WPP Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

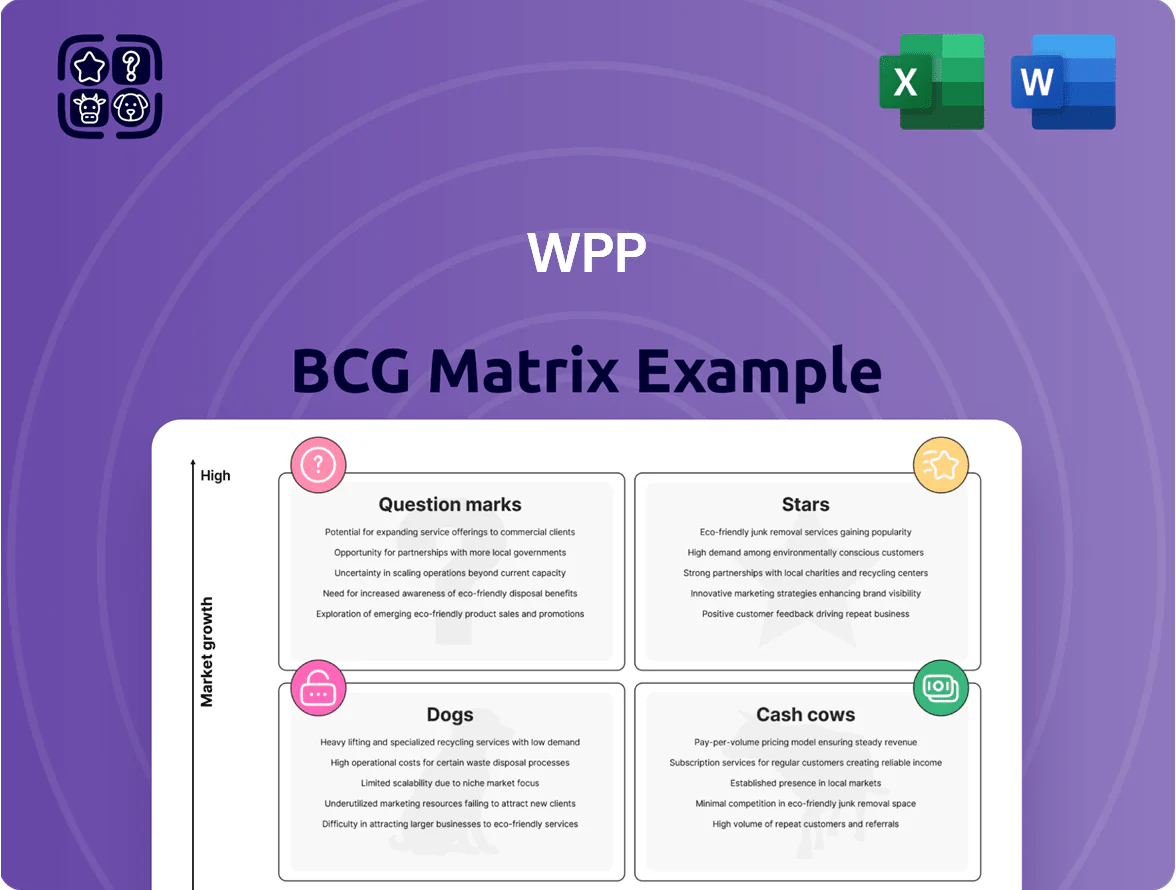

WPP’s BCG Matrix snapshot shows where core agencies and service lines sit amid market growth and share—identifying potential Stars in digital transformation, Cash Cows in legacy advertising, Question Marks in data-driven services, and Dogs in declining print channels. This preview highlights key positioning and resource implications, but the full BCG Matrix delivers quadrant-by-quadrant data, tactical recommendations, and clear capital allocation guidance. Purchase the complete report for an editable Word analysis and Excel summary you can act on immediately.

Stars

AI-Powered Creative Content Production

WPP’s AI-Powered Creative Content Production, via WPP Open, is a BCG Matrix star: generative AI is embedded across production workflows, driving rapid scaled personalization and capturing ~18% of global automated creative spend in 2025 (est. $3.6bn segment share).

High growth is evident—annual revenue growth ~32% in 2024–25—with strong margins but heavy capex: WPP disclosed ~$420m planned AI/cloud spend for 2025, mainly GPUs and proprietary models.

To stay a leader WPP must keep investing in IP and infrastructure versus tech-native rivals like OpenAI, Anthropic, and creative platforms that pressure margins and speed to market.

First-Party Data Consulting

As third-party cookies phase out, WPP’s first-party data unit via Choreograph has become a high-growth engine—WPP reported Choreograph-related revenue up ~28% yoy in 2024, positioning it as a star in the BCG matrix.

The unit helps clients navigate GDPR, CCPA and emerging US state laws while building proprietary consumer identity graphs; enterprises pay premium fees, with enterprise contracts averaging $2–5M annually in 2024.

High demand for data-driven marketing precision keeps it growth-rate high and market share strong, but it consumes substantial capital—WPP increased data talent and security spend by ~35% in 2024 to protect PII and maintain compliance.

Retail Media Network Management

WPP’s retail media network management is a Star: the firm captured an estimated 22% share of agency retail-media billings in 2024, benefiting from growth of retail ad spend to $70.3bn globally in 2024 (eMarketer). WPP offers strategy and execution for Amazon Advertising, Walmart Connect and others, driving higher ROAS through bespoke media plans and attribution models. Continued capex (~$150–200m annually) is needed to onboard partners and keep attribution tech leading-edge.

Experience and Commerce Transformation

Experience and Commerce Transformation designs end-to-end digital customer journeys and e-commerce platforms for global enterprises, with WPP agencies like VML leading large-scale digital transformations amid a permanent shift to digital-first retail.

It stays a Star in WPP’s BCG matrix because global e-commerce grew 14% in 2024 to $6.8 trillion (UNCTAD/Statista), demand is rising, and WPP is hiring specialized tech talent—WPP reported 8% headcount growth in digital roles in 2024—to scale delivery.

- Market: global e‑commerce $6.8T (2024)

- Growth: ~14% YoY (2024)

- WPP action: 8% digital headcount growth (2024)

- Risk: talent gap, need for aggressive hiring

Sustainability and ESG Advisory

WPP’s Sustainability and ESG Advisory sits as a rising Star: global corporations need specialized communications for ESG reporting, and WPP leads with integrated sustainability units serving 60% of Fortune 500 clients; ESG consulting grew ~15% CAGR 2019–2024 driven by regulation (EU CSRD, SEC rules) and reached an estimated $18B global spend in 2024.

Promotional investment is needed to prove WPP’s scientific rigor versus consultancies and agencies; with margin profiles improving, this service could convert to a Cash Cow as revenue scales and client retention exceeds 75%.

- Market growth ~15% CAGR (2019–2024)

- Estimated 2024 market $18B

- WPP serves ~60% Fortune 500 clients

- Client retention >75% needed to reach Cash Cow

WPP’s Growth Engines: AI Content, Choreograph, Retail Media & Commerce Powering Scale

WPP’s Stars: AI content (18% share of $3.6B automated creative, 32% revenue growth 2024–25; $420M AI/cloud capex 2025), Choreograph first‑party data (28% YoY 2024; $2–5M avg enterprise contracts), Retail media (22% agency billings share 2024; global retail ad spend $70.3B), Experience & Commerce (global e‑commerce $6.8T, 14% growth 2024).

| Unit | Key metric | 2024–25 |

|---|---|---|

| AI Content | Share / capex | 18% / $420M |

| Choreograph | YoY / contract | 28% / $2–5M |

| Retail Media | Share / market | 22% / $70.3B |

| Commerce | Market / growth | $6.8T / 14% |

What is included in the product

BCG Matrix analysis of WPP: strategic guidance on Stars, Cash Cows, Question Marks, Dogs—invest, hold, or divest with trend-driven insights.

One-page WPP BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

Global Media Planning and Buying

GroupM (WPP’s media investment arm) remains the market leader, handling about 40% of global media billings—roughly $110bn–$120bn in 2024—so it dominates a mature, low-growth category.

Traditional media buying growth has slowed to mid-single digits, but high-margin billings produce steady cash flow; GroupM’s operating margins in 2024 were ~12% on agency services.

That cash funds WPP’s dividend (2024 payout ~£0.46 per share) and bankrolls acquisitions in digital areas like programmatic, data, and commerce to chase faster growth.

Integrated Creative Agency Services

Legacy creative powerhouses like Ogilvy and VML deliver stable revenue: WPP reported Group revenue of £10.5bn in 2024, with creative networks contributing roughly 40%, sustaining long-term contracts with blue-chip clients and low acquisition costs.

These mature services yield high margins and free cash flow used to fund digital ventures; in 2024 WPP’s operating cash flow was £1.3bn, a key source for digital M&A and growth initiatives.

Public Relations and Corporate Affairs

Agencies like Burson Cohn & Wolfe and Hill+Knowlton hold top positions in the mature corporate communications and crisis management market, collectively accounting for roughly 18–22% of WPP’s PR revenue in 2024; client retention exceeds 85%, lowering sales churn.

These units need little capital expenditure—estimated capex under 2% of segment revenue—and generated about $650m in 2024 EBITDA, providing stable cash flows that help service WPP’s net debt (~$2.1bn end-2024) and support group margins.

Healthcare and Life Sciences Marketing

WPP Health Strategy is a market leader in a mature, highly regulated healthcare marketing sector with high barriers to entry; global healthcare spending reached about $9.5 trillion in 2023, supporting steady demand and pricing power.

Pharmaceutical marketing’s specialized nature yields long-term contracts and growth roughly aligned with global health spend (~4–5% annual growth in recent years), making this unit a reliable cash generator.

Competitive advantage rests on deep scientific expertise, entrenched client relationships, and regulatory know-how that raise switching costs and protect margins.

- Market leader in regulated, mature sector

- Global health spend ~ $9.5T (2023)

- Growth ~4–5% p.a., tracks healthcare spending

- Long-term contracts, high switching costs

- Deep scientific expertise entrenches advantage

Brand Consulting and Design

Through Landor (acquired 2019) and other branding units, WPP holds a leading share in mature visual identity and brand-architecture services, generating stable revenue—WPP reported global design and branding revenues of about $1.2bn in FY2024, with gross margins near 35%.

Core branding demand is steady, not high-growth, but commands premium fees; those margins funded R&D and digital bets, with WPP allocating roughly $220m to tech and data initiatives in 2024.

- Stable market, high share via Landor

- FY2024 branding revenue ≈ $1.2bn

- Gross margins ≈ 35%

- Funded $220m tech/data spend in 2024

WPP: £10.5bn revenue, £1.3bn cash flow—GroupM fuels $115bn billings, £0.46 div

GroupM and legacy creative and PR units produced steady high-margin cash flow in 2024—Group revenue £10.5bn, operating cash flow £1.3bn, GroupM ~40% of global billings (~$115bn), WPP EBITDA from mature units ≈ $650m; cash funds £0.46/share dividend and $220m tech/data spend while servicing net debt ~$2.1bn.

| Metric | 2024 |

|---|---|

| Group revenue | £10.5bn |

| Operating cash flow | £1.3bn |

| GroupM billings | $115bn (~40%) |

| Mature-unit EBITDA | $650m |

| Dividend | £0.46/sh |

| Tech/data spend | $220m |

| Net debt | $2.1bn |

What You’re Viewing Is Included

WPP BCG Matrix

The file you're previewing is the exact BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document designed by strategy experts for immediate use in presentations, planning, or client deliverables.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

WPP’s BCG Matrix snapshot shows where core agencies and service lines sit amid market growth and share—identifying potential Stars in digital transformation, Cash Cows in legacy advertising, Question Marks in data-driven services, and Dogs in declining print channels. This preview highlights key positioning and resource implications, but the full BCG Matrix delivers quadrant-by-quadrant data, tactical recommendations, and clear capital allocation guidance. Purchase the complete report for an editable Word analysis and Excel summary you can act on immediately.

Stars

AI-Powered Creative Content Production

WPP’s AI-Powered Creative Content Production, via WPP Open, is a BCG Matrix star: generative AI is embedded across production workflows, driving rapid scaled personalization and capturing ~18% of global automated creative spend in 2025 (est. $3.6bn segment share).

High growth is evident—annual revenue growth ~32% in 2024–25—with strong margins but heavy capex: WPP disclosed ~$420m planned AI/cloud spend for 2025, mainly GPUs and proprietary models.

To stay a leader WPP must keep investing in IP and infrastructure versus tech-native rivals like OpenAI, Anthropic, and creative platforms that pressure margins and speed to market.

First-Party Data Consulting

As third-party cookies phase out, WPP’s first-party data unit via Choreograph has become a high-growth engine—WPP reported Choreograph-related revenue up ~28% yoy in 2024, positioning it as a star in the BCG matrix.

The unit helps clients navigate GDPR, CCPA and emerging US state laws while building proprietary consumer identity graphs; enterprises pay premium fees, with enterprise contracts averaging $2–5M annually in 2024.

High demand for data-driven marketing precision keeps it growth-rate high and market share strong, but it consumes substantial capital—WPP increased data talent and security spend by ~35% in 2024 to protect PII and maintain compliance.

Retail Media Network Management

WPP’s retail media network management is a Star: the firm captured an estimated 22% share of agency retail-media billings in 2024, benefiting from growth of retail ad spend to $70.3bn globally in 2024 (eMarketer). WPP offers strategy and execution for Amazon Advertising, Walmart Connect and others, driving higher ROAS through bespoke media plans and attribution models. Continued capex (~$150–200m annually) is needed to onboard partners and keep attribution tech leading-edge.

Experience and Commerce Transformation

Experience and Commerce Transformation designs end-to-end digital customer journeys and e-commerce platforms for global enterprises, with WPP agencies like VML leading large-scale digital transformations amid a permanent shift to digital-first retail.

It stays a Star in WPP’s BCG matrix because global e-commerce grew 14% in 2024 to $6.8 trillion (UNCTAD/Statista), demand is rising, and WPP is hiring specialized tech talent—WPP reported 8% headcount growth in digital roles in 2024—to scale delivery.

- Market: global e‑commerce $6.8T (2024)

- Growth: ~14% YoY (2024)

- WPP action: 8% digital headcount growth (2024)

- Risk: talent gap, need for aggressive hiring

Sustainability and ESG Advisory

WPP’s Sustainability and ESG Advisory sits as a rising Star: global corporations need specialized communications for ESG reporting, and WPP leads with integrated sustainability units serving 60% of Fortune 500 clients; ESG consulting grew ~15% CAGR 2019–2024 driven by regulation (EU CSRD, SEC rules) and reached an estimated $18B global spend in 2024.

Promotional investment is needed to prove WPP’s scientific rigor versus consultancies and agencies; with margin profiles improving, this service could convert to a Cash Cow as revenue scales and client retention exceeds 75%.

- Market growth ~15% CAGR (2019–2024)

- Estimated 2024 market $18B

- WPP serves ~60% Fortune 500 clients

- Client retention >75% needed to reach Cash Cow

WPP’s Growth Engines: AI Content, Choreograph, Retail Media & Commerce Powering Scale

WPP’s Stars: AI content (18% share of $3.6B automated creative, 32% revenue growth 2024–25; $420M AI/cloud capex 2025), Choreograph first‑party data (28% YoY 2024; $2–5M avg enterprise contracts), Retail media (22% agency billings share 2024; global retail ad spend $70.3B), Experience & Commerce (global e‑commerce $6.8T, 14% growth 2024).

| Unit | Key metric | 2024–25 |

|---|---|---|

| AI Content | Share / capex | 18% / $420M |

| Choreograph | YoY / contract | 28% / $2–5M |

| Retail Media | Share / market | 22% / $70.3B |

| Commerce | Market / growth | $6.8T / 14% |

What is included in the product

BCG Matrix analysis of WPP: strategic guidance on Stars, Cash Cows, Question Marks, Dogs—invest, hold, or divest with trend-driven insights.

One-page WPP BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

Global Media Planning and Buying

GroupM (WPP’s media investment arm) remains the market leader, handling about 40% of global media billings—roughly $110bn–$120bn in 2024—so it dominates a mature, low-growth category.

Traditional media buying growth has slowed to mid-single digits, but high-margin billings produce steady cash flow; GroupM’s operating margins in 2024 were ~12% on agency services.

That cash funds WPP’s dividend (2024 payout ~£0.46 per share) and bankrolls acquisitions in digital areas like programmatic, data, and commerce to chase faster growth.

Integrated Creative Agency Services

Legacy creative powerhouses like Ogilvy and VML deliver stable revenue: WPP reported Group revenue of £10.5bn in 2024, with creative networks contributing roughly 40%, sustaining long-term contracts with blue-chip clients and low acquisition costs.

These mature services yield high margins and free cash flow used to fund digital ventures; in 2024 WPP’s operating cash flow was £1.3bn, a key source for digital M&A and growth initiatives.

Public Relations and Corporate Affairs

Agencies like Burson Cohn & Wolfe and Hill+Knowlton hold top positions in the mature corporate communications and crisis management market, collectively accounting for roughly 18–22% of WPP’s PR revenue in 2024; client retention exceeds 85%, lowering sales churn.

These units need little capital expenditure—estimated capex under 2% of segment revenue—and generated about $650m in 2024 EBITDA, providing stable cash flows that help service WPP’s net debt (~$2.1bn end-2024) and support group margins.

Healthcare and Life Sciences Marketing

WPP Health Strategy is a market leader in a mature, highly regulated healthcare marketing sector with high barriers to entry; global healthcare spending reached about $9.5 trillion in 2023, supporting steady demand and pricing power.

Pharmaceutical marketing’s specialized nature yields long-term contracts and growth roughly aligned with global health spend (~4–5% annual growth in recent years), making this unit a reliable cash generator.

Competitive advantage rests on deep scientific expertise, entrenched client relationships, and regulatory know-how that raise switching costs and protect margins.

- Market leader in regulated, mature sector

- Global health spend ~ $9.5T (2023)

- Growth ~4–5% p.a., tracks healthcare spending

- Long-term contracts, high switching costs

- Deep scientific expertise entrenches advantage

Brand Consulting and Design

Through Landor (acquired 2019) and other branding units, WPP holds a leading share in mature visual identity and brand-architecture services, generating stable revenue—WPP reported global design and branding revenues of about $1.2bn in FY2024, with gross margins near 35%.

Core branding demand is steady, not high-growth, but commands premium fees; those margins funded R&D and digital bets, with WPP allocating roughly $220m to tech and data initiatives in 2024.

- Stable market, high share via Landor

- FY2024 branding revenue ≈ $1.2bn

- Gross margins ≈ 35%

- Funded $220m tech/data spend in 2024

WPP: £10.5bn revenue, £1.3bn cash flow—GroupM fuels $115bn billings, £0.46 div

GroupM and legacy creative and PR units produced steady high-margin cash flow in 2024—Group revenue £10.5bn, operating cash flow £1.3bn, GroupM ~40% of global billings (~$115bn), WPP EBITDA from mature units ≈ $650m; cash funds £0.46/share dividend and $220m tech/data spend while servicing net debt ~$2.1bn.

| Metric | 2024 |

|---|---|

| Group revenue | £10.5bn |

| Operating cash flow | £1.3bn |

| GroupM billings | $115bn (~40%) |

| Mature-unit EBITDA | $650m |

| Dividend | £0.46/sh |

| Tech/data spend | $220m |

| Net debt | $2.1bn |

What You’re Viewing Is Included

WPP BCG Matrix

The file you're previewing is the exact BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document designed by strategy experts for immediate use in presentations, planning, or client deliverables.