Wheeler Real Estate Investment Trust Porter's Five Forces Analysis

From Overview to Strategy Blueprint

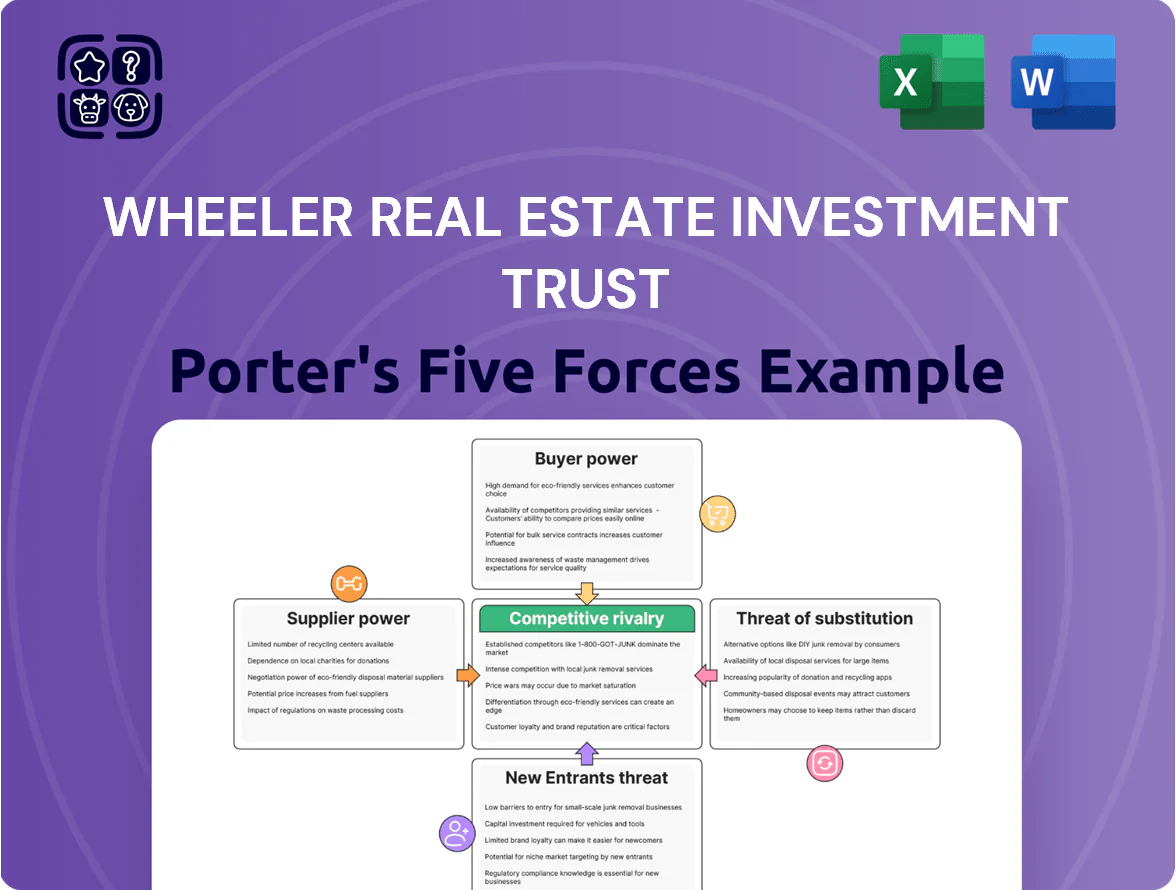

Suppliers Bargaining Power

Access to Capital Markets and Lenders

Primary suppliers for Wheeler REIT are debt and equity providers; by end-2025 banks and bondholders hold strong leverage after 2022–24 rate hikes pushed average commercial mortgage rates to ~6.5%–7.5% and corporate bond yields to ~5%–6%.

Wheeler faces tight lending covenants and credit-rating scrutiny—S&P/Bloomberg sector peers saw net leverage covenants at 55% LTV and interest coverage ratios near 2.0x—so refinancing and acquisitions depend on meeting those metrics.

Construction and Maintenance Contractors

Suppliers of labor and materials for property upkeep and renovations hold moderate power over Wheeler REIT; national wage inflation for construction rose 4.2% in 2024 and specialty contractor rates in secondary US retail markets were up 6–9% year-on-year by Q4 2025.

Utility and Energy Providers

Energy firms supply non-negotiable electricity and water; in 2024 U.S. commercial electricity rates averaged 14.8 cents/kWh and water costs rose ~6% year-over-year, so supplier pricing materially affects operating expenses. Wheeler REIT faces a concentrated local supplier base for these utilities, raising supplier power, but roughly 70–85% of its leases are triple-net (NNN), allowing recovery of utility pass-throughs and thus partially offsetting supplier leverage.

Professional Service and Tech Vendors

Suppliers of property-management software, legal counsel, and auditors are vital to Wheeler REIT’s self-managed model; in 2024 Wheeler spent an estimated $4.2M on IT and professional services (approx 1.1% of assets under management), so disruptions hit operations fast.

Many vendors exist, but switching integrated platforms can cost 6–12 months of lost efficiency and $500k–$2M in migration and retraining; service-level agreements and compliance outputs (audit opinions, legal certs) give these suppliers negotiating leverage.

- 2024 spend ~ $4.2M (1.1% AUM)

- Switch costs 6–12 months; $500k–$2M

- High SLA specificity; compliance outputs essential

Municipalities and Local Governments

Municipalities and local governments supply the regulatory framework and infrastructure for Wheeler REITs grocery-anchored centers, wielding high bargaining power via control of property tax rates, zoning, permits, and business licenses.

In 2024 US median property tax rate was 1.07% and local permitting delays averaged 120 days in large metros, so Wheeler must cultivate positive relations and proactive compliance to protect occupancy and tenant access.

- Control: taxes, zoning, permits, licenses

- Impact: median 1.07% tax rate (US, 2024)

- Risk: 120-day average permit delays (large metros, 2024)

- Action: proactive engagement, compliance, local partnerships

Suppliers Hold Moderate–High Leverage Over Wheeler REIT Amid Rising Rates & Costs

Suppliers (debt/equity, labor, utilities, professional services, municipalities) exert moderate-to-high power on Wheeler REIT—2025 commercial mortgage rates ~6.5%–7.5%, corporate yields 5%–6%, 2024 construction wage +4.2%, commercial electricity 14.8¢/kWh, 2024 spend on IT/legal ~$4.2M (1.1% AUM); NNN leases and pass-throughs partly mitigate cost risk.

| Supplier | Key 2024–25 Metric |

|---|---|

| Debt/equity | Rates 6.5%–7.5%; yields 5%–6% |

| Labor | Wage +4.2% (2024) |

| Utilities | Electricity 14.8¢/kWh (2024) |

| Services | Spend $4.2M (1.1% AUM) |

What is included in the product

Tailored Porter's Five Forces analysis for Wheeler Real Estate Investment Trust, uncovering competitive intensity, buyer/supplier power, substitution risks, and barriers to entry with strategic commentary and industry-backed insights.

A concise, one-sheet Porter's Five Forces summary for Wheeler REIT—instantly highlights competitive pressures and acquisition risks for boardroom decisions.

Customers Bargaining Power

Grocery Anchor Tenant Influence

Small Shop Tenant Sensitivity

Non-anchor tenants—local boutiques and service providers—have limited individual bargaining power but are highly sensitive to economic shifts; by end-2025 about 42% of US small retailers reported asking landlords for flexible terms or rent relief, per a 2025 NFIB survey. Wheeler REIT faces higher risk: a 5-point rise in small-shop vacancy (to 12% in 2025) would cut NAV by roughly 3–4%, since collective churn drives occupancy and valuation.

Lease Renewal and Retention Rates

Tenants can shift to competing retail spaces, giving moderate leverage at renewals; industry average retail turnover rose to 12.4% in 2024, so Wheeler faces real churn risk.

Wheeler must match amenities and upkeep—properties with capital expenditure underinvestment see 8–12% higher vacancy—so proactive maintenance lowers relocation pressure.

High retention stabilizes cash flow; US REITs reported median rent renewal rates of 78% in 2024, forcing Wheeler to offer tenant improvement allowances often equal to 5–8% of annual rent to retain key tenants.

E-commerce Integration Demands

Geographic Concentration of Tenants

- Few large retailers hold multiple leases

- Single exit → clustered vacancies risk

- Top-5 tenants ≈18% regional rent (Q4 2025)

- Diversification + credit monitoring mitigates risk

Anchor tenants (Kroger/Publix) command traffic, rents & financing—TI + omni = retention

| Metric | Value |

|---|---|

| Anchor foot traffic | 40–60% |

| Anchor rent concessions | 10–25% |

| Financing spread benefit | 50–150 bps |

| Small retailers asking relief (2025) | 42% |

| Renewal rate (2024) | 78% |

| BOPIS users (2024) | 72% |

Same Document Delivered

Wheeler Real Estate Investment Trust Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Wheeler Real Estate Investment Trust you’ll receive immediately after purchase—no surprises, no placeholders, fully formatted for download and use.

The document displayed here is the part of the full version you’ll get—ready for immediate access upon payment and containing in-depth assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Suppliers Bargaining Power

Access to Capital Markets and Lenders

Primary suppliers for Wheeler REIT are debt and equity providers; by end-2025 banks and bondholders hold strong leverage after 2022–24 rate hikes pushed average commercial mortgage rates to ~6.5%–7.5% and corporate bond yields to ~5%–6%.

Wheeler faces tight lending covenants and credit-rating scrutiny—S&P/Bloomberg sector peers saw net leverage covenants at 55% LTV and interest coverage ratios near 2.0x—so refinancing and acquisitions depend on meeting those metrics.

Construction and Maintenance Contractors

Suppliers of labor and materials for property upkeep and renovations hold moderate power over Wheeler REIT; national wage inflation for construction rose 4.2% in 2024 and specialty contractor rates in secondary US retail markets were up 6–9% year-on-year by Q4 2025.

Utility and Energy Providers

Energy firms supply non-negotiable electricity and water; in 2024 U.S. commercial electricity rates averaged 14.8 cents/kWh and water costs rose ~6% year-over-year, so supplier pricing materially affects operating expenses. Wheeler REIT faces a concentrated local supplier base for these utilities, raising supplier power, but roughly 70–85% of its leases are triple-net (NNN), allowing recovery of utility pass-throughs and thus partially offsetting supplier leverage.

Professional Service and Tech Vendors

Suppliers of property-management software, legal counsel, and auditors are vital to Wheeler REIT’s self-managed model; in 2024 Wheeler spent an estimated $4.2M on IT and professional services (approx 1.1% of assets under management), so disruptions hit operations fast.

Many vendors exist, but switching integrated platforms can cost 6–12 months of lost efficiency and $500k–$2M in migration and retraining; service-level agreements and compliance outputs (audit opinions, legal certs) give these suppliers negotiating leverage.

- 2024 spend ~ $4.2M (1.1% AUM)

- Switch costs 6–12 months; $500k–$2M

- High SLA specificity; compliance outputs essential

Municipalities and Local Governments

Municipalities and local governments supply the regulatory framework and infrastructure for Wheeler REITs grocery-anchored centers, wielding high bargaining power via control of property tax rates, zoning, permits, and business licenses.

In 2024 US median property tax rate was 1.07% and local permitting delays averaged 120 days in large metros, so Wheeler must cultivate positive relations and proactive compliance to protect occupancy and tenant access.

- Control: taxes, zoning, permits, licenses

- Impact: median 1.07% tax rate (US, 2024)

- Risk: 120-day average permit delays (large metros, 2024)

- Action: proactive engagement, compliance, local partnerships

Suppliers Hold Moderate–High Leverage Over Wheeler REIT Amid Rising Rates & Costs

Suppliers (debt/equity, labor, utilities, professional services, municipalities) exert moderate-to-high power on Wheeler REIT—2025 commercial mortgage rates ~6.5%–7.5%, corporate yields 5%–6%, 2024 construction wage +4.2%, commercial electricity 14.8¢/kWh, 2024 spend on IT/legal ~$4.2M (1.1% AUM); NNN leases and pass-throughs partly mitigate cost risk.

| Supplier | Key 2024–25 Metric |

|---|---|

| Debt/equity | Rates 6.5%–7.5%; yields 5%–6% |

| Labor | Wage +4.2% (2024) |

| Utilities | Electricity 14.8¢/kWh (2024) |

| Services | Spend $4.2M (1.1% AUM) |

What is included in the product

Tailored Porter's Five Forces analysis for Wheeler Real Estate Investment Trust, uncovering competitive intensity, buyer/supplier power, substitution risks, and barriers to entry with strategic commentary and industry-backed insights.

A concise, one-sheet Porter's Five Forces summary for Wheeler REIT—instantly highlights competitive pressures and acquisition risks for boardroom decisions.

Customers Bargaining Power

Grocery Anchor Tenant Influence

Small Shop Tenant Sensitivity

Non-anchor tenants—local boutiques and service providers—have limited individual bargaining power but are highly sensitive to economic shifts; by end-2025 about 42% of US small retailers reported asking landlords for flexible terms or rent relief, per a 2025 NFIB survey. Wheeler REIT faces higher risk: a 5-point rise in small-shop vacancy (to 12% in 2025) would cut NAV by roughly 3–4%, since collective churn drives occupancy and valuation.

Lease Renewal and Retention Rates

Tenants can shift to competing retail spaces, giving moderate leverage at renewals; industry average retail turnover rose to 12.4% in 2024, so Wheeler faces real churn risk.

Wheeler must match amenities and upkeep—properties with capital expenditure underinvestment see 8–12% higher vacancy—so proactive maintenance lowers relocation pressure.

High retention stabilizes cash flow; US REITs reported median rent renewal rates of 78% in 2024, forcing Wheeler to offer tenant improvement allowances often equal to 5–8% of annual rent to retain key tenants.

E-commerce Integration Demands

Geographic Concentration of Tenants

- Few large retailers hold multiple leases

- Single exit → clustered vacancies risk

- Top-5 tenants ≈18% regional rent (Q4 2025)

- Diversification + credit monitoring mitigates risk

Anchor tenants (Kroger/Publix) command traffic, rents & financing—TI + omni = retention

| Metric | Value |

|---|---|

| Anchor foot traffic | 40–60% |

| Anchor rent concessions | 10–25% |

| Financing spread benefit | 50–150 bps |

| Small retailers asking relief (2025) | 42% |

| Renewal rate (2024) | 78% |

| BOPIS users (2024) | 72% |

Same Document Delivered

Wheeler Real Estate Investment Trust Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Wheeler Real Estate Investment Trust you’ll receive immediately after purchase—no surprises, no placeholders, fully formatted for download and use.

The document displayed here is the part of the full version you’ll get—ready for immediate access upon payment and containing in-depth assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution.