Whiting-Turner Contracting PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

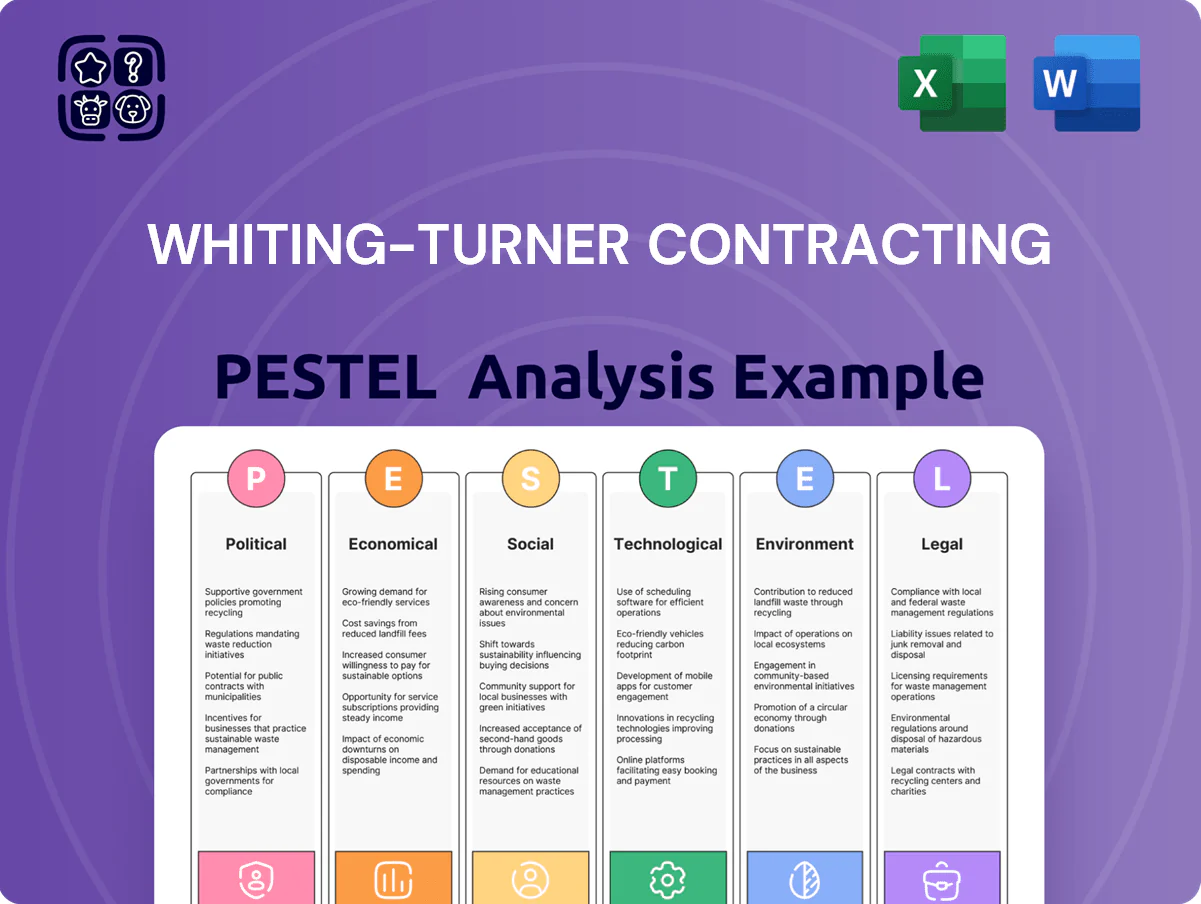

Gain a strategic edge with our PESTLE Analysis of Whiting-Turner Contracting—uncover how political, economic, social, technological, legal, and environmental forces are reshaping its opportunities and risks; purchase the full report for an instantly downloadable, editable breakdown that powers smarter investment and strategic decisions.

Political factors

Infrastructure Investment and Jobs Act implementation

The continued rollout of Infrastructure Investment and Jobs Act funding remains a primary driver for Whiting-Turner projects into late 2025, with the law allocating roughly $110 billion to surface transportation and $65 billion to water infrastructure that fuels public-sector contract pipelines; these government-backed projects helped consolidate ~18% of the firm’s 2024 revenue mix and buffer against private market volatility. The company must manage complex federal reporting, Davis-Bacon wage rules, Buy America provisions and heightened compliance to remain a preferred partner on high-value projects often exceeding $100 million each.

Trade policy and material tariffs

Federal healthcare and education funding

Federal healthcare and higher education allocations in the 2025 fiscal budget—including a proposed $12.5 billion for hospital modernization and $8.2 billion for campus infrastructure—directly shape Whiting-Turner’s project pipeline.

The firm’s heavy exposure to institutional construction makes it sensitive to shifts in federal subsidies, grants, and Department of Education/Health and Human Services capital programs.

Changes in political leadership or fiscal policy could accelerate or defer major campus and hospital renovations, impacting backlog and revenue visibility given institutional project lead times of 12–36 months.

Local government zoning and land-use policies

- 60%+ metros tightened rules (2024–25)

- Average review time +22%

- Entitlement cost impact 8–12%

- Typical delay 3–6 months

Geopolitical stability and supply chain security

Geopolitical tensions in late 2025 elevated freight insurance premiums by ~18% and caused an estimated 12% lead-time increase for specialized data-center components, pressuring Whiting-Turner project margins on tech-heavy builds.

Instability in key manufacturing hubs—notably Southeast Asia—has produced equipment delivery delays averaging 6–10 weeks for electrical/mechanical systems, requiring revised client schedules and contingency sourcing.

Whiting-Turner must continuously monitor risks and offer alternative suppliers, with contingency inventory or airfreight options that can raise project costs by 3–5% but reduce schedule slippage.

- Freight insurance +18% (late 2025)

- Component lead times +12%

- Average equipment delays 6–10 weeks

- Contingency measures add 3–5% to costs

Infrastructure boom fuels 18% public revenue but tariffs, supply and permitting squeeze margins

Federal Infrastructure Investment funding (~$175B to transport/water through IIJA) and 2025 healthcare/education allocations ($12.5B hospitals, $8.2B campuses) drive ~18% of 2024 revenue and backlog; Davis‑Bacon, Buy America and tariffs (steel futures +18% YoY, tariffs ~25%) compress margins and require robust compliance and diversified sourcing; local land‑use tightening (60%+ metros, review times +22%) and geopolitical supply shocks (component lead times +12%, freight insurance +18%) raise costs and schedule risk.

| Metric | Value |

|---|---|

| Public-project revenue share (2024) | ~18% |

| IIJA transport+water | $175B |

| Hospital/campus 2025 alloc. | $12.5B / $8.2B |

| Steel futures YoY (2024-25) | +18% |

| Metro land‑use tightening | 60%+ |

| Review time impact | +22% |

| Component lead times | +12% |

| Freight insurance | +18% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact Whiting-Turner Contracting, with data-driven subpoints and trend-backed examples tailored to the construction and engineering sector.

A concise, PESTLE-segmented brief that distills Whiting-Turner’s external risks and opportunities into an easily shareable slide or meeting handout, enabling quick alignment across teams and focused discussion during strategic planning.

Economic factors

Interest rate environment and capital availability

As of late 2025, the US federal funds rate near 5.25–5.50% has raised corporate borrowing costs, weakening private-sector starts; commercial office vacancy rose to about 18% in major metros while retail investment volumes fell ~12% year-over-year in 2024–25, nudging Whiting-Turner toward industrial, health care and life sciences work.

The firm watches Fed communications and regional reserve bank forecasts to model project pipelines—BLS capex intentions showed nonresidential construction spending growth slowing to roughly 1–2% annualized in 2025—informing bidding and working-capital strategies.

Construction material price volatility

Economic fluctuations in global commodities markets keep project estimating and fixed-price contracting uncertain; lumber and steel saw 2024-2025 price swings of 12-18% and 8-14% respectively, impacting bid accuracy.

Although headline inflation eased to ~3.4% in 2025, specialized materials like HVAC chiller components and semiconductor-based building controls remain volatile, with spot premiums up to 20%.

Whiting-Turner mitigates risk using macroeconomic forecasting, hedging and early-purchase agreements covering roughly 30-40% of critical-material spend, preserving margins and offering clients greater cost certainty.

Skilled labor shortages and wage inflation

As of late 2025 the US construction sector reports a 12% shortfall in skilled trades versus demand, pushing craft wages up ~6–9% yr/yr and extending project timelines; Whiting-Turner faces higher bid costs and schedule risk from this tight labor market.

Competing for talent raises Whiting-Turner’s overhead via recruiting, retention premiums, and overtime, contributing to margin pressure—industry data show labor is ~30–40% of total project cost.

Wage inflation drives investment in productivity: Whiting-Turner is incentivized to scale labor-saving tech (modular construction, robotics, BIM) and crew optimization to offset a 5–8% net impact on project unit labor costs.

Commercial real estate market demand

The commercial real estate sector's health, especially office demand, remained soft through 2024–2025 with U.S. office vacancy near 17% in Q4 2024 and leasing activity down ~15% year-over-year, pressuring traditional construction volumes.

Whiting-Turner has shifted toward life sciences and data centers—sectors with projected CAGR >8% through 2026—supporting revenue diversification after office declines.

The firm's agility to reallocate resources from lower-growth office projects to higher-return segments is vital to sustain margins and top-line growth amid ongoing workplace shifts.

- U.S. office vacancy ~17% (Q4 2024)

- Leasing activity down ~15% YoY (2024)

- Life sciences/data centers projected CAGR >8% to 2026

- Pivoting key to preserving margins and revenue

National GDP growth and infrastructure spending

National GDP growth and infrastructure spending drive construction demand; US GDP grew about 2.5% in 2024 and consensus for 2025 late-year estimates centered near 1.8–2.2%, supporting corporate capex and large industrial projects.

Federal infrastructure outlays from the IIJA and CHIPS/EDA-related programs lifted public construction budgets by an estimated $120–150bn annually through 2024–25, prompting Whiting-Turner to reallocate crews and bid selectively.

Whiting-Turner monitors regional GDP, manufacturing output, and state-level infrastructure awards to prioritize resources where economic momentum and funded projects converge.

- 2024 US GDP ~2.5%; 2025 consensus 1.8–2.2%

- Estimated $120–150bn/year boosted public construction from IIJA/CHIPS

- Resource allocation tied to regional GDP and awarded infrastructure contracts

Rates Bite, CRE Weakness Shifts Whiting‑Turner to Life‑Sciences/Data Centers

Rising rates (Fed funds ~5.25–5.50% late‑2025) and softer CRE (office vacancy ~17% Q4‑24) shift Whiting‑Turner toward life sciences/data centers (CAGR >8% to 2026); materials swung 8–18% (2024–25) and skilled‑labor shortfall ~12% raised wages 6–9%, pressuring margins; IIJA/CHIPS added ~$120–150bn/yr to public construction, supporting selective bidding.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Office vacancy | ~17% |

| Materials volatility | 8–18% |

| Wage rise | 6–9% |

| Public spend boost | $120–150bn/yr |

Preview the Actual Deliverable

Whiting-Turner Contracting PESTLE Analysis

The preview shown here is the exact Whiting‑Turner Contracting PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and insights visible in this sample are identical to the downloadable file delivered immediately after checkout, with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our PESTLE Analysis of Whiting-Turner Contracting—uncover how political, economic, social, technological, legal, and environmental forces are reshaping its opportunities and risks; purchase the full report for an instantly downloadable, editable breakdown that powers smarter investment and strategic decisions.

Political factors

Infrastructure Investment and Jobs Act implementation

The continued rollout of Infrastructure Investment and Jobs Act funding remains a primary driver for Whiting-Turner projects into late 2025, with the law allocating roughly $110 billion to surface transportation and $65 billion to water infrastructure that fuels public-sector contract pipelines; these government-backed projects helped consolidate ~18% of the firm’s 2024 revenue mix and buffer against private market volatility. The company must manage complex federal reporting, Davis-Bacon wage rules, Buy America provisions and heightened compliance to remain a preferred partner on high-value projects often exceeding $100 million each.

Trade policy and material tariffs

Federal healthcare and education funding

Federal healthcare and higher education allocations in the 2025 fiscal budget—including a proposed $12.5 billion for hospital modernization and $8.2 billion for campus infrastructure—directly shape Whiting-Turner’s project pipeline.

The firm’s heavy exposure to institutional construction makes it sensitive to shifts in federal subsidies, grants, and Department of Education/Health and Human Services capital programs.

Changes in political leadership or fiscal policy could accelerate or defer major campus and hospital renovations, impacting backlog and revenue visibility given institutional project lead times of 12–36 months.

Local government zoning and land-use policies

- 60%+ metros tightened rules (2024–25)

- Average review time +22%

- Entitlement cost impact 8–12%

- Typical delay 3–6 months

Geopolitical stability and supply chain security

Geopolitical tensions in late 2025 elevated freight insurance premiums by ~18% and caused an estimated 12% lead-time increase for specialized data-center components, pressuring Whiting-Turner project margins on tech-heavy builds.

Instability in key manufacturing hubs—notably Southeast Asia—has produced equipment delivery delays averaging 6–10 weeks for electrical/mechanical systems, requiring revised client schedules and contingency sourcing.

Whiting-Turner must continuously monitor risks and offer alternative suppliers, with contingency inventory or airfreight options that can raise project costs by 3–5% but reduce schedule slippage.

- Freight insurance +18% (late 2025)

- Component lead times +12%

- Average equipment delays 6–10 weeks

- Contingency measures add 3–5% to costs

Infrastructure boom fuels 18% public revenue but tariffs, supply and permitting squeeze margins

Federal Infrastructure Investment funding (~$175B to transport/water through IIJA) and 2025 healthcare/education allocations ($12.5B hospitals, $8.2B campuses) drive ~18% of 2024 revenue and backlog; Davis‑Bacon, Buy America and tariffs (steel futures +18% YoY, tariffs ~25%) compress margins and require robust compliance and diversified sourcing; local land‑use tightening (60%+ metros, review times +22%) and geopolitical supply shocks (component lead times +12%, freight insurance +18%) raise costs and schedule risk.

| Metric | Value |

|---|---|

| Public-project revenue share (2024) | ~18% |

| IIJA transport+water | $175B |

| Hospital/campus 2025 alloc. | $12.5B / $8.2B |

| Steel futures YoY (2024-25) | +18% |

| Metro land‑use tightening | 60%+ |

| Review time impact | +22% |

| Component lead times | +12% |

| Freight insurance | +18% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact Whiting-Turner Contracting, with data-driven subpoints and trend-backed examples tailored to the construction and engineering sector.

A concise, PESTLE-segmented brief that distills Whiting-Turner’s external risks and opportunities into an easily shareable slide or meeting handout, enabling quick alignment across teams and focused discussion during strategic planning.

Economic factors

Interest rate environment and capital availability

As of late 2025, the US federal funds rate near 5.25–5.50% has raised corporate borrowing costs, weakening private-sector starts; commercial office vacancy rose to about 18% in major metros while retail investment volumes fell ~12% year-over-year in 2024–25, nudging Whiting-Turner toward industrial, health care and life sciences work.

The firm watches Fed communications and regional reserve bank forecasts to model project pipelines—BLS capex intentions showed nonresidential construction spending growth slowing to roughly 1–2% annualized in 2025—informing bidding and working-capital strategies.

Construction material price volatility

Economic fluctuations in global commodities markets keep project estimating and fixed-price contracting uncertain; lumber and steel saw 2024-2025 price swings of 12-18% and 8-14% respectively, impacting bid accuracy.

Although headline inflation eased to ~3.4% in 2025, specialized materials like HVAC chiller components and semiconductor-based building controls remain volatile, with spot premiums up to 20%.

Whiting-Turner mitigates risk using macroeconomic forecasting, hedging and early-purchase agreements covering roughly 30-40% of critical-material spend, preserving margins and offering clients greater cost certainty.

Skilled labor shortages and wage inflation

As of late 2025 the US construction sector reports a 12% shortfall in skilled trades versus demand, pushing craft wages up ~6–9% yr/yr and extending project timelines; Whiting-Turner faces higher bid costs and schedule risk from this tight labor market.

Competing for talent raises Whiting-Turner’s overhead via recruiting, retention premiums, and overtime, contributing to margin pressure—industry data show labor is ~30–40% of total project cost.

Wage inflation drives investment in productivity: Whiting-Turner is incentivized to scale labor-saving tech (modular construction, robotics, BIM) and crew optimization to offset a 5–8% net impact on project unit labor costs.

Commercial real estate market demand

The commercial real estate sector's health, especially office demand, remained soft through 2024–2025 with U.S. office vacancy near 17% in Q4 2024 and leasing activity down ~15% year-over-year, pressuring traditional construction volumes.

Whiting-Turner has shifted toward life sciences and data centers—sectors with projected CAGR >8% through 2026—supporting revenue diversification after office declines.

The firm's agility to reallocate resources from lower-growth office projects to higher-return segments is vital to sustain margins and top-line growth amid ongoing workplace shifts.

- U.S. office vacancy ~17% (Q4 2024)

- Leasing activity down ~15% YoY (2024)

- Life sciences/data centers projected CAGR >8% to 2026

- Pivoting key to preserving margins and revenue

National GDP growth and infrastructure spending

National GDP growth and infrastructure spending drive construction demand; US GDP grew about 2.5% in 2024 and consensus for 2025 late-year estimates centered near 1.8–2.2%, supporting corporate capex and large industrial projects.

Federal infrastructure outlays from the IIJA and CHIPS/EDA-related programs lifted public construction budgets by an estimated $120–150bn annually through 2024–25, prompting Whiting-Turner to reallocate crews and bid selectively.

Whiting-Turner monitors regional GDP, manufacturing output, and state-level infrastructure awards to prioritize resources where economic momentum and funded projects converge.

- 2024 US GDP ~2.5%; 2025 consensus 1.8–2.2%

- Estimated $120–150bn/year boosted public construction from IIJA/CHIPS

- Resource allocation tied to regional GDP and awarded infrastructure contracts

Rates Bite, CRE Weakness Shifts Whiting‑Turner to Life‑Sciences/Data Centers

Rising rates (Fed funds ~5.25–5.50% late‑2025) and softer CRE (office vacancy ~17% Q4‑24) shift Whiting‑Turner toward life sciences/data centers (CAGR >8% to 2026); materials swung 8–18% (2024–25) and skilled‑labor shortfall ~12% raised wages 6–9%, pressuring margins; IIJA/CHIPS added ~$120–150bn/yr to public construction, supporting selective bidding.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Office vacancy | ~17% |

| Materials volatility | 8–18% |

| Wage rise | 6–9% |

| Public spend boost | $120–150bn/yr |

Preview the Actual Deliverable

Whiting-Turner Contracting PESTLE Analysis

The preview shown here is the exact Whiting‑Turner Contracting PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and insights visible in this sample are identical to the downloadable file delivered immediately after checkout, with no placeholders or surprises.