Wintrust Financial Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

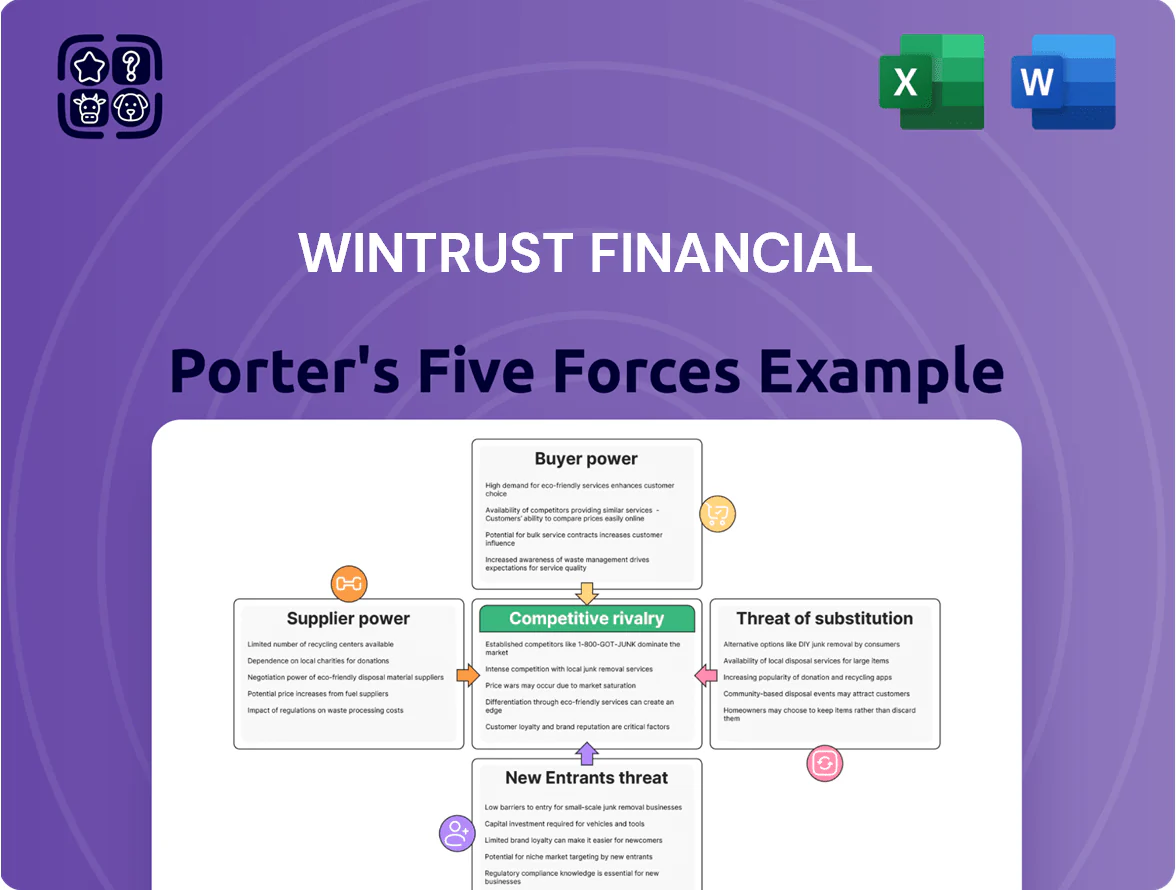

Wintrust Financial operates in a bancassurance-rich regional market where customer loyalty and regulatory scrutiny temper rivalry, while digital entrants and low-cost providers raise the threat of new competition—this snapshot highlights key pressures but omits force-by-force ratings and actionable takeaways.

Suppliers Bargaining Power

Cost and Availability of Core Deposits

Depositors are Wintrust Financials main capital suppliers; by end-2025, with the fed funds rate near 5.25% and retail savings yields averaging 3.5%–4.0%, customers pushed for higher returns, forcing Wintrust to raise deposit costs and compress net interest margin (NIM fell to about 2.65% in 2025).

Maintaining core deposit growth required offering competitive rates—Wintrust reported 12% year-over-year core deposit growth in 2025 but paid higher funding costs.

The Chicago community franchise limits switch risk versus digital-only banks, boosting deposit stickiness and reducing supplier power somewhat.

Reliance on Specialized Financial Technology Vendors

Wintrust relies on third-party vendors for core banking, cybersecurity, and digital platforms; in 2025 about 40% of IT spend goes to external software and services, making these suppliers critical to uptime and compliance.

Switching vendors carries high costs and operational risk—typical core migrations exceed $50M and 12–24 months—so suppliers hold leverage and Wintrust often acts as a price-taker for top-tier updates.

Competition for Skilled Banking Talent

The supply of experienced commercial lenders and wealth managers in the Midwest is a key input for Wintrust's relationship-based model, and Chicago's tight labor market (unemployment 3.6% in 2024) gives top talent bargaining power over pay and benefits. Wintrust faces competition from national banks and boutiques offering 10–25% higher total compensation for senior lenders; attrition rose 12% in 2023 in the regional banking sector. To retain staff, Wintrust must invest in culture, variable incentives, and career paths, budgeting roughly $20–30k per senior hire annually for retention packages.

Access to Wholesale Funding Markets

When Wintrust's deposits lag loan demand, it taps wholesale funding from capital markets and institutional lenders; at year-end 2025 its access and pricing hinge on Wintrust’s credit rating (BBB+ as of Nov 2025) and overall market stability.

Rising federal funds rate (4.25%–5.25% in 2025) and market volatility pushed wholesale costs higher, increasing borrowing spreads by ~75–150 bps vs. pre-2022 levels and tightening liquidity.

- Wholesale reliance grows when loan-to-deposit >100%

- Credit rating BBB+ sets funding spreads

- Fed funds 4.25%–5.25% raised costs

- Spreads widened ~75–150 bps in 2025

Regulatory and Compliance Service Providers

Legal and audit firms that keep Wintrust Financial compliant are specialized suppliers with high bargaining power, since their expertise is essential to maintain the bank charter amid rising regulatory complexity through 2025.

With fewer than a dozen global and regional top-tier firms able to handle complex regional banking audits, these providers command premium fees — audit and compliance retainers for midsize banks often rose 8–12% in 2024.

- Essential supplier: legal/audit firms

- High bargaining power due to scarce expertise

- Charter risk if services lapse

- Fees up ~8–12% in 2024 for midsize banks

Supplier power squeezes margins: NIM ~2.65%, core costs and spreads rise

Suppliers (depositors, vendors, talent, auditors, and wholesale lenders) exert moderate-to-high power: depositor-driven funding costs compressed NIM to ~2.65% in 2025, core deposits grew 12% y/y but at higher rates; third-party IT spend ≈40% of tech budget with core migrations >$50M; senior lender pay gaps 10–25% raise attrition; wholesale spreads widened ~75–150 bps with BBB+ rating.

| Item | 2025 / 2024 |

|---|---|

| NIM | ~2.65% (2025) |

| Core deposit growth | 12% y/y (2025) |

| IT external spend | ~40% (2025) |

| Core migration cost | >$50M, 12–24 months |

| Wholesale spread change | +75–150 bps vs pre-2022 |

| Attrition (regional banks) | +12% (2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Wintrust Financial that uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging disruptors to assess pricing power and profitability.

A concise Porter's Five Forces sheet for Wintrust—fast insight into competitive pressures to streamline strategic decisions.

Customers Bargaining Power

Low Switching Costs for Retail Consumers

In 2025, streamlined digital onboarding and instant ACH transfers mean retail customers can switch banks in days, boosting their bargaining power; industry data shows 38% of US consumers switched primary banks or considered switching in the past 12 months. This mobility pressures Wintrust Financial to match market-leading deposit rates and cut fees, while protecting share through its local-branch network and personalized service that drove a 4.2% YoY household growth in 2024.

Negotiation Leverage of Commercial Clients

Wintrust’s focus on commercial and industrial lending gives large borrowers strong leverage; corporate clients routinely solicit bids from regional and national banks to press for lower spreads and looser covenants. In 2024 commercial loans were about 58% of Wintrust’s $28.9B loan portfolio, so losing a single large relationship can cut net interest income materially. Sophisticated borrowers also demand tailored credit facilities and pricing transparency, raising retention costs.

Price Sensitivity in a High Transparency Market

By late 2025, digital rate-comparison tools let retail and business customers view real-time rates across banks, cutting information asymmetry and raising price sensitivity; industry surveys show 68% of consumers compare rates online before switching, so Wintrust must keep pricing tight to avoid attrition. Customers now routinely demand rate matches or fee waivers—banks report a 12% increase in negotiated fee concessions in 2024—making pricing a key competitive lever for Wintrust.

Demand for Integrated Wealth Management Services

Influence of Small Business Advocacy and Options

Small businesses in Chicago and Wisconsin can choose among banks, credit unions, and fintechs—Chicago has over 1,500 small-business lenders and Illinois small-business loan originations totaled about $8.1B in 2024—so buyers can press for lower rates or flexible terms.

Wintrust leverages its community-bank brand and 2024 retail deposit base of $28.4B to build emotional loyalty, reducing pure price sensitivity and lowering churn versus pure-play lenders.

- Multiple lenders: >1,500 local/regional options

- Illinois SMB loans 2024: ~$8.1B

- Wintrust deposits 2024: $28.4B

- Community brand cuts price-only bargaining

Rising Customer Power: 38% Ready to Switch as 68% Rate-Shop; Wintrust $28B+ Loans/Deposits

Customers wield rising bargaining power: 38% considered switching in 2025, digital rate tools raised price sensitivity (68% compare rates), Wintrust held $28.4B deposits and $28.9B loans (2024), commercial loans ~58% of portfolio, HNW investable wealth $37.7T (2024) pressuring bundled-fee discounts (15–25%).

| Metric | Value |

|---|---|

| Switching consideration (2025) | 38% |

| Compare rates online | 68% |

| Wintrust deposits (2024) | $28.4B |

| Loans (2024) | $28.9B |

| Commercial share | 58% |

| US HNW wealth (2024) | $37.7T |

What You See Is What You Get

Wintrust Financial Porter's Five Forces Analysis

This preview shows the exact Wintrust Financial Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, complete, and ready for immediate download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Wintrust Financial operates in a bancassurance-rich regional market where customer loyalty and regulatory scrutiny temper rivalry, while digital entrants and low-cost providers raise the threat of new competition—this snapshot highlights key pressures but omits force-by-force ratings and actionable takeaways.

Suppliers Bargaining Power

Cost and Availability of Core Deposits

Depositors are Wintrust Financials main capital suppliers; by end-2025, with the fed funds rate near 5.25% and retail savings yields averaging 3.5%–4.0%, customers pushed for higher returns, forcing Wintrust to raise deposit costs and compress net interest margin (NIM fell to about 2.65% in 2025).

Maintaining core deposit growth required offering competitive rates—Wintrust reported 12% year-over-year core deposit growth in 2025 but paid higher funding costs.

The Chicago community franchise limits switch risk versus digital-only banks, boosting deposit stickiness and reducing supplier power somewhat.

Reliance on Specialized Financial Technology Vendors

Wintrust relies on third-party vendors for core banking, cybersecurity, and digital platforms; in 2025 about 40% of IT spend goes to external software and services, making these suppliers critical to uptime and compliance.

Switching vendors carries high costs and operational risk—typical core migrations exceed $50M and 12–24 months—so suppliers hold leverage and Wintrust often acts as a price-taker for top-tier updates.

Competition for Skilled Banking Talent

The supply of experienced commercial lenders and wealth managers in the Midwest is a key input for Wintrust's relationship-based model, and Chicago's tight labor market (unemployment 3.6% in 2024) gives top talent bargaining power over pay and benefits. Wintrust faces competition from national banks and boutiques offering 10–25% higher total compensation for senior lenders; attrition rose 12% in 2023 in the regional banking sector. To retain staff, Wintrust must invest in culture, variable incentives, and career paths, budgeting roughly $20–30k per senior hire annually for retention packages.

Access to Wholesale Funding Markets

When Wintrust's deposits lag loan demand, it taps wholesale funding from capital markets and institutional lenders; at year-end 2025 its access and pricing hinge on Wintrust’s credit rating (BBB+ as of Nov 2025) and overall market stability.

Rising federal funds rate (4.25%–5.25% in 2025) and market volatility pushed wholesale costs higher, increasing borrowing spreads by ~75–150 bps vs. pre-2022 levels and tightening liquidity.

- Wholesale reliance grows when loan-to-deposit >100%

- Credit rating BBB+ sets funding spreads

- Fed funds 4.25%–5.25% raised costs

- Spreads widened ~75–150 bps in 2025

Regulatory and Compliance Service Providers

Legal and audit firms that keep Wintrust Financial compliant are specialized suppliers with high bargaining power, since their expertise is essential to maintain the bank charter amid rising regulatory complexity through 2025.

With fewer than a dozen global and regional top-tier firms able to handle complex regional banking audits, these providers command premium fees — audit and compliance retainers for midsize banks often rose 8–12% in 2024.

- Essential supplier: legal/audit firms

- High bargaining power due to scarce expertise

- Charter risk if services lapse

- Fees up ~8–12% in 2024 for midsize banks

Supplier power squeezes margins: NIM ~2.65%, core costs and spreads rise

Suppliers (depositors, vendors, talent, auditors, and wholesale lenders) exert moderate-to-high power: depositor-driven funding costs compressed NIM to ~2.65% in 2025, core deposits grew 12% y/y but at higher rates; third-party IT spend ≈40% of tech budget with core migrations >$50M; senior lender pay gaps 10–25% raise attrition; wholesale spreads widened ~75–150 bps with BBB+ rating.

| Item | 2025 / 2024 |

|---|---|

| NIM | ~2.65% (2025) |

| Core deposit growth | 12% y/y (2025) |

| IT external spend | ~40% (2025) |

| Core migration cost | >$50M, 12–24 months |

| Wholesale spread change | +75–150 bps vs pre-2022 |

| Attrition (regional banks) | +12% (2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Wintrust Financial that uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging disruptors to assess pricing power and profitability.

A concise Porter's Five Forces sheet for Wintrust—fast insight into competitive pressures to streamline strategic decisions.

Customers Bargaining Power

Low Switching Costs for Retail Consumers

In 2025, streamlined digital onboarding and instant ACH transfers mean retail customers can switch banks in days, boosting their bargaining power; industry data shows 38% of US consumers switched primary banks or considered switching in the past 12 months. This mobility pressures Wintrust Financial to match market-leading deposit rates and cut fees, while protecting share through its local-branch network and personalized service that drove a 4.2% YoY household growth in 2024.

Negotiation Leverage of Commercial Clients

Wintrust’s focus on commercial and industrial lending gives large borrowers strong leverage; corporate clients routinely solicit bids from regional and national banks to press for lower spreads and looser covenants. In 2024 commercial loans were about 58% of Wintrust’s $28.9B loan portfolio, so losing a single large relationship can cut net interest income materially. Sophisticated borrowers also demand tailored credit facilities and pricing transparency, raising retention costs.

Price Sensitivity in a High Transparency Market

By late 2025, digital rate-comparison tools let retail and business customers view real-time rates across banks, cutting information asymmetry and raising price sensitivity; industry surveys show 68% of consumers compare rates online before switching, so Wintrust must keep pricing tight to avoid attrition. Customers now routinely demand rate matches or fee waivers—banks report a 12% increase in negotiated fee concessions in 2024—making pricing a key competitive lever for Wintrust.

Demand for Integrated Wealth Management Services

Influence of Small Business Advocacy and Options

Small businesses in Chicago and Wisconsin can choose among banks, credit unions, and fintechs—Chicago has over 1,500 small-business lenders and Illinois small-business loan originations totaled about $8.1B in 2024—so buyers can press for lower rates or flexible terms.

Wintrust leverages its community-bank brand and 2024 retail deposit base of $28.4B to build emotional loyalty, reducing pure price sensitivity and lowering churn versus pure-play lenders.

- Multiple lenders: >1,500 local/regional options

- Illinois SMB loans 2024: ~$8.1B

- Wintrust deposits 2024: $28.4B

- Community brand cuts price-only bargaining

Rising Customer Power: 38% Ready to Switch as 68% Rate-Shop; Wintrust $28B+ Loans/Deposits

Customers wield rising bargaining power: 38% considered switching in 2025, digital rate tools raised price sensitivity (68% compare rates), Wintrust held $28.4B deposits and $28.9B loans (2024), commercial loans ~58% of portfolio, HNW investable wealth $37.7T (2024) pressuring bundled-fee discounts (15–25%).

| Metric | Value |

|---|---|

| Switching consideration (2025) | 38% |

| Compare rates online | 68% |

| Wintrust deposits (2024) | $28.4B |

| Loans (2024) | $28.9B |

| Commercial share | 58% |

| US HNW wealth (2024) | $37.7T |

What You See Is What You Get

Wintrust Financial Porter's Five Forces Analysis

This preview shows the exact Wintrust Financial Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, complete, and ready for immediate download with no placeholders or samples.