Workday PESTLE Analysis

Skip the Research. Get the Strategy.

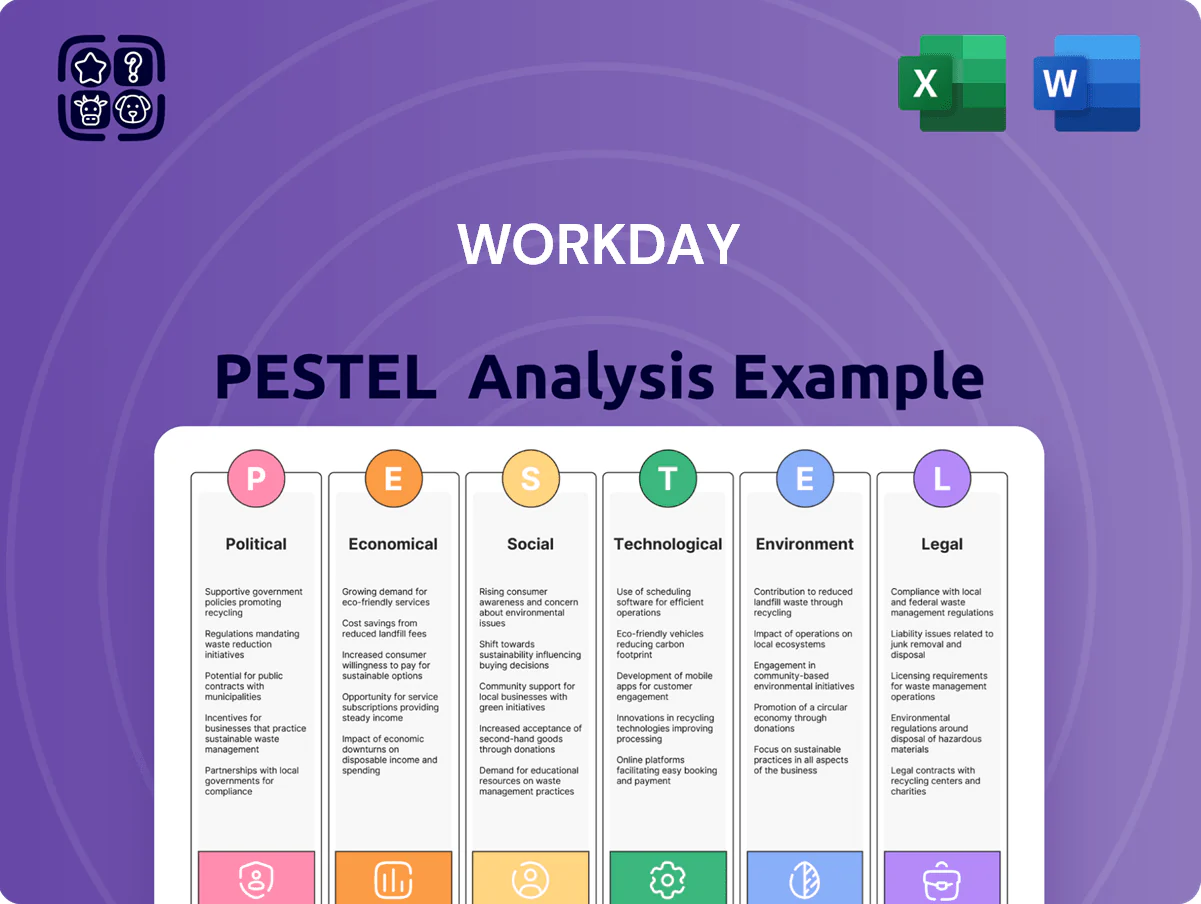

Gain a strategic edge with our PESTLE Analysis of Workday—concise, research-backed insights on political, economic, social, technological, legal, and environmental forces shaping its trajectory; ideal for investors and strategists. Purchase the full report to access detailed risks, opportunities, and actionable recommendations you can use immediately.

Political factors

Data Sovereignty and Localization

As of late 2025, rising data sovereignty laws force Workday to expand regional data centers—raising capex and opex; Workday reported capex of $1.2B in FY2024 and signaled increased infrastructure spend into 2025 to comply with localization in the EU and Southeast Asia. These mandates drive higher per-customer hosting costs, affect cloud scalability, and are critical for retaining government and regulated-industry contracts where noncompliance risks lost revenue and fines.

Geopolitical Trade Tensions

Ongoing trade disputes and geopolitical realignments between major economies, such as US-China tensions and EU-UK post-Brexit rules, are lengthening procurement cycles for multinational Workday clients, with 42% of surveyed global firms in 2024 reporting deferred ERP/HCM purchases due to trade uncertainty. Political instability in regions like the Middle East and parts of Africa has caused implementation delays and demand for localized Workday instances to navigate sanctions and data-residency rules. Workday must stay agile in global strategy to mitigate risks from shifting alliances and rising protectionism, noting that 28% of its 2025 revenue was from EMEA where regulatory fragmentation is increasing.

Public Sector Digital Transformation

Government initiatives to modernize aging administrative systems create a sizable opportunity for Workday: global public sector cloud spend is projected to reach about $95B in 2025, supporting adoption of HCM and financial suites for payroll, procurement and budgeting.

Many countries favor cloud-first policies—over 30 national governments had formal cloud strategies by 2024—driving demand for SaaS HR and finance platforms that improve transparency and cost-efficiency.

Achieving certifications like FedRAMP Moderate/High is politically critical; FedRAMP-authorized vendors capture larger federal contracts, and Workday’s continued certification efforts target a US federal market estimated at $100B+ for IT services.

Global Labor Policy Shifts

Workday's automation of evolving mandates strengthens its competitive edge, reducing compliance costs for clients and supporting recurring subscription revenue (FY2025 revenue $6.3B, growth 11%).

- 20+ countries, 10 US states with pay transparency laws by 2025

- 7,800+ Workday customers (FY2025)

- FY2025 revenue $6.3B, 11% YoY growth

- Compliance automation reduces client risk and switching costs

International Sanctions and Compliance

Workday must enforce rigorous sanctions-compliance frameworks to prevent its SaaS HR and financial systems from being used by prohibited entities, as global sanctions lists grew ~12% in 2023–2025 prompting stricter screening across cloud vendors.

Political shifts can rapidly add jurisdictions or parties to sanctions, forcing immediate customer-screening updates and potential service suspensions that could affect revenue recognition in affected regions.

Maintaining a strong legal and political-risk function is vital to avoid fines and reputational damage; enforcement actions against tech firms have reached multi‑million dollar penalties in recent years.

- Sanctions lists up ~12% (2023–2025)

- Immediate screening updates required after political shifts

- Legal/political-risk teams mitigate multi‑million penalty exposure

Workday faces compliance costs and longer sales cycles but taps $95B public-cloud market

Political risks (data sovereignty, trade tensions, sanctions) raise Workday's compliance capex/opex and lengthen sales cycles, while public-sector cloud spend (~$95B in 2025) and cloud-first policies (30+ governments by 2024) expand opportunity; FY2025 revenue $6.3B, 7,800+ customers; 20+ countries/10 US states with pay-transparency laws drive product compliance demands.

| Metric | Value |

|---|---|

| FY2025 revenue | $6.3B |

| Customers | 7,800+ |

| Public-sector cloud spend 2025 | $95B |

| Pay-transparency jurisdictions | 20+ countries, 10 US states |

What is included in the product

Explores how macro-environmental forces uniquely impact Workday across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and trends to identify risks and opportunities for executives, consultants, and investors.

Condenses Workday's PESTLE insights into a shareable, visually segmented summary that stakeholders can drop into presentations or planning sessions to quickly align on external risks and market positioning.

Economic factors

Corporate IT Spending Trends

The global economic cycle strongly influences corporate IT budgets for ERP and HCM; McKinsey reported 2024 IT spending growth slowed to 3.5% amid tightening corporate balance sheets, prompting delays in large-scale digital transformations. Workday’s subscription model provided revenue resilience, supporting its 2024 ARR growth of about 11% to roughly $7.6 billion. By late 2025 buyers prioritize software delivering rapid ROI via automation and efficiency, with CFOs targeting payback under 18 months on cloud HR/finance investments.

Global Inflation and Interest Rates

Persistent global inflation—consumer price index averaging ~4.5% in 2024 across major markets—raises Workday’s labor and data center costs, squeezing operating margins and increasing talent acquisition expenses.

Rising policy rates (Federal Funds ~5.25% in 2024) lengthen enterprise buying cycles as clients defer capex, slowing new contract closures and subscription upsells.

Workday must calibrate price increases and packaging to protect margin—while noting customers’ cost pressures—to avoid churn and preserve ARR growth.

Currency Exchange Volatility

As a global SaaS provider, Workday faces FX risk that can meaningfully alter reported revenue and operating margin; in FY2024 FX headwinds trimmed cloud subscription revenue growth by about 120–150 basis points versus constant currency.

Strengthening of the US dollar versus the euro, yen, or pound can erode Workday’s price competitiveness abroad and compress local-currency ARR growth; in 2024 the dollar appreciated ~5–6% vs major peers’ markets.

Workday employs forward contracts and other hedges to smooth earnings volatility, but sudden spikes in FX—seen during 2022–2023 market stress—remain a material planning risk for guidance and cash-flow forecasting.

The Subscription Economy Resilience

Workday’s SaaS subscription model captures the market shift to recurring revenue—subscriptions composed 87% of enterprise software revenue growth in 2024—giving predictable ARR (Workday reported $7.9B ARR in fiscal 2025) and steadier cash flows versus perpetual licenses, cushioning minor downturns.

Intense SaaS competition requires ongoing R&D (Workday spent $2.1B on R&D in FY2025) to curb churn and protect valuation amid rivals like Oracle and SAP.

- Subscription-driven ARR: $7.9B (FY2025)

- R&D spend: $2.1B (FY2025)

- Recurring revenue stability vs perpetual licensing

- High competition increases churn risk

Labor Market Tightness and Costs

Rising demand for specialized tech talent has pushed industry salaries up; US median tech wages grew about 6-8% in 2024, increasing Workday’s R&D and sales costs and pressuring operating margins.

Simultaneously, tight labor markets drive customers to spend more on HCM—global HCM software market reached roughly $26.5B in 2024—boosting demand for Workday’s retention and productivity tools.

Workday markets its suite as a solution to talent shortages, emphasizing ROI from reduced turnover and higher workforce productivity to justify customer spend.

- Higher tech wages (+6–8% in 2024) raise Workday’s operating costs

- HCM market ~ $26.5B in 2024, supporting customer investment

- Products positioned to cut turnover and boost productivity, improving customer ROI

Workday logs $7.9B ARR, 11% growth as IT spend slows to ~3.5% in 2024

Macro slowdown cut IT spend growth to ~3.5% in 2024; Workday’s ARR rose to $7.9B (FY2025) with 11% YOY ARR growth in 2024, R&D at $2.1B, FX trimmed subscription growth ~120–150 bps, US tech wages +6–8% (2024), HCM market ~$26.5B (2024), Fed funds ~5.25% (2024) lengthening sales cycles.

| Metric | 2024/25 |

|---|---|

| ARR | $7.9B (FY2025) |

| R&D | $2.1B (FY2025) |

| IT spend growth | ~3.5% (2024) |

| FX drag | 120–150 bps |

What You See Is What You Get

Workday PESTLE Analysis

The preview shown here is the exact Workday PESTLE Analysis document you’ll receive after purchase—fully formatted, professional, and ready to use.

The content, layout, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of Workday—concise, research-backed insights on political, economic, social, technological, legal, and environmental forces shaping its trajectory; ideal for investors and strategists. Purchase the full report to access detailed risks, opportunities, and actionable recommendations you can use immediately.

Political factors

Data Sovereignty and Localization

As of late 2025, rising data sovereignty laws force Workday to expand regional data centers—raising capex and opex; Workday reported capex of $1.2B in FY2024 and signaled increased infrastructure spend into 2025 to comply with localization in the EU and Southeast Asia. These mandates drive higher per-customer hosting costs, affect cloud scalability, and are critical for retaining government and regulated-industry contracts where noncompliance risks lost revenue and fines.

Geopolitical Trade Tensions

Ongoing trade disputes and geopolitical realignments between major economies, such as US-China tensions and EU-UK post-Brexit rules, are lengthening procurement cycles for multinational Workday clients, with 42% of surveyed global firms in 2024 reporting deferred ERP/HCM purchases due to trade uncertainty. Political instability in regions like the Middle East and parts of Africa has caused implementation delays and demand for localized Workday instances to navigate sanctions and data-residency rules. Workday must stay agile in global strategy to mitigate risks from shifting alliances and rising protectionism, noting that 28% of its 2025 revenue was from EMEA where regulatory fragmentation is increasing.

Public Sector Digital Transformation

Government initiatives to modernize aging administrative systems create a sizable opportunity for Workday: global public sector cloud spend is projected to reach about $95B in 2025, supporting adoption of HCM and financial suites for payroll, procurement and budgeting.

Many countries favor cloud-first policies—over 30 national governments had formal cloud strategies by 2024—driving demand for SaaS HR and finance platforms that improve transparency and cost-efficiency.

Achieving certifications like FedRAMP Moderate/High is politically critical; FedRAMP-authorized vendors capture larger federal contracts, and Workday’s continued certification efforts target a US federal market estimated at $100B+ for IT services.

Global Labor Policy Shifts

Workday's automation of evolving mandates strengthens its competitive edge, reducing compliance costs for clients and supporting recurring subscription revenue (FY2025 revenue $6.3B, growth 11%).

- 20+ countries, 10 US states with pay transparency laws by 2025

- 7,800+ Workday customers (FY2025)

- FY2025 revenue $6.3B, 11% YoY growth

- Compliance automation reduces client risk and switching costs

International Sanctions and Compliance

Workday must enforce rigorous sanctions-compliance frameworks to prevent its SaaS HR and financial systems from being used by prohibited entities, as global sanctions lists grew ~12% in 2023–2025 prompting stricter screening across cloud vendors.

Political shifts can rapidly add jurisdictions or parties to sanctions, forcing immediate customer-screening updates and potential service suspensions that could affect revenue recognition in affected regions.

Maintaining a strong legal and political-risk function is vital to avoid fines and reputational damage; enforcement actions against tech firms have reached multi‑million dollar penalties in recent years.

- Sanctions lists up ~12% (2023–2025)

- Immediate screening updates required after political shifts

- Legal/political-risk teams mitigate multi‑million penalty exposure

Workday faces compliance costs and longer sales cycles but taps $95B public-cloud market

Political risks (data sovereignty, trade tensions, sanctions) raise Workday's compliance capex/opex and lengthen sales cycles, while public-sector cloud spend (~$95B in 2025) and cloud-first policies (30+ governments by 2024) expand opportunity; FY2025 revenue $6.3B, 7,800+ customers; 20+ countries/10 US states with pay-transparency laws drive product compliance demands.

| Metric | Value |

|---|---|

| FY2025 revenue | $6.3B |

| Customers | 7,800+ |

| Public-sector cloud spend 2025 | $95B |

| Pay-transparency jurisdictions | 20+ countries, 10 US states |

What is included in the product

Explores how macro-environmental forces uniquely impact Workday across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current data and trends to identify risks and opportunities for executives, consultants, and investors.

Condenses Workday's PESTLE insights into a shareable, visually segmented summary that stakeholders can drop into presentations or planning sessions to quickly align on external risks and market positioning.

Economic factors

Corporate IT Spending Trends

The global economic cycle strongly influences corporate IT budgets for ERP and HCM; McKinsey reported 2024 IT spending growth slowed to 3.5% amid tightening corporate balance sheets, prompting delays in large-scale digital transformations. Workday’s subscription model provided revenue resilience, supporting its 2024 ARR growth of about 11% to roughly $7.6 billion. By late 2025 buyers prioritize software delivering rapid ROI via automation and efficiency, with CFOs targeting payback under 18 months on cloud HR/finance investments.

Global Inflation and Interest Rates

Persistent global inflation—consumer price index averaging ~4.5% in 2024 across major markets—raises Workday’s labor and data center costs, squeezing operating margins and increasing talent acquisition expenses.

Rising policy rates (Federal Funds ~5.25% in 2024) lengthen enterprise buying cycles as clients defer capex, slowing new contract closures and subscription upsells.

Workday must calibrate price increases and packaging to protect margin—while noting customers’ cost pressures—to avoid churn and preserve ARR growth.

Currency Exchange Volatility

As a global SaaS provider, Workday faces FX risk that can meaningfully alter reported revenue and operating margin; in FY2024 FX headwinds trimmed cloud subscription revenue growth by about 120–150 basis points versus constant currency.

Strengthening of the US dollar versus the euro, yen, or pound can erode Workday’s price competitiveness abroad and compress local-currency ARR growth; in 2024 the dollar appreciated ~5–6% vs major peers’ markets.

Workday employs forward contracts and other hedges to smooth earnings volatility, but sudden spikes in FX—seen during 2022–2023 market stress—remain a material planning risk for guidance and cash-flow forecasting.

The Subscription Economy Resilience

Workday’s SaaS subscription model captures the market shift to recurring revenue—subscriptions composed 87% of enterprise software revenue growth in 2024—giving predictable ARR (Workday reported $7.9B ARR in fiscal 2025) and steadier cash flows versus perpetual licenses, cushioning minor downturns.

Intense SaaS competition requires ongoing R&D (Workday spent $2.1B on R&D in FY2025) to curb churn and protect valuation amid rivals like Oracle and SAP.

- Subscription-driven ARR: $7.9B (FY2025)

- R&D spend: $2.1B (FY2025)

- Recurring revenue stability vs perpetual licensing

- High competition increases churn risk

Labor Market Tightness and Costs

Rising demand for specialized tech talent has pushed industry salaries up; US median tech wages grew about 6-8% in 2024, increasing Workday’s R&D and sales costs and pressuring operating margins.

Simultaneously, tight labor markets drive customers to spend more on HCM—global HCM software market reached roughly $26.5B in 2024—boosting demand for Workday’s retention and productivity tools.

Workday markets its suite as a solution to talent shortages, emphasizing ROI from reduced turnover and higher workforce productivity to justify customer spend.

- Higher tech wages (+6–8% in 2024) raise Workday’s operating costs

- HCM market ~ $26.5B in 2024, supporting customer investment

- Products positioned to cut turnover and boost productivity, improving customer ROI

Workday logs $7.9B ARR, 11% growth as IT spend slows to ~3.5% in 2024

Macro slowdown cut IT spend growth to ~3.5% in 2024; Workday’s ARR rose to $7.9B (FY2025) with 11% YOY ARR growth in 2024, R&D at $2.1B, FX trimmed subscription growth ~120–150 bps, US tech wages +6–8% (2024), HCM market ~$26.5B (2024), Fed funds ~5.25% (2024) lengthening sales cycles.

| Metric | 2024/25 |

|---|---|

| ARR | $7.9B (FY2025) |

| R&D | $2.1B (FY2025) |

| IT spend growth | ~3.5% (2024) |

| FX drag | 120–150 bps |

What You See Is What You Get

Workday PESTLE Analysis

The preview shown here is the exact Workday PESTLE Analysis document you’ll receive after purchase—fully formatted, professional, and ready to use.

The content, layout, and structure visible in this preview are identical to the downloadable file you’ll get immediately after checkout.