Whiting-Turner Contracting Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

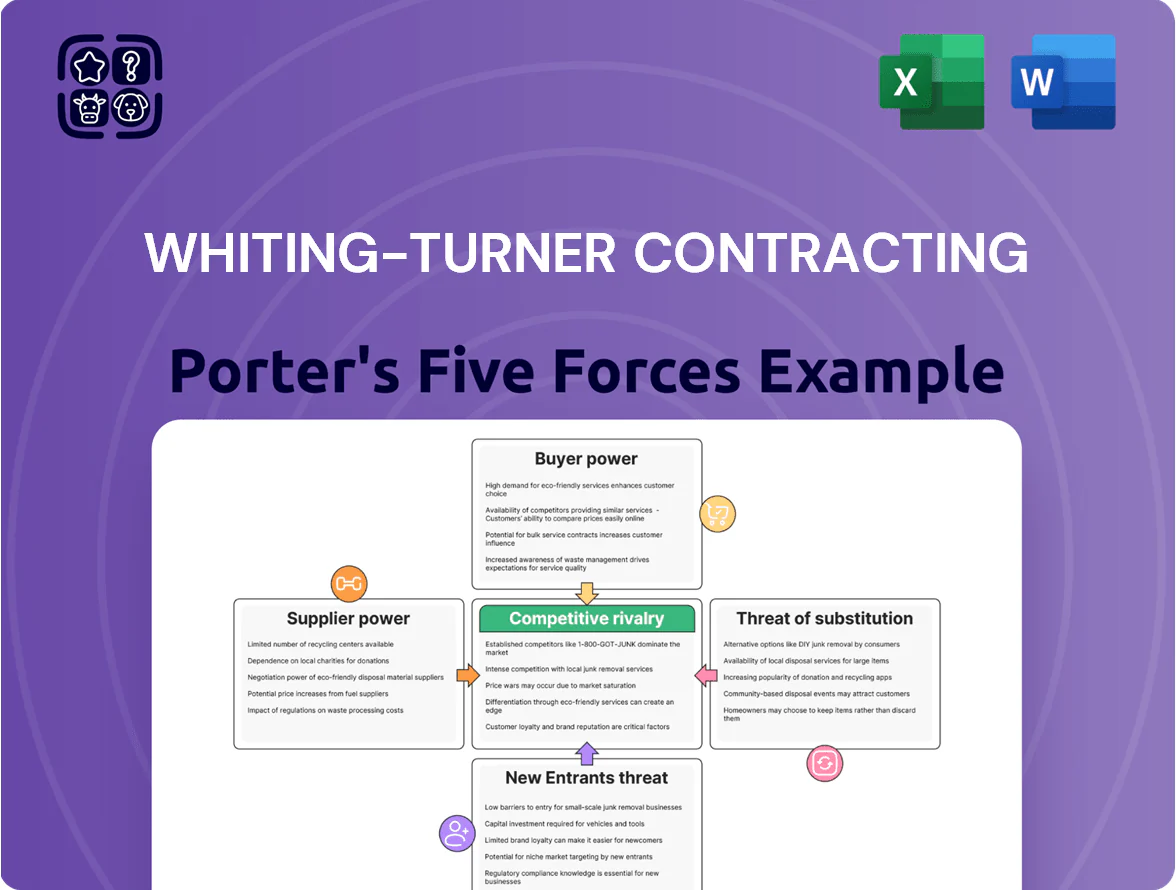

Whiting‑Turner faces moderate supplier leverage, intense bidder competition on large projects, and regulatory hurdles that raise entry costs—yet its scale and reputation create durable customer loyalty and bidding advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Whiting‑Turner’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Skilled Labor Scarcity

The U.S. construction sector faces a chronic shortage of skilled trades; as of Q4 2025, BLS data show 14% fewer licensed electricians and 12% fewer HVAC/mechanical techs versus demand in data center and healthcare projects, letting subcontractors raise rates 10–25% year-over-year and boosting their bargaining power against Whiting-Turner.

Whiting-Turner must secure priority access by maintaining long-term subcontractor agreements, offering 5–10% premium pay or faster payments, and investing in joint training programs to mitigate delays and keep margins intact.

Raw Material Price Volatility

Suppliers of structural steel, concrete, and specialty glass hold substantial leverage amid global supply-chain shocks; steel futures rose 28% in 2021–2023 and were still 9% above 2019 levels in 2024, raising input risk for Whiting-Turner.

Whiting-Turner’s $7.6B 2024 revenue and scale enable better contract terms and bulk buys, but commodity sensitivity to geopolitics and carbon rules keeps price exposure material.

Therefore the firm uses early procurement and fixed-price buyouts—locking up to 12–18 months ahead on major projects—to protect margins and reduce variation.

Specialized Equipment Providers

Energy and Logistics Costs

Suppliers of transportation and logistics gained leverage as U.S. diesel prices rose 23% in 2024 and new state-level carbon fees added $3–12 per tonne CO2, raising heavy-material haul costs contractors pay.

Delivery of modular units and bulk aggregates now drives site overheads; carriers commonly pass 5–12% fuel-surcharge hikes to general contractors on long-haul jobs.

Whiting-Turner must model region-specific fuel, toll, and carbon fees when budgeting national projects to avoid 2–6% margin erosion on large builds.

- 2024 U.S. average diesel +23%

- Carbon fees $3–12/tonne CO2

- Carrier fuel surcharges 5–12%

- Budget risk: 2–6% margin erosion

Strategic Subcontractor Partnerships

In niche sectors like biotech and microelectronics, fewer than 50 qualified subcontractors nationally give those firms high bargaining power; Whiting-Turner signs exclusive or multi-year deals—often 3–7 years—to prevent poaching and secure capacity.

This creates mutual dependency: subcontractor technical skill drives project feasibility while Whiting-Turner provides 30–40% of project management value, aligning incentives and lowering schedule risk.

- Fewer than 50 specialists nationwide

- Typical exclusive deals: 3–7 years

- Subcontractor expertise equals contractor management value

- Deal reduces schedule and poaching risk

Suppliers Gain Leverage; Whiting-Turner Buys Lead Time, Pays Premiums

Suppliers (skilled trades, steel, heavy equipment, logistics) hold medium–high bargaining power vs Whiting-Turner due to labor shortages, stretched lead times (26–34 weeks), and commodity/transport cost rises (steel +9% vs 2019; diesel +23% in 2024). Whiting-Turner counters with long-term subcontractor deals, 5–10% pay premiums, early procurement (12–18 months), and occasional upfront capex financing (10–15% job value).

| Metric | Value |

|---|---|

| Lead times (median) | 26–34 wks |

| Diesel change (2024) | +23% |

| Steel vs 2019 (2024) | +9% |

| Subcontractor pay premium | 5–10% |

| Procurement horizon | 12–18 mos |

What is included in the product

Provides a concise Porter’s Five Forces assessment for Whiting‑Turner Contracting, highlighting competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategy and valuation.

A concise Porter's Five Forces one-sheet for Whiting-Turner—quickly spot supplier, buyer, entrant, substitute, and rivalry pressures to streamline strategic decisions.

Customers Bargaining Power

Institutional Client Sophistication

Whiting-Turner serves high-end healthcare, education, and technology clients whose procurement teams cut average management fees by 5–12% during contract rounds; these institutional buyers demand strict KPIs and risk transfer clauses. Clients with deep market knowledge scrutinize line-item costs—procurement-led projects now award 62% of contracts via competitive RFPs (2024 AIA data). Transparent benchmarking tools let clients compare hourly rates and margin structures across top-tier firms, squeezing pricing power.

Competitive Bidding Environments

The widespread Request for Proposal (RFP) process lets clients pit major contractors like Whiting-Turner against each other, driving bid-driven contracts where average bid discounts of 5–12% off list prices are common in US commercial projects (2024 AIA data).

Private clients routinely invite multiple national firms to bid—studies show 60–70% of mid-size commercial projects see 3+ national bidders—keeping general contractor margins around 3–6% EBITDA.

That buyer leverage also forces contractors to include add-ons—sustainability upgrades or enhanced scheduling—often at minimal extra cost, with green spec premiums commonly limited to 1–3% of contract value.

Low Switching Costs for Future Phases

While mid-project contractor swaps are hard, clients can switch firms for future phases with low friction, so Whiting-Turner must deliver near-perfect results to win repeat work.

In 2024 US construction owners awarded 22% of follow-on contracts to new contractors, so one safety or schedule lapse can cost multi-million repeat revenue.

Competitors like Turner Construction and Gilbane drive this pressure—Whiting-Turner faces dozens of high-quality bidders on large projects, raising churn risk from single failures.

Demand for Integrated Technology

Clients demand BIM and real-time tracking as standard by end-2025, pushing Whiting-Turner to adopt platforms clients specify and meet reporting cadences as frequent as daily.

Customers dictate software choice and reporting, forcing heavy upfront digital investments—industry data shows construction tech spend rose 18% in 2024, and BIM implementation costs average $150–250k per large project.

This shifts adaptation costs to the contractor while clients capture long-term operational ROI, often 8–15% lifecycle savings from BIM and real-time data.

- Clients set platform + frequency

- 2024 tech spend +18%

- BIM cost $150–250k/project

- Client ROI 8–15% lifecycle

Emphasis on ESG and Diversity Goals

Major corporate and government clients now mandate strict ESG metrics and minority-owned business participation; in 2024, 68% of US public-sector RFPs included formal diversity or carbon targets, raising disqualification risk for noncompliant contractors.

Customers can reject bidders failing diversity spend or carbon reduction goals; a 2025 NY state procurement rule requires 15% minority-owned subcontractor spend on many projects, directly affecting eligibility.

Whiting-Turner must align its supply chain to these mandates to keep access to large public/private contracts worth billions annually; missed targets could cost market share and contract awards.

- 68% of 2024 public RFPs had ESG/diversity clauses

- NY 2025: 15% minority-owned subcontractor requirement

- Supply-chain alignment needed to retain billion-dollar contracts

RFP-driven squeeze: buyers wield discounts, rising tech/ESG costs, NY diversity rule ups churn

Buyers hold strong leverage: 62% of contracts via RFPs (AIA 2024), typical bid discounts 5–12%, and GC EBITDA 3–6%; tech spend up 18% (2024) with BIM costs $150–250k/project and client lifecycle ROI 8–15%; 68% public RFPs had ESG/diversity clauses (2024) and NY 2025 rule: 15% minority subcontractor spend, raising disqualification risk and repeat-work churn (22% follow-on contracts to new firms, 2024).

| Metric | Value |

|---|---|

| RFP awards | 62% |

| Bid discounts | 5–12% |

| GC EBITDA | 3–6% |

| Tech spend YoY | +18% |

| BIM cost | $150–250k |

| Public RFPs w/ESG | 68% |

| NY minority rule | 15% |

| Follow-on churn | 22% |

Preview Before You Purchase

Whiting-Turner Contracting Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Whiting-Turner Contracting you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the same professionally formatted file you'll be able to download and use the moment you complete your purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Whiting‑Turner faces moderate supplier leverage, intense bidder competition on large projects, and regulatory hurdles that raise entry costs—yet its scale and reputation create durable customer loyalty and bidding advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Whiting‑Turner’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Skilled Labor Scarcity

The U.S. construction sector faces a chronic shortage of skilled trades; as of Q4 2025, BLS data show 14% fewer licensed electricians and 12% fewer HVAC/mechanical techs versus demand in data center and healthcare projects, letting subcontractors raise rates 10–25% year-over-year and boosting their bargaining power against Whiting-Turner.

Whiting-Turner must secure priority access by maintaining long-term subcontractor agreements, offering 5–10% premium pay or faster payments, and investing in joint training programs to mitigate delays and keep margins intact.

Raw Material Price Volatility

Suppliers of structural steel, concrete, and specialty glass hold substantial leverage amid global supply-chain shocks; steel futures rose 28% in 2021–2023 and were still 9% above 2019 levels in 2024, raising input risk for Whiting-Turner.

Whiting-Turner’s $7.6B 2024 revenue and scale enable better contract terms and bulk buys, but commodity sensitivity to geopolitics and carbon rules keeps price exposure material.

Therefore the firm uses early procurement and fixed-price buyouts—locking up to 12–18 months ahead on major projects—to protect margins and reduce variation.

Specialized Equipment Providers

Energy and Logistics Costs

Suppliers of transportation and logistics gained leverage as U.S. diesel prices rose 23% in 2024 and new state-level carbon fees added $3–12 per tonne CO2, raising heavy-material haul costs contractors pay.

Delivery of modular units and bulk aggregates now drives site overheads; carriers commonly pass 5–12% fuel-surcharge hikes to general contractors on long-haul jobs.

Whiting-Turner must model region-specific fuel, toll, and carbon fees when budgeting national projects to avoid 2–6% margin erosion on large builds.

- 2024 U.S. average diesel +23%

- Carbon fees $3–12/tonne CO2

- Carrier fuel surcharges 5–12%

- Budget risk: 2–6% margin erosion

Strategic Subcontractor Partnerships

In niche sectors like biotech and microelectronics, fewer than 50 qualified subcontractors nationally give those firms high bargaining power; Whiting-Turner signs exclusive or multi-year deals—often 3–7 years—to prevent poaching and secure capacity.

This creates mutual dependency: subcontractor technical skill drives project feasibility while Whiting-Turner provides 30–40% of project management value, aligning incentives and lowering schedule risk.

- Fewer than 50 specialists nationwide

- Typical exclusive deals: 3–7 years

- Subcontractor expertise equals contractor management value

- Deal reduces schedule and poaching risk

Suppliers Gain Leverage; Whiting-Turner Buys Lead Time, Pays Premiums

Suppliers (skilled trades, steel, heavy equipment, logistics) hold medium–high bargaining power vs Whiting-Turner due to labor shortages, stretched lead times (26–34 weeks), and commodity/transport cost rises (steel +9% vs 2019; diesel +23% in 2024). Whiting-Turner counters with long-term subcontractor deals, 5–10% pay premiums, early procurement (12–18 months), and occasional upfront capex financing (10–15% job value).

| Metric | Value |

|---|---|

| Lead times (median) | 26–34 wks |

| Diesel change (2024) | +23% |

| Steel vs 2019 (2024) | +9% |

| Subcontractor pay premium | 5–10% |

| Procurement horizon | 12–18 mos |

What is included in the product

Provides a concise Porter’s Five Forces assessment for Whiting‑Turner Contracting, highlighting competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategy and valuation.

A concise Porter's Five Forces one-sheet for Whiting-Turner—quickly spot supplier, buyer, entrant, substitute, and rivalry pressures to streamline strategic decisions.

Customers Bargaining Power

Institutional Client Sophistication

Whiting-Turner serves high-end healthcare, education, and technology clients whose procurement teams cut average management fees by 5–12% during contract rounds; these institutional buyers demand strict KPIs and risk transfer clauses. Clients with deep market knowledge scrutinize line-item costs—procurement-led projects now award 62% of contracts via competitive RFPs (2024 AIA data). Transparent benchmarking tools let clients compare hourly rates and margin structures across top-tier firms, squeezing pricing power.

Competitive Bidding Environments

The widespread Request for Proposal (RFP) process lets clients pit major contractors like Whiting-Turner against each other, driving bid-driven contracts where average bid discounts of 5–12% off list prices are common in US commercial projects (2024 AIA data).

Private clients routinely invite multiple national firms to bid—studies show 60–70% of mid-size commercial projects see 3+ national bidders—keeping general contractor margins around 3–6% EBITDA.

That buyer leverage also forces contractors to include add-ons—sustainability upgrades or enhanced scheduling—often at minimal extra cost, with green spec premiums commonly limited to 1–3% of contract value.

Low Switching Costs for Future Phases

While mid-project contractor swaps are hard, clients can switch firms for future phases with low friction, so Whiting-Turner must deliver near-perfect results to win repeat work.

In 2024 US construction owners awarded 22% of follow-on contracts to new contractors, so one safety or schedule lapse can cost multi-million repeat revenue.

Competitors like Turner Construction and Gilbane drive this pressure—Whiting-Turner faces dozens of high-quality bidders on large projects, raising churn risk from single failures.

Demand for Integrated Technology

Clients demand BIM and real-time tracking as standard by end-2025, pushing Whiting-Turner to adopt platforms clients specify and meet reporting cadences as frequent as daily.

Customers dictate software choice and reporting, forcing heavy upfront digital investments—industry data shows construction tech spend rose 18% in 2024, and BIM implementation costs average $150–250k per large project.

This shifts adaptation costs to the contractor while clients capture long-term operational ROI, often 8–15% lifecycle savings from BIM and real-time data.

- Clients set platform + frequency

- 2024 tech spend +18%

- BIM cost $150–250k/project

- Client ROI 8–15% lifecycle

Emphasis on ESG and Diversity Goals

Major corporate and government clients now mandate strict ESG metrics and minority-owned business participation; in 2024, 68% of US public-sector RFPs included formal diversity or carbon targets, raising disqualification risk for noncompliant contractors.

Customers can reject bidders failing diversity spend or carbon reduction goals; a 2025 NY state procurement rule requires 15% minority-owned subcontractor spend on many projects, directly affecting eligibility.

Whiting-Turner must align its supply chain to these mandates to keep access to large public/private contracts worth billions annually; missed targets could cost market share and contract awards.

- 68% of 2024 public RFPs had ESG/diversity clauses

- NY 2025: 15% minority-owned subcontractor requirement

- Supply-chain alignment needed to retain billion-dollar contracts

RFP-driven squeeze: buyers wield discounts, rising tech/ESG costs, NY diversity rule ups churn

Buyers hold strong leverage: 62% of contracts via RFPs (AIA 2024), typical bid discounts 5–12%, and GC EBITDA 3–6%; tech spend up 18% (2024) with BIM costs $150–250k/project and client lifecycle ROI 8–15%; 68% public RFPs had ESG/diversity clauses (2024) and NY 2025 rule: 15% minority subcontractor spend, raising disqualification risk and repeat-work churn (22% follow-on contracts to new firms, 2024).

| Metric | Value |

|---|---|

| RFP awards | 62% |

| Bid discounts | 5–12% |

| GC EBITDA | 3–6% |

| Tech spend YoY | +18% |

| BIM cost | $150–250k |

| Public RFPs w/ESG | 68% |

| NY minority rule | 15% |

| Follow-on churn | 22% |

Preview Before You Purchase

Whiting-Turner Contracting Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Whiting-Turner Contracting you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the same professionally formatted file you'll be able to download and use the moment you complete your purchase.