Willis Towers Watson Porter's Five Forces Analysis

Don't Miss the Bigger Picture

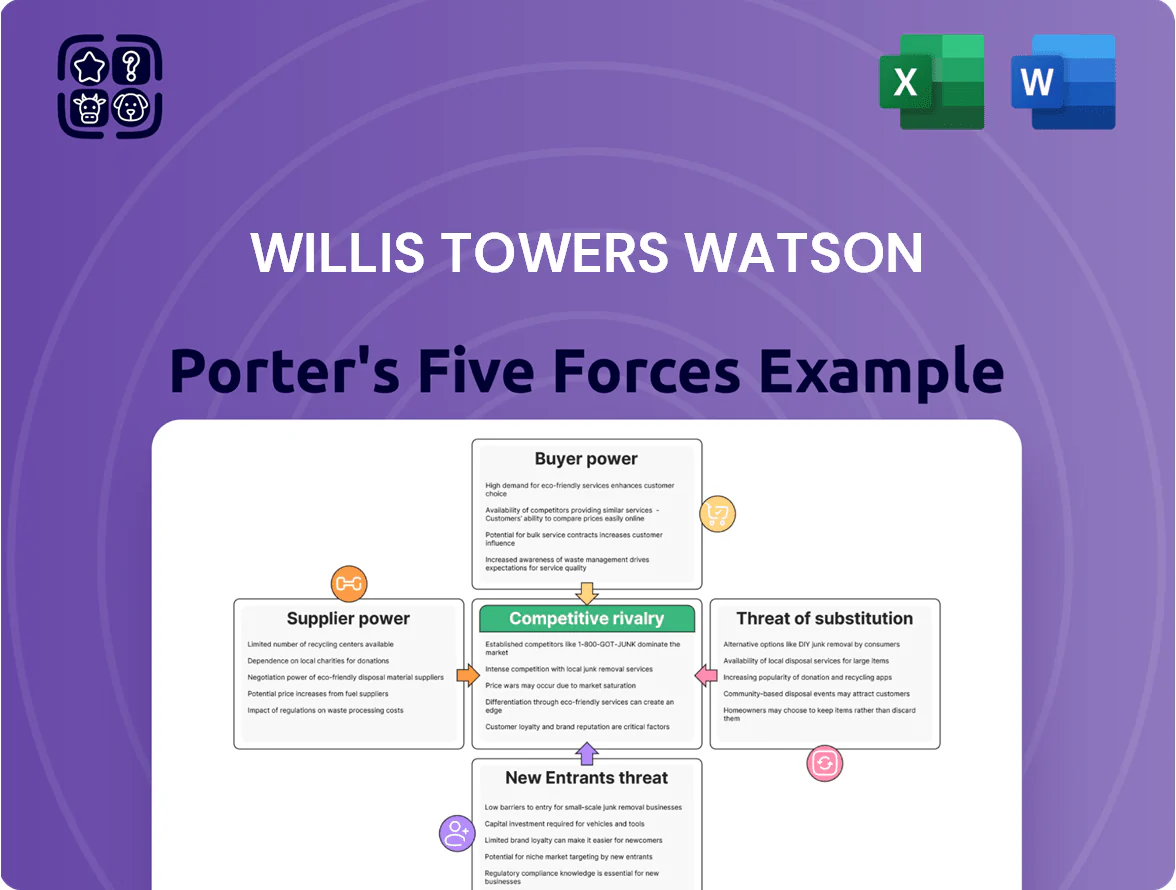

Willis Towers Watson faces moderate buyer power, regulatory pressures, and evolving tech-driven substitutes that shape its advisory and insurance markets; supplier strength and barriers to entry remain mixed, creating both risks and strategic openings. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Willis Towers Watson’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Human Capital and Specialized Talent

As a professional services firm, Willis Towers Watson relies on consultants, actuaries, and brokers whose intellectual capital is the primary supplier input; their work drives revenue and client retention.

The bargaining power of these specialists is high: 2025 industry data show 4–6% annual wage inflation for actuarial and consulting roles and vacancy rates near 10%, boosting leverage.

To retain top talent, Willis Towers Watson needs competitive pay—total rewards often 20–30% above base in bonuses and equity—and clear career pathways and training budgets roughly 2–4% of payroll.

Technology and Data Providers

Willis Towers Watson (WTW) depends on third-party software, cloud providers, and data aggregators for its analytics; industry data shows global cloud IaaS/SaaS spend reached about $550B in 2024, so supplier leverage is real. Switching costs are moderate-to-high due to integrations and need for high-quality data for models; surveys find 62% of insurers cite data quality as a top vendor risk. Strategic tech partnerships (e.g., AWS, Microsoft) keep WTW competitive.

Insurance Carriers and Underwriters

As broker, Willis Towers Watson (WTW) depends on insurance carriers for risk capacity, so carriers effectively shape the products WTW can sell and their pricing.

Industry consolidation reduced carrier count: global top 10 insurers control roughly 40% of premium volume (2024), raising carriers’ bargaining leverage over brokers like WTW.

That power forces WTW to invest in carrier relationships and scale—WTW reported 2024 revenue of $10.3bn—so securing favorable terms requires deal-making and data-driven negotiation.

Regulatory and Compliance Bodies

Global regulators act as indirect suppliers by setting standards that Willis Towers Watson (WTW) must meet; non-compliance risks fines—GDPR fines reached €1.5B cumulatively by 2023, so data rules materially matter to WTW.

Keeping up with evolving financial and privacy laws requires major investment; WTW reported $1.8B in technology and data-related spend in 2024, which regulators can inflate by changing rules.

Regulatory shifts can force service-model changes and raise costs quickly, giving regulators high bargaining power over WTW’s margins and operational flexibility.

- Regulators = indirect suppliers setting standards

- GDPR fines €1.5B (to 2023); compliance non-negotiable

- WTW tech/data spend $1.8B in 2024

- Rule changes can raise costs, cut flexibility

Real Estate and Infrastructure Providers

Suppliers wield moderate power: wage inflation, vacancy, WTW spend & insurer concentration

Suppliers (talent, tech, carriers, landlords, regulators) exert high-to-moderate bargaining power: 4–6% wage inflation and ~10% vacancy (2025); WTW pay mix: bonuses/equity +20–30%; cloud/data spend $1.8B (2024); WTW 2024 revenue $10.3B; top10 insurers ~40% premium share (2024); office cuts ~12% space, ~8% rent saved (2025).

| Item | Metric |

|---|---|

| Wage inflation | 4–6% (2025) |

| Vacancy rate | ~10% (2025) |

| WTW pay mix | +20–30% bonuses/equity |

| Cloud/data spend | $1.8B (2024) |

| WTW revenue | $10.3B (2024) |

| Top insurers share | ~40% (2024) |

| Office cuts | ~12% space, ~8% rent (2025) |

What is included in the product

Tailored exclusively for Willis Towers Watson, this Porter's Five Forces analysis uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats shaping its profitability and strategic positioning.

Concise Porter's Five Forces summary tailored for Willis Towers Watson—instantly visualize competitive pressures and relief points with an editable radar chart to streamline strategic decisions.

Customers Bargaining Power

Concentration of Large Corporate Clients

WTW serves many Fortune Global 500 clients; in 2024 roughly 40% of its revenue came from large multinational accounts, giving those clients strong bargaining power via high volume and repeat business. These firms demand tailored programs and volume discounts, compressing WTW’s margins—WTW’s 2024 operating margin of ~9.2% reflects pricing pressure versus peers. Frequent competitive RFPs force WTW to prove superior value and innovate to retain contracts.

Low Switching Costs for Advisory Services

While Willis Towers Watson (WTW) often keeps long-term client ties, switching costs to rivals like Aon or Marsh McLennan are low—clients commonly move brokerage or consulting at annual renewals or after project end dates.

This mobility pressured WTW in 2024: client retention programs and advisory revenues tied to renewals—about 48% of 2024 commercial advisory contract renewals—forced higher service SLAs.

WTW counters by offering proprietary data and model-based insights—its 2024 human capital analytics platform drove repeat sales, making relationships stickier and harder for competitors to copy.

Increased Financial Sophistication of Buyers

Modern treasury and HR teams now hire ex-consultants who know advisory economics, cutting WTW’s information edge and enabling tougher fee and scope negotiations; in 2024-25 48% of corporate finance hires were from consulting, per McKinsey talent data. Buyers use data-driven benchmarks—clients expect ROI proof and compare WTW against market rates (average consulting fee compression ~6% in 2024), forcing clearer value evidence.

Availability of Alternative Risk Financing

- Global ILS issuance $17.5bn (2024)

- Clients >$100m consider captives

- WTW needs advisory on captives, ILS, parametrics

Consolidation within Client Industries

Mergers among WTW’s clients shrink the pool of high-value buyers and raise churn risk: a single lost merged account can equal multiple legacy contracts, hitting WTW’s FY2024 revenue of $9.2bn (reported 2024) if large clients consolidate.

Consolidation boosts buyer leverage, pushing WTW toward broader global-service bids at lower margins—large combined buyers often demand unified platforms and discounted fees across regions.

- Fewer high-value clients → higher revenue concentration risk

- One merged account can replace several contracts

- Buyers demand global, lower‑margin deals

- 2024 revenue $9.2bn underscores exposure

WTW: Global clients squeeze fees but proprietary analytics protect $9.2B revenue

Large multinational clients drive strong bargaining power at WTW: ~40% of 2024 revenue from global accounts, $9.2bn total revenue, and ~9.2% operating margin. Clients use captives/ILS ($17.5bn ILS issuance 2024) and frequent RFPs to push fees down (~6% consulting fee compression 2024). WTW offsets with proprietary analytics and advisory services to retain contracts.

| Metric | 2024 |

|---|---|

| Revenue | $9.2bn |

| Global accounts % | ~40% |

| Op margin | ~9.2% |

| ILS issuance | $17.5bn |

| Fee compression | ~6% |

Preview Before You Purchase

Willis Towers Watson Porter's Five Forces Analysis

This preview shows the exact Willis Towers Watson Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy, containing complete assessment of industry rivalry, supplier power, buyer power, threat of entrants, and threat of substitutes.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Willis Towers Watson faces moderate buyer power, regulatory pressures, and evolving tech-driven substitutes that shape its advisory and insurance markets; supplier strength and barriers to entry remain mixed, creating both risks and strategic openings. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Willis Towers Watson’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Human Capital and Specialized Talent

As a professional services firm, Willis Towers Watson relies on consultants, actuaries, and brokers whose intellectual capital is the primary supplier input; their work drives revenue and client retention.

The bargaining power of these specialists is high: 2025 industry data show 4–6% annual wage inflation for actuarial and consulting roles and vacancy rates near 10%, boosting leverage.

To retain top talent, Willis Towers Watson needs competitive pay—total rewards often 20–30% above base in bonuses and equity—and clear career pathways and training budgets roughly 2–4% of payroll.

Technology and Data Providers

Willis Towers Watson (WTW) depends on third-party software, cloud providers, and data aggregators for its analytics; industry data shows global cloud IaaS/SaaS spend reached about $550B in 2024, so supplier leverage is real. Switching costs are moderate-to-high due to integrations and need for high-quality data for models; surveys find 62% of insurers cite data quality as a top vendor risk. Strategic tech partnerships (e.g., AWS, Microsoft) keep WTW competitive.

Insurance Carriers and Underwriters

As broker, Willis Towers Watson (WTW) depends on insurance carriers for risk capacity, so carriers effectively shape the products WTW can sell and their pricing.

Industry consolidation reduced carrier count: global top 10 insurers control roughly 40% of premium volume (2024), raising carriers’ bargaining leverage over brokers like WTW.

That power forces WTW to invest in carrier relationships and scale—WTW reported 2024 revenue of $10.3bn—so securing favorable terms requires deal-making and data-driven negotiation.

Regulatory and Compliance Bodies

Global regulators act as indirect suppliers by setting standards that Willis Towers Watson (WTW) must meet; non-compliance risks fines—GDPR fines reached €1.5B cumulatively by 2023, so data rules materially matter to WTW.

Keeping up with evolving financial and privacy laws requires major investment; WTW reported $1.8B in technology and data-related spend in 2024, which regulators can inflate by changing rules.

Regulatory shifts can force service-model changes and raise costs quickly, giving regulators high bargaining power over WTW’s margins and operational flexibility.

- Regulators = indirect suppliers setting standards

- GDPR fines €1.5B (to 2023); compliance non-negotiable

- WTW tech/data spend $1.8B in 2024

- Rule changes can raise costs, cut flexibility

Real Estate and Infrastructure Providers

Suppliers wield moderate power: wage inflation, vacancy, WTW spend & insurer concentration

Suppliers (talent, tech, carriers, landlords, regulators) exert high-to-moderate bargaining power: 4–6% wage inflation and ~10% vacancy (2025); WTW pay mix: bonuses/equity +20–30%; cloud/data spend $1.8B (2024); WTW 2024 revenue $10.3B; top10 insurers ~40% premium share (2024); office cuts ~12% space, ~8% rent saved (2025).

| Item | Metric |

|---|---|

| Wage inflation | 4–6% (2025) |

| Vacancy rate | ~10% (2025) |

| WTW pay mix | +20–30% bonuses/equity |

| Cloud/data spend | $1.8B (2024) |

| WTW revenue | $10.3B (2024) |

| Top insurers share | ~40% (2024) |

| Office cuts | ~12% space, ~8% rent (2025) |

What is included in the product

Tailored exclusively for Willis Towers Watson, this Porter's Five Forces analysis uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats shaping its profitability and strategic positioning.

Concise Porter's Five Forces summary tailored for Willis Towers Watson—instantly visualize competitive pressures and relief points with an editable radar chart to streamline strategic decisions.

Customers Bargaining Power

Concentration of Large Corporate Clients

WTW serves many Fortune Global 500 clients; in 2024 roughly 40% of its revenue came from large multinational accounts, giving those clients strong bargaining power via high volume and repeat business. These firms demand tailored programs and volume discounts, compressing WTW’s margins—WTW’s 2024 operating margin of ~9.2% reflects pricing pressure versus peers. Frequent competitive RFPs force WTW to prove superior value and innovate to retain contracts.

Low Switching Costs for Advisory Services

While Willis Towers Watson (WTW) often keeps long-term client ties, switching costs to rivals like Aon or Marsh McLennan are low—clients commonly move brokerage or consulting at annual renewals or after project end dates.

This mobility pressured WTW in 2024: client retention programs and advisory revenues tied to renewals—about 48% of 2024 commercial advisory contract renewals—forced higher service SLAs.

WTW counters by offering proprietary data and model-based insights—its 2024 human capital analytics platform drove repeat sales, making relationships stickier and harder for competitors to copy.

Increased Financial Sophistication of Buyers

Modern treasury and HR teams now hire ex-consultants who know advisory economics, cutting WTW’s information edge and enabling tougher fee and scope negotiations; in 2024-25 48% of corporate finance hires were from consulting, per McKinsey talent data. Buyers use data-driven benchmarks—clients expect ROI proof and compare WTW against market rates (average consulting fee compression ~6% in 2024), forcing clearer value evidence.

Availability of Alternative Risk Financing

- Global ILS issuance $17.5bn (2024)

- Clients >$100m consider captives

- WTW needs advisory on captives, ILS, parametrics

Consolidation within Client Industries

Mergers among WTW’s clients shrink the pool of high-value buyers and raise churn risk: a single lost merged account can equal multiple legacy contracts, hitting WTW’s FY2024 revenue of $9.2bn (reported 2024) if large clients consolidate.

Consolidation boosts buyer leverage, pushing WTW toward broader global-service bids at lower margins—large combined buyers often demand unified platforms and discounted fees across regions.

- Fewer high-value clients → higher revenue concentration risk

- One merged account can replace several contracts

- Buyers demand global, lower‑margin deals

- 2024 revenue $9.2bn underscores exposure

WTW: Global clients squeeze fees but proprietary analytics protect $9.2B revenue

Large multinational clients drive strong bargaining power at WTW: ~40% of 2024 revenue from global accounts, $9.2bn total revenue, and ~9.2% operating margin. Clients use captives/ILS ($17.5bn ILS issuance 2024) and frequent RFPs to push fees down (~6% consulting fee compression 2024). WTW offsets with proprietary analytics and advisory services to retain contracts.

| Metric | 2024 |

|---|---|

| Revenue | $9.2bn |

| Global accounts % | ~40% |

| Op margin | ~9.2% |

| ILS issuance | $17.5bn |

| Fee compression | ~6% |

Preview Before You Purchase

Willis Towers Watson Porter's Five Forces Analysis

This preview shows the exact Willis Towers Watson Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy, containing complete assessment of industry rivalry, supplier power, buyer power, threat of entrants, and threat of substitutes.