and Whitehaven has little leverage to contest access terms.

Energy and Fuel Input Costs

Energy and fuel costs sharply affect Whitehaven Coal’s margins: diesel for trucks and gensets and grid electricity for processing account for roughly 8–12% of COGS; a US$10/bbl move in oil alters diesel cost by about 3–4% of operating expense. Whitehaven can hedge some exposures, but remains a price taker in global oil and domestic electricity markets, so volatility in Brent or spot NEM (National Electricity Market) rates hits EBITDA with limited negotiation power.

- Diesel + electricity ≈ 8–12% COGS

- US$10/bbl oil → ~3–4% Opex change

- Hedging reduces but not removes risk

- Spot NEM swings directly impact margins

Regulatory and Sovereign Constraints

The Australian federal and state governments control mining licences and environmental permits, effectively acting as suppliers of the legal right to mine; in 2024 Queensland collected A$3.2bn in coal royalties, showing fiscal leverage over miners.

Changes in royalty rates or stricter environmental rules (eg. NSW/QLD 2023-24 compliance updates) raise operating costs and force Whitehaven Coal to comply to retain its social licence.

High supplier power: concentrated OEMs, long lead times, rising costs & royalties

Supplier power is high: concentrated OEMs (Caterpillar/Komatsu >70% share) + 12–24m lead times; rail/port tariffs = 12–18% FOB costs; diesel+electricity ≈8–12% COGS (US$10/bbl → ~3–4% opex); skilled labor shortfall 12–15% and unions lift wages 7–10%; Queensland coal royalties A$3.2bn (2024) tighten regulatory leverage.

| Factor | Key number |

|---|---|

| OEM concentration | >70% |

| Lead times | 12–24 months |

| Rail/port fees | 12–18% FOB |

| Energy share | 8–12% COGS |

| Labor shortfall | 12–15% |

| Union wage rise | 7–10% |

| Royalties (QLD) | A$3.2bn (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Whitehaven Coal, detailing competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats to spotlight strategic risks and opportunities within the coal sector.

Concise Porter's Five Forces summary for Whitehaven Coal—quickly spot strategic pressures and relieve decision-making bottlenecks for investors and managers.

Customers Bargaining Power

Concentration of Asian Steelmakers

Following Whitehaven Coal’s acquisition of major metallurgical coal assets, sales now concentrate with a handful of Asian steelmakers—Japan, South Korea, and India—who together accounted for roughly 60–70% of met coal liftings in 2024; these sophisticated buyers coordinate buying and wield volume leverage in negotiations, enabling them to push prices down, evidenced by a 25% drop in benchmark hard coking coal prices in H2 2024 during global steel demand cooling.

Shift Toward Spot Market Pricing

The coal market shifted toward index-linked spot pricing: by 2024 Asia-Pacific thermal coal spot prices swung 40% year-on-year and seaborne metallurgical coal benchmarks rose 28% in 2023-24, letting buyers time purchases and extract lower prices; this boosts customer bargaining power over Whitehaven.

Whitehaven now tracks global indexes (Newcastle, Platts, ICE) and sells ~60% of production on spot or index-linked deals in 2024, making the company reactive to short-term benchmarks rather than long-term price certainty.

Availability of Alternative Global Supply

Customers in the Indo-Pacific can switch to suppliers in Indonesia, South Africa, or North America; Indonesia supplied ~500 Mt thermal coal in 2024, keeping regional options large. If Whitehaven Coal’s price sits above global benchmarks (Newcastle index averaged US$120/t in 2024), buyers shift to comparable-quality sellers offering better terms. High shipping liquidity—global dry bulk fleet ~800m DWT in 2024—makes switching quick, capping Whitehaven’s pricing power.

Decarbonization Targets and Green Steel

Major corporate customers with net-zero targets—over 2,000 global firms covering 25% of emissions by 2025—push for lower-emission fuels and green-steel routes, raising buyer leverage over coal suppliers.

Buyers demand low-ash, low-sulfur, high-calorific coal to meet scope 3 goals; Whitehaven must prove product quality and emissions intensity to stay preferred.

Whitehaven’s FY2024 EBITDA fell 18% so proving efficiency and partnering on abatement tech is critical to retain large steel buyers.

- Buyers: stronger leverage via net-zero pledges (2,000+ firms)

- Demand: low-impurity, high-calorific coal

- Risk: market share loss if product fails emissions tests

- Action: certify quality, report emissions intensity, co-invest in abatement

Price Sensitivity in Developing Markets

Developing markets such as India and Vietnam show strong coal demand but high price sensitivity; in 2024 India imported about 250 Mt of coal and swung purchases quickly when seaborne thermal prices rose above $120/t.

Buyers shift between coal grades and to gas or renewables if prices spike; a 2023 IEA note found fuel switching accelerated when coal price premia exceeded $15–20/t versus alternatives.

Whitehaven must balance quality—low-ash, high-calorific product premiums of ~$5–$12/t—with competitive pricing to retain contracts and volume.

- India imports ~250 Mt (2024); very price-sensitive

- Fuel switching triggered >$15–$20/t coal premium

- Whitehaven quality premium ~$5–$12/t

Buyers’ leverage caps met‑coal pricing as supply, fleet and net‑zero shifts bite

Buyers hold strong leverage: top Asian steelmakers accounted for ~60–70% of Whitehaven’s met-coal liftings in 2024, >60% of sales on spot/index-linked contracts, and rapid supplier switching (Indonesia ~500 Mt thermal coal, global dry bulk ~800m DWT) caps pricing; net-zero pressure from 2,000+ firms and fuel-switch triggers at >$15–$20/t further strengthen customer bargaining power.

| Metric | 2024 Value |

|---|---|

| Top buyers share | 60–70% |

| Spot/index sales | ~60% |

| Indonesia thermal supply | ~500 Mt |

| Dry bulk fleet | ~800m DWT |

| Net-zero firms | 2,000+ |

Same Document Delivered

Whitehaven Coal Porter's Five Forces Analysis

This preview shows the exact Whitehaven Coal Porter's Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups.

The file displayed is the final, professionally formatted document ready for download and use the moment you buy.

What you see is the deliverable: a complete, ready-to-use analysis available instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Whitehaven Coal faces intense rivalry from larger miners, regulatory and environmental pressures, and concentrated buyer power that squeeze margins, while supplier leverage and limited viable substitutes shape operational risk—this snapshot highlights critical pressures shaping strategy and valuation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Whitehaven Coal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Labor and Union Influence

The Australian mining sector faced a 2025 shortfall of ~12–15% in skilled mining engineers and technicians, tightening supplier (labor) power and raising recruitment costs for Whitehaven Coal; specialized labor scarcity pushes premium wages and contractor rates up to 18% year-on-year.

Strong unions in New South Wales and Queensland—covering ~70% of Whitehaven’s workforce—have secured enterprise bargains lifting base wages by ~7–10% in 2024–25, increasing operating costs and EBITDA pressure.

Higher labor costs plus a 4–6% probability of industrial actions in the coal belts risk production outages; a 1–3% hit to annual coal volumes would materially compress margins and cash flow.

Heavy Equipment and OEM Concentration

The supply of ultra-class haul trucks and specialized mining gear is concentrated among a few OEMs such as Caterpillar and Komatsu, giving suppliers high bargaining power; global market share for these OEMs exceeds 70% in the >100‑ton class as of 2024. Long lead times (12–24 months for new units) and multi-year parts backlogs raise dependency, and Whitehaven Coal’s fleet reliance limits price negotiation and forces capital timing tied to vendor availability.

Monopolistic Infrastructure Providers

Whitehaven Coal depends on rail and port links from Gunnedah and Bowen Basins; Australian Rail Track Corporation and major terminal operators act like natural monopolies with regulated tariffs, leaving limited alternatives.

In 2024, rail and port fees made up about 12–18% of A$ per-tonne FOB cash costs for NSW/QLD producers, so tariff rises materially cut margins and Whitehaven has little leverage to contest access terms.

Energy and Fuel Input Costs

Energy and fuel costs sharply affect Whitehaven Coal’s margins: diesel for trucks and gensets and grid electricity for processing account for roughly 8–12% of COGS; a US$10/bbl move in oil alters diesel cost by about 3–4% of operating expense. Whitehaven can hedge some exposures, but remains a price taker in global oil and domestic electricity markets, so volatility in Brent or spot NEM (National Electricity Market) rates hits EBITDA with limited negotiation power.

- Diesel + electricity ≈ 8–12% COGS

- US$10/bbl oil → ~3–4% Opex change

- Hedging reduces but not removes risk

- Spot NEM swings directly impact margins

Regulatory and Sovereign Constraints

The Australian federal and state governments control mining licences and environmental permits, effectively acting as suppliers of the legal right to mine; in 2024 Queensland collected A$3.2bn in coal royalties, showing fiscal leverage over miners.

Changes in royalty rates or stricter environmental rules (eg. NSW/QLD 2023-24 compliance updates) raise operating costs and force Whitehaven Coal to comply to retain its social licence.

High supplier power: concentrated OEMs, long lead times, rising costs & royalties

Supplier power is high: concentrated OEMs (Caterpillar/Komatsu >70% share) + 12–24m lead times; rail/port tariffs = 12–18% FOB costs; diesel+electricity ≈8–12% COGS (US$10/bbl → ~3–4% opex); skilled labor shortfall 12–15% and unions lift wages 7–10%; Queensland coal royalties A$3.2bn (2024) tighten regulatory leverage.

| Factor | Key number |

|---|---|

| OEM concentration | >70% |

| Lead times | 12–24 months |

| Rail/port fees | 12–18% FOB |

| Energy share | 8–12% COGS |

| Labor shortfall | 12–15% |

| Union wage rise | 7–10% |

| Royalties (QLD) | A$3.2bn (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Whitehaven Coal, detailing competitive rivalry, supplier and buyer power, barriers to entry, and substitute threats to spotlight strategic risks and opportunities within the coal sector.

Concise Porter's Five Forces summary for Whitehaven Coal—quickly spot strategic pressures and relieve decision-making bottlenecks for investors and managers.

Customers Bargaining Power

Concentration of Asian Steelmakers

Following Whitehaven Coal’s acquisition of major metallurgical coal assets, sales now concentrate with a handful of Asian steelmakers—Japan, South Korea, and India—who together accounted for roughly 60–70% of met coal liftings in 2024; these sophisticated buyers coordinate buying and wield volume leverage in negotiations, enabling them to push prices down, evidenced by a 25% drop in benchmark hard coking coal prices in H2 2024 during global steel demand cooling.

Shift Toward Spot Market Pricing

The coal market shifted toward index-linked spot pricing: by 2024 Asia-Pacific thermal coal spot prices swung 40% year-on-year and seaborne metallurgical coal benchmarks rose 28% in 2023-24, letting buyers time purchases and extract lower prices; this boosts customer bargaining power over Whitehaven.

Whitehaven now tracks global indexes (Newcastle, Platts, ICE) and sells ~60% of production on spot or index-linked deals in 2024, making the company reactive to short-term benchmarks rather than long-term price certainty.

Availability of Alternative Global Supply

Customers in the Indo-Pacific can switch to suppliers in Indonesia, South Africa, or North America; Indonesia supplied ~500 Mt thermal coal in 2024, keeping regional options large. If Whitehaven Coal’s price sits above global benchmarks (Newcastle index averaged US$120/t in 2024), buyers shift to comparable-quality sellers offering better terms. High shipping liquidity—global dry bulk fleet ~800m DWT in 2024—makes switching quick, capping Whitehaven’s pricing power.

Decarbonization Targets and Green Steel

Major corporate customers with net-zero targets—over 2,000 global firms covering 25% of emissions by 2025—push for lower-emission fuels and green-steel routes, raising buyer leverage over coal suppliers.

Buyers demand low-ash, low-sulfur, high-calorific coal to meet scope 3 goals; Whitehaven must prove product quality and emissions intensity to stay preferred.

Whitehaven’s FY2024 EBITDA fell 18% so proving efficiency and partnering on abatement tech is critical to retain large steel buyers.

- Buyers: stronger leverage via net-zero pledges (2,000+ firms)

- Demand: low-impurity, high-calorific coal

- Risk: market share loss if product fails emissions tests

- Action: certify quality, report emissions intensity, co-invest in abatement

Price Sensitivity in Developing Markets

Developing markets such as India and Vietnam show strong coal demand but high price sensitivity; in 2024 India imported about 250 Mt of coal and swung purchases quickly when seaborne thermal prices rose above $120/t.

Buyers shift between coal grades and to gas or renewables if prices spike; a 2023 IEA note found fuel switching accelerated when coal price premia exceeded $15–20/t versus alternatives.

Whitehaven must balance quality—low-ash, high-calorific product premiums of ~$5–$12/t—with competitive pricing to retain contracts and volume.

- India imports ~250 Mt (2024); very price-sensitive

- Fuel switching triggered >$15–$20/t coal premium

- Whitehaven quality premium ~$5–$12/t

Buyers’ leverage caps met‑coal pricing as supply, fleet and net‑zero shifts bite

Buyers hold strong leverage: top Asian steelmakers accounted for ~60–70% of Whitehaven’s met-coal liftings in 2024, >60% of sales on spot/index-linked contracts, and rapid supplier switching (Indonesia ~500 Mt thermal coal, global dry bulk ~800m DWT) caps pricing; net-zero pressure from 2,000+ firms and fuel-switch triggers at >$15–$20/t further strengthen customer bargaining power.

| Metric | 2024 Value |

|---|---|

| Top buyers share | 60–70% |

| Spot/index sales | ~60% |

| Indonesia thermal supply | ~500 Mt |

| Dry bulk fleet | ~800m DWT |

| Net-zero firms | 2,000+ |

Same Document Delivered

Whitehaven Coal Porter's Five Forces Analysis

This preview shows the exact Whitehaven Coal Porter's Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups.

The file displayed is the final, professionally formatted document ready for download and use the moment you buy.

What you see is the deliverable: a complete, ready-to-use analysis available instantly after payment.