Wilbur-Ellis PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, supply-chain dynamics, and sustainability trends are shaping Wilbur-Ellis's strategic outlook in our concise PESTLE snapshot—designed to fast-track your analysis and decision-making; purchase the full PESTLE for a complete, editable breakdown and actionable recommendations.

Political factors

Global Trade Relations and Tariffs

US-China tariffs and shifting trade policies materially affect Wilbur-Ellis, as agricultural exports and imported specialty chemicals—which comprised roughly 42% of FY2024 segment revenues—face tariff risk; 2023 US-China goods tariffs averaged 7.5% vs pre-2018 levels under 3%.

Protectionist measures and changing alliances raise raw material costs and logistics expenses, contributing to input-cost volatility that squeezed global agribusiness margins in 2024, with freight rates up ~18% YoY.

Wilbur-Ellis’ Connell and Agribusiness divisions, with significant APAC exposure (APAC sales ~28% of consolidated FY2024 revenue), depend on stable relations to sustain export volume and margin profiles across the region.

Farm Bill Legislation and Subsidies

The 2024-2025 US Farm Bill updates critically affect Wilbur-Ellis’s customer base by shaping crop insurance, conservation payments, and commodity supports that drive farmer cashflow; USDA forecasts 2025 net farm income at roughly $144 billion, impacting input demand. Policymaker shifts toward climate-smart ag—reflected in a 20% uptick in conservation program funding in 2024—could raise demand for precision nutrition, carbon credits, and specialty inputs. Changes to subsidy formulas or insurance triggers may alter planting choices, directly affecting Wilbur-Ellis sales mix and working capital needs.

Geopolitical Stability in Supply Chains

Ongoing geopolitical tensions in Eastern Europe and the Middle East have increased fertilizer and energy-chemical price volatility, with global ammonia prices up ~45% year-over-year in 2024 and Brent crude averaging $82/bbl in 2024, raising input costs for Wilbur-Ellis.

Maritime security risks and potential disruptions to key shipping lanes—Black Sea, Suez—threaten transit times and insurance premiums, which rose ~30% for bulk cargoes during 2023–24, pressuring distribution margins.

Political instability elevates landed costs and inventory risk: delayed shipments drove average lead-time variability up roughly 20% in 2024, forcing higher safety stock and working capital for Wilbur-Ellis to maintain supply reliability.

Government Support for Sustainable Agriculture

- 2024–25 incentives > $10B

- Opportunity: inputs + advisory = higher recurring revenue

- Risk: policy reversal → need for diversification

Regional Regulatory Alignment in Asia

Regional regulatory alignment in ASEAN is critical for Wilbur-Ellis Connell, as the bloc accounted for about 7% of global chemical imports in 2024 and 5–7% annual growth in specialty agrochemicals across Southeast Asia; shifts in trade agreements or local political instability can disrupt supply chains and margins for specialty chemical distribution.

Continuous monitoring of country-level political risk and regulatory shifts is required to maintain compliance and protect market share in fast-growing markets like Vietnam and Indonesia.

- ASEAN = ~7% global chemical imports (2024)

- Specialty agrochemical growth 5–7% p.a. in SE Asia

- Track trade agreements, local political risk, regulatory changes

Tariffs, rising input costs and $10B+ incentives reshape Wilbur‑Ellis: risk and revenue spike

US-China tariffs, geopolitical tensions and maritime risks raised input and logistics costs for Wilbur-Ellis in 2024–25 (ammonia +45% YoY; Brent $82/bbl; freight insurance +30%), while 2024–25 US Farm Bill and >$10B in climate/regenerative incentives shifted demand toward precision inputs and advisory services (APAC ~28% revenue; ASEAN ~7% global chemical imports), creating both revenue upside and policy-reversal risk.

| Metric | 2024/25 Value |

|---|---|

| Ammonia prices | +45% YoY |

| Brent crude | $82/bbl |

| Freight insurance | +30% |

| APAC share (FY2024) | ~28% |

| ASEAN chemical imports | ~7% |

| Climate/regenerative incentives | >$10B |

What is included in the product

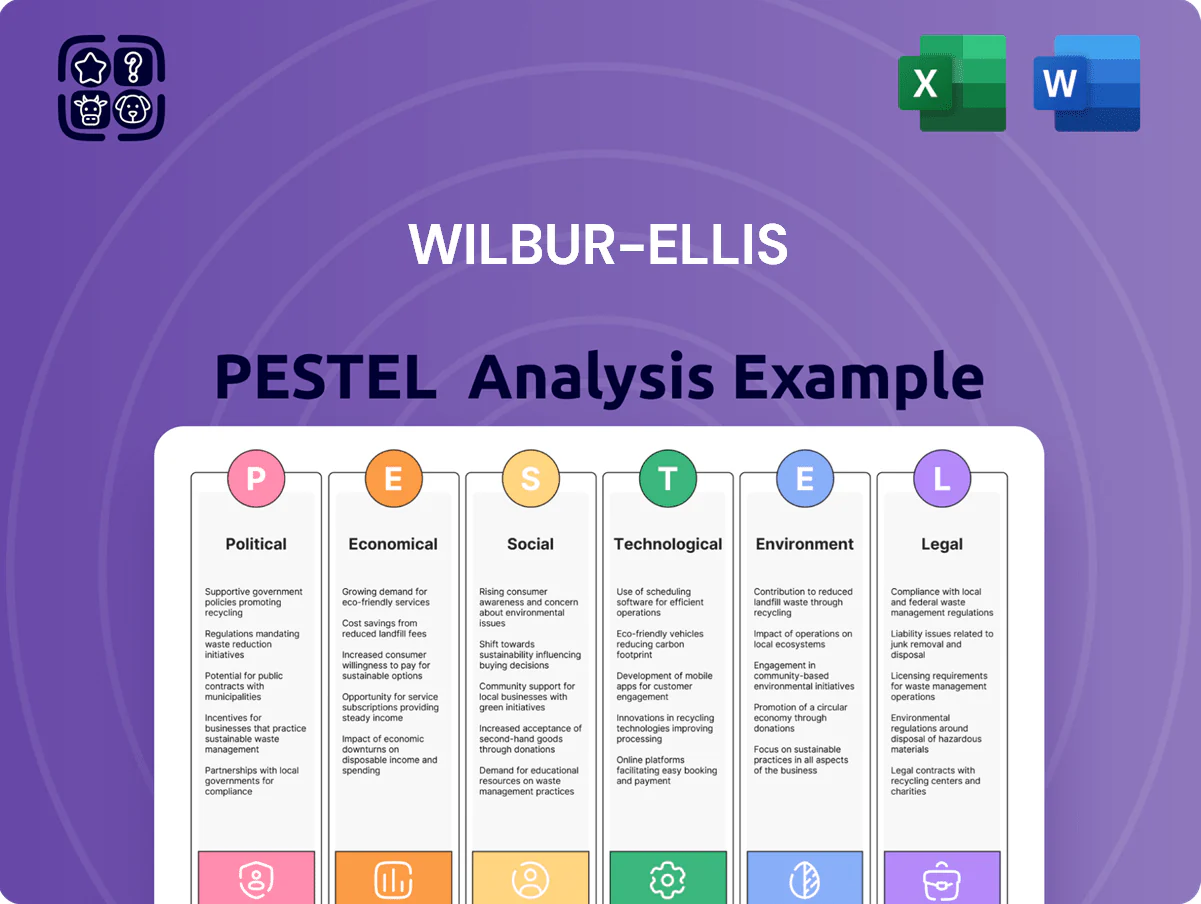

Explores how macro-environmental factors uniquely affect Wilbur-Ellis across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry trends to identify risks and opportunities.

Provides a concise, PESTLE-segmented summary of Wilbur-Ellis’s external environment that’s easy to drop into presentations or share across teams for faster strategic alignment and risk discussions.

Economic factors

Commodity Price Volatility

Fluctuations in corn, soy and wheat prices directly affect growers’ cash for Wilbur-Ellis inputs; for example, US corn fell ~18% in 2024 while soybean futures averaged down 12%, tightening farmer purchasing power and lowering volume for premium seeds and fertilizers.

Interest Rates and Credit Accessibility

As of late 2025, US benchmark rates around 5.25–5.50% raise Wilbur‑Ellis financing costs and increase working capital strain for distributors; higher borrowing costs elevated inventory carrying expenses by an estimated 1–2% of sales for ag distributors in 2024–25. Tight farm credit and a 2025 USDA farm loan uptick of ~8% constrained farmer capex, slowing equipment and precision-tech adoption. Stabilizing rates could lower W/E borrowing costs and enable M&A or CAPEX for facilities and digital platforms.

Currency Exchange Rate Fluctuations

Wilbur-Ellis faces currency risk as a strong U.S. dollar lowers competitiveness of U.S. agricultural exports and cut translated FY2024 foreign sales—around 18% of revenue—by an estimated $40–60 million versus a 10% dollar appreciation versus EUR/CNY. The company uses forward contracts and currency swaps and offsets exposure by sourcing ~25% of inputs in local currencies while matching regional sales and procurement to hedge translation risk.

Labor Costs and Workforce Availability

The agricultural and logistics sectors saw average hourly wages rise 4.2% year-over-year in 2024, while rural counties report a 6–8% shortfall in skilled labor for farm and distribution roles, pressuring Wilbur-Ellis to offer premium pay to retain staff.

Balancing higher compensation with efficiency, the company must optimize labor productivity in distribution centers and field teams to protect margins amid industry net income pressures.

Economic strain has accelerated capital expenditure into automation and digital tools; industry data show a 12–15% increase in ag-logistics automation investment in 2024, a trend Wilbur-Ellis is likely to follow to reduce human dependency.

- Wage growth ~4.2% (2024)

- Rural skilled labor shortfall 6–8%

- Ag-logistics automation investment up 12–15% (2024)

- Trade-off: higher compensation vs. automation capex

Global Fertilizer and Energy Costs

The production of nitrogen fertilizers is energy-intensive, tying Wilbur-Ellis’s input costs to global natural gas prices; U.S. natural gas Henry Hub averaged about 3.84 USD/MMBtu in 2024, up from 3.50 in 2023, pressuring margins on ammonia-based products.

Rapid energy-sector shifts can force quick fertilizer price spikes that may lag in being passed to growers, increasing working-capital strain given 2024 global urea spot prices near 420–460 USD/ton.

Continuous monitoring of global energy markets, hedging gas exposure and flexible sourcing are essential to set accurate prices and protect competitive position.

- 2024 Henry Hub ~3.84 USD/MMBtu

- Global urea ~420–460 USD/ton (2024)

- High pass-through lag raises working-capital risk

Commodity slump, higher rates and USD dent farmer margins and boost input costs

Commodity price drops (US corn -18% 2024; soy -12% 2024) cut farmer purchasing power; higher US rates (5.25–5.50% 2025) raised financing costs; USD strength reduced FY2024 foreign sales ~$40–60M; labor costs +4.2% and 6–8% rural skills gap; Henry Hub ~3.84 USD/MMBtu and urea $420–460/ton 2024 drove input-cost pressure.

| Metric | 2024/25 |

|---|---|

| Corn/soy | -18% / -12% |

| Rates | 5.25–5.50% |

| FX impact | $40–60M |

| Wages | +4.2% |

| Henry Hub | $3.84/MMBtu |

Preview the Actual Deliverable

Wilbur-Ellis PESTLE Analysis

The preview shown here is the exact Wilbur‑Ellis PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, supply-chain dynamics, and sustainability trends are shaping Wilbur-Ellis's strategic outlook in our concise PESTLE snapshot—designed to fast-track your analysis and decision-making; purchase the full PESTLE for a complete, editable breakdown and actionable recommendations.

Political factors

Global Trade Relations and Tariffs

US-China tariffs and shifting trade policies materially affect Wilbur-Ellis, as agricultural exports and imported specialty chemicals—which comprised roughly 42% of FY2024 segment revenues—face tariff risk; 2023 US-China goods tariffs averaged 7.5% vs pre-2018 levels under 3%.

Protectionist measures and changing alliances raise raw material costs and logistics expenses, contributing to input-cost volatility that squeezed global agribusiness margins in 2024, with freight rates up ~18% YoY.

Wilbur-Ellis’ Connell and Agribusiness divisions, with significant APAC exposure (APAC sales ~28% of consolidated FY2024 revenue), depend on stable relations to sustain export volume and margin profiles across the region.

Farm Bill Legislation and Subsidies

The 2024-2025 US Farm Bill updates critically affect Wilbur-Ellis’s customer base by shaping crop insurance, conservation payments, and commodity supports that drive farmer cashflow; USDA forecasts 2025 net farm income at roughly $144 billion, impacting input demand. Policymaker shifts toward climate-smart ag—reflected in a 20% uptick in conservation program funding in 2024—could raise demand for precision nutrition, carbon credits, and specialty inputs. Changes to subsidy formulas or insurance triggers may alter planting choices, directly affecting Wilbur-Ellis sales mix and working capital needs.

Geopolitical Stability in Supply Chains

Ongoing geopolitical tensions in Eastern Europe and the Middle East have increased fertilizer and energy-chemical price volatility, with global ammonia prices up ~45% year-over-year in 2024 and Brent crude averaging $82/bbl in 2024, raising input costs for Wilbur-Ellis.

Maritime security risks and potential disruptions to key shipping lanes—Black Sea, Suez—threaten transit times and insurance premiums, which rose ~30% for bulk cargoes during 2023–24, pressuring distribution margins.

Political instability elevates landed costs and inventory risk: delayed shipments drove average lead-time variability up roughly 20% in 2024, forcing higher safety stock and working capital for Wilbur-Ellis to maintain supply reliability.

Government Support for Sustainable Agriculture

- 2024–25 incentives > $10B

- Opportunity: inputs + advisory = higher recurring revenue

- Risk: policy reversal → need for diversification

Regional Regulatory Alignment in Asia

Regional regulatory alignment in ASEAN is critical for Wilbur-Ellis Connell, as the bloc accounted for about 7% of global chemical imports in 2024 and 5–7% annual growth in specialty agrochemicals across Southeast Asia; shifts in trade agreements or local political instability can disrupt supply chains and margins for specialty chemical distribution.

Continuous monitoring of country-level political risk and regulatory shifts is required to maintain compliance and protect market share in fast-growing markets like Vietnam and Indonesia.

- ASEAN = ~7% global chemical imports (2024)

- Specialty agrochemical growth 5–7% p.a. in SE Asia

- Track trade agreements, local political risk, regulatory changes

Tariffs, rising input costs and $10B+ incentives reshape Wilbur‑Ellis: risk and revenue spike

US-China tariffs, geopolitical tensions and maritime risks raised input and logistics costs for Wilbur-Ellis in 2024–25 (ammonia +45% YoY; Brent $82/bbl; freight insurance +30%), while 2024–25 US Farm Bill and >$10B in climate/regenerative incentives shifted demand toward precision inputs and advisory services (APAC ~28% revenue; ASEAN ~7% global chemical imports), creating both revenue upside and policy-reversal risk.

| Metric | 2024/25 Value |

|---|---|

| Ammonia prices | +45% YoY |

| Brent crude | $82/bbl |

| Freight insurance | +30% |

| APAC share (FY2024) | ~28% |

| ASEAN chemical imports | ~7% |

| Climate/regenerative incentives | >$10B |

What is included in the product

Explores how macro-environmental factors uniquely affect Wilbur-Ellis across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry trends to identify risks and opportunities.

Provides a concise, PESTLE-segmented summary of Wilbur-Ellis’s external environment that’s easy to drop into presentations or share across teams for faster strategic alignment and risk discussions.

Economic factors

Commodity Price Volatility

Fluctuations in corn, soy and wheat prices directly affect growers’ cash for Wilbur-Ellis inputs; for example, US corn fell ~18% in 2024 while soybean futures averaged down 12%, tightening farmer purchasing power and lowering volume for premium seeds and fertilizers.

Interest Rates and Credit Accessibility

As of late 2025, US benchmark rates around 5.25–5.50% raise Wilbur‑Ellis financing costs and increase working capital strain for distributors; higher borrowing costs elevated inventory carrying expenses by an estimated 1–2% of sales for ag distributors in 2024–25. Tight farm credit and a 2025 USDA farm loan uptick of ~8% constrained farmer capex, slowing equipment and precision-tech adoption. Stabilizing rates could lower W/E borrowing costs and enable M&A or CAPEX for facilities and digital platforms.

Currency Exchange Rate Fluctuations

Wilbur-Ellis faces currency risk as a strong U.S. dollar lowers competitiveness of U.S. agricultural exports and cut translated FY2024 foreign sales—around 18% of revenue—by an estimated $40–60 million versus a 10% dollar appreciation versus EUR/CNY. The company uses forward contracts and currency swaps and offsets exposure by sourcing ~25% of inputs in local currencies while matching regional sales and procurement to hedge translation risk.

Labor Costs and Workforce Availability

The agricultural and logistics sectors saw average hourly wages rise 4.2% year-over-year in 2024, while rural counties report a 6–8% shortfall in skilled labor for farm and distribution roles, pressuring Wilbur-Ellis to offer premium pay to retain staff.

Balancing higher compensation with efficiency, the company must optimize labor productivity in distribution centers and field teams to protect margins amid industry net income pressures.

Economic strain has accelerated capital expenditure into automation and digital tools; industry data show a 12–15% increase in ag-logistics automation investment in 2024, a trend Wilbur-Ellis is likely to follow to reduce human dependency.

- Wage growth ~4.2% (2024)

- Rural skilled labor shortfall 6–8%

- Ag-logistics automation investment up 12–15% (2024)

- Trade-off: higher compensation vs. automation capex

Global Fertilizer and Energy Costs

The production of nitrogen fertilizers is energy-intensive, tying Wilbur-Ellis’s input costs to global natural gas prices; U.S. natural gas Henry Hub averaged about 3.84 USD/MMBtu in 2024, up from 3.50 in 2023, pressuring margins on ammonia-based products.

Rapid energy-sector shifts can force quick fertilizer price spikes that may lag in being passed to growers, increasing working-capital strain given 2024 global urea spot prices near 420–460 USD/ton.

Continuous monitoring of global energy markets, hedging gas exposure and flexible sourcing are essential to set accurate prices and protect competitive position.

- 2024 Henry Hub ~3.84 USD/MMBtu

- Global urea ~420–460 USD/ton (2024)

- High pass-through lag raises working-capital risk

Commodity slump, higher rates and USD dent farmer margins and boost input costs

Commodity price drops (US corn -18% 2024; soy -12% 2024) cut farmer purchasing power; higher US rates (5.25–5.50% 2025) raised financing costs; USD strength reduced FY2024 foreign sales ~$40–60M; labor costs +4.2% and 6–8% rural skills gap; Henry Hub ~3.84 USD/MMBtu and urea $420–460/ton 2024 drove input-cost pressure.

| Metric | 2024/25 |

|---|---|

| Corn/soy | -18% / -12% |

| Rates | 5.25–5.50% |

| FX impact | $40–60M |

| Wages | +4.2% |

| Henry Hub | $3.84/MMBtu |

Preview the Actual Deliverable

Wilbur-Ellis PESTLE Analysis

The preview shown here is the exact Wilbur‑Ellis PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.