Wuliangye Yibin Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

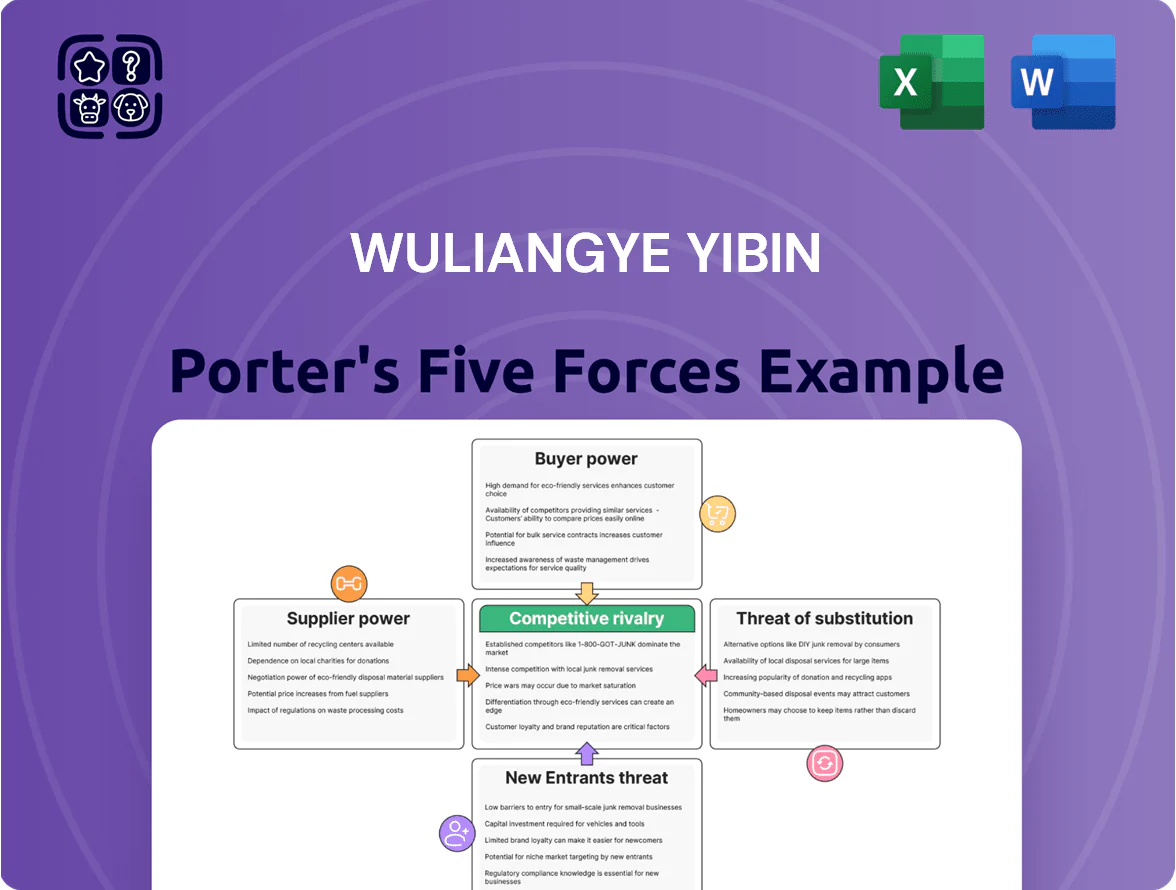

Wuliangye Yibin faces intense rivalry from premium baijiu brands, moderate supplier leverage due to strong ingredient sourcing, rising buyer sophistication, limited threat from new entrants because of high brand loyalty and capital needs, and growing substitution risks from craft spirits and health trends; this snapshot reveals core pressures on margins and growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Wuliangye Yibin’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Agricultural Supply Base

Wuliangye sources sorghum, rice, glutinous rice, wheat and corn from hundreds of thousands of small farmers across Sichuan and neighbouring provinces, so suppliers are highly fragmented and lack pricing power.

By 2025 Wuliangye’s annual grain procurement exceeded 600,000 tons, so individual suppliers’ leverage is negligible and switching costs for the firm remain low.

Strategic Control Over Raw Material Bases

Wuliangye Yibin has invested over RMB 2.1 billion since 2018 to build 120,000 hectares of company-controlled high-quality grain bases, securing about 35% of its annual sorghum needs and cutting external procurements by ~22% in 2024.

Vertical integration into cultivation and logistics lowers supplier dependence, caps third-party grain merchants’ price power, and helped stabilize production cost inflation to 3.8% in 2024 versus 7.2% industry average.

Low Switching Costs for Standard Inputs

For commodity inputs like packaging, glass bottles, and logistics, Wuliangye Yibin faces a deep supplier market—China's glass container capacity rose 3.8% in 2024 to ~55 million tonnes, keeping prices competitive. Low switching costs let Wuliangye secure bulk discounts and spot contracts; procurement reports show top distillers cut packaging spend by ~6% YoY in 2024. This supplier abundance preserves Wuliangye’s leverage in negotiations and contract terms.

Uniqueness of Specialized Yeast and Water

Wuliangye controls proprietary medicinal yeast and Yibin-region water, removing reliance on external suppliers for its core fermentation inputs and cutting supplier bargaining power sharply.

This vertical control supports margin stability: gross margin was 73.4% in 2024, reflecting low input-cost pressure vs peers.

- Proprietary yeast and water = internal supply

Scale-Driven Procurement Leverage

Wuliangye Yibin uses scale-driven procurement leverage: with 2024 revenue ~RMB 90.3bn and annual baijiu output >100,000 kiloliters, it secures double-digit supplier discounts and priority allocations.

Suppliers accept thinner margins for prestige and steady volumes, making them more dependent—company accounts for an estimated 15–30% of key packaging suppliers’ sales, so switching costs favor Wuliangye.

- 2024 revenue ~RMB 90.3bn; output >100,000 kl

- Supplier share of sales ~15–30%

- Double-digit procurement discounts common

- Switching costs and volume stability favor Wuliangye

Scale, proprietary inputs and RMB2.1bn farms secure cheap grain, 35% sorghum supply

Suppliers have low power: fragmented grain network, 600,000+ t procured in 2025, and 120,000 ha company bases supplying ~35% of sorghum needs after RMB 2.1bn investment; proprietary yeast/water and scale (2024 revenue RMB 90.3bn; output >100,000 kl) secure double-digit discounts, cut input inflation to 3.8% in 2024, and keep switching costs low.

| Metric | Value |

|---|---|

| Grain procured (2025) | 600,000+ t |

| Company bases | 120,000 ha (~35% sorghum) |

| Investment since 2018 | RMB 2.1bn |

| Revenue (2024) | RMB 90.3bn |

| Gross margin (2024) | 73.4% |

What is included in the product

Tailored Porter's Five Forces analysis for Wuliangye Yibin, uncovering competitive drivers, buyer and supplier power, substitute threats, and entry barriers that shape its pricing and profitability.

Concise Porter's Five Forces summary for Wuliangye Yibin—quickly spot competitive threats and supplier/buyer leverage to guide strategic moves.

Customers Bargaining Power

High Brand Equity and Consumer Loyalty

Wuliangye, China’s premium baijiu maker, holds strong national-brand status and deep cultural ties, driving high consumer loyalty and low price sensitivity among top-tier buyers; in 2024 premium SKUs accounted for about 62% of group revenue, supporting elevated ASPs.

Distributor Network Dependency

Wuliangye Yibin relies on a vast regional distributor network as primary market intermediaries, but its brand pull—53% premium ASP over provincial rivals in 2024—makes distributers dependent: losing distribution rights would cut many wholesalers’ revenues by an estimated 30–50%. This power lets Wuliangye set strict monthly sales quotas and inventory turns (target 8–10 turns/year), keeping distributor bargaining power low.

Impact of Digitalization and DTC Channels

By late 2025 Wuliangye had scaled DTC channels to 480 stores and a digital ecosystem generating CNY 6.2 billion in retail sales, cutting distributor-sourced volume share from 68% in 2022 to 44%—this shift reduces middlemen power by routing orders and price setting through company channels.

First-party data from 32 million registered users lets Wuliangye price dynamically and run targeted promotions, improving gross margin on DTC sales by ~9 percentage points versus wholesale and weakening distributors’ leverage.

Direct engagement also centralizes loyalty and inventory control, so large-scale distributors can no longer coordinate pricing or demand concessions without risking channel conflict and lost capture of high-margin customers.

Sensitivity to Macroeconomic Conditions

Wealthy individuals and corporate clients drive Wuliangye Yibin’s premium baijiu sales, and their spending rose 12% in 2023 but slowed in 2024 amid China’s 2023–24 GDP growth cooling to about 5.0% (IMF, 2024); during downturns they shift to lower tiers or cut discretionary purchases, reducing average selling prices.

That behavioral shift gives customers passive leverage, forcing Wuliangye to increase promotions and channel discounts to protect volumes—trade marketing spend rose ~8% in 2024 to stabilize shipments.

- Premium buyers = major segment; 2023 sales +12%

- China GDP ~5.0% in 2024; demand softened

- Shift to lower tiers reduces ASPs

- Promotions up ~8% in 2024 to defend volume

Product Transparency and Price Comparison

The rise of e-commerce and liquor apps (e.g., JD.com, Tmall, and Moutai-verified channels) has cut search costs; 2024 surveys show 68% of Chinese spirits buyers compare prices online, forcing Wuliangye Yibin to keep pricing consistent across channels to avoid arbitrage and regional markups.

This transparency limits excessive localized pricing, increases customer bargaining power, and pushes the firm to publish unified MSRP and channel policies—impacting margins if discounts proliferate.

- 68% of buyers compare prices online (2024 survey)

- Channel price gaps >10% trigger buyer defection

- Unified MSRP reduces regional overcharging

Premium brand, DTC surge vs rising online price scrutiny—promo spend up 8%

Strong national brand and premium mix (62% revenue from premium SKUs in 2024) keep customer bargaining low despite distributor dependence; DTC growth (480 stores, CNY 6.2bn DTC sales by 2025) and 32m users boost pricing power, but softened demand (China GDP ~5.0% in 2024) and 68% online price comparison raise buyer leverage, prompting ~8% higher trade promo spend in 2024.

| Metric | Value |

|---|---|

| Premium share (2024) | 62% |

| DTC sales (2025) | CNY 6.2bn |

| Registered users | 32m |

| Online price compare (2024) | 68% |

| Trade promo rise (2024) | +8% |

What You See Is What You Get

Wuliangye Yibin Porter's Five Forces Analysis

This preview shows the exact Wuliangye Yibin Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file ready for download and use the moment you buy. You're looking at the actual deliverable: complete, actionable, and ready for immediate application to strategy or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Wuliangye Yibin faces intense rivalry from premium baijiu brands, moderate supplier leverage due to strong ingredient sourcing, rising buyer sophistication, limited threat from new entrants because of high brand loyalty and capital needs, and growing substitution risks from craft spirits and health trends; this snapshot reveals core pressures on margins and growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Wuliangye Yibin’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Agricultural Supply Base

Wuliangye sources sorghum, rice, glutinous rice, wheat and corn from hundreds of thousands of small farmers across Sichuan and neighbouring provinces, so suppliers are highly fragmented and lack pricing power.

By 2025 Wuliangye’s annual grain procurement exceeded 600,000 tons, so individual suppliers’ leverage is negligible and switching costs for the firm remain low.

Strategic Control Over Raw Material Bases

Wuliangye Yibin has invested over RMB 2.1 billion since 2018 to build 120,000 hectares of company-controlled high-quality grain bases, securing about 35% of its annual sorghum needs and cutting external procurements by ~22% in 2024.

Vertical integration into cultivation and logistics lowers supplier dependence, caps third-party grain merchants’ price power, and helped stabilize production cost inflation to 3.8% in 2024 versus 7.2% industry average.

Low Switching Costs for Standard Inputs

For commodity inputs like packaging, glass bottles, and logistics, Wuliangye Yibin faces a deep supplier market—China's glass container capacity rose 3.8% in 2024 to ~55 million tonnes, keeping prices competitive. Low switching costs let Wuliangye secure bulk discounts and spot contracts; procurement reports show top distillers cut packaging spend by ~6% YoY in 2024. This supplier abundance preserves Wuliangye’s leverage in negotiations and contract terms.

Uniqueness of Specialized Yeast and Water

Wuliangye controls proprietary medicinal yeast and Yibin-region water, removing reliance on external suppliers for its core fermentation inputs and cutting supplier bargaining power sharply.

This vertical control supports margin stability: gross margin was 73.4% in 2024, reflecting low input-cost pressure vs peers.

- Proprietary yeast and water = internal supply

Scale-Driven Procurement Leverage

Wuliangye Yibin uses scale-driven procurement leverage: with 2024 revenue ~RMB 90.3bn and annual baijiu output >100,000 kiloliters, it secures double-digit supplier discounts and priority allocations.

Suppliers accept thinner margins for prestige and steady volumes, making them more dependent—company accounts for an estimated 15–30% of key packaging suppliers’ sales, so switching costs favor Wuliangye.

- 2024 revenue ~RMB 90.3bn; output >100,000 kl

- Supplier share of sales ~15–30%

- Double-digit procurement discounts common

- Switching costs and volume stability favor Wuliangye

Scale, proprietary inputs and RMB2.1bn farms secure cheap grain, 35% sorghum supply

Suppliers have low power: fragmented grain network, 600,000+ t procured in 2025, and 120,000 ha company bases supplying ~35% of sorghum needs after RMB 2.1bn investment; proprietary yeast/water and scale (2024 revenue RMB 90.3bn; output >100,000 kl) secure double-digit discounts, cut input inflation to 3.8% in 2024, and keep switching costs low.

| Metric | Value |

|---|---|

| Grain procured (2025) | 600,000+ t |

| Company bases | 120,000 ha (~35% sorghum) |

| Investment since 2018 | RMB 2.1bn |

| Revenue (2024) | RMB 90.3bn |

| Gross margin (2024) | 73.4% |

What is included in the product

Tailored Porter's Five Forces analysis for Wuliangye Yibin, uncovering competitive drivers, buyer and supplier power, substitute threats, and entry barriers that shape its pricing and profitability.

Concise Porter's Five Forces summary for Wuliangye Yibin—quickly spot competitive threats and supplier/buyer leverage to guide strategic moves.

Customers Bargaining Power

High Brand Equity and Consumer Loyalty

Wuliangye, China’s premium baijiu maker, holds strong national-brand status and deep cultural ties, driving high consumer loyalty and low price sensitivity among top-tier buyers; in 2024 premium SKUs accounted for about 62% of group revenue, supporting elevated ASPs.

Distributor Network Dependency

Wuliangye Yibin relies on a vast regional distributor network as primary market intermediaries, but its brand pull—53% premium ASP over provincial rivals in 2024—makes distributers dependent: losing distribution rights would cut many wholesalers’ revenues by an estimated 30–50%. This power lets Wuliangye set strict monthly sales quotas and inventory turns (target 8–10 turns/year), keeping distributor bargaining power low.

Impact of Digitalization and DTC Channels

By late 2025 Wuliangye had scaled DTC channels to 480 stores and a digital ecosystem generating CNY 6.2 billion in retail sales, cutting distributor-sourced volume share from 68% in 2022 to 44%—this shift reduces middlemen power by routing orders and price setting through company channels.

First-party data from 32 million registered users lets Wuliangye price dynamically and run targeted promotions, improving gross margin on DTC sales by ~9 percentage points versus wholesale and weakening distributors’ leverage.

Direct engagement also centralizes loyalty and inventory control, so large-scale distributors can no longer coordinate pricing or demand concessions without risking channel conflict and lost capture of high-margin customers.

Sensitivity to Macroeconomic Conditions

Wealthy individuals and corporate clients drive Wuliangye Yibin’s premium baijiu sales, and their spending rose 12% in 2023 but slowed in 2024 amid China’s 2023–24 GDP growth cooling to about 5.0% (IMF, 2024); during downturns they shift to lower tiers or cut discretionary purchases, reducing average selling prices.

That behavioral shift gives customers passive leverage, forcing Wuliangye to increase promotions and channel discounts to protect volumes—trade marketing spend rose ~8% in 2024 to stabilize shipments.

- Premium buyers = major segment; 2023 sales +12%

- China GDP ~5.0% in 2024; demand softened

- Shift to lower tiers reduces ASPs

- Promotions up ~8% in 2024 to defend volume

Product Transparency and Price Comparison

The rise of e-commerce and liquor apps (e.g., JD.com, Tmall, and Moutai-verified channels) has cut search costs; 2024 surveys show 68% of Chinese spirits buyers compare prices online, forcing Wuliangye Yibin to keep pricing consistent across channels to avoid arbitrage and regional markups.

This transparency limits excessive localized pricing, increases customer bargaining power, and pushes the firm to publish unified MSRP and channel policies—impacting margins if discounts proliferate.

- 68% of buyers compare prices online (2024 survey)

- Channel price gaps >10% trigger buyer defection

- Unified MSRP reduces regional overcharging

Premium brand, DTC surge vs rising online price scrutiny—promo spend up 8%

Strong national brand and premium mix (62% revenue from premium SKUs in 2024) keep customer bargaining low despite distributor dependence; DTC growth (480 stores, CNY 6.2bn DTC sales by 2025) and 32m users boost pricing power, but softened demand (China GDP ~5.0% in 2024) and 68% online price comparison raise buyer leverage, prompting ~8% higher trade promo spend in 2024.

| Metric | Value |

|---|---|

| Premium share (2024) | 62% |

| DTC sales (2025) | CNY 6.2bn |

| Registered users | 32m |

| Online price compare (2024) | 68% |

| Trade promo rise (2024) | +8% |

What You See Is What You Get

Wuliangye Yibin Porter's Five Forces Analysis

This preview shows the exact Wuliangye Yibin Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file ready for download and use the moment you buy. You're looking at the actual deliverable: complete, actionable, and ready for immediate application to strategy or investment decisions.