Wolverine World Wide SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Wolverine World Wide blends heritage brands and global distribution into a resilient footwear portfolio, yet faces margin pressure from raw material costs and intense retail competition; its sustainability investments and DTC expansion are key growth levers. Purchase the full SWOT analysis to access a professionally written, editable report and Excel matrix with deep, research-backed insights—ideal for investors, strategists, and advisors.

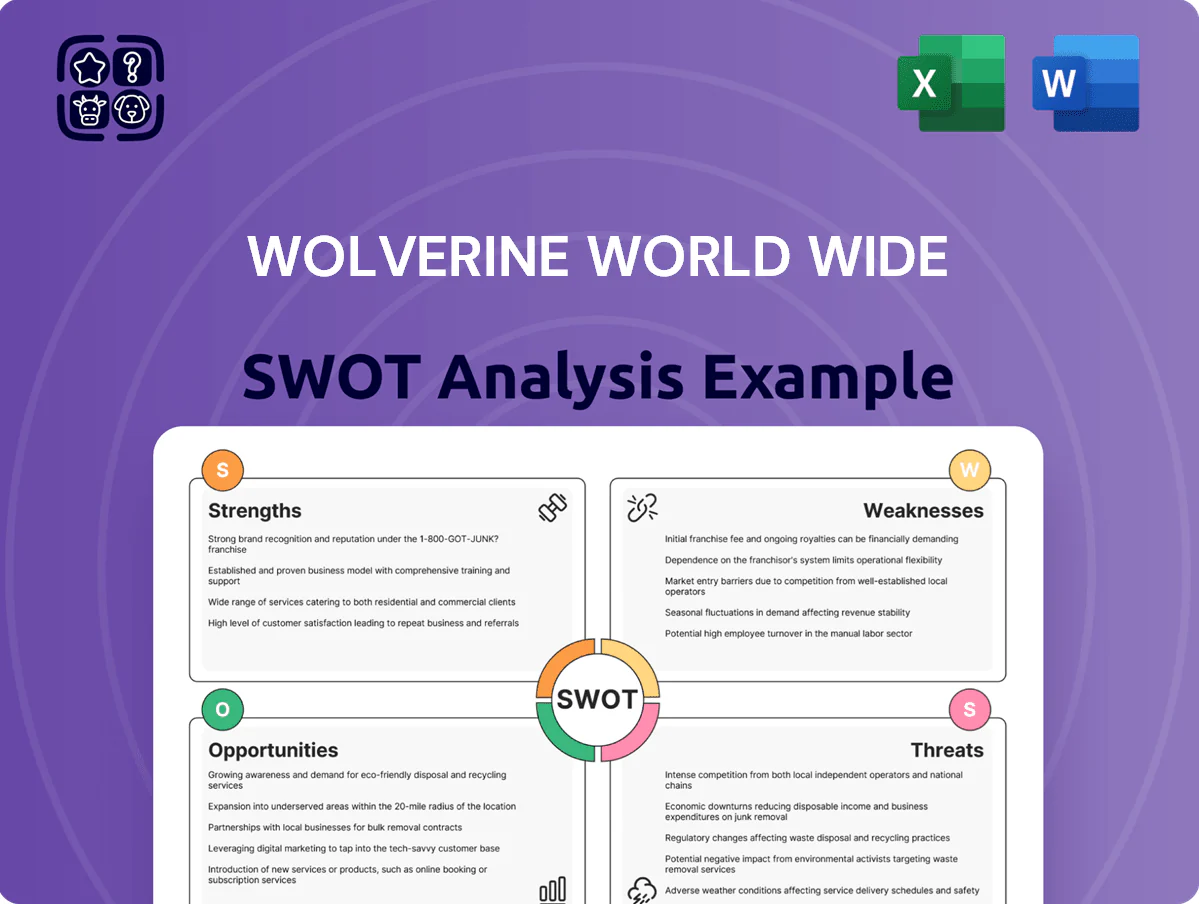

Strengths

Resilient Core Brand Equity

Wolverine World Wide's anchor brands Merrell and Saucony drive resilient core equity, with Merrell holding ~12% share of the US outdoor footwear market and Saucony ranking among the top five US running brands; both score above 80 Net Promoter Score in recent 2024 consumer surveys for durability and tech performance. Their loyalty-backed pricing power helped the company sustain 2024 net revenue of $1.8B despite a 3% industry downturn, stabilizing cash flow.

Streamlined Portfolio Architecture

After divesting Sperry in 2024 and Keds in 2025, Wolverine World Wide trimmed portfolio complexity, leaving a focused set of higher-margin brands; FY2025 adjusted operating margin rose to about 11.2%, up ~180 bps vs FY2023. This leaner architecture lets management redirect capital and marketing to priority growth drivers—recently a 15% increase in DTC (direct-to-consumer) sales shows faster ROI on digital spend. Faster decisions lowered SG&A as a percent of sales by ~120 bps in 2025.

Global Multi-Channel Distribution

Wolverine World Wide uses a three-pronged distribution mix—wholesale, 680+ company-owned and franchise retail stores (2024), and extensive third-party international licensing—covering 170+ countries; this blend drove $2.0B revenue in FY2024 from North America and $0.8B internationally.

Advanced Technical Innovation Capabilities

Enhanced Direct-to-Consumer Infrastructure

Wolverine World Wide’s 2024 DTC sales grew to 25% of net revenue (fiscal 2024), driven by a revamped ecommerce platform that captures first-party data and boosted DTC gross margins by ~400 basis points vs wholesale.

Real-time consumer signals now cut stock‑out risk and markdowns; the company reported inventory turns improved from 3.8 to 4.3 in 2024, enabling more targeted email and personalization that raised repeat purchase rates by ~12% year‑over‑year.

- 25% of revenue via DTC (fiscal 2024)

- ≈400 bps higher DTC gross margin

- Inventory turns +0.5 (3.8→4.3) in 2024

- Repeat purchases +12% YoY

Merrell & Saucony fuel $1.8B sales, 25% DTC and 11.2% adj. op margin

Merrell and Saucony drive resilient brand equity (~12% US outdoor share; Saucony top‑5 running), supporting 2024 net revenue $1.8B and FY2025 adjusted operating margin ~11.2%. DTC rose to 25% of sales (2024), boosting gross margin ~400 bps vs wholesale; inventory turns improved 3.8→4.3, repeat purchases +12% YoY; R&D ~$45M, performance gross margin ~48%.

| Metric | Value |

|---|---|

| 2024 Net Rev | $1.8B |

| FY2025 Adj Op Margin | 11.2% |

| DTC % (2024) | 25% |

| R&D (2024) | $45M |

What is included in the product

Provides a concise SWOT overview highlighting Wolverine World Wide’s core strengths, operational weaknesses, market opportunities, and external threats to assess its strategic position and growth prospects.

Delivers a focused SWOT snapshot of Wolverine World Wide to speed strategic alignment and stakeholder briefings.

Weaknesses

Elevated Debt Obligations

Heavy Exposure to Wholesale Volatility

Significant Brand Concentration Risk

Historical Inventory Management Challenges

- 220 bps gross margin hit (FY2023)

- $120M inventory write-down (FY2022)

- 8–12% seasonal order swings

- Promotions risk brand dilution

Variable Operating Margins

WWW burdened by $880M net debt, margin erosion and wholesale inventory risks

| Metric | Value |

|---|---|

| Net debt (YE2024) | $880M |

| Interest expense (2024) | $45M |

| Wholesale share (FY2024) | 42% |

| Gross margin (FY2024) | 34.2% |

| Gross margin (FY2022) | 36.8% |

| Freight change (2024 YoY) | +12% |

| Inventory write-down (FY2022) | $120M |

| Gross margin hit (FY2023) | 220 bps |

Preview the Actual Deliverable

Wolverine World Wide SWOT Analysis

This preview is taken directly from the full Wolverine World Wide SWOT report you'll receive upon purchase—professional quality and complete structure with no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Wolverine World Wide blends heritage brands and global distribution into a resilient footwear portfolio, yet faces margin pressure from raw material costs and intense retail competition; its sustainability investments and DTC expansion are key growth levers. Purchase the full SWOT analysis to access a professionally written, editable report and Excel matrix with deep, research-backed insights—ideal for investors, strategists, and advisors.

Strengths

Resilient Core Brand Equity

Wolverine World Wide's anchor brands Merrell and Saucony drive resilient core equity, with Merrell holding ~12% share of the US outdoor footwear market and Saucony ranking among the top five US running brands; both score above 80 Net Promoter Score in recent 2024 consumer surveys for durability and tech performance. Their loyalty-backed pricing power helped the company sustain 2024 net revenue of $1.8B despite a 3% industry downturn, stabilizing cash flow.

Streamlined Portfolio Architecture

After divesting Sperry in 2024 and Keds in 2025, Wolverine World Wide trimmed portfolio complexity, leaving a focused set of higher-margin brands; FY2025 adjusted operating margin rose to about 11.2%, up ~180 bps vs FY2023. This leaner architecture lets management redirect capital and marketing to priority growth drivers—recently a 15% increase in DTC (direct-to-consumer) sales shows faster ROI on digital spend. Faster decisions lowered SG&A as a percent of sales by ~120 bps in 2025.

Global Multi-Channel Distribution

Wolverine World Wide uses a three-pronged distribution mix—wholesale, 680+ company-owned and franchise retail stores (2024), and extensive third-party international licensing—covering 170+ countries; this blend drove $2.0B revenue in FY2024 from North America and $0.8B internationally.

Advanced Technical Innovation Capabilities

Enhanced Direct-to-Consumer Infrastructure

Wolverine World Wide’s 2024 DTC sales grew to 25% of net revenue (fiscal 2024), driven by a revamped ecommerce platform that captures first-party data and boosted DTC gross margins by ~400 basis points vs wholesale.

Real-time consumer signals now cut stock‑out risk and markdowns; the company reported inventory turns improved from 3.8 to 4.3 in 2024, enabling more targeted email and personalization that raised repeat purchase rates by ~12% year‑over‑year.

- 25% of revenue via DTC (fiscal 2024)

- ≈400 bps higher DTC gross margin

- Inventory turns +0.5 (3.8→4.3) in 2024

- Repeat purchases +12% YoY

Merrell & Saucony fuel $1.8B sales, 25% DTC and 11.2% adj. op margin

Merrell and Saucony drive resilient brand equity (~12% US outdoor share; Saucony top‑5 running), supporting 2024 net revenue $1.8B and FY2025 adjusted operating margin ~11.2%. DTC rose to 25% of sales (2024), boosting gross margin ~400 bps vs wholesale; inventory turns improved 3.8→4.3, repeat purchases +12% YoY; R&D ~$45M, performance gross margin ~48%.

| Metric | Value |

|---|---|

| 2024 Net Rev | $1.8B |

| FY2025 Adj Op Margin | 11.2% |

| DTC % (2024) | 25% |

| R&D (2024) | $45M |

What is included in the product

Provides a concise SWOT overview highlighting Wolverine World Wide’s core strengths, operational weaknesses, market opportunities, and external threats to assess its strategic position and growth prospects.

Delivers a focused SWOT snapshot of Wolverine World Wide to speed strategic alignment and stakeholder briefings.

Weaknesses

Elevated Debt Obligations

Heavy Exposure to Wholesale Volatility

Significant Brand Concentration Risk

Historical Inventory Management Challenges

- 220 bps gross margin hit (FY2023)

- $120M inventory write-down (FY2022)

- 8–12% seasonal order swings

- Promotions risk brand dilution

Variable Operating Margins

WWW burdened by $880M net debt, margin erosion and wholesale inventory risks

| Metric | Value |

|---|---|

| Net debt (YE2024) | $880M |

| Interest expense (2024) | $45M |

| Wholesale share (FY2024) | 42% |

| Gross margin (FY2024) | 34.2% |

| Gross margin (FY2022) | 36.8% |

| Freight change (2024 YoY) | +12% |

| Inventory write-down (FY2022) | $120M |

| Gross margin hit (FY2023) | 220 bps |

Preview the Actual Deliverable

Wolverine World Wide SWOT Analysis

This preview is taken directly from the full Wolverine World Wide SWOT report you'll receive upon purchase—professional quality and complete structure with no surprises.