Wheeler Real Estate Investment Trust PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

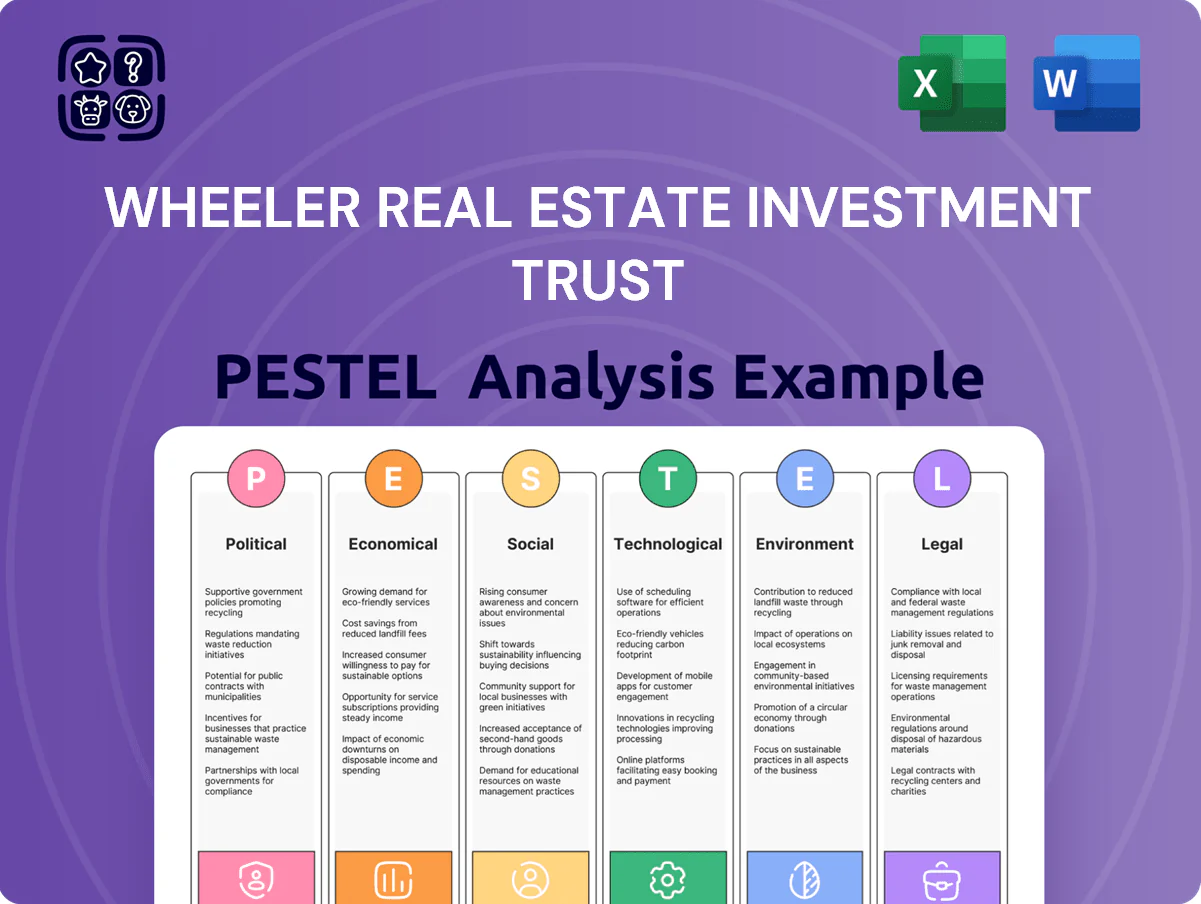

Gain strategic clarity with our PESTLE Analysis of Wheeler Real Estate Investment Trust—uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental forces will shape its prospects; purchase the full report for a complete, actionable breakdown you can deploy in investment decisions or strategy planning.

Political factors

Local zoning and land use regulations

Wheeler REIT, with ~220 grocery-anchored centers across secondary/tertiary U.S. markets, faces direct impact from local zoning: recent municipal land-use updates in 2024 increased allowable outparcel density in 12% of its markets, while stricter mixed-use caps in 8% limited redevelopment potential, affecting projected NOI growth of ~1.3% annually if expansions are blocked; mastering these political environments is critical to preserve asset value and expansion economics.

Federal tax policy and REIT status

As a REIT Wheeler must distribute at least 90% of taxable income to shareholders, a rule that preserved its 2024 effective tax profile and supported a 2024 total shareholder yield near 6.2%; any federal changes to corporate tax rates or to TCJA provisions through 2025–2026 could shift the economic benefit of the REIT wrapper. Legislative stability of the dividends-paid deduction is critical for Wheeler’s capital recycling—its 2024 asset turnover and $0.18/share quarterly payouts depend on predictable tax treatment. Policy risk could increase WACC and reduce FFO multiples if deductions are curtailed.

Infrastructure investment in secondary markets

Government support for essential retail

Political recognition of grocery stores and pharmacies as essential infrastructure stabilizes Wheeler REIT’s tenant base; during COVID-19 these tenants saw sales increases—grocery sales rose ~18% in 2020 and pharmacies maintained steady traffic—protecting rent collection and occupancy.

Policies bolstering food-supply resilience and subsidies for healthy-food access in low-income areas (e.g., federal nutrition assistance programs reaching >40 million households in 2024) align with Wheeler’s community-focused retail locations.

This alignment keeps Wheeler’s centers prioritized by planners and emergency responses, supporting long-term asset value and leasing demand in strategic corridors.

- Essential designation = higher occupancy/resilience

- Grocery sales +18% in 2020; nutrition programs >40M households (2024)

- Policy support increases asset priority for planners

Trade policies and tenant supply chains

International trade agreements and US tariff policies affect input costs for Wheeler’s retail tenants—discount and hardware chains saw import cost pressure after 2018–2020 tariffs, with US goods imports tariffs averaging 1.7% but specific steel/metal tariffs raising sector costs by up to 10–15% in 2018–2020.

Political volatility raising import costs can compress tenant EBITDA margins (retail averages 3–6%), increasing risk of missed rent or delayed expansion for small chains.

Wheeler must monitor federal trade stances and CBP data, using tenant-level sales and debt-service metrics to reassess credit exposure and occupancy risk.

- Tariff shocks can raise sector input costs up to 15%

- Retail EBITDA margins often 3–6%, vulnerable to cost increases

- Monitoring federal trade policy and tenant financials reduces lease default risk

Policy Shifts Drive Retail Returns: Zoning, REIT Rules, Infra Flows & Tariff Risks

Political factors: zoning changes (12% markets eased, 8% tightened in 2024) affect redevelopment and ~1.3% projected NOI growth; REIT tax rules (90% distribution) kept 2024 yield ~6.2% and $0.18/qtr; infrastructure funds (CHIPS+Infra $110B regional flows) can boost tenant sales 5–12%; tariffs historically raised input costs up to 15%, stressing retail EBITDA (3–6%).

| Factor | Key Data |

|---|---|

| Zoning | 12% eased / 8% tightened (2024) |

| REIT rules | 90% distribution; 2024 yield 6.2%; $0.18/qtr |

| Infrastructure | $110B regional flows; sales +5–12% |

| Tariffs | Input cost +≤15%; retail EBITDA 3–6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Wheeler Real Estate Investment Trust across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Wheeler REIT that streamlines external risk review, is easily dropped into presentations or planner packs, and allows quick note edits so teams can align on regulatory, economic, social, technological, environmental, and legal implications during strategy sessions.

Economic factors

Interest rate environment and debt servicing

The late-2025 interest rate environment—with the Fed funds target at 5.25–5.50% and 10‑year Treasury near 4.2% as of Dec 2025—raises Wheeler REIT’s cost of capital, increasing interest expense and refinancing costs on upcoming maturities. Higher rates can compress cap rates and reduce NAV, while heavier debt servicing squeezes cash flow; Wheeler’s liquidity and debt‑management (debt-to-equity and interest‑coverage ratios) will hinge on the Fed’s 2026 policy path.

Inflationary impact on operating costs

Persisting inflation raised US CPI to 3.4% in 2024, driving Wheeler REIT common area maintenance and insurance costs up ~6–8% year-over-year, squeezing margins on large retail assets.

Many leases permit pass-throughs, but CPI-linked cost jumps contributed to a national retail vacancy uptick to 7.1% in 2024, risking tenant defaults and lost rent for Wheeler.

Robust cost controls, capex prioritization, and lease clauses indexing recoveries to CPI and minimum rent floors are necessary to protect NOI.

Consumer spending power in secondary markets

Consumer spending power in Wheeler’s Southeast and Mid-Atlantic secondary markets drives foot traffic and sales for its grocery-anchored centers; metro unemployment averaged 3.8% in 2024 vs national 4.0%, while regional wage growth ran about 4.2% YoY, supporting steady retail demand.

A 2024 household median income of $62,400 in core markets underpins grocery sales, but a dip in consumer confidence—Conference Board index down 5.1% YoY—could shift purchases to discount grocers.

Such a shift would pressure rent rolls and compel Wheeler to reweight tenant mix toward value-oriented grocers and flexible lease terms to preserve occupancy and NOI.

Capital market volatility and liquidity

Wheeler’s ability to raise equity or issue new debt depends on capital market stability and investor appetite for retail REITs; US REIT equity issuance fell about 28% in 2024 vs 2023 amid higher rates and quarterly volatility (S&P Global, 2024).

Market volatility can restrict access to liquidity for acquisitions or capex, with commercial real estate lending down ~15% y/y in 2024, tightening credit availability for expansions.

Maintaining transparent financials—Wheeler’s trailing 12-month FFO margin and stable occupancy metrics—is critical to attract institutional and retail investors in a competitive capital environment.

- Equity/debt issuance sensitivity to market sentiment

- 2024 REIT equity issuance down ~28%

- CRE lending fell ~15% y/y in 2024

- Transparent FFO/occupancy crucial for investor access

Evolving retail landscape and tenant demand

The demand for physical retail space is driven by consolidation among national grocery chains—top 5 grocers gained ~4 percentage points market share to ~48% in 2024—while service-oriented tenants (healthcare, urgent care, dollar stores) grew leasing activity by ~12% year-over-year, favoring Wheeler’s grocery-anchored centers.

Economic shifts toward essentials during 2023–2025 have supported stable occupancy and same-store NOI resilience; grocery-anchored assets showed ~200–300 bps lower vacancy vs. non-anchored centers in 2024.

Wheeler must monitor market rents, tenant credit, and demographic trends; targeting recession-resistant tenants can sustain rental income and reduce rent volatility, with grocery-anchored centers historically delivering mid-single-digit rent growth.

- Grocery market share consolidation: top 5 ≈48% (2024)

- Service-tenant leasing growth: ≈12% YoY (2024)

- Lower vacancy for grocery-anchored: ≈200–300 bps advantage (2024)

- Target: recession-resistant tenants to sustain mid-single-digit rent growth

Higher rates squeeze Wheeler: rising costs, tighter cash flow, retail shift to value

Higher rates (Fed 5.25–5.50% late‑2025; 10y ≈4.2%) raise Wheeler’s refinancing and interest costs, compress NAV and stress cash flow; 2024–25 inflation/CPI (~3.4% in 2024) lifted OPEX ~6–8%, while retail vacancy rose to 7.1% (2024), forcing tenant mix shifts toward value and service tenants to protect NOI.

| Metric | Value (2024–25) |

|---|---|

| Fed funds | 5.25–5.50% |

| 10‑yr Treasury | ≈4.2% |

| CPI (US) | ≈3.4% |

| Retail vacancy (US) | 7.1% |

| REIT equity issuance | −28% YoY (2024) |

| CRE lending | −15% YoY (2024) |

Full Version Awaits

Wheeler Real Estate Investment Trust PESTLE Analysis

The preview shown here is the exact Wheeler Real Estate Investment Trust PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE Analysis of Wheeler Real Estate Investment Trust—uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental forces will shape its prospects; purchase the full report for a complete, actionable breakdown you can deploy in investment decisions or strategy planning.

Political factors

Local zoning and land use regulations

Wheeler REIT, with ~220 grocery-anchored centers across secondary/tertiary U.S. markets, faces direct impact from local zoning: recent municipal land-use updates in 2024 increased allowable outparcel density in 12% of its markets, while stricter mixed-use caps in 8% limited redevelopment potential, affecting projected NOI growth of ~1.3% annually if expansions are blocked; mastering these political environments is critical to preserve asset value and expansion economics.

Federal tax policy and REIT status

As a REIT Wheeler must distribute at least 90% of taxable income to shareholders, a rule that preserved its 2024 effective tax profile and supported a 2024 total shareholder yield near 6.2%; any federal changes to corporate tax rates or to TCJA provisions through 2025–2026 could shift the economic benefit of the REIT wrapper. Legislative stability of the dividends-paid deduction is critical for Wheeler’s capital recycling—its 2024 asset turnover and $0.18/share quarterly payouts depend on predictable tax treatment. Policy risk could increase WACC and reduce FFO multiples if deductions are curtailed.

Infrastructure investment in secondary markets

Government support for essential retail

Political recognition of grocery stores and pharmacies as essential infrastructure stabilizes Wheeler REIT’s tenant base; during COVID-19 these tenants saw sales increases—grocery sales rose ~18% in 2020 and pharmacies maintained steady traffic—protecting rent collection and occupancy.

Policies bolstering food-supply resilience and subsidies for healthy-food access in low-income areas (e.g., federal nutrition assistance programs reaching >40 million households in 2024) align with Wheeler’s community-focused retail locations.

This alignment keeps Wheeler’s centers prioritized by planners and emergency responses, supporting long-term asset value and leasing demand in strategic corridors.

- Essential designation = higher occupancy/resilience

- Grocery sales +18% in 2020; nutrition programs >40M households (2024)

- Policy support increases asset priority for planners

Trade policies and tenant supply chains

International trade agreements and US tariff policies affect input costs for Wheeler’s retail tenants—discount and hardware chains saw import cost pressure after 2018–2020 tariffs, with US goods imports tariffs averaging 1.7% but specific steel/metal tariffs raising sector costs by up to 10–15% in 2018–2020.

Political volatility raising import costs can compress tenant EBITDA margins (retail averages 3–6%), increasing risk of missed rent or delayed expansion for small chains.

Wheeler must monitor federal trade stances and CBP data, using tenant-level sales and debt-service metrics to reassess credit exposure and occupancy risk.

- Tariff shocks can raise sector input costs up to 15%

- Retail EBITDA margins often 3–6%, vulnerable to cost increases

- Monitoring federal trade policy and tenant financials reduces lease default risk

Policy Shifts Drive Retail Returns: Zoning, REIT Rules, Infra Flows & Tariff Risks

Political factors: zoning changes (12% markets eased, 8% tightened in 2024) affect redevelopment and ~1.3% projected NOI growth; REIT tax rules (90% distribution) kept 2024 yield ~6.2% and $0.18/qtr; infrastructure funds (CHIPS+Infra $110B regional flows) can boost tenant sales 5–12%; tariffs historically raised input costs up to 15%, stressing retail EBITDA (3–6%).

| Factor | Key Data |

|---|---|

| Zoning | 12% eased / 8% tightened (2024) |

| REIT rules | 90% distribution; 2024 yield 6.2%; $0.18/qtr |

| Infrastructure | $110B regional flows; sales +5–12% |

| Tariffs | Input cost +≤15%; retail EBITDA 3–6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Wheeler Real Estate Investment Trust across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Wheeler REIT that streamlines external risk review, is easily dropped into presentations or planner packs, and allows quick note edits so teams can align on regulatory, economic, social, technological, environmental, and legal implications during strategy sessions.

Economic factors

Interest rate environment and debt servicing

The late-2025 interest rate environment—with the Fed funds target at 5.25–5.50% and 10‑year Treasury near 4.2% as of Dec 2025—raises Wheeler REIT’s cost of capital, increasing interest expense and refinancing costs on upcoming maturities. Higher rates can compress cap rates and reduce NAV, while heavier debt servicing squeezes cash flow; Wheeler’s liquidity and debt‑management (debt-to-equity and interest‑coverage ratios) will hinge on the Fed’s 2026 policy path.

Inflationary impact on operating costs

Persisting inflation raised US CPI to 3.4% in 2024, driving Wheeler REIT common area maintenance and insurance costs up ~6–8% year-over-year, squeezing margins on large retail assets.

Many leases permit pass-throughs, but CPI-linked cost jumps contributed to a national retail vacancy uptick to 7.1% in 2024, risking tenant defaults and lost rent for Wheeler.

Robust cost controls, capex prioritization, and lease clauses indexing recoveries to CPI and minimum rent floors are necessary to protect NOI.

Consumer spending power in secondary markets

Consumer spending power in Wheeler’s Southeast and Mid-Atlantic secondary markets drives foot traffic and sales for its grocery-anchored centers; metro unemployment averaged 3.8% in 2024 vs national 4.0%, while regional wage growth ran about 4.2% YoY, supporting steady retail demand.

A 2024 household median income of $62,400 in core markets underpins grocery sales, but a dip in consumer confidence—Conference Board index down 5.1% YoY—could shift purchases to discount grocers.

Such a shift would pressure rent rolls and compel Wheeler to reweight tenant mix toward value-oriented grocers and flexible lease terms to preserve occupancy and NOI.

Capital market volatility and liquidity

Wheeler’s ability to raise equity or issue new debt depends on capital market stability and investor appetite for retail REITs; US REIT equity issuance fell about 28% in 2024 vs 2023 amid higher rates and quarterly volatility (S&P Global, 2024).

Market volatility can restrict access to liquidity for acquisitions or capex, with commercial real estate lending down ~15% y/y in 2024, tightening credit availability for expansions.

Maintaining transparent financials—Wheeler’s trailing 12-month FFO margin and stable occupancy metrics—is critical to attract institutional and retail investors in a competitive capital environment.

- Equity/debt issuance sensitivity to market sentiment

- 2024 REIT equity issuance down ~28%

- CRE lending fell ~15% y/y in 2024

- Transparent FFO/occupancy crucial for investor access

Evolving retail landscape and tenant demand

The demand for physical retail space is driven by consolidation among national grocery chains—top 5 grocers gained ~4 percentage points market share to ~48% in 2024—while service-oriented tenants (healthcare, urgent care, dollar stores) grew leasing activity by ~12% year-over-year, favoring Wheeler’s grocery-anchored centers.

Economic shifts toward essentials during 2023–2025 have supported stable occupancy and same-store NOI resilience; grocery-anchored assets showed ~200–300 bps lower vacancy vs. non-anchored centers in 2024.

Wheeler must monitor market rents, tenant credit, and demographic trends; targeting recession-resistant tenants can sustain rental income and reduce rent volatility, with grocery-anchored centers historically delivering mid-single-digit rent growth.

- Grocery market share consolidation: top 5 ≈48% (2024)

- Service-tenant leasing growth: ≈12% YoY (2024)

- Lower vacancy for grocery-anchored: ≈200–300 bps advantage (2024)

- Target: recession-resistant tenants to sustain mid-single-digit rent growth

Higher rates squeeze Wheeler: rising costs, tighter cash flow, retail shift to value

Higher rates (Fed 5.25–5.50% late‑2025; 10y ≈4.2%) raise Wheeler’s refinancing and interest costs, compress NAV and stress cash flow; 2024–25 inflation/CPI (~3.4% in 2024) lifted OPEX ~6–8%, while retail vacancy rose to 7.1% (2024), forcing tenant mix shifts toward value and service tenants to protect NOI.

| Metric | Value (2024–25) |

|---|---|

| Fed funds | 5.25–5.50% |

| 10‑yr Treasury | ≈4.2% |

| CPI (US) | ≈3.4% |

| Retail vacancy (US) | 7.1% |

| REIT equity issuance | −28% YoY (2024) |

| CRE lending | −15% YoY (2024) |

Full Version Awaits

Wheeler Real Estate Investment Trust PESTLE Analysis

The preview shown here is the exact Wheeler Real Estate Investment Trust PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.