Wielton PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and technological advances are shaping Wielton’s prospects in our concise PESTLE snapshot—designed to inform investors and strategists alike. Purchase the full PESTLE analysis for a complete, actionable breakdown of risks and opportunities, ready to download and use in your next decision or pitch.

Political factors

EU Infrastructure Funding Initiatives

The EU's Connecting Europe Facility pledged 33.7 billion euros for 2021–2027 mobility projects, boosting demand for Wielton's construction and logistics trailers as member states ramp up road and bridge works.

Political commitment to corridor upgrades (TEN-T) concentrates funds in Central and Eastern Europe, aligning with Wielton's Poland-based production and export markets.

Management should track annual disbursements and 2024–25 national allocation updates to scale capacity toward high-growth regions receiving the largest shares.

Geopolitical Stability in Eastern Europe

Wielton’s Polish roots and exposure to Eastern markets mean that tensions near the Ukrainian border materially affect operations; in 2024 Ukraine accounted for roughly 3–5% of regional freight flows affecting trailer demand. Political decisions on EU reconstruction aid—EU approved €50bn+ macro-financial assistance packages in 2024—and corridor designations can boost orders for transport equipment but also raise supply-chain disruption risk and cross-border safety costs.

Trade Policies and Tariffs

Changes in trade agreements and tariffs on inputs like steel—which rose 18% EU-wide in 2024—can increase Wielton's trailer production costs, squeezing 2024 gross margin (reported at 15.2%) if not mitigated.

Rising protectionism in Poland's export markets may force Wielton to expand localized assembly or switch suppliers; the company sourced ~42% of components from EU suppliers in 2023.

Navigating EU relations with non-member states (UK, Turkey) is critical for Wielton, given exports to non-EU markets accounted for ~34% of revenues in 2024.

Government Incentives for Fleet Modernization

Many EU governments rolled out subsidy schemes—for example, Poland’s 2024 Clean Transport Fund allocated €250m for fleet upgrades—boosting demand for efficient, safety-enhanced trailers and favoring manufacturers like Wielton.

These incentives, linked to 2030/2050 climate targets, accelerate replacement cycles: EU truck fleet renewals rose ~6% in 2024, directly increasing orders for high-tech trailer models.

Wielton sees revenue upside when policymakers subsidize end-users, lowering purchase barriers and shortening sales cycles.

- Poland Clean Transport Fund €250m (2024)

- EU truck fleet renewals +6% (2024)

- Subsidies shorten sales cycles, raise trailer demand

Regulatory Harmonization within the EU

Regulatory harmonization across the EU lowers compliance costs for heavy-duty vehicle makers like Wielton by cutting country-specific trailer modifications; EU-wide standards reduce rework and speed time-to-market.

According to EU Transport Committee data, unified technical standards could reduce manufacturing variant costs by up to 8% and support exportable unit volumes—Wielton reported 2024 revenues of PLN 2.3bn, gaining scale from cross-border sales.

- Lower compliance costs (≈8% reduction)

- Fewer country-specific variants

- Enhanced economies of scale for Wielton (PLN 2.3bn 2024 revenue)

EU funding, subsidies drive Wielton growth; steel costs & geopolitics threaten margins

EU funding (€33.7bn CEF 2021–27) and national subsidies (Poland Clean Transport Fund €250m 2024) boost Wielton trailer demand; EU truck renewals +6% (2024) raise replacement cycles. Trade/tariff shifts (steel +18% 2024) and regional tensions (Ukraine-linked flows 3–5%) pose cost and disruption risks; non-EU exports ~34% of 2024 revenues. Regulatory harmonization may cut variant costs ≈8%, aiding scale (PLN 2.3bn 2024).

| Metric | Value (2024) |

|---|---|

| Wielton revenue | PLN 2.3bn |

| Non-EU exports | ~34% |

| Steel price change | +18% |

| Truck renewals | +6% |

| CEF funding | €33.7bn (2021–27) |

| Poland fund | €250m (2024) |

What is included in the product

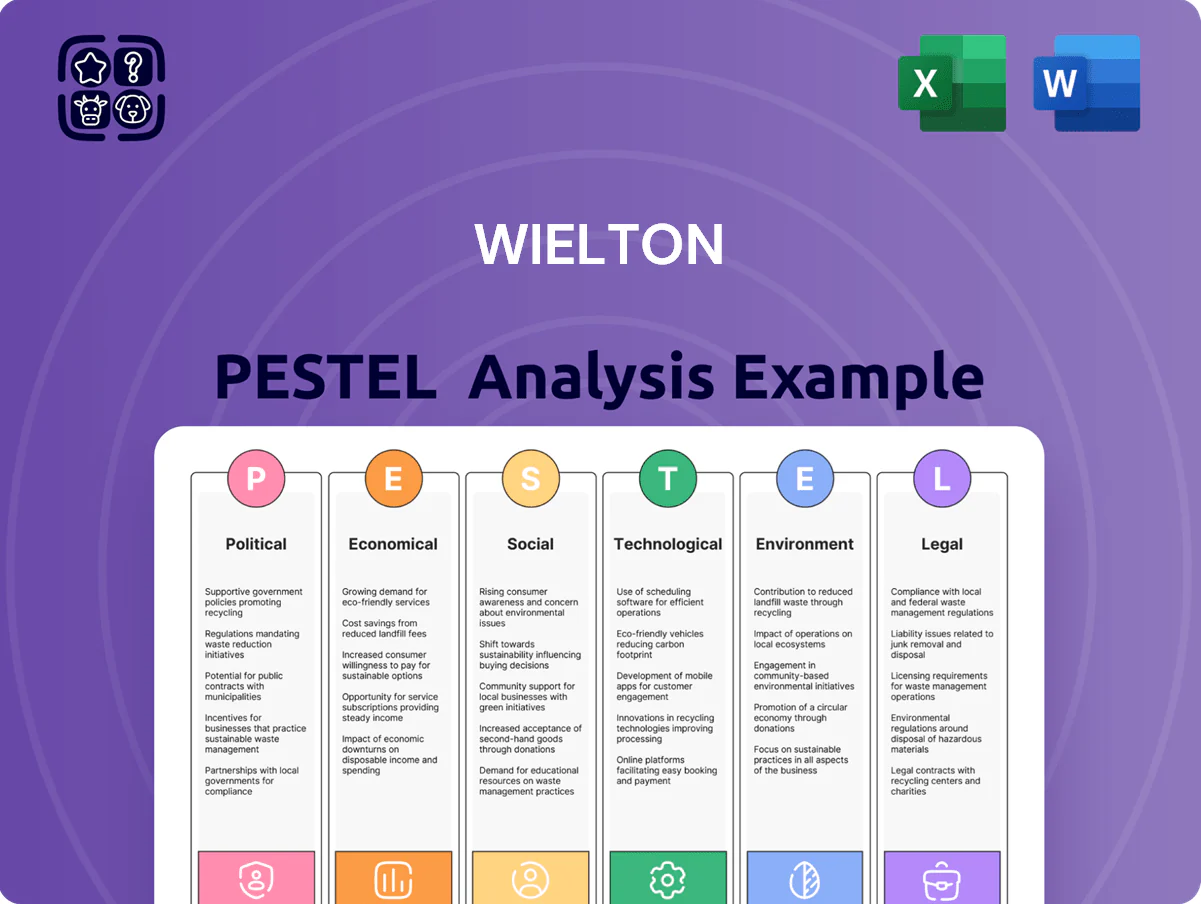

Explores how external macro-environmental factors uniquely affect Wielton across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities for executives, investors, and strategists.

Concise Wielton PESTLE summary, neatly segmented by category for quick interpretation and easy insertion into presentations or strategy packs to support risk discussions and team alignment.

Economic factors

Fluctuations in Raw Material Costs

The 2025 surge in high-strength steel (+18% YoY) and aluminum (+12% YoY) has materially squeezed Wielton's margins, prompting adoption of flexible pricing and hedging; management reported raw material cost inflation increased COGS by ~7 percentage points in H1 2025. Analysts track commodity futures and hedging ratios to assess whether Wielton can sustain competitive pricing without eroding net margin targets near 6–8%.

Interest Rate and Financing Environments

Central bank rate moves shape leasing and purchase costs for transport firms; the ECB rate at 3.50% in Dec 2025 raised borrowing costs compared with near-zero levels in 2021, slowing fleet expansion and capex for many carriers. Higher rates reduce demand for new trailers—industry capex fell ~12% in 2023—while easing cycles historically spur replacement waves. Wielton’s sales depend on affordable credit across its SME and large-carrier customers, with ~60% of European transport firms citing financing as a key purchase constraint in 2024.

Labor Cost Inflation in Central Europe

Rising wages in Poland and neighbors erode Wielton’s low-cost edge: average hourly labor costs in Poland rose 8.3% y/y in 2024 to €8.9, while Czech and Slovak rates climbed similarly, pressuring margins.

Tightening labor markets (Poland unemployment ~2.8% in 2024) force Wielton to balance higher pay with CAPEX for automation; the company may need 10–20% productivity gains to offset wage inflation.

Regional shifts require strategic talent retention—investing in training and process improvements to lift output per worker and protect EBITDA amid rising labor costs.

Currency Exchange Rate Volatility

As a major exporter, Wielton is highly sensitive to PLN/EUR swings; a 10% zloty appreciation in 2024 would cut euro-priced margins by roughly 8–12%, directly reducing repatriated profits.

End-2025 financial strategy emphasizes sophisticated hedging—forward contracts and options—covering an estimated 60–75% of near-term FX exposure and increased localized production in EU plants to lower currency risk.

- 10% PLN appreciation → ~8–12% margin hit

- 60–75% of exposure hedged (end-2025)

- Expanded EU production to shift costs into euros

GDP Growth and Industrial Output

The demand for semi-trailers is pro-cyclical, tracking European GDP and industrial output; Eurozone GDP grew 0.5% q/q in Q4 2025 and industrial production rose 1.2% y/y, supporting higher road freight volumes and trailer orders.

When growth slows—as in 2023’s flat GDP and -0.6% industrial output—buyers deferred purchases and maintenance, reducing new vehicle orders and highlighting the need for macro-driven production planning at Wielton.

- Pro-cyclical demand tied to Eurozone GDP and industrial output

- Q4 2025: Eurozone GDP +0.5% q/q, industrial production +1.2% y/y

- 2023 slowdown: flat GDP, industrial output -0.6% drove order deferrals

- Macroeconomic forecasting critical for production scheduling and inventory

Rising input costs, tight labor and PLN strength squeeze margins despite hedges

Commodity inflation (steel +18%, aluminum +12% in 2025) raised COGS ~7pp H1 2025; wage inflation (Poland hourly +8.3% in 2024) and tight labor (unemployment ~2.8% 2024) press margins; ECB rate 3.50% (Dec 2025) tightened financing, cutting industry capex ~12% in 2023; FX: 10% PLN appreciation → ~8–12% euro-margin hit, 60–75% exposure hedged end-2025.

| Metric | Value |

|---|---|

| Steel/Aluminum 2025 | +18% / +12% |

| COGS impact H1 2025 | +7 pp |

| Poland hourly 2024 | €8.9 (+8.3%) |

| Unemployment Poland 2024 | ~2.8% |

| ECB rate Dec 2025 | 3.50% |

| Industry capex 2023 | -12% |

| PLN FX sensitivity | 10% → -8–12% margin |

| Hedging coverage end-2025 | 60–75% |

What You See Is What You Get

Wielton PESTLE Analysis

The preview shown here is the exact Wielton PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and technological advances are shaping Wielton’s prospects in our concise PESTLE snapshot—designed to inform investors and strategists alike. Purchase the full PESTLE analysis for a complete, actionable breakdown of risks and opportunities, ready to download and use in your next decision or pitch.

Political factors

EU Infrastructure Funding Initiatives

The EU's Connecting Europe Facility pledged 33.7 billion euros for 2021–2027 mobility projects, boosting demand for Wielton's construction and logistics trailers as member states ramp up road and bridge works.

Political commitment to corridor upgrades (TEN-T) concentrates funds in Central and Eastern Europe, aligning with Wielton's Poland-based production and export markets.

Management should track annual disbursements and 2024–25 national allocation updates to scale capacity toward high-growth regions receiving the largest shares.

Geopolitical Stability in Eastern Europe

Wielton’s Polish roots and exposure to Eastern markets mean that tensions near the Ukrainian border materially affect operations; in 2024 Ukraine accounted for roughly 3–5% of regional freight flows affecting trailer demand. Political decisions on EU reconstruction aid—EU approved €50bn+ macro-financial assistance packages in 2024—and corridor designations can boost orders for transport equipment but also raise supply-chain disruption risk and cross-border safety costs.

Trade Policies and Tariffs

Changes in trade agreements and tariffs on inputs like steel—which rose 18% EU-wide in 2024—can increase Wielton's trailer production costs, squeezing 2024 gross margin (reported at 15.2%) if not mitigated.

Rising protectionism in Poland's export markets may force Wielton to expand localized assembly or switch suppliers; the company sourced ~42% of components from EU suppliers in 2023.

Navigating EU relations with non-member states (UK, Turkey) is critical for Wielton, given exports to non-EU markets accounted for ~34% of revenues in 2024.

Government Incentives for Fleet Modernization

Many EU governments rolled out subsidy schemes—for example, Poland’s 2024 Clean Transport Fund allocated €250m for fleet upgrades—boosting demand for efficient, safety-enhanced trailers and favoring manufacturers like Wielton.

These incentives, linked to 2030/2050 climate targets, accelerate replacement cycles: EU truck fleet renewals rose ~6% in 2024, directly increasing orders for high-tech trailer models.

Wielton sees revenue upside when policymakers subsidize end-users, lowering purchase barriers and shortening sales cycles.

- Poland Clean Transport Fund €250m (2024)

- EU truck fleet renewals +6% (2024)

- Subsidies shorten sales cycles, raise trailer demand

Regulatory Harmonization within the EU

Regulatory harmonization across the EU lowers compliance costs for heavy-duty vehicle makers like Wielton by cutting country-specific trailer modifications; EU-wide standards reduce rework and speed time-to-market.

According to EU Transport Committee data, unified technical standards could reduce manufacturing variant costs by up to 8% and support exportable unit volumes—Wielton reported 2024 revenues of PLN 2.3bn, gaining scale from cross-border sales.

- Lower compliance costs (≈8% reduction)

- Fewer country-specific variants

- Enhanced economies of scale for Wielton (PLN 2.3bn 2024 revenue)

EU funding, subsidies drive Wielton growth; steel costs & geopolitics threaten margins

EU funding (€33.7bn CEF 2021–27) and national subsidies (Poland Clean Transport Fund €250m 2024) boost Wielton trailer demand; EU truck renewals +6% (2024) raise replacement cycles. Trade/tariff shifts (steel +18% 2024) and regional tensions (Ukraine-linked flows 3–5%) pose cost and disruption risks; non-EU exports ~34% of 2024 revenues. Regulatory harmonization may cut variant costs ≈8%, aiding scale (PLN 2.3bn 2024).

| Metric | Value (2024) |

|---|---|

| Wielton revenue | PLN 2.3bn |

| Non-EU exports | ~34% |

| Steel price change | +18% |

| Truck renewals | +6% |

| CEF funding | €33.7bn (2021–27) |

| Poland fund | €250m (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Wielton across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities for executives, investors, and strategists.

Concise Wielton PESTLE summary, neatly segmented by category for quick interpretation and easy insertion into presentations or strategy packs to support risk discussions and team alignment.

Economic factors

Fluctuations in Raw Material Costs

The 2025 surge in high-strength steel (+18% YoY) and aluminum (+12% YoY) has materially squeezed Wielton's margins, prompting adoption of flexible pricing and hedging; management reported raw material cost inflation increased COGS by ~7 percentage points in H1 2025. Analysts track commodity futures and hedging ratios to assess whether Wielton can sustain competitive pricing without eroding net margin targets near 6–8%.

Interest Rate and Financing Environments

Central bank rate moves shape leasing and purchase costs for transport firms; the ECB rate at 3.50% in Dec 2025 raised borrowing costs compared with near-zero levels in 2021, slowing fleet expansion and capex for many carriers. Higher rates reduce demand for new trailers—industry capex fell ~12% in 2023—while easing cycles historically spur replacement waves. Wielton’s sales depend on affordable credit across its SME and large-carrier customers, with ~60% of European transport firms citing financing as a key purchase constraint in 2024.

Labor Cost Inflation in Central Europe

Rising wages in Poland and neighbors erode Wielton’s low-cost edge: average hourly labor costs in Poland rose 8.3% y/y in 2024 to €8.9, while Czech and Slovak rates climbed similarly, pressuring margins.

Tightening labor markets (Poland unemployment ~2.8% in 2024) force Wielton to balance higher pay with CAPEX for automation; the company may need 10–20% productivity gains to offset wage inflation.

Regional shifts require strategic talent retention—investing in training and process improvements to lift output per worker and protect EBITDA amid rising labor costs.

Currency Exchange Rate Volatility

As a major exporter, Wielton is highly sensitive to PLN/EUR swings; a 10% zloty appreciation in 2024 would cut euro-priced margins by roughly 8–12%, directly reducing repatriated profits.

End-2025 financial strategy emphasizes sophisticated hedging—forward contracts and options—covering an estimated 60–75% of near-term FX exposure and increased localized production in EU plants to lower currency risk.

- 10% PLN appreciation → ~8–12% margin hit

- 60–75% of exposure hedged (end-2025)

- Expanded EU production to shift costs into euros

GDP Growth and Industrial Output

The demand for semi-trailers is pro-cyclical, tracking European GDP and industrial output; Eurozone GDP grew 0.5% q/q in Q4 2025 and industrial production rose 1.2% y/y, supporting higher road freight volumes and trailer orders.

When growth slows—as in 2023’s flat GDP and -0.6% industrial output—buyers deferred purchases and maintenance, reducing new vehicle orders and highlighting the need for macro-driven production planning at Wielton.

- Pro-cyclical demand tied to Eurozone GDP and industrial output

- Q4 2025: Eurozone GDP +0.5% q/q, industrial production +1.2% y/y

- 2023 slowdown: flat GDP, industrial output -0.6% drove order deferrals

- Macroeconomic forecasting critical for production scheduling and inventory

Rising input costs, tight labor and PLN strength squeeze margins despite hedges

Commodity inflation (steel +18%, aluminum +12% in 2025) raised COGS ~7pp H1 2025; wage inflation (Poland hourly +8.3% in 2024) and tight labor (unemployment ~2.8% 2024) press margins; ECB rate 3.50% (Dec 2025) tightened financing, cutting industry capex ~12% in 2023; FX: 10% PLN appreciation → ~8–12% euro-margin hit, 60–75% exposure hedged end-2025.

| Metric | Value |

|---|---|

| Steel/Aluminum 2025 | +18% / +12% |

| COGS impact H1 2025 | +7 pp |

| Poland hourly 2024 | €8.9 (+8.3%) |

| Unemployment Poland 2024 | ~2.8% |

| ECB rate Dec 2025 | 3.50% |

| Industry capex 2023 | -12% |

| PLN FX sensitivity | 10% → -8–12% margin |

| Hedging coverage end-2025 | 60–75% |

What You See Is What You Get

Wielton PESTLE Analysis

The preview shown here is the exact Wielton PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.