W. R. Berkley PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

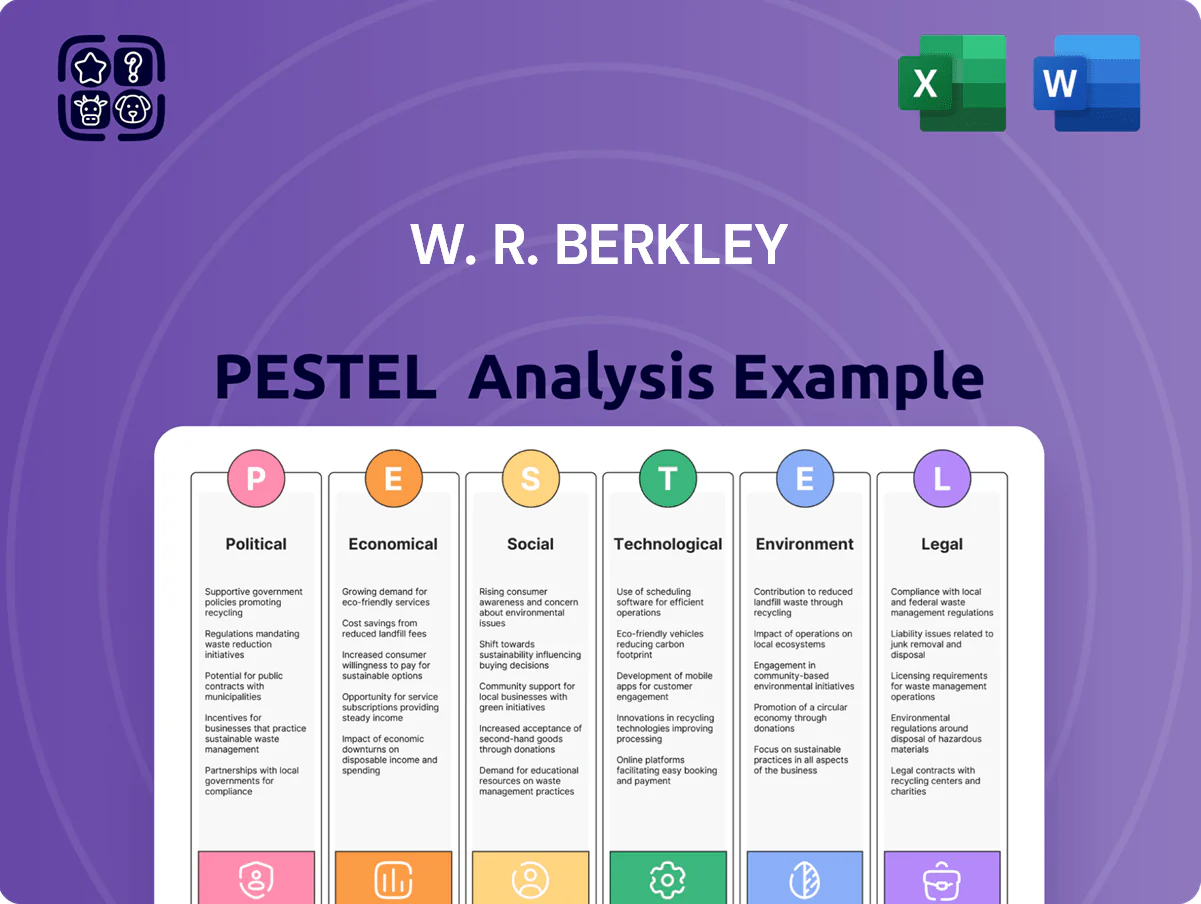

Gain a competitive edge with our PESTLE Analysis of W. R. Berkley—concise insights into political, economic, social, technological, legal, and environmental forces shaping its risk and opportunity landscape; ideal for investors and strategists seeking actionable intelligence. Purchase the full report to unlock detailed trends, quantified impacts, and ready-to-use recommendations for confident decision-making.

Political factors

Geopolitical instability and international operations

W. R. Berkley operates in 50+ countries; geopolitical unrest (e.g., 2023–2025 Middle East and Russia tensions) risks claims spikes and disrupted premium flows—international P&C exposures comprised ~35% of gross written premium in 2024. Changes in trade deals or sanctions can hinder decentralized underwriting and reinsurance placements. Management must monitor political risk to protect international asset allocation and ensure timely premium collection.

Changes in insurance regulatory oversight

As a heavily regulated insurer, W. R. Berkley faces evolving oversight from federal and 50 state authorities; in 2024 U.S. state insurance regulators issued over 120 rule changes impacting capital and market conduct. New political administrations can push stricter risk-based capital norms—NAIC stress-testing and RBC tweaks could raise capital buffers by several percentage points, affecting Berkley’s $7.8B shareholders’ equity (2024). Adapting to changing mandates for insurance commissioners is essential to retain licenses across all active territories and avoid fines or market constraints.

Government mandates for specialized coverage

Political mandates for specialized coverage, such as state workers compensation and commercial auto requirements, drive predictable demand—US workers compensation premiums reached about $56.5bn in 2024, influencing W. R. Berkley’s underwriting volumes. Changes to government-backed programs or expansions of safety nets can shift market share away from private carriers; for example, proposed federal initiatives in 2025 could affect ~5–10% of niche commercial lines. Berkley actively monitors legislative changes across 49 states and international markets to adjust product offerings and maintain compliance with evolving legal requirements.

Protectionist trade policies

Protectionist tariffs raise input costs for W. R. Berkley policyholders—US steel tariffs since 2018 raised domestic prices by ~25%, increasing property/casualty exposure for manufacturers and contractors.

Higher costs reshape commercial risk profiles in manufacturing/logistics, raising claims frequency and supply-chain interruption losses; US manufacturing PMI fell to 47.3 in Dec 2023, signaling stress.

Protectionism can constrain cross-border reinsurance capital; global reinsurance capital totaled about $640bn in 2023, and restrictions would tighten capacity and raise ceded premium rates.

- Tariffs → higher input costs → increased P&C exposures

- Manufacturing PMI decline → elevated business interruption risk

- Reinsurance capital concentration (~$640bn in 2023) vulnerable to cross-border limits

National security and terrorism insurance

The political environment shapes renewal and terms of programs like the Terrorism Risk Insurance Act, which in 2024 backstops insurers for losses exceeding a federal trigger (historically $200m) and a program cap that supported $1bn+ insurer retention in major events.

Such government-backed safety nets reduce systemic exposure for W. R. Berkley, which reported $2.9bn P/C underwriting income in 2024, but renewal uncertainty can spike pricing and shrink coverage for high-risk commercial assets.

Market volatility after legislative uncertainty historically raised terrorism premiums by 10–30% for exposed commercial portfolios within 12 months.

- Government trigger level: ~$200m

- Program reduces insurer catastrophic exposure

- W. R. Berkley 2024 P/C underwriting income: $2.9bn

- Premiums can rise 10–30% amid renewal uncertainty

Geopolitics, regulation and reinsurance squeeze insurers — $7.8B equity, 35% intl GWP

Political risks (geopolitical unrest, protectionism, regulatory shifts) can spike claims, constrain reinsurance, and force higher capital; 2024: 35% international GWP, $7.8B shareholders’ equity, $2.9B P/C underwriting income, global reinsurance capital ~$640B. Regulators issued 120+ rule changes (2024) affecting capital and conduct; terrorism backstop trigger ~$200M.

| Metric | 2024/2023 |

|---|---|

| Intl GWP | ~35% |

| Shareholders' equity | $7.8B (2024) |

| P/C underwriting income | $2.9B (2024) |

| Reinsurance capital | ~$640B (2023) |

| Regulatory changes | 120+ (2024) |

| Terrorism trigger | ~$200M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact W. R. Berkley, combining data-driven trends and region-specific regulatory context to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary for W. R. Berkley that streamlines external risk review during meetings and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

Interest rate environment and investment income

W. R. Berkley holds roughly $28.5 billion in investments (2024), so market interest-rate moves materially affect investment income; a 100 bps rise can increase annual interest yield by an estimated $285 million before tax. Higher rates have supported yield on fixed-income assets, helping offset tight underwriting margins where combined ratios hovered near 97–99% in 2023–24. In contrast, prolonged low rates would force greater reliance on underwriting discipline and pricing to sustain ROE around the company’s long-term target of ~12%.

Inflationary pressure on loss costs

Sustained inflation raises claim costs for W. R. Berkley, notably medical inflation (~4–6% annual U.S. health CPI in 2023–2024), rising construction material prices (lumber +12% year-over-year in 2024) and auto-part shortages pushing repair costs; this forces pricing and reserve increases.

Higher claim severity requires proactive repricing and reserve strengthening—Berkley reported reserve strengthening in prior filings—and inaccurate forecasting risks adverse development in prior-year reserves, as seen industry-wide with multi-percent reserve increases in 2023–2024.

Global GDP growth and commercial demand

Demand for W. R. Berkley’s commercial lines closely tracks global GDP growth; IMF projected 2025 world GDP growth at about 3.0% in Oct 2024 updates, supporting higher payrolls and capex that drove U.S. commercial insurance premiums up ~6% in 2024 per industry data, boosting potential premium volumes for the insurer.

Labor market conditions and workers compensation

The US unemployment rate fell to 3.5% in Dec 2024, supporting payroll growth and lifting workers compensation premium volumes for W. R. Berkley, where higher employment increases exposure across construction and manufacturing segments.

However, influx of less-experienced hires correlates with higher claim frequency; Bureau of Labor Statistics 2024 data shows recordable incident rates rose 4% in high-turnover sectors, prompting Berkley to tighten underwriting and raise rates in selected classes.

Monitoring monthly payroll and sectoral hiring—notably a 3.8% payroll increase year-over-year in 2024 for private industry—allows dynamic pricing and portfolio risk adjustments to protect combined ratios.

- 3.5% US unemployment (Dec 2024)

- +3.8% private payrolls YoY (2024)

- +4% incident rate in high-turnover sectors (2024 BLS)

- Targets: tightened underwriting, selective rate increases

Currency exchange rate volatility

With operations across North America, Europe and Asia, W. R. Berkley faces FX volatility that can swing reported international premiums and claim costs; a 5% USD strengthening in 2024 would reduce euro-denominated revenue by roughly $50–75m given ~€4–6bn gross written premium exposure.

The company uses strategic hedges and local-currency asset matching to mitigate translation and transaction risk, supporting a relatively stable adjusted pre-tax margin and limiting FX impact on consolidated equity.

- Estimated 2024 FX sensitivity: 5% USD move ≈ $50–75m revenue translation effect

- Hedging and local-currency assets reduce earnings volatility

- Claims settlement exposure concentrated in Europe and Asia

Higher rates fuel ~$285m per 100bps on $28.5bn, underwriting pressure from rising claims

Rising rates boost investment income on ~$28.5bn investments (100bps ≈ +$285m), offsetting tight combined ratios (~97–99% 2023–24); sustained inflation (medical 4–6%, lumber +12% 2024) raises claim costs and reserves; payroll growth (private payrolls +3.8% YoY 2024) and low unemployment (3.5% Dec 2024) lift commercial premium volumes; 5% USD strength ≈ $50–75m translation hit mitigated by hedging.

| Metric | 2024/2025 |

|---|---|

| Investments | $28.5bn |

| Rate sensitivity | 100bps ≈ +$285m |

| Combined ratio | 97–99% |

| Unemployment | 3.5% (Dec 2024) |

| Payrolls YoY | +3.8% |

| FX sensitivity | 5% USD ≈ $50–75m |

Same Document Delivered

W. R. Berkley PESTLE Analysis

The preview shown here is the exact W. R. Berkley PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE Analysis of W. R. Berkley—concise insights into political, economic, social, technological, legal, and environmental forces shaping its risk and opportunity landscape; ideal for investors and strategists seeking actionable intelligence. Purchase the full report to unlock detailed trends, quantified impacts, and ready-to-use recommendations for confident decision-making.

Political factors

Geopolitical instability and international operations

W. R. Berkley operates in 50+ countries; geopolitical unrest (e.g., 2023–2025 Middle East and Russia tensions) risks claims spikes and disrupted premium flows—international P&C exposures comprised ~35% of gross written premium in 2024. Changes in trade deals or sanctions can hinder decentralized underwriting and reinsurance placements. Management must monitor political risk to protect international asset allocation and ensure timely premium collection.

Changes in insurance regulatory oversight

As a heavily regulated insurer, W. R. Berkley faces evolving oversight from federal and 50 state authorities; in 2024 U.S. state insurance regulators issued over 120 rule changes impacting capital and market conduct. New political administrations can push stricter risk-based capital norms—NAIC stress-testing and RBC tweaks could raise capital buffers by several percentage points, affecting Berkley’s $7.8B shareholders’ equity (2024). Adapting to changing mandates for insurance commissioners is essential to retain licenses across all active territories and avoid fines or market constraints.

Government mandates for specialized coverage

Political mandates for specialized coverage, such as state workers compensation and commercial auto requirements, drive predictable demand—US workers compensation premiums reached about $56.5bn in 2024, influencing W. R. Berkley’s underwriting volumes. Changes to government-backed programs or expansions of safety nets can shift market share away from private carriers; for example, proposed federal initiatives in 2025 could affect ~5–10% of niche commercial lines. Berkley actively monitors legislative changes across 49 states and international markets to adjust product offerings and maintain compliance with evolving legal requirements.

Protectionist trade policies

Protectionist tariffs raise input costs for W. R. Berkley policyholders—US steel tariffs since 2018 raised domestic prices by ~25%, increasing property/casualty exposure for manufacturers and contractors.

Higher costs reshape commercial risk profiles in manufacturing/logistics, raising claims frequency and supply-chain interruption losses; US manufacturing PMI fell to 47.3 in Dec 2023, signaling stress.

Protectionism can constrain cross-border reinsurance capital; global reinsurance capital totaled about $640bn in 2023, and restrictions would tighten capacity and raise ceded premium rates.

- Tariffs → higher input costs → increased P&C exposures

- Manufacturing PMI decline → elevated business interruption risk

- Reinsurance capital concentration (~$640bn in 2023) vulnerable to cross-border limits

National security and terrorism insurance

The political environment shapes renewal and terms of programs like the Terrorism Risk Insurance Act, which in 2024 backstops insurers for losses exceeding a federal trigger (historically $200m) and a program cap that supported $1bn+ insurer retention in major events.

Such government-backed safety nets reduce systemic exposure for W. R. Berkley, which reported $2.9bn P/C underwriting income in 2024, but renewal uncertainty can spike pricing and shrink coverage for high-risk commercial assets.

Market volatility after legislative uncertainty historically raised terrorism premiums by 10–30% for exposed commercial portfolios within 12 months.

- Government trigger level: ~$200m

- Program reduces insurer catastrophic exposure

- W. R. Berkley 2024 P/C underwriting income: $2.9bn

- Premiums can rise 10–30% amid renewal uncertainty

Geopolitics, regulation and reinsurance squeeze insurers — $7.8B equity, 35% intl GWP

Political risks (geopolitical unrest, protectionism, regulatory shifts) can spike claims, constrain reinsurance, and force higher capital; 2024: 35% international GWP, $7.8B shareholders’ equity, $2.9B P/C underwriting income, global reinsurance capital ~$640B. Regulators issued 120+ rule changes (2024) affecting capital and conduct; terrorism backstop trigger ~$200M.

| Metric | 2024/2023 |

|---|---|

| Intl GWP | ~35% |

| Shareholders' equity | $7.8B (2024) |

| P/C underwriting income | $2.9B (2024) |

| Reinsurance capital | ~$640B (2023) |

| Regulatory changes | 120+ (2024) |

| Terrorism trigger | ~$200M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact W. R. Berkley, combining data-driven trends and region-specific regulatory context to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary for W. R. Berkley that streamlines external risk review during meetings and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

Interest rate environment and investment income

W. R. Berkley holds roughly $28.5 billion in investments (2024), so market interest-rate moves materially affect investment income; a 100 bps rise can increase annual interest yield by an estimated $285 million before tax. Higher rates have supported yield on fixed-income assets, helping offset tight underwriting margins where combined ratios hovered near 97–99% in 2023–24. In contrast, prolonged low rates would force greater reliance on underwriting discipline and pricing to sustain ROE around the company’s long-term target of ~12%.

Inflationary pressure on loss costs

Sustained inflation raises claim costs for W. R. Berkley, notably medical inflation (~4–6% annual U.S. health CPI in 2023–2024), rising construction material prices (lumber +12% year-over-year in 2024) and auto-part shortages pushing repair costs; this forces pricing and reserve increases.

Higher claim severity requires proactive repricing and reserve strengthening—Berkley reported reserve strengthening in prior filings—and inaccurate forecasting risks adverse development in prior-year reserves, as seen industry-wide with multi-percent reserve increases in 2023–2024.

Global GDP growth and commercial demand

Demand for W. R. Berkley’s commercial lines closely tracks global GDP growth; IMF projected 2025 world GDP growth at about 3.0% in Oct 2024 updates, supporting higher payrolls and capex that drove U.S. commercial insurance premiums up ~6% in 2024 per industry data, boosting potential premium volumes for the insurer.

Labor market conditions and workers compensation

The US unemployment rate fell to 3.5% in Dec 2024, supporting payroll growth and lifting workers compensation premium volumes for W. R. Berkley, where higher employment increases exposure across construction and manufacturing segments.

However, influx of less-experienced hires correlates with higher claim frequency; Bureau of Labor Statistics 2024 data shows recordable incident rates rose 4% in high-turnover sectors, prompting Berkley to tighten underwriting and raise rates in selected classes.

Monitoring monthly payroll and sectoral hiring—notably a 3.8% payroll increase year-over-year in 2024 for private industry—allows dynamic pricing and portfolio risk adjustments to protect combined ratios.

- 3.5% US unemployment (Dec 2024)

- +3.8% private payrolls YoY (2024)

- +4% incident rate in high-turnover sectors (2024 BLS)

- Targets: tightened underwriting, selective rate increases

Currency exchange rate volatility

With operations across North America, Europe and Asia, W. R. Berkley faces FX volatility that can swing reported international premiums and claim costs; a 5% USD strengthening in 2024 would reduce euro-denominated revenue by roughly $50–75m given ~€4–6bn gross written premium exposure.

The company uses strategic hedges and local-currency asset matching to mitigate translation and transaction risk, supporting a relatively stable adjusted pre-tax margin and limiting FX impact on consolidated equity.

- Estimated 2024 FX sensitivity: 5% USD move ≈ $50–75m revenue translation effect

- Hedging and local-currency assets reduce earnings volatility

- Claims settlement exposure concentrated in Europe and Asia

Higher rates fuel ~$285m per 100bps on $28.5bn, underwriting pressure from rising claims

Rising rates boost investment income on ~$28.5bn investments (100bps ≈ +$285m), offsetting tight combined ratios (~97–99% 2023–24); sustained inflation (medical 4–6%, lumber +12% 2024) raises claim costs and reserves; payroll growth (private payrolls +3.8% YoY 2024) and low unemployment (3.5% Dec 2024) lift commercial premium volumes; 5% USD strength ≈ $50–75m translation hit mitigated by hedging.

| Metric | 2024/2025 |

|---|---|

| Investments | $28.5bn |

| Rate sensitivity | 100bps ≈ +$285m |

| Combined ratio | 97–99% |

| Unemployment | 3.5% (Dec 2024) |

| Payrolls YoY | +3.8% |

| FX sensitivity | 5% USD ≈ $50–75m |

Same Document Delivered

W. R. Berkley PESTLE Analysis

The preview shown here is the exact W. R. Berkley PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.