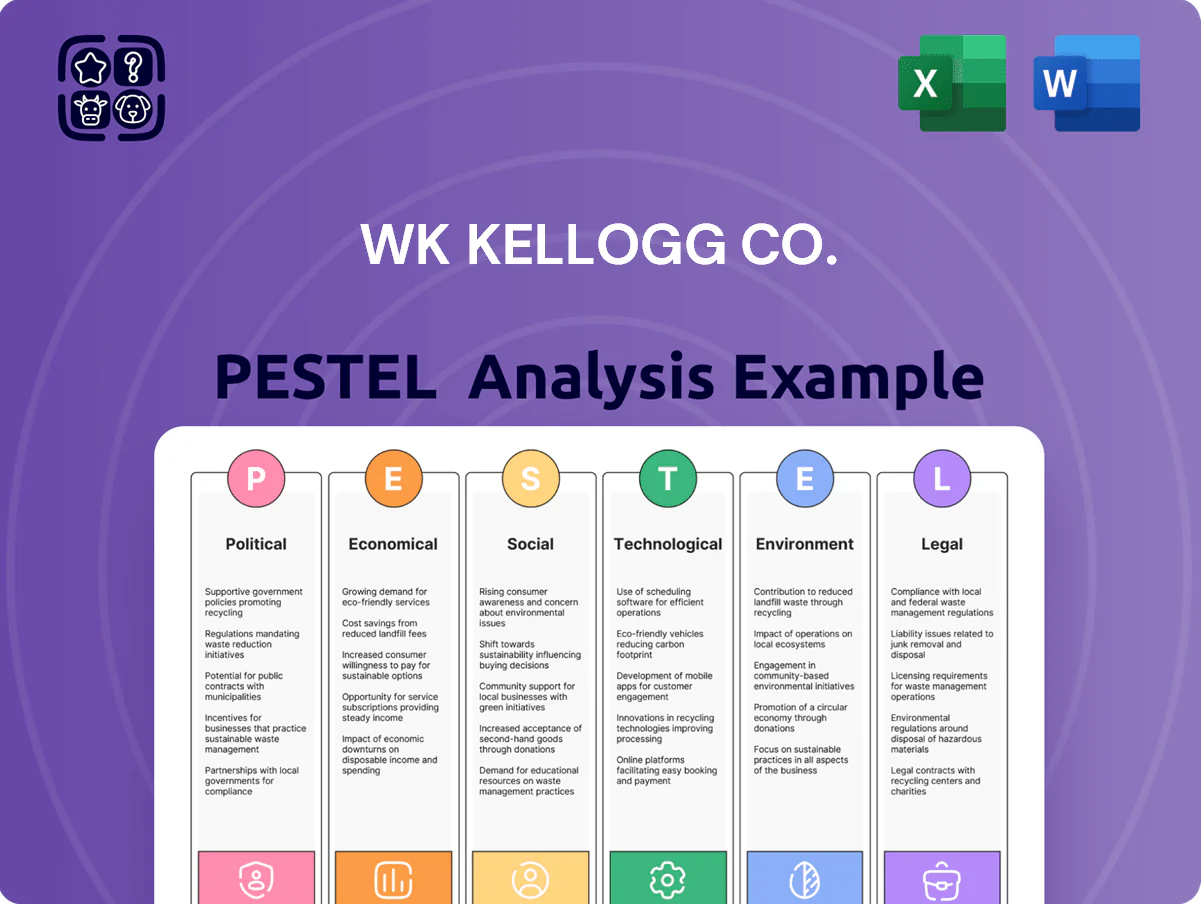

WK Kellogg Co. PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis for WK Kellogg Co. highlights how regulatory shifts, changing consumer health preferences, supply-chain cost pressures, technological innovation in food processing, and sustainability mandates will shape the company’s near-term risks and growth opportunities—buy the full report to access actionable insights and editable charts for strategy or investment decisions.

Political factors

USMCA Trade Policy Stability

The company’s exclusive North American footprint ties supply-chain resilience to USMCA stability; USMCA accounted for roughly 75% of Kellogg’s 2024 regional revenue exposure, so tariff shifts could materially affect costs.

Imposition of cross-border duties or stricter rules of origin would raise input costs for grain and packaging, impacting gross margins—Kellogg reported a 2024 gross margin of about 33.4%, sensitive to commodity cost changes.

Management must track political shifts and potential renegotiations through 2026, including US–Mexico bilateral tensions and Canadian policy moves, as even modest tariff adjustments (1–3%) could trim EPS given Kellogg’s 2024 adjusted EPS of $2.79.

Federal Agricultural Subsidy Shifts

Federal support for corn and wheat—corn subsidies totaled about $12.3bn in 2024—directly affects input costs for Kellogg’s cereal lines, where grain can be 20–30% of COGS. Ongoing Farm Bill debates in 2024–25 created price volatility, with corn futures up ~18% YoY in 2024. A cut in subsidies would likely force Kellogg to raise retail prices or compress margins; a 10% raw grain cost rise could cut operating margin by ~1–1.5 percentage points.

Public Health Policy Initiatives

Government efforts to cut obesity and sugar intake—CDC reports adult obesity at 41.9% in 2019–2020 and WHO pushing sugar reduction—heighten regulatory risk for WK Kellogg Co; proposed federal sugar taxes or 2025 dietary guideline shifts could force reformulation across its $14.4B 2024 revenue cereal portfolio, raising R&D and CAPEX; active lobbying and policy engagement will be vital to shape legislation affecting ready-to-eat cereals.

School Nutrition Program Standards

Political changes to federal school breakfast nutrition standards directly affect WK Kellogg Co.’s institutional sales, which represented about 6% of North American cereal revenue in 2024 (approx. $120–150 million estimated).

Amendments to the Healthy, Hunger-Free Kids Act or new USDA mandates can render existing products ineligible for school programs, risking contract losses and inventory write-downs.

Ongoing compliance efforts and reformulation costs are necessary to retain long-term government contracts and safeguard recurring institutional revenue.

- Institutional sales ~6% of NA cereal revenue in 2024 (~$120–150M)

- Policy shifts can disqualify brands from schools

- Reformulation/compliance required to secure government contracts

Geopolitical Supply Chain Security

While WK Kellogg Co. targets North America, political instability in supplier regions for specialty ingredients (e.g., cocoa, palm oil) risks input shortages; in 2024 global cocoa supply shocks lifted prices ~18% YoY, pressuring margins.

Diplomatic tensions and sanctions can raise energy and additive costs—oil price volatility (2024 average Brent ~USD 86/bbl) increases manufacturing expense for large plants.

Energy-region unrest raises logistics and production costs; Kellogg’s 2024 freight and energy-related SG&A pressure contributed to a ~1–2% hit to operating margin.

- Exposure to specialty-ingredient supply risks (cocoa, palm oil)

- 2024 Brent ~USD 86/bbl; cocoa +18% YoY

- Energy/logistics volatility can reduce operating margin by ~1–2%

Kellogg margins at risk: USMCA exposure, commodity shocks & policy threats compress 2024

Political risks—USMCA exposure (~75% of 2024 NA revenue), tariff/ROO changes, Farm Bill subsidy shifts (corn subsidies ≈$12.3bn in 2024; corn futures +18% YoY), sugar/obesity policy threats to cereal reformulation, school nutrition rule changes impacting ~6% of NA cereal revenue (~$120–150M), and commodity/energy price shocks (cocoa +18% YoY; Brent ≈$86/bbl)—can compress Kellogg’s 2024 margins (gross 33.4%; adj. EPS $2.79).

| Metric | 2024 |

|---|---|

| USMCA revenue share | ~75% |

| Gross margin | 33.4% |

| Adj. EPS | $2.79 |

| Corn subsidies | $12.3bn |

| Corn futures YoY | +18% |

| Cocoa YoY | +18% |

| Brent avg | $86/bbl |

| School sales | ~$120–150M (6% NA cereal) |

What is included in the product

Explores how external macro-environmental factors uniquely affect WK Kellogg Co. across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, forward-looking insights, and actionable implications to inform strategy, risk mitigation, and investor communications.

A concise, visually segmented PESTLE snapshot of WK Kellogg Co. that’s easily inserted into presentations or shared across teams to streamline discussions on regulatory, economic, social, technological, environmental, and political risks and opportunities.

Economic factors

Commodity Price Volatility

Prices for sugar, corn and wheat—inputs accounting for a material share of WK Kellogg Co.’s COGS—are volatile: CBOT corn rose ~22% in 2023 while global sugar jumped ~18%, and such swings feed directly into margin pressure if costs cannot be passed to consumers.

Kellogg reported raw material inflation contributed to a 2023 gross margin decline versus 2022, and persistent agricultural inflation or supply shocks would further compress margins.

The company employs hedging and long-term supply contracts to manage exposure, but sustained elevated commodity prices remain a significant financial risk to profitability.

Consumer Purchasing Power

As a consumer staples firm, WK Kellogg Co. is exposed to shifts in disposable income; US real disposable personal income fell 0.3% in 2024 Q3 year-on-year, increasing pressure on premium lines like Bear Naked.

In downturns shoppers often trade down to private labels, which now hold about 17% of US cereal and snack categories (2024 IRI data), risking market share loss.

Maintaining brand equity and clear value propositions, plus targeted price promotions, is critical to retain customers when budgets tighten.

Interest Rate and Debt Management

Following the 2023 spin-off, WK Kellogg Co.’s capital structure and funding for its Supply Chain Reinvention are sensitive to prevailing interest rates; with US 10-year Treasury yields averaging ~4.2% in 2024 and the Fed funds rate at 5.25–5.50% by late 2024, borrowing costs rose, increasing debt servicing expense and constraining capital for facility upgrades.

Labor Market Inflation

- Average hourly earnings +4.2% YoY (2025)

- 14 states with min wage ≥15 USD (2025)

- Kellogg capex +8% in 2024 to support automation

North American Market Maturity

The North American ready-to-eat cereal market is highly mature, with 2024 US retail sales around $8.2 billion and CAGR near 0-1%, forcing WK Kellogg Co to pursue share shifts rather than category growth.

Competitive intensity is high; Kellogg's market share declined to roughly 30% in 2024 amid private-label and healthier-positioned entrants, pressuring volume gains.

Maintaining or growing share requires elevated marketing and trade promotion spend—Kellogg's 2024 ad and promotion intensity rose to ~12-14% of net sales—compressing gross and operating margins.

- Slow market growth: ~0-1% CAGR (North America, 2024)

- Large but stagnant sales: ~$8.2B US retail cereal (2024)

- Kellogg share pressure: ~30% (2024)

- Higher promo intensity: ~12-14% of net sales (2024)

Kellogg margins squeezed: commodity spikes, higher rates & rising costs crush cash flow

Commodity-driven COGS volatility (corn +22% in 2023; sugar +18% in 2023) and raw-material inflation cut Kellogg’s margins in 2023–24; higher borrowing costs (10y ~4.2% in 2024; Fed funds 5.25–5.50% late-2024) and rising wages (+4.2% avg hourly earnings 2025) further press cash flow, while slow category growth (~0–1% CAGR North America 2024) and 30% market share force elevated promo spend (~12–14% of sales).

| Metric | Value |

|---|---|

| Corn (2023) | +22% |

| Sugar (2023) | +18% |

| US 10y (2024 avg) | ~4.2% |

| Fed funds (late‑2024) | 5.25–5.50% |

| Avg hourly earnings (2025) | +4.2% YoY |

| NA cereal CAGR (2024) | ~0–1% |

| Kellogg share (2024) | ~30% |

| Promo/ad intensity (2024) | ~12–14% net sales |

Preview the Actual Deliverable

WK Kellogg Co. PESTLE Analysis

The preview shown here is the exact WK Kellogg Co. PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and insights visible in this preview are identical to the downloadable file you’ll get immediately after checkout—no placeholders, no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis for WK Kellogg Co. highlights how regulatory shifts, changing consumer health preferences, supply-chain cost pressures, technological innovation in food processing, and sustainability mandates will shape the company’s near-term risks and growth opportunities—buy the full report to access actionable insights and editable charts for strategy or investment decisions.

Political factors

USMCA Trade Policy Stability

The company’s exclusive North American footprint ties supply-chain resilience to USMCA stability; USMCA accounted for roughly 75% of Kellogg’s 2024 regional revenue exposure, so tariff shifts could materially affect costs.

Imposition of cross-border duties or stricter rules of origin would raise input costs for grain and packaging, impacting gross margins—Kellogg reported a 2024 gross margin of about 33.4%, sensitive to commodity cost changes.

Management must track political shifts and potential renegotiations through 2026, including US–Mexico bilateral tensions and Canadian policy moves, as even modest tariff adjustments (1–3%) could trim EPS given Kellogg’s 2024 adjusted EPS of $2.79.

Federal Agricultural Subsidy Shifts

Federal support for corn and wheat—corn subsidies totaled about $12.3bn in 2024—directly affects input costs for Kellogg’s cereal lines, where grain can be 20–30% of COGS. Ongoing Farm Bill debates in 2024–25 created price volatility, with corn futures up ~18% YoY in 2024. A cut in subsidies would likely force Kellogg to raise retail prices or compress margins; a 10% raw grain cost rise could cut operating margin by ~1–1.5 percentage points.

Public Health Policy Initiatives

Government efforts to cut obesity and sugar intake—CDC reports adult obesity at 41.9% in 2019–2020 and WHO pushing sugar reduction—heighten regulatory risk for WK Kellogg Co; proposed federal sugar taxes or 2025 dietary guideline shifts could force reformulation across its $14.4B 2024 revenue cereal portfolio, raising R&D and CAPEX; active lobbying and policy engagement will be vital to shape legislation affecting ready-to-eat cereals.

School Nutrition Program Standards

Political changes to federal school breakfast nutrition standards directly affect WK Kellogg Co.’s institutional sales, which represented about 6% of North American cereal revenue in 2024 (approx. $120–150 million estimated).

Amendments to the Healthy, Hunger-Free Kids Act or new USDA mandates can render existing products ineligible for school programs, risking contract losses and inventory write-downs.

Ongoing compliance efforts and reformulation costs are necessary to retain long-term government contracts and safeguard recurring institutional revenue.

- Institutional sales ~6% of NA cereal revenue in 2024 (~$120–150M)

- Policy shifts can disqualify brands from schools

- Reformulation/compliance required to secure government contracts

Geopolitical Supply Chain Security

While WK Kellogg Co. targets North America, political instability in supplier regions for specialty ingredients (e.g., cocoa, palm oil) risks input shortages; in 2024 global cocoa supply shocks lifted prices ~18% YoY, pressuring margins.

Diplomatic tensions and sanctions can raise energy and additive costs—oil price volatility (2024 average Brent ~USD 86/bbl) increases manufacturing expense for large plants.

Energy-region unrest raises logistics and production costs; Kellogg’s 2024 freight and energy-related SG&A pressure contributed to a ~1–2% hit to operating margin.

- Exposure to specialty-ingredient supply risks (cocoa, palm oil)

- 2024 Brent ~USD 86/bbl; cocoa +18% YoY

- Energy/logistics volatility can reduce operating margin by ~1–2%

Kellogg margins at risk: USMCA exposure, commodity shocks & policy threats compress 2024

Political risks—USMCA exposure (~75% of 2024 NA revenue), tariff/ROO changes, Farm Bill subsidy shifts (corn subsidies ≈$12.3bn in 2024; corn futures +18% YoY), sugar/obesity policy threats to cereal reformulation, school nutrition rule changes impacting ~6% of NA cereal revenue (~$120–150M), and commodity/energy price shocks (cocoa +18% YoY; Brent ≈$86/bbl)—can compress Kellogg’s 2024 margins (gross 33.4%; adj. EPS $2.79).

| Metric | 2024 |

|---|---|

| USMCA revenue share | ~75% |

| Gross margin | 33.4% |

| Adj. EPS | $2.79 |

| Corn subsidies | $12.3bn |

| Corn futures YoY | +18% |

| Cocoa YoY | +18% |

| Brent avg | $86/bbl |

| School sales | ~$120–150M (6% NA cereal) |

What is included in the product

Explores how external macro-environmental factors uniquely affect WK Kellogg Co. across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, forward-looking insights, and actionable implications to inform strategy, risk mitigation, and investor communications.

A concise, visually segmented PESTLE snapshot of WK Kellogg Co. that’s easily inserted into presentations or shared across teams to streamline discussions on regulatory, economic, social, technological, environmental, and political risks and opportunities.

Economic factors

Commodity Price Volatility

Prices for sugar, corn and wheat—inputs accounting for a material share of WK Kellogg Co.’s COGS—are volatile: CBOT corn rose ~22% in 2023 while global sugar jumped ~18%, and such swings feed directly into margin pressure if costs cannot be passed to consumers.

Kellogg reported raw material inflation contributed to a 2023 gross margin decline versus 2022, and persistent agricultural inflation or supply shocks would further compress margins.

The company employs hedging and long-term supply contracts to manage exposure, but sustained elevated commodity prices remain a significant financial risk to profitability.

Consumer Purchasing Power

As a consumer staples firm, WK Kellogg Co. is exposed to shifts in disposable income; US real disposable personal income fell 0.3% in 2024 Q3 year-on-year, increasing pressure on premium lines like Bear Naked.

In downturns shoppers often trade down to private labels, which now hold about 17% of US cereal and snack categories (2024 IRI data), risking market share loss.

Maintaining brand equity and clear value propositions, plus targeted price promotions, is critical to retain customers when budgets tighten.

Interest Rate and Debt Management

Following the 2023 spin-off, WK Kellogg Co.’s capital structure and funding for its Supply Chain Reinvention are sensitive to prevailing interest rates; with US 10-year Treasury yields averaging ~4.2% in 2024 and the Fed funds rate at 5.25–5.50% by late 2024, borrowing costs rose, increasing debt servicing expense and constraining capital for facility upgrades.

Labor Market Inflation

- Average hourly earnings +4.2% YoY (2025)

- 14 states with min wage ≥15 USD (2025)

- Kellogg capex +8% in 2024 to support automation

North American Market Maturity

The North American ready-to-eat cereal market is highly mature, with 2024 US retail sales around $8.2 billion and CAGR near 0-1%, forcing WK Kellogg Co to pursue share shifts rather than category growth.

Competitive intensity is high; Kellogg's market share declined to roughly 30% in 2024 amid private-label and healthier-positioned entrants, pressuring volume gains.

Maintaining or growing share requires elevated marketing and trade promotion spend—Kellogg's 2024 ad and promotion intensity rose to ~12-14% of net sales—compressing gross and operating margins.

- Slow market growth: ~0-1% CAGR (North America, 2024)

- Large but stagnant sales: ~$8.2B US retail cereal (2024)

- Kellogg share pressure: ~30% (2024)

- Higher promo intensity: ~12-14% of net sales (2024)

Kellogg margins squeezed: commodity spikes, higher rates & rising costs crush cash flow

Commodity-driven COGS volatility (corn +22% in 2023; sugar +18% in 2023) and raw-material inflation cut Kellogg’s margins in 2023–24; higher borrowing costs (10y ~4.2% in 2024; Fed funds 5.25–5.50% late-2024) and rising wages (+4.2% avg hourly earnings 2025) further press cash flow, while slow category growth (~0–1% CAGR North America 2024) and 30% market share force elevated promo spend (~12–14% of sales).

| Metric | Value |

|---|---|

| Corn (2023) | +22% |

| Sugar (2023) | +18% |

| US 10y (2024 avg) | ~4.2% |

| Fed funds (late‑2024) | 5.25–5.50% |

| Avg hourly earnings (2025) | +4.2% YoY |

| NA cereal CAGR (2024) | ~0–1% |

| Kellogg share (2024) | ~30% |

| Promo/ad intensity (2024) | ~12–14% net sales |

Preview the Actual Deliverable

WK Kellogg Co. PESTLE Analysis

The preview shown here is the exact WK Kellogg Co. PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and insights visible in this preview are identical to the downloadable file you’ll get immediately after checkout—no placeholders, no surprises.