Waste Management Boston Consulting Group Matrix

Download Your Competitive Advantage

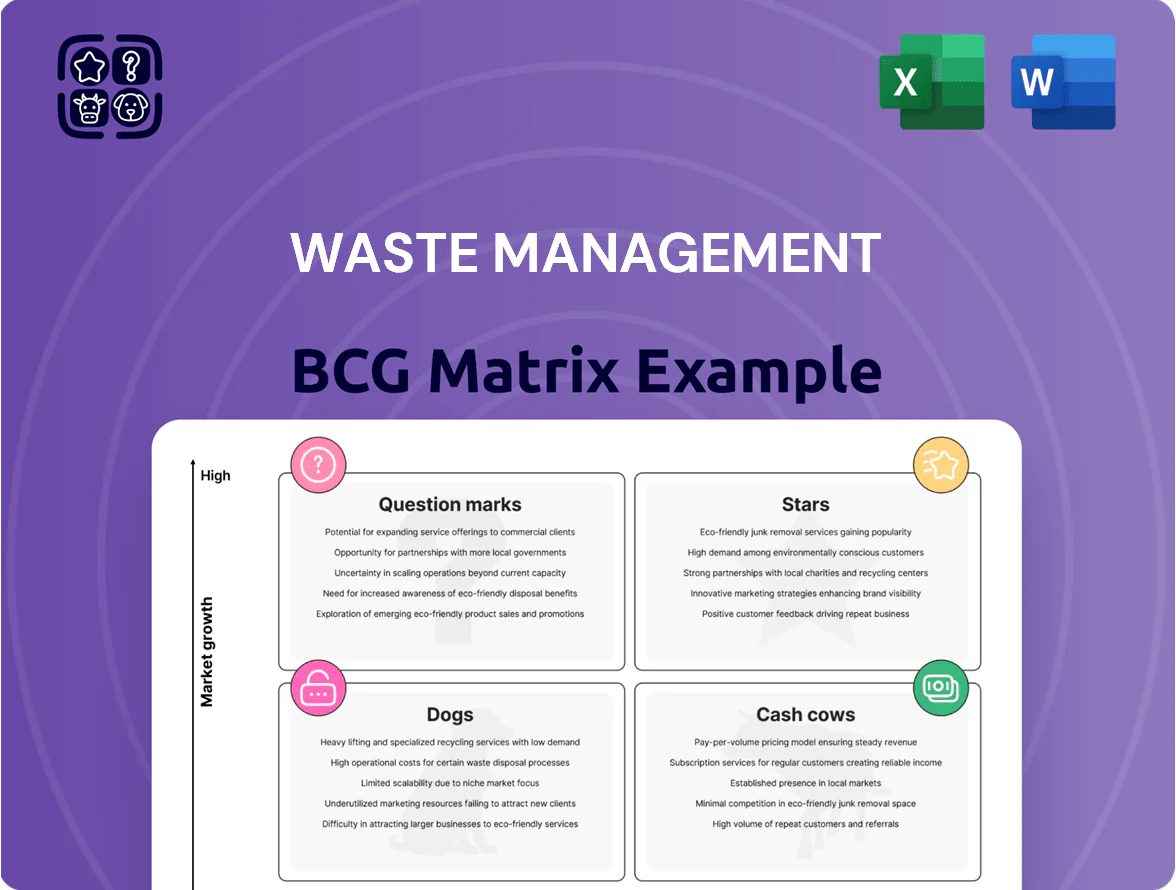

Waste Management’s BCG Matrix snapshot highlights which service lines drive cash (Cash Cows), which growth areas could become Stars, and where underperforming segments (Dogs) may need divestment—offering a concise view of portfolio strength and capital allocation priorities. This preview scratches the surface; purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and strategic actions you can implement immediately to optimize returns and operational focus.

Stars

Renewable Natural Gas (RNG) Production

This Star segment sees Waste Management converting landfill methane into pipeline-quality renewable natural gas (RNG), with 20 new RNG facilities planned through 2026 and roughly 500,000 MMBtu/year of additional capacity pre-sold under offtake agreements as of Dec 2025.

WM is deploying about $1.2 billion through 2026 to build and operate these sites, matching the Star profile: high growth (projected RNG revenue CAGR ~35% 2023–2026) and heavy cash consumption.

Market position is leading: WM estimates capturing ~15–20% of US landfill-to-RNG supply by 2026, strengthening margins via contracted sales and federal/state clean fuel credits.

Automated Recycling Operations

WM has upgraded recycling plants with AI sorting and robotics, lifting throughput ~25% and material purity to ~95%—boosting recovered commodity sales by an estimated $120M in 2025.

These automated facilities hold a leading North American market share (~30%) in circular-economy services as demand for recycled feedstock grows 8% CAGR through 2025.

Ongoing capex (~$200M–$300M annually) is needed to stay ahead, but automation cuts labor costs ~20%, pushing the segment toward higher EBITDA margins.

Industrial Waste Collection

Industrial Waste Collection became a Star after an inflection in late 2025 as global manufacturing PMI rose to 52.3 in Dec 2025, boosting volumes 18% YoY; WM’s market share sits near 28% in North America with revenue growth of 12% H2 2025. The segment benefits from high entry barriers and specialized fleet CAPEX of ~$200k per unit, where WM’s scale cuts unit cost 15%. Continued industrial output recovery through 2026 needs targeted sales and ~$120m in strategic investment to capture new contracts.

Healthcare Solutions (Stericycle Integration)

Following WM’s acquisition of Stericycle in 2024, the Healthcare Solutions unit now leads the medical waste and secure information disposal market, with pro forma FY2025 revenues ~USD 3.2bn and year-over-year growth ~18% as of Q4 2025.

Integration into WM’s field management drove margin expansion—adjusted EBIT margin rose ~220 basis points to ~12.6% by Q4 2025—despite ERP-related disruptions early 2025.

WM prioritizes investment here to consolidate share, targeting 6–8% organic growth and further margin gains through cross-selling and route optimization in 2026.

- Pro forma FY2025 revenue ~USD 3.2bn

- YoY growth ~18% (Q4 2025)

- Adjusted EBIT margin ~12.6% (Q4 2025)

- Investment focus: market consolidation, stabilize ERP issues

Sustainability Consulting Services

Sustainability Consulting Services sits in WM’s BCG Matrix as a Question Star: demand is surging due to stricter ESG mandates, and WM’s access to 30+ years of operational data gives it a clear competitive edge in carbon-footprint and waste-diversion strategy work.

The global sustainability consulting market is projected above $15 billion by 2026; WM’s unit can scale premium margins but must out‑market Big Four firms to capture share.

High growth and strategic fit signal strong future potential, though continued promotion and investment in analytics and client ROI proofs are required to convert growth into cash cows.

- 2026 market > $15B

- WM: 30+ years of operational data

- High growth, needs marketing vs Big Four

- Requires investment to become cash-generating

High-Growth RNG, Recycling & Healthcare: $1.2B RNG Capex, $3.2B Healthcare Rev

Stars: WM’s RNG, recycling automation, industrial waste, and Healthcare Solutions show high growth and heavy reinvestment—RNG capex $1.2B to 2026, ~500k MMBtu/year pre-sold, RNG revenue CAGR ~35% (2023–2026); recycling +25% throughput, $120M recovered sales (2025); Healthcare pro forma FY2025 rev ~$3.2B, adj. EBIT ~12.6% (Q4 2025).

| Unit | Key 2025–26 metrics |

|---|---|

| RNG | $1.2B capex; 500k MMBtu; 35% CAGR |

| Recycling | +25% throughput; $120M sales |

| Healthcare | $3.2B rev; 12.6% EBIT |

What is included in the product

Comprehensive BCG Matrix review of Waste Management’s units with strategic recommendations—invest in Stars, milk Cash Cows, evaluate Question Marks, divest Dogs.

One-page Waste Management BCG Matrix placing each business unit in a quadrant for quick strategic decisions

Cash Cows

Commercial Collection Services

Commercial Collection Services is the backbone of Waste Management’s revenue, generating stable cash flow from ~45,000 commercial customers across North America and contributing about 55% of 2024 consolidated operating cash flow (WM reported $5.2B operating cash flow in FY2024).

With high market share in core markets and thousands of established routes, the segment needs minimal incremental capital versus its cash generation—capex per revenue in 2024 was ~4%, well below company average.

Strong pricing power and high gross margins (mid-30s percent in 2024) let WM fund capital-intensive sustainability and energy projects like landfill gas-to-energy and recycling upgrades without diluting returns.

Landfill Disposal and Management

Operating over 250 active landfills, Waste Management controls scarce, hard-to-permit disposal sites, creating regional near-monopolies that reduced competition; in 2024 landfill volumes stayed ~55% of company total tons, underpinning steady demand.

This mature unit generates strong free cash flow—WM reported $3.6 billion adjusted free cash flow in 2024—with high barriers to entry and stable tip-fee revenue, making it a predictable cash cow.

Landfills act as the primary milkable asset, funding dividends and debt service: WM paid $1.35 billion in dividends and reduced net debt by $500 million in 2024, supporting balance-sheet resilience.

Municipal Solid Waste Contracts

WM holds multi-year municipal solid waste contracts with over 1,200 municipalities, delivering predictable, low-risk revenues—these agreements contributed roughly $7.4 billion in 2024 equivalent revenue, about 35% of consolidated service revenue.

Market growth for traditional municipal waste is ~1% annually, but WM’s high market share (estimated 17% national hauling share in 2024) secures dominant positioning and steady cash inflows.

These contracts act as a defensive portfolio layer, cutting volatility: in 2023–2024 recession periods, municipal contract revenue declined <2% versus 6–10% in commercial volumes, preserving free cash flow.

Transfer Station Network

Waste Management's 3,300+ transfer stations (2025) streamline logistics, cutting haul miles and costing low capex while earning mid-to-high single-digit EBITDA margins from third-party haulers, making them steady cash cows.

As mature assets, they need routine maintenance only, produced roughly $1.1B in fee revenue in 2024 and sustain predictable cash flow that underpins network efficiency and collection/disposal throughput.

- 3,300+ stations (2025)

- $1.1B fee revenue (2024)

- Mid–high single-digit EBITDA margins

- Low capex, routine maintenance

- Boosts haul efficiency, reduces miles

Hazardous Waste Management

Hazardous Waste Management sits in Waste Management’s Cash Cows quadrant: it runs specialized, highly regulated facilities in a mature market with few rivals able to match WM’s 2024 scale (Colex & US operations handled ~€1.2bn revenue across specialty services).

The high expertise and strict compliance keep gross margins near 28–32% and secure steady, high-margin contracts from industrial and government clients, supporting free cash flow.

It needs limited capex and modest marketing, delivering predictable cash to fund growth units while maintaining compliance and safety investments.

- 2024 revenue ~€1.2bn

- Gross margins 28–32%

- Low capex, high FCF

Waste Management: Predictable FCF Powerhouse — $3.6B Adj. FCF, 55% Landfill Tons

Waste Management’s Cash Cows (Commercial Collection, Landfills, Transfer Stations, Hazardous) produced predictable FCF: $3.6B adj. FCF (2024), $5.2B operating cash flow (2024), $1.35B dividends (2024); landfill volumes ~55% of tons (2024); capex/rev ~4% (2024); 3,300+ transfer stations (2025); hazardous revenue ~€1.2B (2024).

| Metric | 2024/2025 |

|---|---|

| Adj. FCF | $3.6B |

| Op CF | $5.2B |

| Dividends | $1.35B |

| Capex/Revs | ~4% |

| Landfill % tons | ~55% |

| Transfer stations | 3,300+ |

| Hazardous rev | €1.2B |

Preview = Final Product

Waste Management BCG Matrix

The file you're previewing is the exact Waste Management BCG Matrix report you’ll receive after purchase—no watermarks, no demo content—fully formatted and ready for strategic use. This preview mirrors the final downloadable document, built with market-backed analysis and clear visuals for immediate presentation or editing. Upon purchase, the complete file is delivered to your inbox with no surprises, revisions, or mockups—just a professional, analysis-ready report.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Waste Management’s BCG Matrix snapshot highlights which service lines drive cash (Cash Cows), which growth areas could become Stars, and where underperforming segments (Dogs) may need divestment—offering a concise view of portfolio strength and capital allocation priorities. This preview scratches the surface; purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and strategic actions you can implement immediately to optimize returns and operational focus.

Stars

Renewable Natural Gas (RNG) Production

This Star segment sees Waste Management converting landfill methane into pipeline-quality renewable natural gas (RNG), with 20 new RNG facilities planned through 2026 and roughly 500,000 MMBtu/year of additional capacity pre-sold under offtake agreements as of Dec 2025.

WM is deploying about $1.2 billion through 2026 to build and operate these sites, matching the Star profile: high growth (projected RNG revenue CAGR ~35% 2023–2026) and heavy cash consumption.

Market position is leading: WM estimates capturing ~15–20% of US landfill-to-RNG supply by 2026, strengthening margins via contracted sales and federal/state clean fuel credits.

Automated Recycling Operations

WM has upgraded recycling plants with AI sorting and robotics, lifting throughput ~25% and material purity to ~95%—boosting recovered commodity sales by an estimated $120M in 2025.

These automated facilities hold a leading North American market share (~30%) in circular-economy services as demand for recycled feedstock grows 8% CAGR through 2025.

Ongoing capex (~$200M–$300M annually) is needed to stay ahead, but automation cuts labor costs ~20%, pushing the segment toward higher EBITDA margins.

Industrial Waste Collection

Industrial Waste Collection became a Star after an inflection in late 2025 as global manufacturing PMI rose to 52.3 in Dec 2025, boosting volumes 18% YoY; WM’s market share sits near 28% in North America with revenue growth of 12% H2 2025. The segment benefits from high entry barriers and specialized fleet CAPEX of ~$200k per unit, where WM’s scale cuts unit cost 15%. Continued industrial output recovery through 2026 needs targeted sales and ~$120m in strategic investment to capture new contracts.

Healthcare Solutions (Stericycle Integration)

Following WM’s acquisition of Stericycle in 2024, the Healthcare Solutions unit now leads the medical waste and secure information disposal market, with pro forma FY2025 revenues ~USD 3.2bn and year-over-year growth ~18% as of Q4 2025.

Integration into WM’s field management drove margin expansion—adjusted EBIT margin rose ~220 basis points to ~12.6% by Q4 2025—despite ERP-related disruptions early 2025.

WM prioritizes investment here to consolidate share, targeting 6–8% organic growth and further margin gains through cross-selling and route optimization in 2026.

- Pro forma FY2025 revenue ~USD 3.2bn

- YoY growth ~18% (Q4 2025)

- Adjusted EBIT margin ~12.6% (Q4 2025)

- Investment focus: market consolidation, stabilize ERP issues

Sustainability Consulting Services

Sustainability Consulting Services sits in WM’s BCG Matrix as a Question Star: demand is surging due to stricter ESG mandates, and WM’s access to 30+ years of operational data gives it a clear competitive edge in carbon-footprint and waste-diversion strategy work.

The global sustainability consulting market is projected above $15 billion by 2026; WM’s unit can scale premium margins but must out‑market Big Four firms to capture share.

High growth and strategic fit signal strong future potential, though continued promotion and investment in analytics and client ROI proofs are required to convert growth into cash cows.

- 2026 market > $15B

- WM: 30+ years of operational data

- High growth, needs marketing vs Big Four

- Requires investment to become cash-generating

High-Growth RNG, Recycling & Healthcare: $1.2B RNG Capex, $3.2B Healthcare Rev

Stars: WM’s RNG, recycling automation, industrial waste, and Healthcare Solutions show high growth and heavy reinvestment—RNG capex $1.2B to 2026, ~500k MMBtu/year pre-sold, RNG revenue CAGR ~35% (2023–2026); recycling +25% throughput, $120M recovered sales (2025); Healthcare pro forma FY2025 rev ~$3.2B, adj. EBIT ~12.6% (Q4 2025).

| Unit | Key 2025–26 metrics |

|---|---|

| RNG | $1.2B capex; 500k MMBtu; 35% CAGR |

| Recycling | +25% throughput; $120M sales |

| Healthcare | $3.2B rev; 12.6% EBIT |

What is included in the product

Comprehensive BCG Matrix review of Waste Management’s units with strategic recommendations—invest in Stars, milk Cash Cows, evaluate Question Marks, divest Dogs.

One-page Waste Management BCG Matrix placing each business unit in a quadrant for quick strategic decisions

Cash Cows

Commercial Collection Services

Commercial Collection Services is the backbone of Waste Management’s revenue, generating stable cash flow from ~45,000 commercial customers across North America and contributing about 55% of 2024 consolidated operating cash flow (WM reported $5.2B operating cash flow in FY2024).

With high market share in core markets and thousands of established routes, the segment needs minimal incremental capital versus its cash generation—capex per revenue in 2024 was ~4%, well below company average.

Strong pricing power and high gross margins (mid-30s percent in 2024) let WM fund capital-intensive sustainability and energy projects like landfill gas-to-energy and recycling upgrades without diluting returns.

Landfill Disposal and Management

Operating over 250 active landfills, Waste Management controls scarce, hard-to-permit disposal sites, creating regional near-monopolies that reduced competition; in 2024 landfill volumes stayed ~55% of company total tons, underpinning steady demand.

This mature unit generates strong free cash flow—WM reported $3.6 billion adjusted free cash flow in 2024—with high barriers to entry and stable tip-fee revenue, making it a predictable cash cow.

Landfills act as the primary milkable asset, funding dividends and debt service: WM paid $1.35 billion in dividends and reduced net debt by $500 million in 2024, supporting balance-sheet resilience.

Municipal Solid Waste Contracts

WM holds multi-year municipal solid waste contracts with over 1,200 municipalities, delivering predictable, low-risk revenues—these agreements contributed roughly $7.4 billion in 2024 equivalent revenue, about 35% of consolidated service revenue.

Market growth for traditional municipal waste is ~1% annually, but WM’s high market share (estimated 17% national hauling share in 2024) secures dominant positioning and steady cash inflows.

These contracts act as a defensive portfolio layer, cutting volatility: in 2023–2024 recession periods, municipal contract revenue declined <2% versus 6–10% in commercial volumes, preserving free cash flow.

Transfer Station Network

Waste Management's 3,300+ transfer stations (2025) streamline logistics, cutting haul miles and costing low capex while earning mid-to-high single-digit EBITDA margins from third-party haulers, making them steady cash cows.

As mature assets, they need routine maintenance only, produced roughly $1.1B in fee revenue in 2024 and sustain predictable cash flow that underpins network efficiency and collection/disposal throughput.

- 3,300+ stations (2025)

- $1.1B fee revenue (2024)

- Mid–high single-digit EBITDA margins

- Low capex, routine maintenance

- Boosts haul efficiency, reduces miles

Hazardous Waste Management

Hazardous Waste Management sits in Waste Management’s Cash Cows quadrant: it runs specialized, highly regulated facilities in a mature market with few rivals able to match WM’s 2024 scale (Colex & US operations handled ~€1.2bn revenue across specialty services).

The high expertise and strict compliance keep gross margins near 28–32% and secure steady, high-margin contracts from industrial and government clients, supporting free cash flow.

It needs limited capex and modest marketing, delivering predictable cash to fund growth units while maintaining compliance and safety investments.

- 2024 revenue ~€1.2bn

- Gross margins 28–32%

- Low capex, high FCF

Waste Management: Predictable FCF Powerhouse — $3.6B Adj. FCF, 55% Landfill Tons

Waste Management’s Cash Cows (Commercial Collection, Landfills, Transfer Stations, Hazardous) produced predictable FCF: $3.6B adj. FCF (2024), $5.2B operating cash flow (2024), $1.35B dividends (2024); landfill volumes ~55% of tons (2024); capex/rev ~4% (2024); 3,300+ transfer stations (2025); hazardous revenue ~€1.2B (2024).

| Metric | 2024/2025 |

|---|---|

| Adj. FCF | $3.6B |

| Op CF | $5.2B |

| Dividends | $1.35B |

| Capex/Revs | ~4% |

| Landfill % tons | ~55% |

| Transfer stations | 3,300+ |

| Hazardous rev | €1.2B |

Preview = Final Product

Waste Management BCG Matrix

The file you're previewing is the exact Waste Management BCG Matrix report you’ll receive after purchase—no watermarks, no demo content—fully formatted and ready for strategic use. This preview mirrors the final downloadable document, built with market-backed analysis and clear visuals for immediate presentation or editing. Upon purchase, the complete file is delivered to your inbox with no surprises, revisions, or mockups—just a professional, analysis-ready report.