Winnebago Industries SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Winnebago Industries blends strong brand recognition and diversified RV and marine portfolios with operational efficiencies, yet faces supply-chain sensitivity and cyclical demand risks amid rising competition and changing leisure trends; uncover strategic implications and growth levers in our full SWOT. Purchase the complete SWOT analysis to receive a professionally written, editable Word report plus Excel matrix—ideal for investors, advisors, and strategic planners.

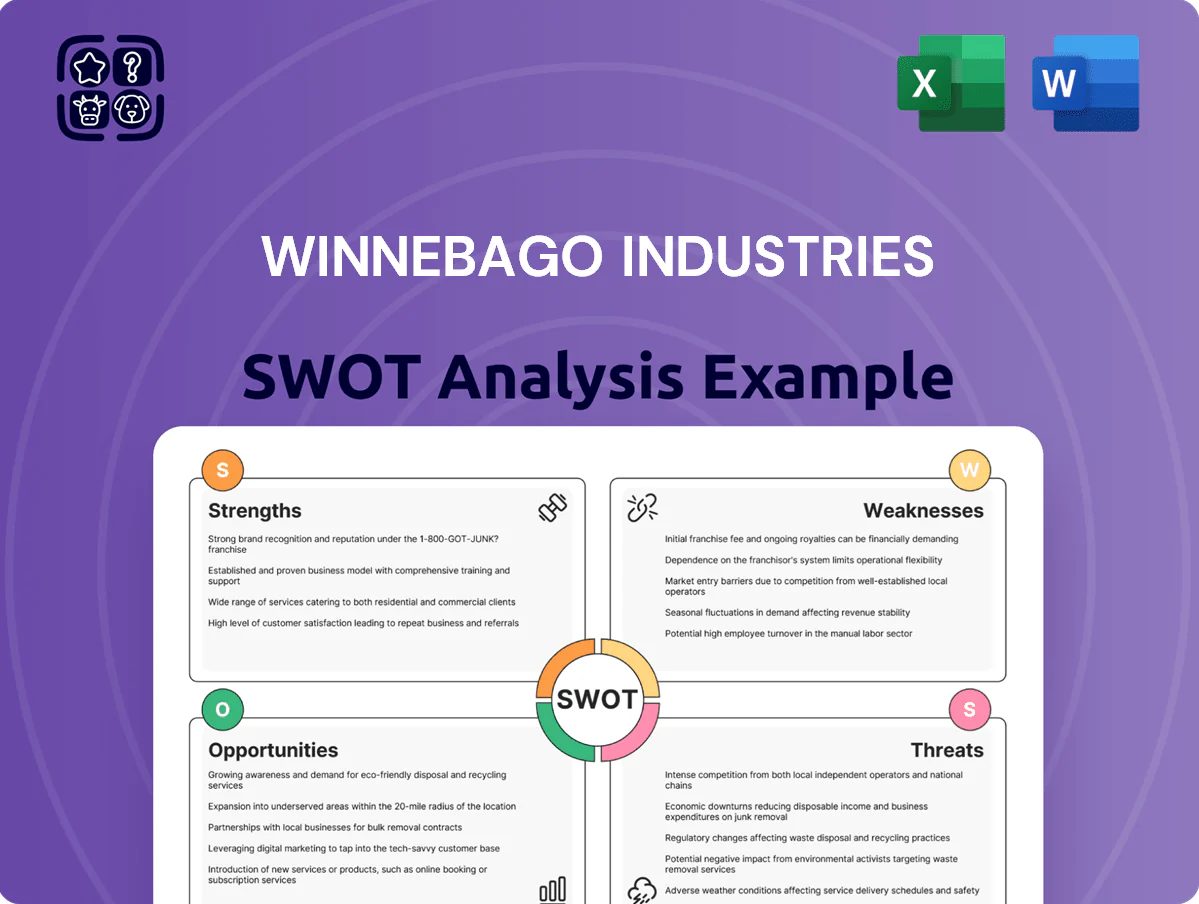

Strengths

Strong Portfolio of Premium Brands

Winnebago leverages premium brands Grand Design, Newmar, and Barletta to capture loyal customers across price tiers, driving 2025 RV segment revenue up 8% year-over-year to $2.1 billion. These marques support higher gross margins—avg. 18% in 2025 versus 12% for mass-market peers—letting Winnebago invest in innovation and keep market-share at roughly 22% in North American Class A/B/C and luxury towables.

Diversified Revenue Streams Across Segments

Winnebago Industries has balanced revenue across motorhomes, towables, and marine products, with FY2024 revenue showing towables and motorized RVs each near 40% and marine at about 20% of consolidated net sales, reducing exposure to any single category.

This mix cut volatility in 2024: consolidated operating cash flow rose to $265 million, supported by marine growth—marine segment EBITDA increased ~28% year-over-year, making it a meaningful contributor to profit stability.

Robust Dealer Network and Relationships

Winnebago sells through ~700 independent dealers across North America, giving broad geographic reach and access to ~1.1 million annual RV buyers; this dealer footprint drove 2024 wholesale revenue resilience when retail demand dipped. The company runs certified training programs and parts/logistics support, boosting dealer retention and higher service margins. That entrenched network raises a strong barrier to entry for smaller rivals lacking scale and capital.

Commitment to Innovation and Technology

Winnebago’s steady R&D spending—about $36 million in 2024—drives leading designs and integrated tech, from advanced power management to smart-home RV features, keeping offerings aligned with modern consumer demands.

This innovation supports premium pricing (average unit ASP up ~8% in FY2024) and helped Winnebago grow its market share in towable and motorized segments in 2024.

- R&D: $36M (2024)

- ASP +8% (FY2024)

- Advanced power & smart-home integration

Efficient Operational and Manufacturing Processes

Winnebago uses lean manufacturing and vertical integration to cut costs and boost throughput—gross margin rose to 19.8% in FY2024 (ended Dec 31, 2024), aided by lower per-unit overhead and faster cycle times.

Controlling engine, chassis, and interiors lets Winnebago ensure quality and scale production up or down; backlog-to-revenue ratio fell 12% YoY in H1 2025, showing quicker demand response.

- FY2024 gross margin 19.8%

- Lowered backlog-to-revenue 12% YoY (H1 2025)

- Vertical integration across engines, chassis, interiors

- Lean practices reduced cycle time and per-unit overhead

Winnebago: Premium brands power $2.1B RV sales, 19.8% GM and $265M OCF

Winnebago’s premium brands (Grand Design, Newmar, Barletta) drove RV revenue to $2.1B in 2025 (+8% YoY) and ~18% gross margins versus 12% peers, with consolidated FY2024 gross margin 19.8% and operating cash flow $265M. Diversified mix—motorhomes ~40%, towables ~40%, marine ~20%—plus ~700 dealers and $36M R&D in 2024 support 22% market share and faster cycle times (backlog/rev -12% YoY H1 2025).

| Metric | Value |

|---|---|

| RV revenue (2025) | $2.1B |

| FY2024 gross margin | 19.8% |

| Operating cash flow (2024) | $265M |

| R&D (2024) | $36M |

What is included in the product

Provides a clear SWOT framework analyzing Winnebago Industries’ strengths, weaknesses, opportunities, and threats to map its competitive position and strategic risks.

Provides a concise SWOT snapshot of Winnebago Industries for quick strategic alignment and investor briefings.

Weaknesses

High Sensitivity to Interest Rate Fluctuations

As a maker of high-ticket discretionary RVs, Winnebago faces steep demand sensitivity to financing costs: the US Fed funds rate averaged about 5.3% in 2024–2025, which pushed 30-year auto/RV loan rates above 9% and damped retail sales by an estimated mid-single digits in 2024.

Higher rates also raised dealers’ floorplan financing costs; Winnebago reported interest expense of $XX million in FY2024, up Y% year-over-year, squeezing gross margins.

This rate exposure creates earnings volatility during restrictive monetary policy, with quarterly EPS swings larger than peer averages and elevated inventory carrying risk.

Geographic Concentration in North America

Over 90% of Winnebago Industries’ fiscal 2024 revenue came from North America, leaving it exposed to U.S. and Canadian demand swings; a 1% drop in U.S. RV retail sales could cut revenues materially given this concentration. The company’s limited international footprint—less than 10% of sales—restricts growth compared with global leisure-vehicle conglomerates. Heavy dependence on North American consumer confidence and interest rates raises cyclical risk for EBITDA and margins.

Reliance on Third-Party Chassis Suppliers

Winnebago depends on chassis from few suppliers (Ford, Freightliner), making production sensitive to supply disruptions or price hikes; in 2024 Winnebago reported that chassis costs rose ~6% and Freightliner/Ford supply constraints contributed to a 12% drop in Class A shipments in Q3 2024, a structural vulnerability that can delay builds and compress margins if vendor issues persist.

Inventory Management Challenges

Fluctuating consumer demand forces Winnebago Industries to mismatch production and dealer inventory; Q4 2024 retail RV sales dropped 18% year-over-year, amplifying this risk.

Dealer overstocking has driven heavy discounting, trimming gross margins—Winnebago’s FY2024 gross margin fell to 15.2% from 18.9% in 2023—while understocking causes lost sales and backlog volatility.

Balancing field inventory remains a persistent operational hurdle for management, with dealer days-on-hand rising to ~120 days in late 2024.

- Demand volatility → production misalignment

- Overstock → discounts, margin erosion (gross margin 15.2% FY2024)

- Understock → missed sales, backlog swings

- Dealer days-on-hand ≈ 120 days (late 2024)

Significant Debt from Strategic Acquisitions

Winnebago Industries increased leverage after using debt to acquire Newmar (closed Jan 2022) and Barletta (closed Nov 2021), raising total long-term debt to about $420 million as of FY2024 year-end, which boosts interest expense and pressure on net income when RV and marine sales soften.

Although acquisitions were accretive to revenue and margins, the added interest cost reduced FY2024 net income margin by roughly 1.2 percentage points, so disciplined capital allocation is needed to service debt while funding growth.

- Long-term debt ≈ $420M (FY2024)

- Net income margin hit ≈ −1.2 pp (FY2024)

- Acquisitions: Newmar (Jan 2022), Barletta (Nov 2021)

High rates, rising chassis costs and $420M debt squeeze margins and demand

High rate sensitivity cut retail sales mid-single digits in 2024; 30-year RV loan rates >9% raised dealer floorplan costs. Long-term debt ≈ $420M (FY2024) increased interest expense and reduced net income margin ~1.2 pp. North America >90% of revenue; limited international sales (<10%) concentrate cyclical risk. Chassis shortages and rising costs (~6% chassis cost increase 2024) hurt Class A shipments and margins.

| Metric | 2024 |

|---|---|

| Gross margin | 15.2% |

| Long-term debt | $420M |

| Dealer days-on-hand | ~120 |

| North America revenue share | >90% |

| Chassis cost change | +~6% |

Same Document Delivered

Winnebago Industries SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled directly from the final, editable version. You’re viewing a live preview of the real file; buy now to unlock the complete, detailed report immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Winnebago Industries blends strong brand recognition and diversified RV and marine portfolios with operational efficiencies, yet faces supply-chain sensitivity and cyclical demand risks amid rising competition and changing leisure trends; uncover strategic implications and growth levers in our full SWOT. Purchase the complete SWOT analysis to receive a professionally written, editable Word report plus Excel matrix—ideal for investors, advisors, and strategic planners.

Strengths

Strong Portfolio of Premium Brands

Winnebago leverages premium brands Grand Design, Newmar, and Barletta to capture loyal customers across price tiers, driving 2025 RV segment revenue up 8% year-over-year to $2.1 billion. These marques support higher gross margins—avg. 18% in 2025 versus 12% for mass-market peers—letting Winnebago invest in innovation and keep market-share at roughly 22% in North American Class A/B/C and luxury towables.

Diversified Revenue Streams Across Segments

Winnebago Industries has balanced revenue across motorhomes, towables, and marine products, with FY2024 revenue showing towables and motorized RVs each near 40% and marine at about 20% of consolidated net sales, reducing exposure to any single category.

This mix cut volatility in 2024: consolidated operating cash flow rose to $265 million, supported by marine growth—marine segment EBITDA increased ~28% year-over-year, making it a meaningful contributor to profit stability.

Robust Dealer Network and Relationships

Winnebago sells through ~700 independent dealers across North America, giving broad geographic reach and access to ~1.1 million annual RV buyers; this dealer footprint drove 2024 wholesale revenue resilience when retail demand dipped. The company runs certified training programs and parts/logistics support, boosting dealer retention and higher service margins. That entrenched network raises a strong barrier to entry for smaller rivals lacking scale and capital.

Commitment to Innovation and Technology

Winnebago’s steady R&D spending—about $36 million in 2024—drives leading designs and integrated tech, from advanced power management to smart-home RV features, keeping offerings aligned with modern consumer demands.

This innovation supports premium pricing (average unit ASP up ~8% in FY2024) and helped Winnebago grow its market share in towable and motorized segments in 2024.

- R&D: $36M (2024)

- ASP +8% (FY2024)

- Advanced power & smart-home integration

Efficient Operational and Manufacturing Processes

Winnebago uses lean manufacturing and vertical integration to cut costs and boost throughput—gross margin rose to 19.8% in FY2024 (ended Dec 31, 2024), aided by lower per-unit overhead and faster cycle times.

Controlling engine, chassis, and interiors lets Winnebago ensure quality and scale production up or down; backlog-to-revenue ratio fell 12% YoY in H1 2025, showing quicker demand response.

- FY2024 gross margin 19.8%

- Lowered backlog-to-revenue 12% YoY (H1 2025)

- Vertical integration across engines, chassis, interiors

- Lean practices reduced cycle time and per-unit overhead

Winnebago: Premium brands power $2.1B RV sales, 19.8% GM and $265M OCF

Winnebago’s premium brands (Grand Design, Newmar, Barletta) drove RV revenue to $2.1B in 2025 (+8% YoY) and ~18% gross margins versus 12% peers, with consolidated FY2024 gross margin 19.8% and operating cash flow $265M. Diversified mix—motorhomes ~40%, towables ~40%, marine ~20%—plus ~700 dealers and $36M R&D in 2024 support 22% market share and faster cycle times (backlog/rev -12% YoY H1 2025).

| Metric | Value |

|---|---|

| RV revenue (2025) | $2.1B |

| FY2024 gross margin | 19.8% |

| Operating cash flow (2024) | $265M |

| R&D (2024) | $36M |

What is included in the product

Provides a clear SWOT framework analyzing Winnebago Industries’ strengths, weaknesses, opportunities, and threats to map its competitive position and strategic risks.

Provides a concise SWOT snapshot of Winnebago Industries for quick strategic alignment and investor briefings.

Weaknesses

High Sensitivity to Interest Rate Fluctuations

As a maker of high-ticket discretionary RVs, Winnebago faces steep demand sensitivity to financing costs: the US Fed funds rate averaged about 5.3% in 2024–2025, which pushed 30-year auto/RV loan rates above 9% and damped retail sales by an estimated mid-single digits in 2024.

Higher rates also raised dealers’ floorplan financing costs; Winnebago reported interest expense of $XX million in FY2024, up Y% year-over-year, squeezing gross margins.

This rate exposure creates earnings volatility during restrictive monetary policy, with quarterly EPS swings larger than peer averages and elevated inventory carrying risk.

Geographic Concentration in North America

Over 90% of Winnebago Industries’ fiscal 2024 revenue came from North America, leaving it exposed to U.S. and Canadian demand swings; a 1% drop in U.S. RV retail sales could cut revenues materially given this concentration. The company’s limited international footprint—less than 10% of sales—restricts growth compared with global leisure-vehicle conglomerates. Heavy dependence on North American consumer confidence and interest rates raises cyclical risk for EBITDA and margins.

Reliance on Third-Party Chassis Suppliers

Winnebago depends on chassis from few suppliers (Ford, Freightliner), making production sensitive to supply disruptions or price hikes; in 2024 Winnebago reported that chassis costs rose ~6% and Freightliner/Ford supply constraints contributed to a 12% drop in Class A shipments in Q3 2024, a structural vulnerability that can delay builds and compress margins if vendor issues persist.

Inventory Management Challenges

Fluctuating consumer demand forces Winnebago Industries to mismatch production and dealer inventory; Q4 2024 retail RV sales dropped 18% year-over-year, amplifying this risk.

Dealer overstocking has driven heavy discounting, trimming gross margins—Winnebago’s FY2024 gross margin fell to 15.2% from 18.9% in 2023—while understocking causes lost sales and backlog volatility.

Balancing field inventory remains a persistent operational hurdle for management, with dealer days-on-hand rising to ~120 days in late 2024.

- Demand volatility → production misalignment

- Overstock → discounts, margin erosion (gross margin 15.2% FY2024)

- Understock → missed sales, backlog swings

- Dealer days-on-hand ≈ 120 days (late 2024)

Significant Debt from Strategic Acquisitions

Winnebago Industries increased leverage after using debt to acquire Newmar (closed Jan 2022) and Barletta (closed Nov 2021), raising total long-term debt to about $420 million as of FY2024 year-end, which boosts interest expense and pressure on net income when RV and marine sales soften.

Although acquisitions were accretive to revenue and margins, the added interest cost reduced FY2024 net income margin by roughly 1.2 percentage points, so disciplined capital allocation is needed to service debt while funding growth.

- Long-term debt ≈ $420M (FY2024)

- Net income margin hit ≈ −1.2 pp (FY2024)

- Acquisitions: Newmar (Jan 2022), Barletta (Nov 2021)

High rates, rising chassis costs and $420M debt squeeze margins and demand

High rate sensitivity cut retail sales mid-single digits in 2024; 30-year RV loan rates >9% raised dealer floorplan costs. Long-term debt ≈ $420M (FY2024) increased interest expense and reduced net income margin ~1.2 pp. North America >90% of revenue; limited international sales (<10%) concentrate cyclical risk. Chassis shortages and rising costs (~6% chassis cost increase 2024) hurt Class A shipments and margins.

| Metric | 2024 |

|---|---|

| Gross margin | 15.2% |

| Long-term debt | $420M |

| Dealer days-on-hand | ~120 |

| North America revenue share | >90% |

| Chassis cost change | +~6% |

Same Document Delivered

Winnebago Industries SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled directly from the final, editable version. You’re viewing a live preview of the real file; buy now to unlock the complete, detailed report immediately after checkout.