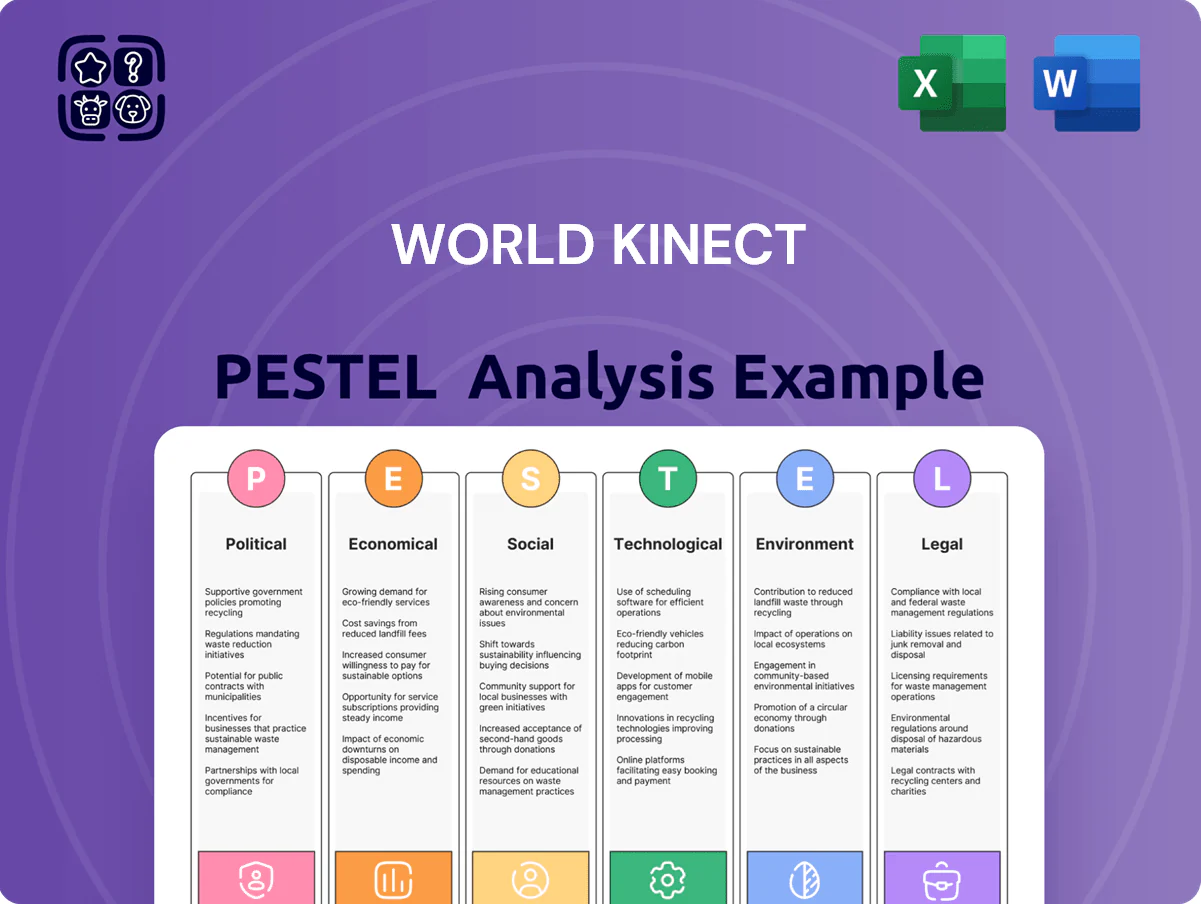

World Kinect PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political, economic, and technological forces are shaping World Kinect’s strategic trajectory with our concise PESTLE brief—ideal for investors and strategists seeking actionable context. Purchase the full PESTLE to get a detailed, ready-to-use report with risk forecasts, opportunity maps, and editable charts for immediate decision-making.

Political factors

Geopolitical instability affecting energy supply chains

Ongoing conflicts in key energy-producing regions through late 2025 have reduced spot tanker availability by about 12% and pushed average jet fuel FOB premiums up roughly 18%, disrupting global distribution networks.

World Kinect faces volatile trade routes and sanctions risk—over 30% of its 2024 marine fuel volumes transited high-risk corridors—necessitating contingency logistics and compliance costs that strain margins.

To mitigate regional political upheaval, World Kinect needs diversified sourcing: increasing purchases from low-risk suppliers could cut supply disruption exposure by an estimated 40% and stabilize procurement costs.

Governmental mandates for decarbonization

Trade policies and protectionism

Shifting trade agreements and new tariffs on energy—EU carbon border adjustments and recent US tariffs proposals—can raise cross‑border fuel logistics costs by an estimated 3–7%, squeezing World Kinect’s margins on international fuel trading.

As a global intermediary handling >200 million gallons monthly, World Kinect is exposed to disrupted supply chains if EU‑US trade tensions or regional protectionism impede seamless fuel movement across borders.

Strategic planning should model tariff shocks and non‑tariff barriers in key markets—EU and North America—using scenario analyses given 2024–2025 volatility in energy trade flows and tariff policy shifts.

Energy security and sovereignty initiatives

- Rising energy sovereignty reduces import volumes for brokers

- Local supplier preference pressures international margins

- Strengthen partnerships and domestic supply to protect market share

Regulatory lobbying and industry influence

World Kinect leverages political engagement and participation in trade associations to influence energy transition policies, aiming to shape realistic timelines and secure infrastructure funding that protect its $12.7B global fuel and services revenue (2024) while enabling renewables growth.

By advocating for grid upgrades and CCS support, the company reduces operational disruption risk; tracking over 1,200 energy-related bills in the US and EU helps anticipate constraints and market openings.

- Advocacy targets pragmatic timelines to balance legacy fuel margins and renewables investment

- Seeks infrastructure funding (grid, storage, CCS) to de-risk transition

- Monitors ~1,200 legislative items to forecast regulatory impact

Geopolitical shocks cut tankers, spike jet premiums—diversify to shield WWII revenue

Political risks (2024–25) cut tanker availability ~12%, raised jet fuel FOB premiums ~18%, and exposed >30% of World Kinect's marine volumes to high‑risk corridors; diversification could lower disruption exposure ~40% while tariff shocks (CBAM, US proposals) may add 3–7% to logistics costs. Net‑zero commitments (132 countries, ~90% GDP) and $7.5B SAF/$4B hydrogen incentives force capital reallocation from legacy fuels to SAF/hydrogen to protect $12.7B 2024 revenue.

| Metric | 2024/2025 |

|---|---|

| Tanker availability impact | -12% |

| Jet fuel FOB premium rise | +18% |

| Marine volumes via high‑risk corridors | 30%+ |

| Net‑zero countries | 132 (90% GDP) |

| SAF incentives | $7.5B |

| World Kinect revenue (2024) | $12.7B |

What is included in the product

Explores how macro-environmental forces uniquely impact World Kinect across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends, forward-looking insights, and sector-specific examples to help executives, consultants, and entrepreneurs identify opportunities, mitigate risks, and align strategy with actual market and regulatory dynamics.

Condenses World Kinect's PESTLE into a clean, shareable summary that teams can drop into presentations or planning packs for quick alignment on external risks and market positioning.

Economic factors

Volatility in global oil and gas prices

Fluctuations in benchmark crude, with Brent averaging ~$85/bbl in 2025 vs $78/bbl in 2024, directly pressure revenue and margins for energy management firms through cost-pass-through and contract adjustments.

Price sensitivity remains high at end-2025 as emerging-market demand grew 3.6% y/y while OPEC+ measured cuts tightened supply, raising volatility.

World Kinect employs forward hedges and swaps covering ~40% of client exposure to cap downside and stabilize fees against extreme swings.

Global inflationary pressures and interest rates

Persistently high global interest rates—with the US Fed funds rate at 5.25–5.50% in 2024 and BBB corporate yields around 5.5%—raise World Kinect’s cost of capital for energy infrastructure and inventory financing, squeezing project NPV and extending payback periods. Inflation at ~3.4% globally in 2024 has lifted logistics and transportation costs, pushing fuel and labor expenses higher and demanding tighter cost controls. The company must balance existing debt servicing—total debt reported at $3.2bn in 2024—against necessary capex, where higher borrowing costs may defer expansion or require alternate financing.

Economic growth rates in aviation and shipping

The demand for World Kinect’s services tracks global travel and trade: IATA projected 2024 passenger traffic at 92% of 2019 levels and UNCTAD reported 2024 global merchandise trade growth of 1.5%, so weak growth in 2024–25 in major economies cut flight frequencies and port volumes, reducing jet and marine fuel demand. Strong tourism rebound (WTTC: global travel GDP +59% vs 2020 by 2024) and rising container throughput (UNCTAD: 2023 volumes +2.8%) support fuel sales.

Currency exchange rate fluctuations

Operating in over 200 countries exposes World Kinect to material FX risk; in 2024, currency moves (USD vs EUR, BRL, INR) contributed to a reported 3–5% swing in regional revenue translation for many energy traders.

Energy commodities priced in USD mean local-currency declines erode client purchasing power—e.g., a 10% depreciation of BRL vs USD in 2023 raised fuel import costs by roughly 10% for Brazilian buyers.

Effective treasury management and hedging—forward contracts, options, and netting—are essential; industry peers report hedging can reduce earnings volatility by up to 60% annually.

- Exposure: 200+ countries; FX-driven revenue swings ~3–5%

- USD pricing: local depreciations directly raise client costs (example BRL 10% → ~10% cost increase)

- Mitigation: hedging/treasury can cut volatility up to ~60%

Shift toward service-based energy models

Market demand is shifting to Energy-as-a-Service, with EaaS projected to grow at ~24% CAGR to $220B by 2028, pushing clients to pay for performance over volume; World Kinect must evolve from commodity sales to integrated solutions to capture higher-margin contracts.

This pivot can boost EBIT margins by 200–400 basis points versus commodity supply but requires upfront investment in advisory, asset management, and digital platforms—estimated CAPEX/OPEX increase of 5–8% of revenue over 3 years for capability buildout.

- EaaS market ~24% CAGR to $220B (2028)

- Potential margin uplift 200–400 bps

- Required investment ~5–8% revenue over 3 years

Energy & EaaS: Rising costs, FX risks, but 24% EaaS growth fuels margin upside

Economic headwinds—Brent ~$85/bbl (2025e) vs $78 (2024), global inflation ~3.4% (2024), Fed funds 5.25–5.50%—raise costs and capex financing needs; FX volatility (200+ countries) causes ~3–5% revenue translation swings; EaaS growth (~24% CAGR to $220B by 2028) offers 200–400bps margin upside but needs 5–8% revenue investment.

| Metric | Value |

|---|---|

| Brent (2025e) | $85/bbl |

| Inflation (2024) | 3.4% |

| Fed funds | 5.25–5.50% |

| FX swing | 3–5% |

| EaaS CAGR | 24% to $220B (2028) |

Preview Before You Purchase

World Kinect PESTLE Analysis

The preview shown here is the exact World Kinect PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in the preview are identical to the file you’ll instantly download after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock how political, economic, and technological forces are shaping World Kinect’s strategic trajectory with our concise PESTLE brief—ideal for investors and strategists seeking actionable context. Purchase the full PESTLE to get a detailed, ready-to-use report with risk forecasts, opportunity maps, and editable charts for immediate decision-making.

Political factors

Geopolitical instability affecting energy supply chains

Ongoing conflicts in key energy-producing regions through late 2025 have reduced spot tanker availability by about 12% and pushed average jet fuel FOB premiums up roughly 18%, disrupting global distribution networks.

World Kinect faces volatile trade routes and sanctions risk—over 30% of its 2024 marine fuel volumes transited high-risk corridors—necessitating contingency logistics and compliance costs that strain margins.

To mitigate regional political upheaval, World Kinect needs diversified sourcing: increasing purchases from low-risk suppliers could cut supply disruption exposure by an estimated 40% and stabilize procurement costs.

Governmental mandates for decarbonization

Trade policies and protectionism

Shifting trade agreements and new tariffs on energy—EU carbon border adjustments and recent US tariffs proposals—can raise cross‑border fuel logistics costs by an estimated 3–7%, squeezing World Kinect’s margins on international fuel trading.

As a global intermediary handling >200 million gallons monthly, World Kinect is exposed to disrupted supply chains if EU‑US trade tensions or regional protectionism impede seamless fuel movement across borders.

Strategic planning should model tariff shocks and non‑tariff barriers in key markets—EU and North America—using scenario analyses given 2024–2025 volatility in energy trade flows and tariff policy shifts.

Energy security and sovereignty initiatives

- Rising energy sovereignty reduces import volumes for brokers

- Local supplier preference pressures international margins

- Strengthen partnerships and domestic supply to protect market share

Regulatory lobbying and industry influence

World Kinect leverages political engagement and participation in trade associations to influence energy transition policies, aiming to shape realistic timelines and secure infrastructure funding that protect its $12.7B global fuel and services revenue (2024) while enabling renewables growth.

By advocating for grid upgrades and CCS support, the company reduces operational disruption risk; tracking over 1,200 energy-related bills in the US and EU helps anticipate constraints and market openings.

- Advocacy targets pragmatic timelines to balance legacy fuel margins and renewables investment

- Seeks infrastructure funding (grid, storage, CCS) to de-risk transition

- Monitors ~1,200 legislative items to forecast regulatory impact

Geopolitical shocks cut tankers, spike jet premiums—diversify to shield WWII revenue

Political risks (2024–25) cut tanker availability ~12%, raised jet fuel FOB premiums ~18%, and exposed >30% of World Kinect's marine volumes to high‑risk corridors; diversification could lower disruption exposure ~40% while tariff shocks (CBAM, US proposals) may add 3–7% to logistics costs. Net‑zero commitments (132 countries, ~90% GDP) and $7.5B SAF/$4B hydrogen incentives force capital reallocation from legacy fuels to SAF/hydrogen to protect $12.7B 2024 revenue.

| Metric | 2024/2025 |

|---|---|

| Tanker availability impact | -12% |

| Jet fuel FOB premium rise | +18% |

| Marine volumes via high‑risk corridors | 30%+ |

| Net‑zero countries | 132 (90% GDP) |

| SAF incentives | $7.5B |

| World Kinect revenue (2024) | $12.7B |

What is included in the product

Explores how macro-environmental forces uniquely impact World Kinect across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends, forward-looking insights, and sector-specific examples to help executives, consultants, and entrepreneurs identify opportunities, mitigate risks, and align strategy with actual market and regulatory dynamics.

Condenses World Kinect's PESTLE into a clean, shareable summary that teams can drop into presentations or planning packs for quick alignment on external risks and market positioning.

Economic factors

Volatility in global oil and gas prices

Fluctuations in benchmark crude, with Brent averaging ~$85/bbl in 2025 vs $78/bbl in 2024, directly pressure revenue and margins for energy management firms through cost-pass-through and contract adjustments.

Price sensitivity remains high at end-2025 as emerging-market demand grew 3.6% y/y while OPEC+ measured cuts tightened supply, raising volatility.

World Kinect employs forward hedges and swaps covering ~40% of client exposure to cap downside and stabilize fees against extreme swings.

Global inflationary pressures and interest rates

Persistently high global interest rates—with the US Fed funds rate at 5.25–5.50% in 2024 and BBB corporate yields around 5.5%—raise World Kinect’s cost of capital for energy infrastructure and inventory financing, squeezing project NPV and extending payback periods. Inflation at ~3.4% globally in 2024 has lifted logistics and transportation costs, pushing fuel and labor expenses higher and demanding tighter cost controls. The company must balance existing debt servicing—total debt reported at $3.2bn in 2024—against necessary capex, where higher borrowing costs may defer expansion or require alternate financing.

Economic growth rates in aviation and shipping

The demand for World Kinect’s services tracks global travel and trade: IATA projected 2024 passenger traffic at 92% of 2019 levels and UNCTAD reported 2024 global merchandise trade growth of 1.5%, so weak growth in 2024–25 in major economies cut flight frequencies and port volumes, reducing jet and marine fuel demand. Strong tourism rebound (WTTC: global travel GDP +59% vs 2020 by 2024) and rising container throughput (UNCTAD: 2023 volumes +2.8%) support fuel sales.

Currency exchange rate fluctuations

Operating in over 200 countries exposes World Kinect to material FX risk; in 2024, currency moves (USD vs EUR, BRL, INR) contributed to a reported 3–5% swing in regional revenue translation for many energy traders.

Energy commodities priced in USD mean local-currency declines erode client purchasing power—e.g., a 10% depreciation of BRL vs USD in 2023 raised fuel import costs by roughly 10% for Brazilian buyers.

Effective treasury management and hedging—forward contracts, options, and netting—are essential; industry peers report hedging can reduce earnings volatility by up to 60% annually.

- Exposure: 200+ countries; FX-driven revenue swings ~3–5%

- USD pricing: local depreciations directly raise client costs (example BRL 10% → ~10% cost increase)

- Mitigation: hedging/treasury can cut volatility up to ~60%

Shift toward service-based energy models

Market demand is shifting to Energy-as-a-Service, with EaaS projected to grow at ~24% CAGR to $220B by 2028, pushing clients to pay for performance over volume; World Kinect must evolve from commodity sales to integrated solutions to capture higher-margin contracts.

This pivot can boost EBIT margins by 200–400 basis points versus commodity supply but requires upfront investment in advisory, asset management, and digital platforms—estimated CAPEX/OPEX increase of 5–8% of revenue over 3 years for capability buildout.

- EaaS market ~24% CAGR to $220B (2028)

- Potential margin uplift 200–400 bps

- Required investment ~5–8% revenue over 3 years

Energy & EaaS: Rising costs, FX risks, but 24% EaaS growth fuels margin upside

Economic headwinds—Brent ~$85/bbl (2025e) vs $78 (2024), global inflation ~3.4% (2024), Fed funds 5.25–5.50%—raise costs and capex financing needs; FX volatility (200+ countries) causes ~3–5% revenue translation swings; EaaS growth (~24% CAGR to $220B by 2028) offers 200–400bps margin upside but needs 5–8% revenue investment.

| Metric | Value |

|---|---|

| Brent (2025e) | $85/bbl |

| Inflation (2024) | 3.4% |

| Fed funds | 5.25–5.50% |

| FX swing | 3–5% |

| EaaS CAGR | 24% to $220B (2028) |

Preview Before You Purchase

World Kinect PESTLE Analysis

The preview shown here is the exact World Kinect PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in the preview are identical to the file you’ll instantly download after payment.