Wintrust Financial Business Model Canvas

Wintrust Financial: Concise Business Model Canvas for Investors & Strategists

Unlock Wintrust Financial’s strategic playbook with our concise Business Model Canvas—revealing how the bank creates customer value, leverages partnerships, and monetizes core services to sustain growth; perfect for investors, advisors, and strategists seeking actionable insights and a ready-to-use template to benchmark or adapt.

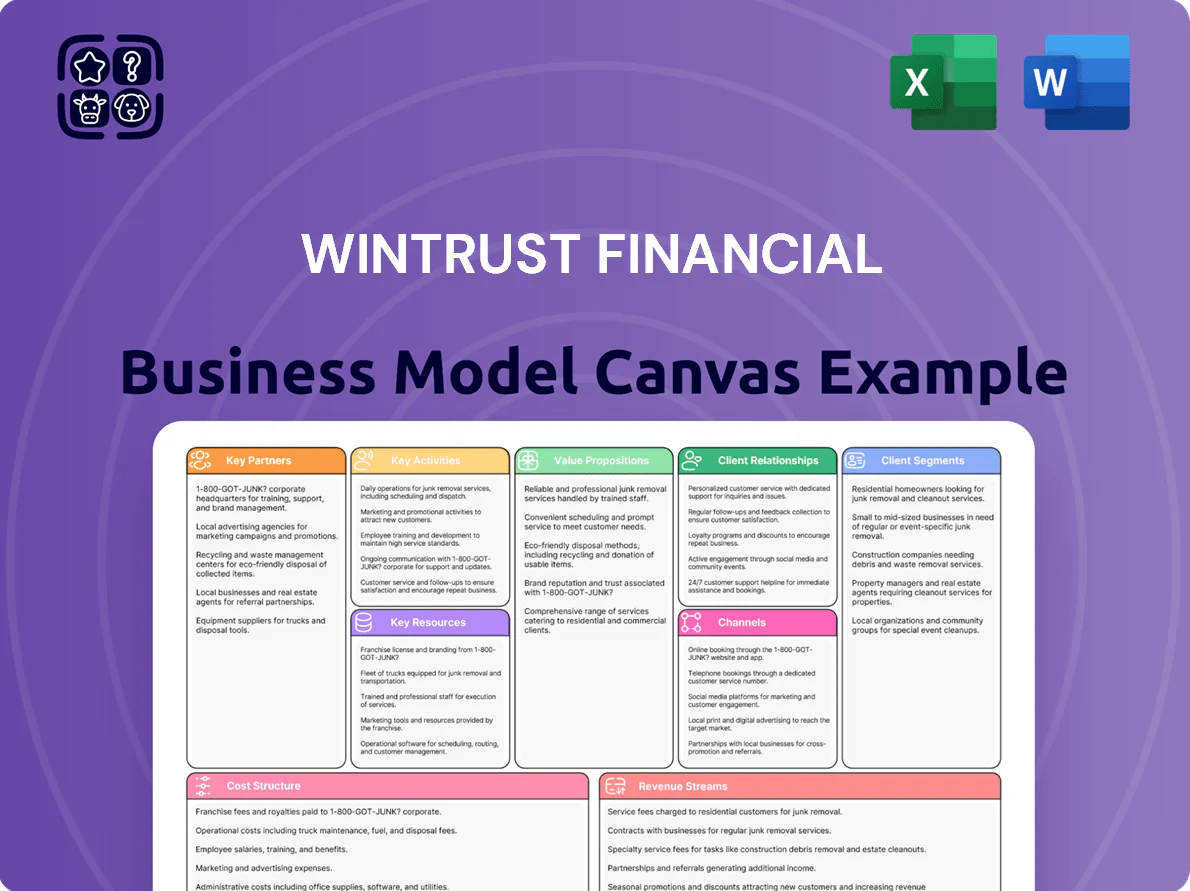

Partnerships

Strategic Fintech Collaborations

Wintrust partners with fintechs to boost digital banking and automate back-office functions, cutting time-to-market and capex; by Q4 2025 these alliances support ~42% of digital deposits and reduced processing costs by an estimated 12% year-over-year.

Insurance Premium Finance Networks

Wintrust’s FIRST Insurance Funding partners with 12,000+ insurance agents and brokers nationwide, who supply the bulk of commercial premium financing referrals; this channel supported roughly $3.2 billion in funded premiums in 2024, about 65% of FIRST’s originations.

Community and Civic Organizations

Wintrust partners with 200+ local non-profits, dozens of civic groups, and teams across Chicago and Southern Wisconsin, funding $35M in community programs and sponsoring events that drove ~12% of new retail account openings in 2024; these ties boost the Have It All proposition by pairing local trust with Wintrust’s $60B+ assets (2024) and broader product set.

Mortgage Secondary Market Investors

Wintrust sells mortgages to Fannie Mae, Freddie Mac, and private investors, retaining origination fees while reducing long-term interest-rate and liquidity exposure; in 2024 secondary market sales funded roughly 35% of originated mortgage volume, supporting capital ratios and NIM stability.

- Partners: Fannie Mae, Freddie Mac, private institutions

- Benefit: offloads long-term debt, preserves liquidity

- 2024 stat: ~35% of originations sold

- Result: steady origination fee income, lower interest-rate risk

Wealth Management Platform Providers

The wealth management division relies on custodians and platform providers (eg, Pershing, Fidelity Clearing & Custody Services) to execute trades and manage $~18.5bn in client assets under custody at Wintrust Wealth Management as of YE 2025, enabling access to mutual funds, ETFs, and alternatives.

These integrations power advisory services for high-net-worth clients, supporting multi-asset portfolios, SMA access, and operational reporting required for fiduciary compliance.

- Custodians: Pershing, Fidelity

- Assets under custody: ~$18.5bn (YE 2025)

- Products: mutual funds, ETFs, alternatives, SMAs

- Benefits: trade execution, reporting, compliance

Wintrust partners fuel digital growth: $3.2B FIRST, $35M community, $18.5B AUC

Wintrust’s key partners—fintechs, 12,000+ FIRST agents, 200+ community orgs, Fannie Mae/Freddie/private investors, Pershing/Fidelity—drive digital deposits (~42% by Q4 2025), $3.2B FIRST funded premiums (2024), $35M community funding (2024), ~35% mortgage sales (2024), and ~$18.5B AUC (YE 2025).

| Partner | Metric | Value |

|---|---|---|

| Fintechs | Digital deposits | ~42% (Q4 2025) |

| FIRST agents | Funded premiums | $3.2B (2024) |

| Community orgs | Community funding | $35M (2024) |

| Secondary market | Mortgages sold | ~35% (2024) |

| Custodians | Assets under custody | $18.5B (YE 2025) |

What is included in the product

A concise Business Model Canvas for Wintrust Financial detailing its nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with the bank’s community-focused commercial banking, wealth management, and specialty finance strategies.

Condenses Wintrust Financial’s community banking strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and boardroom-ready insight for decision-making.

Activities

Commercial and Industrial Lending

Wintrust underwrites and manages commercial and industrial loans to small‑ and mid‑sized firms across its Chicagoland and regional footprint, holding about $16.5 billion in commercial loans on December 31, 2024; local decision‑making and relationship lending give faster approvals versus centralized banks. Rigorous credit underwriting, covenant monitoring, and quarterly portfolio stress tests aim to keep nonperforming loans low—NPLs were 0.42% at year‑end 2024.

Deposit Gathering and Management

Wintrust actively manages a diverse base of core deposits from retail and commercial clients to fund lending, offering competitive checking, savings, and sweep accounts and maintaining 350+ branches and modern digital banking to boost long-term balances; as of 2024 year-end, deposits were $50.2 billion, supporting a net interest margin near 3.40% and keeping cost of funds below peers to preserve liquidity and lend efficiently.

Specialized Insurance Premium Financing

Wintrust operates a specialized premium financing arm that funds commercial insurance premiums nationwide, managing a distinct credit cycle and processing high volumes—roughly $1.2 billion in financed premiums and ~35,000 policies in 2024—contributing materially to non-traditional lending revenue (about 8% of 2024 loan income) and enhancing geographic diversification across all 50 states.

Mortgage Origination and Servicing

Wintrust handles the full residential mortgage lifecycle—application, underwriting, closing, servicing, and secondary-market sales—anchored by a strong community brand that drove $7.8 billion in mortgage originations in 2024, per company filings.

Mortgage volume is rate-sensitive; net interest margin and origination revenue fell in 2023–2024 as rates rose, so Wintrust scales operations up or down quickly to manage credit and servicing costs.

- Full lifecycle: origination to secondary sales

- $7.8B originations in 2024

- Community brand boosts purchase/refi share

- High sensitivity to interest rates

- Needs agile operational scaling

Wealth Management and Trust Services

Wintrust: $16.5B loans, $50.2B deposits, ~3.4% NIM, $7.8B mortgages, $430M wealth fees

Wintrust underwrites $16.5B commercial loans (12/31/2024), manages $50.2B deposits (2024) with NIM ~3.40%, originates $7.8B mortgages (2024), finances ~$1.2B insurance premiums (2024), and earned ~$430M wealth fees (2025).

| Metric | 2024/2025 |

|---|---|

| Commercial loans | $16.5B (12/31/2024) |

| Deposits | $50.2B (2024) |

| NPLs | 0.42% (2024) |

| NIM | ~3.40% (2024) |

| Mortgage originations | $7.8B (2024) |

| Premium financing | $1.2B (2024) |

| Wealth fees | $430M (2025) |

Full Document Unlocks After Purchase

Business Model Canvas

The preview you’re viewing is the actual Wintrust Financial Business Model Canvas, not a mockup—it's a direct excerpt from the final file you’ll receive after purchase.

When you complete your order, you’ll instantly get this same professional document in full, ready-to-edit Word and Excel formats with all sections and content included.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Wintrust Financial: Concise Business Model Canvas for Investors & Strategists

Unlock Wintrust Financial’s strategic playbook with our concise Business Model Canvas—revealing how the bank creates customer value, leverages partnerships, and monetizes core services to sustain growth; perfect for investors, advisors, and strategists seeking actionable insights and a ready-to-use template to benchmark or adapt.

Partnerships

Strategic Fintech Collaborations

Wintrust partners with fintechs to boost digital banking and automate back-office functions, cutting time-to-market and capex; by Q4 2025 these alliances support ~42% of digital deposits and reduced processing costs by an estimated 12% year-over-year.

Insurance Premium Finance Networks

Wintrust’s FIRST Insurance Funding partners with 12,000+ insurance agents and brokers nationwide, who supply the bulk of commercial premium financing referrals; this channel supported roughly $3.2 billion in funded premiums in 2024, about 65% of FIRST’s originations.

Community and Civic Organizations

Wintrust partners with 200+ local non-profits, dozens of civic groups, and teams across Chicago and Southern Wisconsin, funding $35M in community programs and sponsoring events that drove ~12% of new retail account openings in 2024; these ties boost the Have It All proposition by pairing local trust with Wintrust’s $60B+ assets (2024) and broader product set.

Mortgage Secondary Market Investors

Wintrust sells mortgages to Fannie Mae, Freddie Mac, and private investors, retaining origination fees while reducing long-term interest-rate and liquidity exposure; in 2024 secondary market sales funded roughly 35% of originated mortgage volume, supporting capital ratios and NIM stability.

- Partners: Fannie Mae, Freddie Mac, private institutions

- Benefit: offloads long-term debt, preserves liquidity

- 2024 stat: ~35% of originations sold

- Result: steady origination fee income, lower interest-rate risk

Wealth Management Platform Providers

The wealth management division relies on custodians and platform providers (eg, Pershing, Fidelity Clearing & Custody Services) to execute trades and manage $~18.5bn in client assets under custody at Wintrust Wealth Management as of YE 2025, enabling access to mutual funds, ETFs, and alternatives.

These integrations power advisory services for high-net-worth clients, supporting multi-asset portfolios, SMA access, and operational reporting required for fiduciary compliance.

- Custodians: Pershing, Fidelity

- Assets under custody: ~$18.5bn (YE 2025)

- Products: mutual funds, ETFs, alternatives, SMAs

- Benefits: trade execution, reporting, compliance

Wintrust partners fuel digital growth: $3.2B FIRST, $35M community, $18.5B AUC

Wintrust’s key partners—fintechs, 12,000+ FIRST agents, 200+ community orgs, Fannie Mae/Freddie/private investors, Pershing/Fidelity—drive digital deposits (~42% by Q4 2025), $3.2B FIRST funded premiums (2024), $35M community funding (2024), ~35% mortgage sales (2024), and ~$18.5B AUC (YE 2025).

| Partner | Metric | Value |

|---|---|---|

| Fintechs | Digital deposits | ~42% (Q4 2025) |

| FIRST agents | Funded premiums | $3.2B (2024) |

| Community orgs | Community funding | $35M (2024) |

| Secondary market | Mortgages sold | ~35% (2024) |

| Custodians | Assets under custody | $18.5B (YE 2025) |

What is included in the product

A concise Business Model Canvas for Wintrust Financial detailing its nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with the bank’s community-focused commercial banking, wealth management, and specialty finance strategies.

Condenses Wintrust Financial’s community banking strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and boardroom-ready insight for decision-making.

Activities

Commercial and Industrial Lending

Wintrust underwrites and manages commercial and industrial loans to small‑ and mid‑sized firms across its Chicagoland and regional footprint, holding about $16.5 billion in commercial loans on December 31, 2024; local decision‑making and relationship lending give faster approvals versus centralized banks. Rigorous credit underwriting, covenant monitoring, and quarterly portfolio stress tests aim to keep nonperforming loans low—NPLs were 0.42% at year‑end 2024.

Deposit Gathering and Management

Wintrust actively manages a diverse base of core deposits from retail and commercial clients to fund lending, offering competitive checking, savings, and sweep accounts and maintaining 350+ branches and modern digital banking to boost long-term balances; as of 2024 year-end, deposits were $50.2 billion, supporting a net interest margin near 3.40% and keeping cost of funds below peers to preserve liquidity and lend efficiently.

Specialized Insurance Premium Financing

Wintrust operates a specialized premium financing arm that funds commercial insurance premiums nationwide, managing a distinct credit cycle and processing high volumes—roughly $1.2 billion in financed premiums and ~35,000 policies in 2024—contributing materially to non-traditional lending revenue (about 8% of 2024 loan income) and enhancing geographic diversification across all 50 states.

Mortgage Origination and Servicing

Wintrust handles the full residential mortgage lifecycle—application, underwriting, closing, servicing, and secondary-market sales—anchored by a strong community brand that drove $7.8 billion in mortgage originations in 2024, per company filings.

Mortgage volume is rate-sensitive; net interest margin and origination revenue fell in 2023–2024 as rates rose, so Wintrust scales operations up or down quickly to manage credit and servicing costs.

- Full lifecycle: origination to secondary sales

- $7.8B originations in 2024

- Community brand boosts purchase/refi share

- High sensitivity to interest rates

- Needs agile operational scaling

Wealth Management and Trust Services

Wintrust: $16.5B loans, $50.2B deposits, ~3.4% NIM, $7.8B mortgages, $430M wealth fees

Wintrust underwrites $16.5B commercial loans (12/31/2024), manages $50.2B deposits (2024) with NIM ~3.40%, originates $7.8B mortgages (2024), finances ~$1.2B insurance premiums (2024), and earned ~$430M wealth fees (2025).

| Metric | 2024/2025 |

|---|---|

| Commercial loans | $16.5B (12/31/2024) |

| Deposits | $50.2B (2024) |

| NPLs | 0.42% (2024) |

| NIM | ~3.40% (2024) |

| Mortgage originations | $7.8B (2024) |

| Premium financing | $1.2B (2024) |

| Wealth fees | $430M (2025) |

Full Document Unlocks After Purchase

Business Model Canvas

The preview you’re viewing is the actual Wintrust Financial Business Model Canvas, not a mockup—it's a direct excerpt from the final file you’ll receive after purchase.

When you complete your order, you’ll instantly get this same professional document in full, ready-to-edit Word and Excel formats with all sections and content included.