Wielton Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Wielton faces moderate supplier leverage, rising buyer price sensitivity, and steady rivalry from European trailer makers, while new entrants and substitutes exert limited but growing pressure as logistics tech evolves; strategic moves in cost, innovation, and distribution will shape resilience and margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Wielton’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Raw material price volatility, notably steel and aluminum, remained a key cost driver for Wielton late 2025: steel billet prices averaged about $720/ton in Q4 2025, up ~18% year-over-year, squeezing margins when price increases can't be passed on.

Commodity swings directly hit gross margin—Wielton reported a 120 bps margin contraction H2 2025—so the firm uses long-term supply contracts and multi-region sourcing (Poland, Turkey, Italy) to limit single-supplier risk.

Concentration of Specialized Component Providers

Energy Costs and Production Efficiency

Energy prices in Central and Eastern Europe drove Wielton’s 2024 manufacturing energy spend to about 6% of COGS, and spot gas and power volatility in 2025—up to ±25% since Jan—keeps supplier pricing power high for energy‑intensive parts.

Geopolitical risk in 2025 means parts suppliers can pass higher fuel and electricity costs downstream; Wielton reported supplier cost inflation of ~4–7% in 2024.

Wielton’s investment in energy‑efficient presses and LED lighting cut factory energy intensity by 12% in 2023–24, limiting exposure to future price shocks and reducing unit production cost risk.

Impact of Global Supply Chain Stability

Supplier Integration and Technical Collaboration

Supplier Integration and Technical Collaboration raises supplier power as suppliers now co-design trailers’ telematics and smart monitoring, creating dependency on proprietary software/hardware; Wielton faced a 2024 supplier-related redesign cost increase estimated at 6–8% of unit BOM (bill of materials).

This improves reliability and offers 12–18% uptime gains for fleets but locks Wielton to specific vendors, making supplier-switching costly and time-consuming.

Here’s the quick math: replacing a telematics module can trigger redesign and validation costs of €200–€450 per unit and 3–6 months of development delay, so supplier hold-up risk is material.

- Suppliers co-design telematics → higher switching cost

- 2024 redesign cost rise ~6–8% of BOM

- Fleet uptime +12–18% with integrated systems

- Swap cost ≈ €200–€450/unit and 3–6 months delay

Suppliers Exert Moderate‑High Power on Wielton Despite Scale and Contracts

Suppliers hold moderate-to-high power for Wielton due to concentrated OEMs for axles/electronics (SAF‑HOLLAND, BPW), long lead times (26 weeks in 2024), and commodity/energy volatility (steel ~$720/ton Q4 2025; supplier inflation 4–7% in 2024), though Wielton’s PLN 1.6bn scale, long-term contracts, and 10–15% local sourcing plan reduce but do not eliminate risk.

| Metric | Value |

|---|---|

| Steel price Q4 2025 | $720/ton |

| Lead times (2024) | 26 weeks |

| Wielton rev (2024) | PLN 1.6bn |

| Supplier inflation (2024) | 4–7% |

What is included in the product

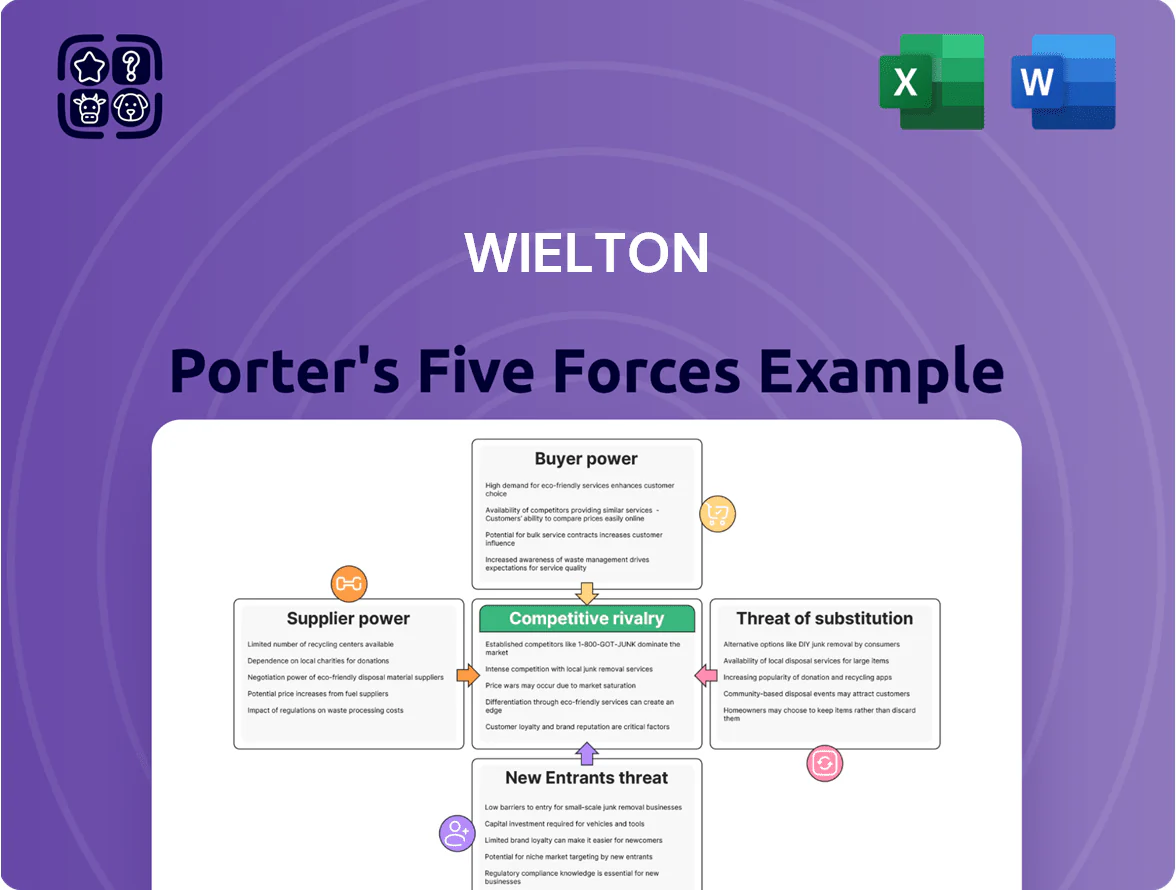

Analyzes competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and identifies disruptive forces and entry barriers shaping Wielton’s profitability and strategic positioning.

Clear, one-sheet Wielton Porter Five Forces summary that maps supplier, buyer, entrant, substitute, and rivalry pressures—perfect for quick strategic decisions and slide-ready reporting.

Customers Bargaining Power

Consolidation of Major Logistics Fleets

Large logistics operators like DB Schenker and DHL (global fleet spends >€3bn annually) leverage volume to secure discounts of 8–15% and extended 60–90 day payment terms, pressing Wielton on price.

These buyers demand telematics integration and custom chassis/ISO fittings; 2024 survey: 62% of fleets require OEM telematics as standard, raising unit customization cost by ~€1,200–€2,500.

Wielton must trade lower margins for scale—balancing price cuts with service SLAs—to win contracts where a single client can represent 5–12% of annual revenue.

Price Sensitivity in Commodity Transport

Smaller transport firms and contractors rank initial purchase price as decisive; 68% of EU SME hauliers cited cost as top factor in a 2024 ACEA survey, so price sensitivity is high.

With 2025 borrowing costs elevated (ECB main rate 4.00% in Dec 2025), buyers compare brands on sticker and financing terms.

Wielton mitigates this by offering three product tiers and leasing via partners like BNP Paribas Leasing, cutting upfront cost by up to 40% in 2024 campaigns.

Low Switching Costs Between Major Brands

The standardized design of semi-trailers means fleet operators can swap manufacturers with low friction; industry data shows top-tier models share 80–90% component commonality, so price or service drives 60% of tender awards.

Brand reputation for durability helps, but functional similarity makes switching easy—European fleet churn hit ~12% in 2024 when uptime or pricing lagged.

Wielton raises switching costs by offering extended after-sales programs, 24‑month warranty and 48‑hour spare parts delivery in 90% of EU markets, improving retention and reducing churn risk.

Demand for Sustainable and Green Solutions

Availability of Comprehensive Financing Options

At purchase time, customers often pick the trailer maker offering the lowest total cost of ownership (finance, maintenance, buy-back), so financing terms heavily sway demand; in Europe 2024 data show 58% of commercial-vehicle buyers cited financing as a top buying factor.

Wielton’s integrated finance and after-sales packages—if matching peers’ typical 3–5 year leasing deals and residual guarantees—directly cut churn and increase fleet repeat orders.

- 58% of buyers: financing key (Europe, 2024)

- Typical lease term: 3–5 years

- Buy-back/residuals raise repeat orders

- Integrated finance needed to retain diverse fleets

Wielton faces buyer power: deep discounts, telematics mandates; counters with leasing & warranties

Buyers wield strong leverage: large fleets secure 8–15% price cuts and 60–90 day terms, single clients can be 5–12% of Wielton revenue, and 2024 data show 62% require OEM telematics; price and financing drive 58% of purchases. Wielton offsets this with tiered products, leasing (up to 40% lower upfront), extended warranties and 48‑hour parts to raise switching costs.

| Metric | Value (2024–25) |

|---|---|

| Buyer discounts | 8–15% |

| Payment terms | 60–90 days |

| OEM telematics required | 62% |

| Buyers citing financing | 58% |

| Upfront cut via leasing | up to 40% |

| Single-client revenue share | 5–12% |

What You See Is What You Get

Wielton Porter's Five Forces Analysis

This preview shows the exact Wielton Porter Five Forces Analysis you'll receive after purchase—no mockups or placeholders—fully formatted, professionally written, and ready for immediate download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Wielton faces moderate supplier leverage, rising buyer price sensitivity, and steady rivalry from European trailer makers, while new entrants and substitutes exert limited but growing pressure as logistics tech evolves; strategic moves in cost, innovation, and distribution will shape resilience and margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Wielton’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Raw material price volatility, notably steel and aluminum, remained a key cost driver for Wielton late 2025: steel billet prices averaged about $720/ton in Q4 2025, up ~18% year-over-year, squeezing margins when price increases can't be passed on.

Commodity swings directly hit gross margin—Wielton reported a 120 bps margin contraction H2 2025—so the firm uses long-term supply contracts and multi-region sourcing (Poland, Turkey, Italy) to limit single-supplier risk.

Concentration of Specialized Component Providers

Energy Costs and Production Efficiency

Energy prices in Central and Eastern Europe drove Wielton’s 2024 manufacturing energy spend to about 6% of COGS, and spot gas and power volatility in 2025—up to ±25% since Jan—keeps supplier pricing power high for energy‑intensive parts.

Geopolitical risk in 2025 means parts suppliers can pass higher fuel and electricity costs downstream; Wielton reported supplier cost inflation of ~4–7% in 2024.

Wielton’s investment in energy‑efficient presses and LED lighting cut factory energy intensity by 12% in 2023–24, limiting exposure to future price shocks and reducing unit production cost risk.

Impact of Global Supply Chain Stability

Supplier Integration and Technical Collaboration

Supplier Integration and Technical Collaboration raises supplier power as suppliers now co-design trailers’ telematics and smart monitoring, creating dependency on proprietary software/hardware; Wielton faced a 2024 supplier-related redesign cost increase estimated at 6–8% of unit BOM (bill of materials).

This improves reliability and offers 12–18% uptime gains for fleets but locks Wielton to specific vendors, making supplier-switching costly and time-consuming.

Here’s the quick math: replacing a telematics module can trigger redesign and validation costs of €200–€450 per unit and 3–6 months of development delay, so supplier hold-up risk is material.

- Suppliers co-design telematics → higher switching cost

- 2024 redesign cost rise ~6–8% of BOM

- Fleet uptime +12–18% with integrated systems

- Swap cost ≈ €200–€450/unit and 3–6 months delay

Suppliers Exert Moderate‑High Power on Wielton Despite Scale and Contracts

Suppliers hold moderate-to-high power for Wielton due to concentrated OEMs for axles/electronics (SAF‑HOLLAND, BPW), long lead times (26 weeks in 2024), and commodity/energy volatility (steel ~$720/ton Q4 2025; supplier inflation 4–7% in 2024), though Wielton’s PLN 1.6bn scale, long-term contracts, and 10–15% local sourcing plan reduce but do not eliminate risk.

| Metric | Value |

|---|---|

| Steel price Q4 2025 | $720/ton |

| Lead times (2024) | 26 weeks |

| Wielton rev (2024) | PLN 1.6bn |

| Supplier inflation (2024) | 4–7% |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and identifies disruptive forces and entry barriers shaping Wielton’s profitability and strategic positioning.

Clear, one-sheet Wielton Porter Five Forces summary that maps supplier, buyer, entrant, substitute, and rivalry pressures—perfect for quick strategic decisions and slide-ready reporting.

Customers Bargaining Power

Consolidation of Major Logistics Fleets

Large logistics operators like DB Schenker and DHL (global fleet spends >€3bn annually) leverage volume to secure discounts of 8–15% and extended 60–90 day payment terms, pressing Wielton on price.

These buyers demand telematics integration and custom chassis/ISO fittings; 2024 survey: 62% of fleets require OEM telematics as standard, raising unit customization cost by ~€1,200–€2,500.

Wielton must trade lower margins for scale—balancing price cuts with service SLAs—to win contracts where a single client can represent 5–12% of annual revenue.

Price Sensitivity in Commodity Transport

Smaller transport firms and contractors rank initial purchase price as decisive; 68% of EU SME hauliers cited cost as top factor in a 2024 ACEA survey, so price sensitivity is high.

With 2025 borrowing costs elevated (ECB main rate 4.00% in Dec 2025), buyers compare brands on sticker and financing terms.

Wielton mitigates this by offering three product tiers and leasing via partners like BNP Paribas Leasing, cutting upfront cost by up to 40% in 2024 campaigns.

Low Switching Costs Between Major Brands

The standardized design of semi-trailers means fleet operators can swap manufacturers with low friction; industry data shows top-tier models share 80–90% component commonality, so price or service drives 60% of tender awards.

Brand reputation for durability helps, but functional similarity makes switching easy—European fleet churn hit ~12% in 2024 when uptime or pricing lagged.

Wielton raises switching costs by offering extended after-sales programs, 24‑month warranty and 48‑hour spare parts delivery in 90% of EU markets, improving retention and reducing churn risk.

Demand for Sustainable and Green Solutions

Availability of Comprehensive Financing Options

At purchase time, customers often pick the trailer maker offering the lowest total cost of ownership (finance, maintenance, buy-back), so financing terms heavily sway demand; in Europe 2024 data show 58% of commercial-vehicle buyers cited financing as a top buying factor.

Wielton’s integrated finance and after-sales packages—if matching peers’ typical 3–5 year leasing deals and residual guarantees—directly cut churn and increase fleet repeat orders.

- 58% of buyers: financing key (Europe, 2024)

- Typical lease term: 3–5 years

- Buy-back/residuals raise repeat orders

- Integrated finance needed to retain diverse fleets

Wielton faces buyer power: deep discounts, telematics mandates; counters with leasing & warranties

Buyers wield strong leverage: large fleets secure 8–15% price cuts and 60–90 day terms, single clients can be 5–12% of Wielton revenue, and 2024 data show 62% require OEM telematics; price and financing drive 58% of purchases. Wielton offsets this with tiered products, leasing (up to 40% lower upfront), extended warranties and 48‑hour parts to raise switching costs.

| Metric | Value (2024–25) |

|---|---|

| Buyer discounts | 8–15% |

| Payment terms | 60–90 days |

| OEM telematics required | 62% |

| Buyers citing financing | 58% |

| Upfront cut via leasing | up to 40% |

| Single-client revenue share | 5–12% |

What You See Is What You Get

Wielton Porter's Five Forces Analysis

This preview shows the exact Wielton Porter Five Forces Analysis you'll receive after purchase—no mockups or placeholders—fully formatted, professionally written, and ready for immediate download and use.