Williams Marketing Mix

Your Shortcut to a Strategic 4Ps Breakdown

Discover how Williams synchronizes Product, Price, Place, and Promotion to build competitive advantage—this concise preview highlights key tactics, but the full 4P’s Marketing Mix Analysis delivers editable, presentation-ready sections, real-world data, and actionable recommendations to save you hours and power strategic decisions.

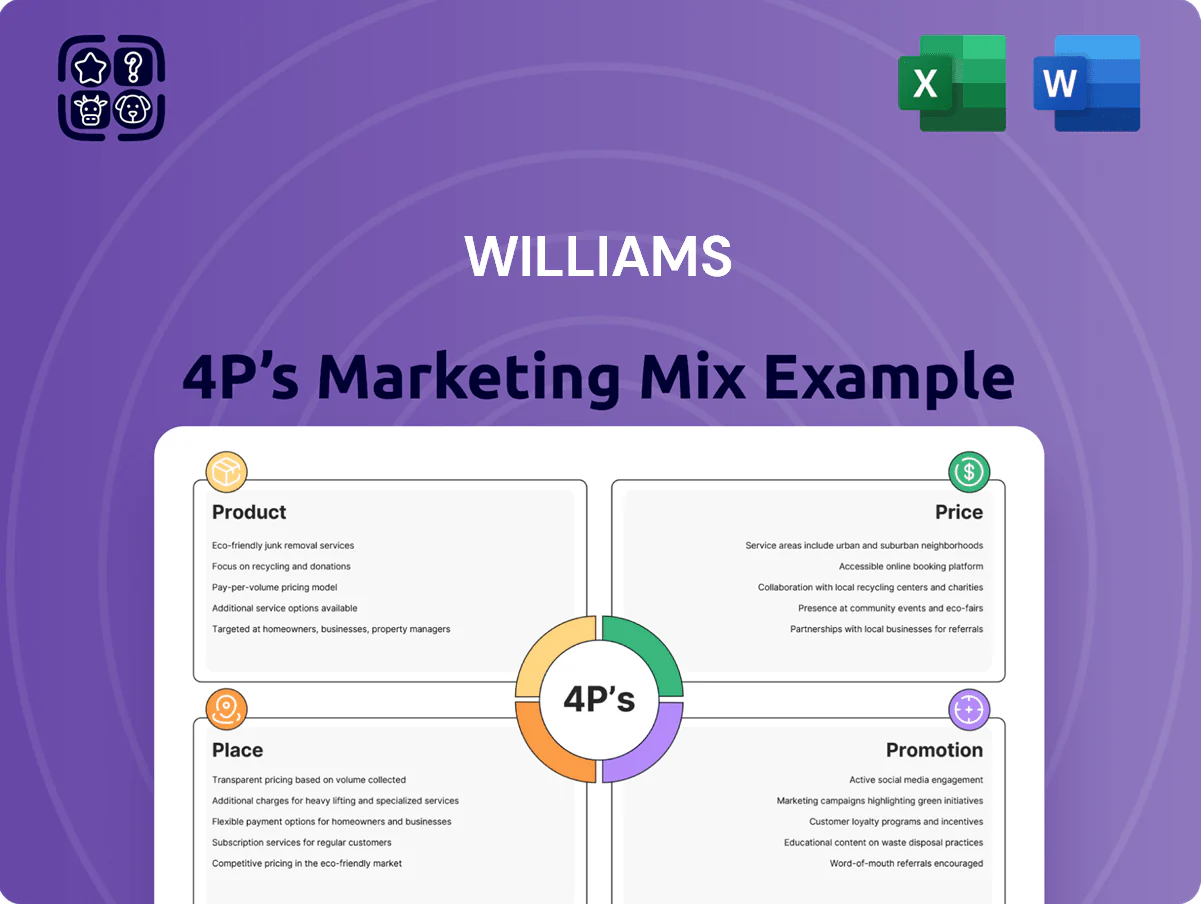

Product

Natural Gas Transmission Services

Williams’ Natural Gas Transmission Services center on the Transco pipeline, the largest U.S. interstate gas system, which in 2025 handled roughly 10.5 billion cubic feet per day (Bcf/d) capacity and remained the backbone of Williams’ portfolio, covering Gulf Coast to Eastern Seaboard delivery.

The product emphasizes high-capacity throughput and 99.95% system reliability targets to serve utility and industrial customers, underpinning firm transportation contracts that generated about $2.1 billion in segment EBITDA in 2024.

Gathering and Processing Infrastructure

Natural Gas Liquids Fractionation

Williams’ Natural Gas Liquids fractionation converts mixed NGLs into ethane, propane, and butane—key petrochemical feedstocks and heating/transport fuels—and by 2025 the company raised fractionation throughput to ~600,000 barrels per day, improving realized margins by ~180 basis points and contributing an estimated $420 million in incremental annual EBITDA versus 2022 levels.

Deepwater Gulf of Mexico Solutions

Low-Carbon Energy Ventures

- RNG and CCS launched late 2025

Williams: 10.5 Bcf/d Transco, 28% EBITDA Margin, $210M RNG/CCS Boost

Williams’ core product is high-capacity natural gas transmission (Transco ~10.5 Bcf/d in 2025) plus gathering/processing (~12,000 miles, 3.2 Bcf/d) and 600,000 bpd NGL fractionation, generating strong margins (adjusted EBITDA margin ~28% in 2025) with new RNG/CCS adding ~$210m revenue in 2025 and targeting 1.2 MtCO2e avoided by 2030.

| Product | 2025 Key metric |

|---|---|

| Transco capacity | 10.5 Bcf/d |

| Gathering/processing | 12,000 miles; 3.2 Bcf/d |

| NGL fractionation | 600,000 bpd |

| Adj. EBITDA margin | ~28% |

| RNG/CCS revenue | $210m |

What is included in the product

Delivers a company-specific deep dive into Williams’s Product, Price, Place, and Promotion strategies, using real brand practices and competitive context to ground insights.

Condenses Williams' 4P marketing analysis into a concise, presentation-ready snapshot that relieves briefing overload and accelerates strategic alignment for leadership and cross-functional teams.

Place

The Transco Pipeline Corridor

The Transco pipeline corridor spans ~10,500 miles from Texas to New York, reaching 7 of the 10 largest US metropolitan gas markets and transporting ~8.5 Bcf/d (2024 peak capacity), giving Williams direct access to high-margin Atlantic coast demand for heating and power generation.

Dominant Shale Basin Footprint

Gulf Coast Energy Hubs

Williams centers operations on the U.S. Gulf Coast, giving direct access to petrochemical complexes in Texas and Louisiana that handled about 70% of U.S. steam cracker feedstock throughput in 2024; this proximity boosts NGL (natural gas liquids) distribution and sales.

Gulf hubs supply natural gas to heavy manufacturers and refiners—Williams transported ~9.8 Bcf/d (billion cubic feet per day) on its networks in 2024—supporting domestic processing and export via nearby terminals.

LNG Export Terminal Connectivity

By end-2025 Williams had expanded pipeline capacity to Gulf Coast LNG export terminals, routing roughly 3.2 Bcf/d (billion cubic feet per day) toward Sabine Pass, Freeport, and Corpus Christi, enabling the firm to move domestic gas into global markets and capture export tolling fees and capacity premiums.

This placement leverages rising LNG demand—global LNG trade reached ~380 mtpa in 2024—positioning Williams to benefit from the transition-fuel shift and expected U.S. export growth of ~1–1.5 Bcf/d annual additions in 2025–26.

- 3.2 Bcf/d capacity to Gulf LNG terminals

Strategic Storage and Interconnects

- ~20 underground storage sites

- 1,500+ pipeline interconnects

- Supports seasonal injections/withdrawals

- 2024 midstream operating income: ~$2.8B

Williams: Coast‑to‑coast pipeline reach—10.5k mi Transco, 12k mi gathering, $2.8B midstream

Williams’ place strategy centers on coast-to-coast pipeline reach: Transco ~10,500 miles, 8.5 Bcf/d peak (2024); gathering ~12,000 miles, 7.2 Bcf/d gathered (2024) with ~$1.8B 2024 EBITDA; Gulf corridor ~9.8 Bcf/d moved (2024) and 3.2 Bcf/d to LNG terminals (end-2025); ~20 storage sites, 1,500+ interconnects, 2024 midstream operating income ~$2.8B.

| Metric | Value |

|---|---|

| Transco length | ~10,500 miles |

| Transco peak cap | 8.5 Bcf/d (2024) |

| Gathering network | ~12,000 miles; 7.2 Bcf/d (2024) |

| Gathering EBITDA | ~$1.8B (2024) |

| Gulf throughput | 9.8 Bcf/d (2024) |

| LNG routing | 3.2 Bcf/d (end-2025) |

| Storage sites | ~20 |

| Interconnects | 1,500+ |

| Midstream op income | ~$2.8B (2024) |

Full Version Awaits

Williams 4P's Marketing Mix Analysis

The preview shown here is the actual Williams 4P's Marketing Mix Analysis you’ll receive instantly after purchase—no surprises.

This is the exact, fully complete document you'll download immediately after checkout, editable and ready to use.

The file shown is not a sample or demo; it’s the final, high-quality analysis included with your order.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to a Strategic 4Ps Breakdown

Discover how Williams synchronizes Product, Price, Place, and Promotion to build competitive advantage—this concise preview highlights key tactics, but the full 4P’s Marketing Mix Analysis delivers editable, presentation-ready sections, real-world data, and actionable recommendations to save you hours and power strategic decisions.

Product

Natural Gas Transmission Services

Williams’ Natural Gas Transmission Services center on the Transco pipeline, the largest U.S. interstate gas system, which in 2025 handled roughly 10.5 billion cubic feet per day (Bcf/d) capacity and remained the backbone of Williams’ portfolio, covering Gulf Coast to Eastern Seaboard delivery.

The product emphasizes high-capacity throughput and 99.95% system reliability targets to serve utility and industrial customers, underpinning firm transportation contracts that generated about $2.1 billion in segment EBITDA in 2024.

Gathering and Processing Infrastructure

Natural Gas Liquids Fractionation

Williams’ Natural Gas Liquids fractionation converts mixed NGLs into ethane, propane, and butane—key petrochemical feedstocks and heating/transport fuels—and by 2025 the company raised fractionation throughput to ~600,000 barrels per day, improving realized margins by ~180 basis points and contributing an estimated $420 million in incremental annual EBITDA versus 2022 levels.

Deepwater Gulf of Mexico Solutions

Low-Carbon Energy Ventures

- RNG and CCS launched late 2025

Williams: 10.5 Bcf/d Transco, 28% EBITDA Margin, $210M RNG/CCS Boost

Williams’ core product is high-capacity natural gas transmission (Transco ~10.5 Bcf/d in 2025) plus gathering/processing (~12,000 miles, 3.2 Bcf/d) and 600,000 bpd NGL fractionation, generating strong margins (adjusted EBITDA margin ~28% in 2025) with new RNG/CCS adding ~$210m revenue in 2025 and targeting 1.2 MtCO2e avoided by 2030.

| Product | 2025 Key metric |

|---|---|

| Transco capacity | 10.5 Bcf/d |

| Gathering/processing | 12,000 miles; 3.2 Bcf/d |

| NGL fractionation | 600,000 bpd |

| Adj. EBITDA margin | ~28% |

| RNG/CCS revenue | $210m |

What is included in the product

Delivers a company-specific deep dive into Williams’s Product, Price, Place, and Promotion strategies, using real brand practices and competitive context to ground insights.

Condenses Williams' 4P marketing analysis into a concise, presentation-ready snapshot that relieves briefing overload and accelerates strategic alignment for leadership and cross-functional teams.

Place

The Transco Pipeline Corridor

The Transco pipeline corridor spans ~10,500 miles from Texas to New York, reaching 7 of the 10 largest US metropolitan gas markets and transporting ~8.5 Bcf/d (2024 peak capacity), giving Williams direct access to high-margin Atlantic coast demand for heating and power generation.

Dominant Shale Basin Footprint

Gulf Coast Energy Hubs

Williams centers operations on the U.S. Gulf Coast, giving direct access to petrochemical complexes in Texas and Louisiana that handled about 70% of U.S. steam cracker feedstock throughput in 2024; this proximity boosts NGL (natural gas liquids) distribution and sales.

Gulf hubs supply natural gas to heavy manufacturers and refiners—Williams transported ~9.8 Bcf/d (billion cubic feet per day) on its networks in 2024—supporting domestic processing and export via nearby terminals.

LNG Export Terminal Connectivity

By end-2025 Williams had expanded pipeline capacity to Gulf Coast LNG export terminals, routing roughly 3.2 Bcf/d (billion cubic feet per day) toward Sabine Pass, Freeport, and Corpus Christi, enabling the firm to move domestic gas into global markets and capture export tolling fees and capacity premiums.

This placement leverages rising LNG demand—global LNG trade reached ~380 mtpa in 2024—positioning Williams to benefit from the transition-fuel shift and expected U.S. export growth of ~1–1.5 Bcf/d annual additions in 2025–26.

- 3.2 Bcf/d capacity to Gulf LNG terminals

Strategic Storage and Interconnects

- ~20 underground storage sites

- 1,500+ pipeline interconnects

- Supports seasonal injections/withdrawals

- 2024 midstream operating income: ~$2.8B

Williams: Coast‑to‑coast pipeline reach—10.5k mi Transco, 12k mi gathering, $2.8B midstream

Williams’ place strategy centers on coast-to-coast pipeline reach: Transco ~10,500 miles, 8.5 Bcf/d peak (2024); gathering ~12,000 miles, 7.2 Bcf/d gathered (2024) with ~$1.8B 2024 EBITDA; Gulf corridor ~9.8 Bcf/d moved (2024) and 3.2 Bcf/d to LNG terminals (end-2025); ~20 storage sites, 1,500+ interconnects, 2024 midstream operating income ~$2.8B.

| Metric | Value |

|---|---|

| Transco length | ~10,500 miles |

| Transco peak cap | 8.5 Bcf/d (2024) |

| Gathering network | ~12,000 miles; 7.2 Bcf/d (2024) |

| Gathering EBITDA | ~$1.8B (2024) |

| Gulf throughput | 9.8 Bcf/d (2024) |

| LNG routing | 3.2 Bcf/d (end-2025) |

| Storage sites | ~20 |

| Interconnects | 1,500+ |

| Midstream op income | ~$2.8B (2024) |

Full Version Awaits

Williams 4P's Marketing Mix Analysis

The preview shown here is the actual Williams 4P's Marketing Mix Analysis you’ll receive instantly after purchase—no surprises.

This is the exact, fully complete document you'll download immediately after checkout, editable and ready to use.

The file shown is not a sample or demo; it’s the final, high-quality analysis included with your order.