Waste Management PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unpack how regulation, commodity cycles, and green technology are reshaping Waste Management’s strategy and margin profile—our concise PESTLE highlights the key external drivers you need to assess risk and spot opportunity; purchase the full report for the complete, actionable breakdown and editable charts to use in pitches, forecasts, or investment memos.

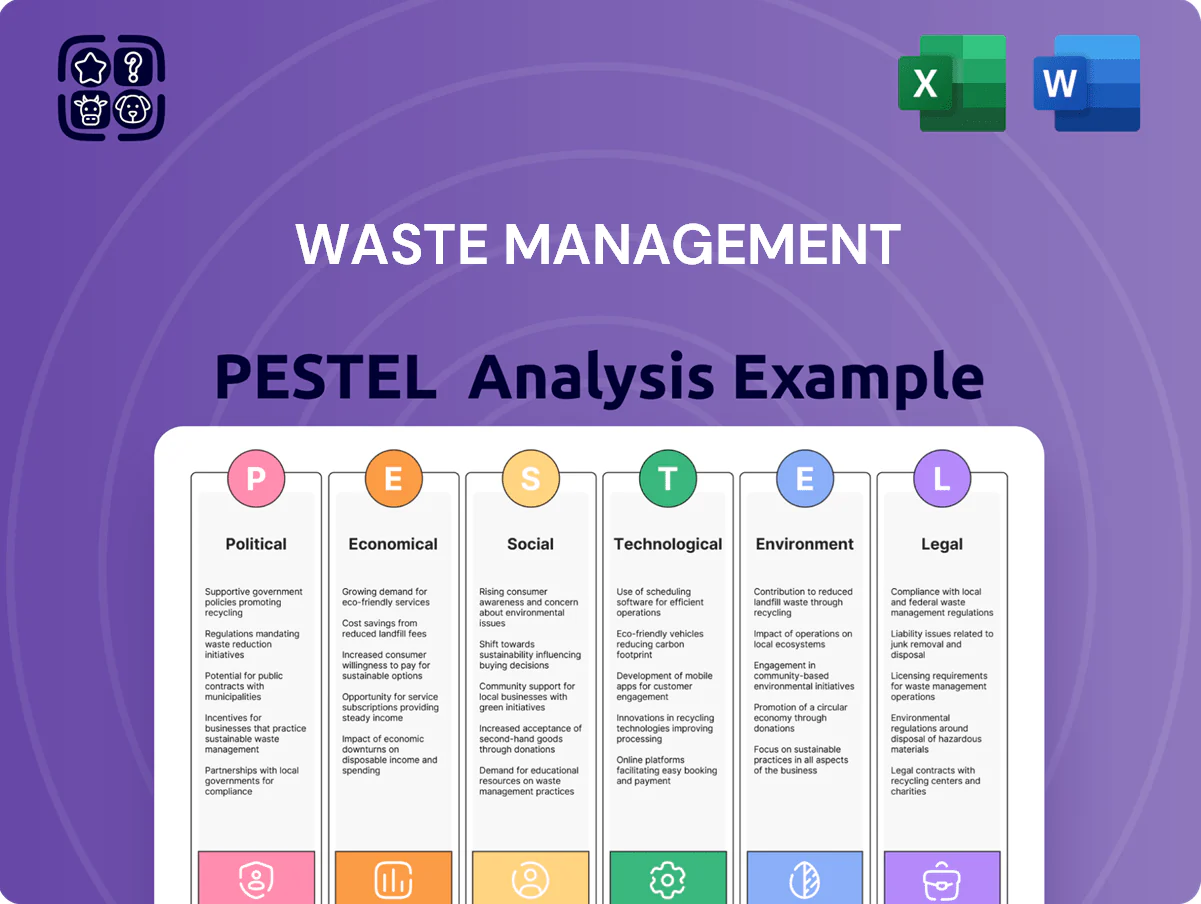

Political factors

Federal Incentives for Renewable Natural Gas

The Inflation Reduction Act provides production tax credits up to $85/metric ton CO2e avoided for renewable natural gas (RNG) from landfill methane, improving project IRRs; Waste Management reports over 100 operational RNG projects and targeted RNG sales of ~80 million MMBtu by 2025, boosting revenue and cash flow from gas-to-energy assets.

Municipal Contract Stability and Procurement

Local government policies and leadership changes shape procurement for long-term waste collection contracts; in the US, municipal contracts represent about 60–70% of sector revenues, with average contract lengths of 5–10 years providing revenue predictability for operators reporting stable cashflows and average EBITDA margins near 12% in 2024.

Election-driven policy shifts at city level frequently alter sustainability and recycling targets—cities adopting zero-waste or 50%+ recycling goals force contractors to invest in new sorting tech, affecting capital expenditure and contract renewal prospects.

International Trade Policy on Recyclables

Trade tensions and shifting import bans—China’s 2018 National Sword and Indonesia’s 2020 plastic restrictions—cut global recyclable trade volumes by over 50% in some streams, forcing U.S. exporters to reroute materials and depressing mixed paper prices by roughly 30% through 2024; political limits on plastic and paper scrap exports raise domestic processing needs, capital expenditures and operating costs for recyclers, with Waste Management reporting recycling segment revenue pressure and margin contraction (recycling profitability declined mid-single digits in 2024) as it adapts to complex international regulations.

Infrastructure Spending and Modernization Legislation

Federal grants and USDA/DOE loan programs funneled over $8.3 billion into U.S. waste-to-energy and recycling infrastructure in 2024–2025, lowering upfront costs for facility modernization.

Green economy initiatives, including the Inflation Reduction Act provisions, are accelerating shifts from landfilling to advanced material recovery, raising projected recycling-capacity investments by ~22% through 2026.

Policy subsidies and tax credits commonly cover portions of capital expenditures, reducing effective upgrade costs for processors by an estimated 15–30%.

- 2024–25 federal funding: $8.3B+

- Expected recycling-capacity investment growth: ~22% to 2026

- Typical subsidy impact on CAPEX: 15–30%

Carbon Taxation and Emissions Pricing

The introduction of carbon pricing—currently $15–$25/ton in several US state proposals and EU ETS prices averaging €95/ton in 2025—raises landfill operating costs via methane-equivalent charges, pushing operators toward gas capture and RNG projects to avoid fees.

Political debates over carbon costs shift strategy toward lower-emission disposal and increased recycling; Waste Management Inc. reported $420M in renewable energy revenue in 2024, reflecting this trend.

Favorable policies that reward low-carbon energy and penalize methane help WM capitalize on RNG, landfill-gas-to-energy projects and carbon credit sales, improving margins as carbon prices rise.

- Carbon price signals: EU €95/t (2025), US proposals $15–$25/t

- WM 2024 renewable energy revenue: $420M

- Policy impact: incentivizes gas capture, RNG, carbon credit monetization

Policy & funding surge fuels RNG, gas capture and WM renewables; recycling margins tighten

Political drivers—IRA tax credits (up to $85/t CO2e), $8.3B+ federal waste funding (2024–25), rising carbon prices (EU €95/t 2025; US proposals $15–$25/t), and municipal contract dynamics (60–70% sector revenue, 5–10yr terms)—accelerate RNG, gas capture, recycling CAPEX (+22% to 2026) and boost WM renewable revenue ($420M in 2024) while compressing recycling margins.

| Metric | Value |

|---|---|

| IRA RNG credit | $85/ton CO2e |

| Federal funding | $8.3B+ |

| EU carbon price (2025) | €95/t |

| WM renewable rev 2024 | $420M |

| Recycling CAPEX growth | ~22% to 2026 |

What is included in the product

Explores how macro-environmental factors uniquely affect Waste Management across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and regional regulatory context to identify threats and opportunities for executives and investors.

Condenses the Waste Management PESTLE into a crisp, shareable summary—segmented by category for quick risk/strategy alignment in meetings, editable for local context and ready to drop into presentations or consulting reports.

Economic factors

Commodity Price Volatility in Recycling

Commodity price volatility in recycling drives revenue swings as global supply-demand shifts push recycled paper, plastic and metal prices up to 30% year-over-year; recycled paper fell from about $120/ton in 2022 to $85/ton in parts of 2023, while scrap aluminum ranged $600–$1,800/ton in 2024.

Economic downturns compress demand and prices, reducing recovery margins—2023 saw U.S. recycled plastic bale prices drop ~25%, challenging profitability without fee adjustments.

Waste Management’s fee-for-service model, representing over 60% of revenue in 2024, cushions volatility, yet commodity markets remain a material economic driver for recycling unit economics.

Inflationary Pressure on Operating Costs

Rising diesel prices — up roughly 18% year-over-year in 2024 to an average of about $3.80/gal in the US—plus higher vehicle maintenance and parts costs compress Waste Management’s margins as fuel and repair account for a significant portion of operating expenses.

As a capital-intensive operator, Waste Management must offset inflation via targeted price adjustments and efficiency gains; the company’s 2024 capex guidance near $1.3–1.5 billion underscores ongoing fleet and facility investments.

Elevated interest rates (US 10-year Treasury averaging ~4.5% in 2024) raise borrowing costs for landfill expansions and fleet upgrades, increasing project finance costs and pressuring return on invested capital.

Consumer Spending and Waste Generation Volumes

Waste volumes track economic activity: global municipal solid waste rose to 2.24 billion tonnes in 2022 and is forecast to reach 3.40 billion tonnes by 2050, while OECD industrial production gains correlate with higher commercial waste tonnage; in 2023 US commercial waste increased ~4% amid GDP growth.

Labor Market Dynamics and Wage Inflation

Tight labor markets for commercial drivers and technicians have pushed median heavy-truck driver wages up about 7–9% year-over-year in 2024, raising recruitment and retention costs for waste management firms.

Rising wage expectations force higher spend on automation—capex per route rose ~5% in 2024—and competitive benefits, squeezing margins unless efficiency gains offset costs.

Workforce availability remains critical: regional vacancy rates for skilled technicians exceeded 10% in several U.S. metro areas in 2024, risking service reliability across diverse geographies.

- Driver wages +7–9% YoY (2024)

- Capex per route +5% (2024)

- Technician vacancy >10% in key metros (2024)

Capital Allocation for Fleet Electrification

The economic feasibility of electrifying waste fleets hinges on battery pack cost declines (down ~85% since 2010 to ~$120–140/kWh in 2024) and public/private charging deployment; converting a 100-truck diesel fleet can require $10–50M capex depending on vehicle type and charger intensity.

Long-term energy price forecasts (EIA 2025: oil $75–90/bbl base cases) shape replacement timing; ROI depends on diesel vs RNG or electricity price spreads and incentives (e.g., 30% ITC or state grants), with payback often 5–12 years.

- Battery cost ~120–140 USD/kWh (2024)

- Capex to convert 100 trucks: ~10–50 million USD

- Typical payback: 5–12 years depending on fuel price spreads

- Policy incentives (ITC, grants) materially improve ROI

Commodity shocks squeeze margins; fee-for-service steadies growth amid rising capex

Commodity price swings (recycled paper $85–120/ton 2022–23; scrap aluminum $600–1,800/ton 2024) and fuel (+18% to ~$3.80/gal 2024) compress margins; fee-for-service (>60% revenue 2024) cushions risk. Capex ~$1.3–1.5B (2024) and rising wages (+7–9% drivers 2024) plus higher borrowing costs (10y ~4.5% 2024) raise unit economics; EV battery ~$120–140/kWh aids transition with 5–12y paybacks.

| Metric | 2024/2023 |

|---|---|

| Fee-for-service | >60% rev |

| Capex guidance | $1.3–1.5B |

| Driver wages YoY | +7–9% |

| Fuel | ~$3.80/gal (+18%) |

| Battery cost | $120–140/kWh |

What You See Is What You Get

Waste Management PESTLE Analysis

The preview shown here is the exact Waste Management PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unpack how regulation, commodity cycles, and green technology are reshaping Waste Management’s strategy and margin profile—our concise PESTLE highlights the key external drivers you need to assess risk and spot opportunity; purchase the full report for the complete, actionable breakdown and editable charts to use in pitches, forecasts, or investment memos.

Political factors

Federal Incentives for Renewable Natural Gas

The Inflation Reduction Act provides production tax credits up to $85/metric ton CO2e avoided for renewable natural gas (RNG) from landfill methane, improving project IRRs; Waste Management reports over 100 operational RNG projects and targeted RNG sales of ~80 million MMBtu by 2025, boosting revenue and cash flow from gas-to-energy assets.

Municipal Contract Stability and Procurement

Local government policies and leadership changes shape procurement for long-term waste collection contracts; in the US, municipal contracts represent about 60–70% of sector revenues, with average contract lengths of 5–10 years providing revenue predictability for operators reporting stable cashflows and average EBITDA margins near 12% in 2024.

Election-driven policy shifts at city level frequently alter sustainability and recycling targets—cities adopting zero-waste or 50%+ recycling goals force contractors to invest in new sorting tech, affecting capital expenditure and contract renewal prospects.

International Trade Policy on Recyclables

Trade tensions and shifting import bans—China’s 2018 National Sword and Indonesia’s 2020 plastic restrictions—cut global recyclable trade volumes by over 50% in some streams, forcing U.S. exporters to reroute materials and depressing mixed paper prices by roughly 30% through 2024; political limits on plastic and paper scrap exports raise domestic processing needs, capital expenditures and operating costs for recyclers, with Waste Management reporting recycling segment revenue pressure and margin contraction (recycling profitability declined mid-single digits in 2024) as it adapts to complex international regulations.

Infrastructure Spending and Modernization Legislation

Federal grants and USDA/DOE loan programs funneled over $8.3 billion into U.S. waste-to-energy and recycling infrastructure in 2024–2025, lowering upfront costs for facility modernization.

Green economy initiatives, including the Inflation Reduction Act provisions, are accelerating shifts from landfilling to advanced material recovery, raising projected recycling-capacity investments by ~22% through 2026.

Policy subsidies and tax credits commonly cover portions of capital expenditures, reducing effective upgrade costs for processors by an estimated 15–30%.

- 2024–25 federal funding: $8.3B+

- Expected recycling-capacity investment growth: ~22% to 2026

- Typical subsidy impact on CAPEX: 15–30%

Carbon Taxation and Emissions Pricing

The introduction of carbon pricing—currently $15–$25/ton in several US state proposals and EU ETS prices averaging €95/ton in 2025—raises landfill operating costs via methane-equivalent charges, pushing operators toward gas capture and RNG projects to avoid fees.

Political debates over carbon costs shift strategy toward lower-emission disposal and increased recycling; Waste Management Inc. reported $420M in renewable energy revenue in 2024, reflecting this trend.

Favorable policies that reward low-carbon energy and penalize methane help WM capitalize on RNG, landfill-gas-to-energy projects and carbon credit sales, improving margins as carbon prices rise.

- Carbon price signals: EU €95/t (2025), US proposals $15–$25/t

- WM 2024 renewable energy revenue: $420M

- Policy impact: incentivizes gas capture, RNG, carbon credit monetization

Policy & funding surge fuels RNG, gas capture and WM renewables; recycling margins tighten

Political drivers—IRA tax credits (up to $85/t CO2e), $8.3B+ federal waste funding (2024–25), rising carbon prices (EU €95/t 2025; US proposals $15–$25/t), and municipal contract dynamics (60–70% sector revenue, 5–10yr terms)—accelerate RNG, gas capture, recycling CAPEX (+22% to 2026) and boost WM renewable revenue ($420M in 2024) while compressing recycling margins.

| Metric | Value |

|---|---|

| IRA RNG credit | $85/ton CO2e |

| Federal funding | $8.3B+ |

| EU carbon price (2025) | €95/t |

| WM renewable rev 2024 | $420M |

| Recycling CAPEX growth | ~22% to 2026 |

What is included in the product

Explores how macro-environmental factors uniquely affect Waste Management across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and regional regulatory context to identify threats and opportunities for executives and investors.

Condenses the Waste Management PESTLE into a crisp, shareable summary—segmented by category for quick risk/strategy alignment in meetings, editable for local context and ready to drop into presentations or consulting reports.

Economic factors

Commodity Price Volatility in Recycling

Commodity price volatility in recycling drives revenue swings as global supply-demand shifts push recycled paper, plastic and metal prices up to 30% year-over-year; recycled paper fell from about $120/ton in 2022 to $85/ton in parts of 2023, while scrap aluminum ranged $600–$1,800/ton in 2024.

Economic downturns compress demand and prices, reducing recovery margins—2023 saw U.S. recycled plastic bale prices drop ~25%, challenging profitability without fee adjustments.

Waste Management’s fee-for-service model, representing over 60% of revenue in 2024, cushions volatility, yet commodity markets remain a material economic driver for recycling unit economics.

Inflationary Pressure on Operating Costs

Rising diesel prices — up roughly 18% year-over-year in 2024 to an average of about $3.80/gal in the US—plus higher vehicle maintenance and parts costs compress Waste Management’s margins as fuel and repair account for a significant portion of operating expenses.

As a capital-intensive operator, Waste Management must offset inflation via targeted price adjustments and efficiency gains; the company’s 2024 capex guidance near $1.3–1.5 billion underscores ongoing fleet and facility investments.

Elevated interest rates (US 10-year Treasury averaging ~4.5% in 2024) raise borrowing costs for landfill expansions and fleet upgrades, increasing project finance costs and pressuring return on invested capital.

Consumer Spending and Waste Generation Volumes

Waste volumes track economic activity: global municipal solid waste rose to 2.24 billion tonnes in 2022 and is forecast to reach 3.40 billion tonnes by 2050, while OECD industrial production gains correlate with higher commercial waste tonnage; in 2023 US commercial waste increased ~4% amid GDP growth.

Labor Market Dynamics and Wage Inflation

Tight labor markets for commercial drivers and technicians have pushed median heavy-truck driver wages up about 7–9% year-over-year in 2024, raising recruitment and retention costs for waste management firms.

Rising wage expectations force higher spend on automation—capex per route rose ~5% in 2024—and competitive benefits, squeezing margins unless efficiency gains offset costs.

Workforce availability remains critical: regional vacancy rates for skilled technicians exceeded 10% in several U.S. metro areas in 2024, risking service reliability across diverse geographies.

- Driver wages +7–9% YoY (2024)

- Capex per route +5% (2024)

- Technician vacancy >10% in key metros (2024)

Capital Allocation for Fleet Electrification

The economic feasibility of electrifying waste fleets hinges on battery pack cost declines (down ~85% since 2010 to ~$120–140/kWh in 2024) and public/private charging deployment; converting a 100-truck diesel fleet can require $10–50M capex depending on vehicle type and charger intensity.

Long-term energy price forecasts (EIA 2025: oil $75–90/bbl base cases) shape replacement timing; ROI depends on diesel vs RNG or electricity price spreads and incentives (e.g., 30% ITC or state grants), with payback often 5–12 years.

- Battery cost ~120–140 USD/kWh (2024)

- Capex to convert 100 trucks: ~10–50 million USD

- Typical payback: 5–12 years depending on fuel price spreads

- Policy incentives (ITC, grants) materially improve ROI

Commodity shocks squeeze margins; fee-for-service steadies growth amid rising capex

Commodity price swings (recycled paper $85–120/ton 2022–23; scrap aluminum $600–1,800/ton 2024) and fuel (+18% to ~$3.80/gal 2024) compress margins; fee-for-service (>60% revenue 2024) cushions risk. Capex ~$1.3–1.5B (2024) and rising wages (+7–9% drivers 2024) plus higher borrowing costs (10y ~4.5% 2024) raise unit economics; EV battery ~$120–140/kWh aids transition with 5–12y paybacks.

| Metric | 2024/2023 |

|---|---|

| Fee-for-service | >60% rev |

| Capex guidance | $1.3–1.5B |

| Driver wages YoY | +7–9% |

| Fuel | ~$3.80/gal (+18%) |

| Battery cost | $120–140/kWh |

What You See Is What You Get

Waste Management PESTLE Analysis

The preview shown here is the exact Waste Management PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.