Woolworths Porter's Five Forces Analysis

From Overview to Strategy Blueprint

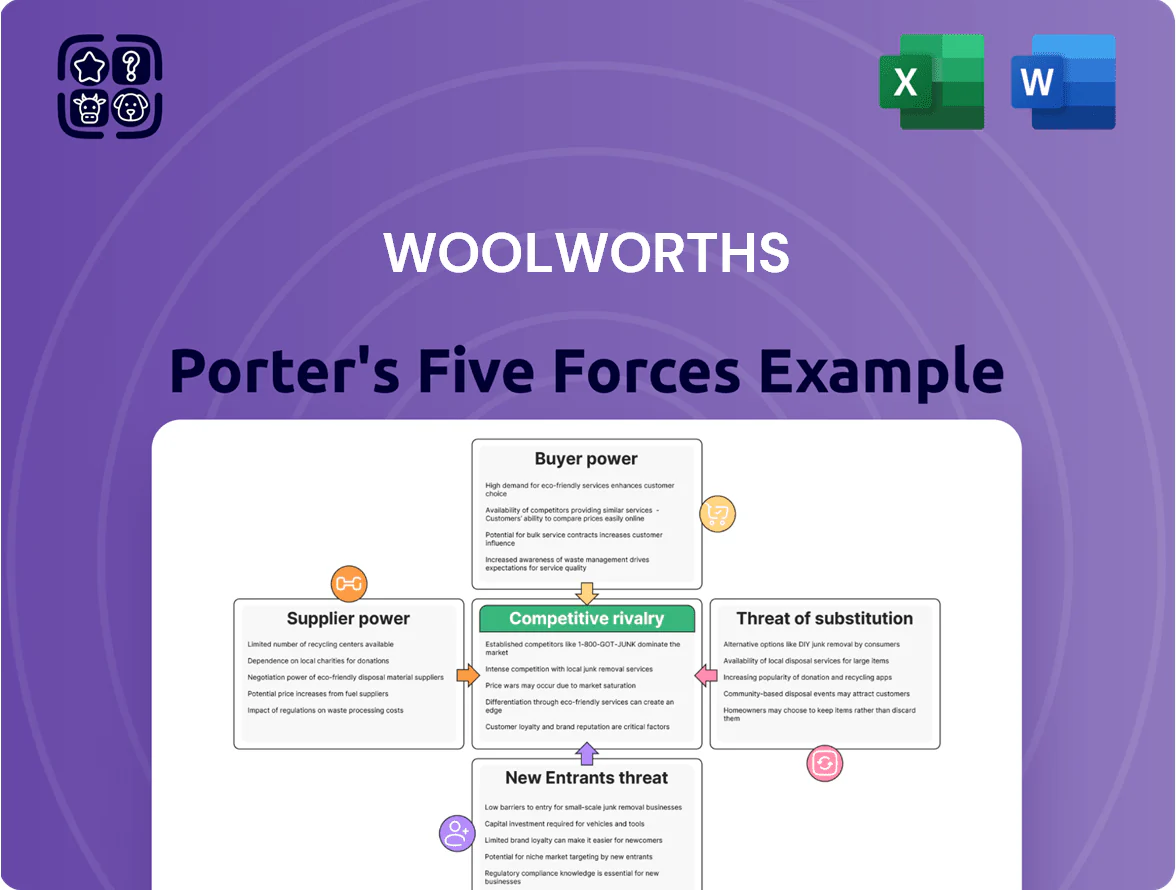

Woolworths faces intense buyer power and competitive rivalry, moderate supplier influence, low threat of new entrants due to scale, and rising substitution pressures from discounters and online grocers—putting margin pressure on incumbents.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Woolworths’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Global Brand Manufacturers

Woolworths depends on multinationals like Nestle, Procter & Gamble and Coca-Cola, whose strong brand equity and combined supermarket shelf share exceed 40% in many FMCG categories, giving suppliers moderate bargaining power because delisting risks footfall loss. Woolworths counters this with scale — FY2024 Australia group sales A$45.6bn — pressuring suppliers into lower wholesale prices and funded promotions, securing margin relief and in-store prominence.

Fragmented Local Agricultural Supply Base

The fragmented local agricultural supply base gives individual Australian farmers low bargaining power versus Woolworths, which held about 37% grocery market share in 2024 and often sets quality, delivery and price terms for small producers.

Few alternative large buyers exist, squeezing margins for small suppliers; a 2023 ACCC review noted repeated complaints and drove the 2023 voluntary Retail Grocery Industry Code of Conduct to protect primary producers.

Strategic Expansion of Private Label Brands

Woolworths has grown its private-label roster—Woolworths Essentials and Macro Wholefoods—so private-label sales reached 19.2% of supermarket sales in FY2024, cutting reliance on big-brand suppliers. By vertically integrating production and sourcing, Woolworths captures higher margins (private label gross margins ~28% vs national brands ~18% in FY2024) and gains bargaining leverage. This gives a credible threat to delist third-party lines and switch shelf space to own brands, thereby lowering supplier power and input cost exposure.

High Switching Costs for Suppliers

For most suppliers, losing a Woolworths distribution contract is catastrophic: Woolworths held ~37% of Australian supermarket share in 2024, so alternatives cannot match its volume or shelf reach.

This dependence lets Woolworths enforce strict logistics standards and real-time data sharing (POS/EPC), reducing suppliers’ negotiating power and raising their effective switching costs.

- Woolworths market share ~37% (2024)

- Major suppliers often rely on single-retailer volume

- Mandatory logistics/data requirements (POS/EPC)

Advancements in Vertical Integration

By end-2025 Woolworths expanded vertical integration with A$420m in primary-processing and logistics capex, boosting in-house fresh produce and meat sourcing and cutting reliance on wholesalers.

This reduced intermediary bargaining power, improved margin control (gross margin +0.8ppt YoY to 25.6% in FY25) and lowered supply cost volatility.

- Capex A$420m

- Gross margin 25.6% FY25 (+0.8ppt)

- Less wholesale exposure

- More stable fresh supply

Woolworths' scale and private-label push squeeze supplier power

Suppliers have moderate-to-low power: big multinationals hold strong brands, but Woolworths’ ~37% Aussie grocery share (2024), private-label mix 19.2% (FY2024), and A$420m FY25 capex for vertical integration shift leverage to Woolworths, raising switching costs for suppliers and lowering input price pressure.

| Metric | Value |

|---|---|

| Woolworths market share (2024) | ~37% |

| Private-label sales (FY2024) | 19.2% |

| Capex for integration (end-2025) | A$420m |

| Private-label gross margin (FY2024) | ~28% vs brands ~18% |

What is included in the product

Tailored exclusively for Woolworths, this Porter's Five Forces overview uncovers competitive intensity, buyer/supplier power, entry barriers, substitutes, and emerging threats—highlighting key drivers of pricing, profitability, and strategic defense within its retail landscape.

Concise Porter's Five Forces summary for Woolworths—quickly gauge competitive pressure and prioritize strategic actions.

Customers Bargaining Power

Negligible Switching Costs for Shoppers

Consumers face almost zero switching costs—shopping at Coles or Aldi costs Australians no extra fees and takes similar time, so loyalty is volatile; Woolworths reported a 0.6% like-for-like sales growth in FY2024, showing sensitivity to small moves in market share.

This lack of friction forces Woolworths to constantly earn loyalty via pricing and service; the retailer spent A$1.1bn on supply-chain and store investments in FY2024 to keep availability high and reduce churn.

High Price Sensitivity Amid Economic Pressures

In late 2025 Australian consumers remain highly value-focused as CPI inflation eased to 3.6% year-on-year in Q3 2025 but real wages are still down ~1.5% since 2022, driving price sensitivity. Shoppers use price-comparison apps and Woolworths’ app price checks; 62% of grocery buyers report hunting promotions weekly in a 2025 Roy Morgan survey. This limits Woolworths’ pricing power—price hikes above 2–3% risk cutting volumes and market share in a ~33% market where private label growth is rising.

Influence of Sophisticated Loyalty Programs

The Everyday Rewards program reduces buyer power by creating stickiness: as of FY2024 Woolworths reported 14.6 million active members, who generated ~60% of supermarket sales, raising the perceived switching cost via points redeemable for fuel and groceries.

Transparency Through Digital Platforms

The rise of mobile apps and online grocery platforms gives Australian shoppers instant price checks and product data, with 54% of grocery purchases influenced by online research (Roy Morgan, 2024), pushing Woolworths to match prices and promos in real time to retain customers.

Customers track spend and compare rivals in minutes, and Woolworths’ 2024 online sales growth of ~12% shows pressure to expand digital offers and price transparency.

- 54% influenced by online research (Roy Morgan 2024)

- Woolworths online sales +12% in 2024

- Real-time price matching needed

Concentrated Buying Power in Urban Centers

In dense urban areas, collective customer choices steer Woolworths’ strategy: about 70% of Australian retail spend occurs in metro regions, so city-level demand shapes product range and store format decisions.

Woolworths must tailor inventory and smaller-format stores to local demographics; mismatches risk ceding share to niche players—Aldi and local grocers grew metro share by ~2–4% in 2024.

- Urban spend concentration ~70%

- Metro-driven format shifts: smaller stores up 12% since 2020

- Failing to localize → 2–4% share loss to discounters (2024)

Promo-driven shoppers squeeze Woolworths’ pricing power despite 14.6m loyalty members

Customers have high bargaining power: near-zero switching costs, strong price sensitivity (CPI 3.6% YoY Q3 2025; real wages down ~1.5% since 2022), and 62% hunt promos weekly (Roy Morgan 2025), forcing Woolworths to match prices and invest in loyalty; Everyday Rewards (14.6m members, ~60% sales FY2024) raises stickiness but pricing power stays limited.

| Metric | Value |

|---|---|

| Everyday Rewards members (FY2024) | 14.6m |

| Share of sales from members | ~60% |

| Like-for-like sales (FY2024) | +0.6% |

| Online sales growth (2024) | +12% |

| Promo hunters (Roy Morgan 2025) | 62% |

| CPI (Q3 2025) | 3.6% YoY |

| Real wages since 2022 | -~1.5% |

What You See Is What You Get

Woolworths Porter's Five Forces Analysis

This preview shows the exact Woolworths Porter’s Five Forces analysis you’ll receive—no placeholders or mockups—fully formatted and ready for immediate download upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Woolworths faces intense buyer power and competitive rivalry, moderate supplier influence, low threat of new entrants due to scale, and rising substitution pressures from discounters and online grocers—putting margin pressure on incumbents.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Woolworths’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Global Brand Manufacturers

Woolworths depends on multinationals like Nestle, Procter & Gamble and Coca-Cola, whose strong brand equity and combined supermarket shelf share exceed 40% in many FMCG categories, giving suppliers moderate bargaining power because delisting risks footfall loss. Woolworths counters this with scale — FY2024 Australia group sales A$45.6bn — pressuring suppliers into lower wholesale prices and funded promotions, securing margin relief and in-store prominence.

Fragmented Local Agricultural Supply Base

The fragmented local agricultural supply base gives individual Australian farmers low bargaining power versus Woolworths, which held about 37% grocery market share in 2024 and often sets quality, delivery and price terms for small producers.

Few alternative large buyers exist, squeezing margins for small suppliers; a 2023 ACCC review noted repeated complaints and drove the 2023 voluntary Retail Grocery Industry Code of Conduct to protect primary producers.

Strategic Expansion of Private Label Brands

Woolworths has grown its private-label roster—Woolworths Essentials and Macro Wholefoods—so private-label sales reached 19.2% of supermarket sales in FY2024, cutting reliance on big-brand suppliers. By vertically integrating production and sourcing, Woolworths captures higher margins (private label gross margins ~28% vs national brands ~18% in FY2024) and gains bargaining leverage. This gives a credible threat to delist third-party lines and switch shelf space to own brands, thereby lowering supplier power and input cost exposure.

High Switching Costs for Suppliers

For most suppliers, losing a Woolworths distribution contract is catastrophic: Woolworths held ~37% of Australian supermarket share in 2024, so alternatives cannot match its volume or shelf reach.

This dependence lets Woolworths enforce strict logistics standards and real-time data sharing (POS/EPC), reducing suppliers’ negotiating power and raising their effective switching costs.

- Woolworths market share ~37% (2024)

- Major suppliers often rely on single-retailer volume

- Mandatory logistics/data requirements (POS/EPC)

Advancements in Vertical Integration

By end-2025 Woolworths expanded vertical integration with A$420m in primary-processing and logistics capex, boosting in-house fresh produce and meat sourcing and cutting reliance on wholesalers.

This reduced intermediary bargaining power, improved margin control (gross margin +0.8ppt YoY to 25.6% in FY25) and lowered supply cost volatility.

- Capex A$420m

- Gross margin 25.6% FY25 (+0.8ppt)

- Less wholesale exposure

- More stable fresh supply

Woolworths' scale and private-label push squeeze supplier power

Suppliers have moderate-to-low power: big multinationals hold strong brands, but Woolworths’ ~37% Aussie grocery share (2024), private-label mix 19.2% (FY2024), and A$420m FY25 capex for vertical integration shift leverage to Woolworths, raising switching costs for suppliers and lowering input price pressure.

| Metric | Value |

|---|---|

| Woolworths market share (2024) | ~37% |

| Private-label sales (FY2024) | 19.2% |

| Capex for integration (end-2025) | A$420m |

| Private-label gross margin (FY2024) | ~28% vs brands ~18% |

What is included in the product

Tailored exclusively for Woolworths, this Porter's Five Forces overview uncovers competitive intensity, buyer/supplier power, entry barriers, substitutes, and emerging threats—highlighting key drivers of pricing, profitability, and strategic defense within its retail landscape.

Concise Porter's Five Forces summary for Woolworths—quickly gauge competitive pressure and prioritize strategic actions.

Customers Bargaining Power

Negligible Switching Costs for Shoppers

Consumers face almost zero switching costs—shopping at Coles or Aldi costs Australians no extra fees and takes similar time, so loyalty is volatile; Woolworths reported a 0.6% like-for-like sales growth in FY2024, showing sensitivity to small moves in market share.

This lack of friction forces Woolworths to constantly earn loyalty via pricing and service; the retailer spent A$1.1bn on supply-chain and store investments in FY2024 to keep availability high and reduce churn.

High Price Sensitivity Amid Economic Pressures

In late 2025 Australian consumers remain highly value-focused as CPI inflation eased to 3.6% year-on-year in Q3 2025 but real wages are still down ~1.5% since 2022, driving price sensitivity. Shoppers use price-comparison apps and Woolworths’ app price checks; 62% of grocery buyers report hunting promotions weekly in a 2025 Roy Morgan survey. This limits Woolworths’ pricing power—price hikes above 2–3% risk cutting volumes and market share in a ~33% market where private label growth is rising.

Influence of Sophisticated Loyalty Programs

The Everyday Rewards program reduces buyer power by creating stickiness: as of FY2024 Woolworths reported 14.6 million active members, who generated ~60% of supermarket sales, raising the perceived switching cost via points redeemable for fuel and groceries.

Transparency Through Digital Platforms

The rise of mobile apps and online grocery platforms gives Australian shoppers instant price checks and product data, with 54% of grocery purchases influenced by online research (Roy Morgan, 2024), pushing Woolworths to match prices and promos in real time to retain customers.

Customers track spend and compare rivals in minutes, and Woolworths’ 2024 online sales growth of ~12% shows pressure to expand digital offers and price transparency.

- 54% influenced by online research (Roy Morgan 2024)

- Woolworths online sales +12% in 2024

- Real-time price matching needed

Concentrated Buying Power in Urban Centers

In dense urban areas, collective customer choices steer Woolworths’ strategy: about 70% of Australian retail spend occurs in metro regions, so city-level demand shapes product range and store format decisions.

Woolworths must tailor inventory and smaller-format stores to local demographics; mismatches risk ceding share to niche players—Aldi and local grocers grew metro share by ~2–4% in 2024.

- Urban spend concentration ~70%

- Metro-driven format shifts: smaller stores up 12% since 2020

- Failing to localize → 2–4% share loss to discounters (2024)

Promo-driven shoppers squeeze Woolworths’ pricing power despite 14.6m loyalty members

Customers have high bargaining power: near-zero switching costs, strong price sensitivity (CPI 3.6% YoY Q3 2025; real wages down ~1.5% since 2022), and 62% hunt promos weekly (Roy Morgan 2025), forcing Woolworths to match prices and invest in loyalty; Everyday Rewards (14.6m members, ~60% sales FY2024) raises stickiness but pricing power stays limited.

| Metric | Value |

|---|---|

| Everyday Rewards members (FY2024) | 14.6m |

| Share of sales from members | ~60% |

| Like-for-like sales (FY2024) | +0.6% |

| Online sales growth (2024) | +12% |

| Promo hunters (Roy Morgan 2025) | 62% |

| CPI (Q3 2025) | 3.6% YoY |

| Real wages since 2022 | -~1.5% |

What You See Is What You Get

Woolworths Porter's Five Forces Analysis

This preview shows the exact Woolworths Porter’s Five Forces analysis you’ll receive—no placeholders or mockups—fully formatted and ready for immediate download upon purchase.