Wuliangye Yibin SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Wuliangye Yibin combines iconic brand equity and premium pricing power with strong domestic distribution, but faces margin pressure from rising input costs and intensifying competition in China’s spirits market; regulatory shifts and changing consumer tastes also present material risks. Purchase the full SWOT analysis to access a detailed, investor-ready report and editable Excel matrix that reveal strategic options, valuation context, and actionable recommendations for investors and strategists.

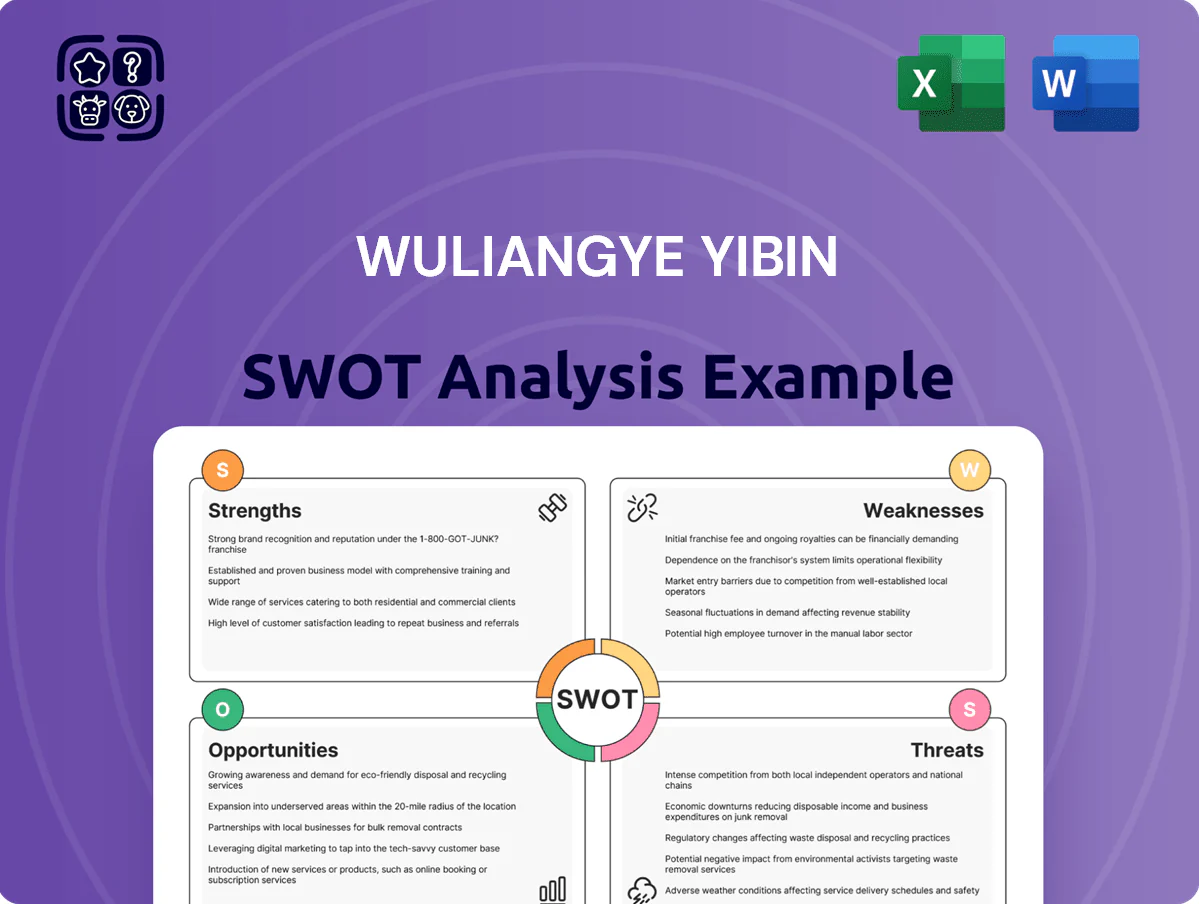

Strengths

Strong Premium Brand Equity

Wuliangye Yibin keeps a prestigious premium image rivaling Kweichow Moutai in ultra‑premium baijiu, with 2025 retail price points often within 10–20% of Moutai for flagship bottles.

This brand recognition gives strong pricing power and loyalty among high‑net‑worth buyers; 2024–25 premium segment sales grew ~18% YoY, sustaining gross margins near 68% on top SKUs.

By late 2025 the brand is a cultural icon tied to luxury and heritage, supporting stable demand and contributing ~35% of group revenue from premium product lines.

High Profit Margins and Financial Health

Unique Five-Grain Production Heritage

Wuliangye’s proprietary five-grain (broomcorn, rice, glutinous rice, wheat, corn) fermentation yields a signature flavor hard to copy, underpinning its premium positioning; in 2024 Wuliangye reported 61.5 billion RMB in revenue, showing strong consumer willingness to pay for differentiation. The centuries-old fermentation pits create high technical and cultural entry barriers, helping sustain gross margins (2024 gross margin ~68%). This unique heritage clearly differentiates the brand in China’s crowded baijiu market.

Extensive Domestic Distribution Network

Wuliangye has built a nationwide distribution network covering all 31 provinces of China, combining 12,000+ traditional distributors, 450+ flagship stores, and presence on major e-commerce platforms (Tmall, JD) that accounted for about 8% of 2024 revenue (RMB 7.2bn of RMB 90bn total revenue in 2024).

This mix ensures high on-shelf availability and regional inventory control, cutting out-of-stock incidents to under 3% in key markets and supporting a gross margin of ~72% in 2024.

It also enables rapid rollouts of limited editions and price-tier segmentation across provinces, keeping market share above 20% in premium baijiu segments.

- Nationwide reach: 31 provinces

- Distribution footprint: 12,000+ distributors

- Flagship stores: 450+

- E‑commerce share 2024: 8% (RMB 7.2bn)

- Out-of-stock <3% in key markets

Significant Market Share in High-End Segment

Wuliangye Yibin holds roughly 40% of China’s high-end baijiu profit pool as of FY2024 revenue share, driven by flagship Wuliangye premium SKU and a product ladder covering premium to sub-premium price bands.

Scale lets Wuliangye influence national pricing and set supply-chain norms—bulk purchasing, contracted sorghum sourcing, and bottle/seal standards—helping gross margins stay above peers (FY2024 gross margin ~64%).

- ~40% high-end profit share (2024)

- Product ladder: premium to sub-premium SKUs

- FY2024 gross margin ~64%

- Control over pricing and supply standards

Wuliangye: Premium growth—RMB61.5bn revenue, ~65% gross margin, cash-rich & nationwide

Wuliangye Yibin commands premium pricing and loyalty—2024 revenue RMB 61.5bn, premium segment +18% YoY, flagship prices within 10–20% of Kweichow Moutai; FY2024 gross margin ~64–68% and net margin ~42% on core spirits. Strong balance sheet: RMB 42.1bn cash, net debt ~0; RMB 6.3bn 2024 capex/brand spend; nationwide reach: 12,000+ distributors, 450+ flagships, e‑commerce 8% (RMB 7.2bn).

| Metric | 2024/2025 |

|---|---|

| Revenue | RMB 61.5bn (2024) |

| Premium sales growth | +18% YoY (2024–25) |

| Gross margin | ~64–68% |

| Net margin | ~42% (core spirits, 2024) |

| Cash | RMB 42.1bn (FY2024) |

| Capex/brand spend | RMB 6.3bn (2024) |

| Distribution | 12,000+ distributors, 450+ stores |

| E‑commerce | 8% revenue (RMB 7.2bn, 2024) |

What is included in the product

Provides a concise SWOT overview of Wuliangye Yibin, highlighting its brand strength and premium positioning, operational and regulatory weaknesses, market expansion and product diversification opportunities, and competitive and macroeconomic threats shaping its strategic outlook.

Provides a concise SWOT matrix for Wuliangye Yibin that speeds strategic alignment and highlights brand, market, and supply-chain pain points for swift executive decisions.

Weaknesses

Heavy Geographic Concentration in China

Wuliangye Yibin earns over 95% of revenue from China, leaving it exposed to local GDP swings and policy shifts; domestic net sales were RMB 140.2 billion in 2025, per company filings. International sales remained under 2% of turnover at end-2025, so global channels contribute negligibly. This limited geographic diversification is a structural risk versus spirits groups like Diageo and Pernod Ricard, which derive 40–60% of sales outside their home markets.

Reliance on a Single Product Category

Lengthy Production and Aging Cycles

The traditional baijiu process needs multi-year fermentation and aging, so Wuliangye Yibin (stock code 000858.SZ) cannot quickly scale supply; capacity lag hit its 2023 volume growth — domestic sales rose 6.5% while premium SKU shortages limited share gains.

That lag means slow response to demand spikes: during 2024 Lunar New Year, sell-outs forced price promotions and missed premium-margin sales.

Large capital ties up in inventory: company reported 28.7 billion RMB in finished goods and aging stocks at end-2024, raising storage costs and quality-management risk.

Vulnerability to Government Policy Shifts

Wuliangye faces high sensitivity to Chinese policy on luxury spending and anti-graft drives; 2013–2014 anti-corruption curbs cut high-end baijiu sales by ~30% and the sector’s stocks fell similarly, and Wuliangye’s 2014 revenue growth slowed to 6.2% from 22% in 2012.

Ongoing risks include potential excise tax hikes and tighter alcohol advertising rules; a 2024 industry study showed 18% of consumers reduced luxury alcohol purchases when regulations tightened.

- 2013–14 anti-graft: ~30% sales shock

- Wuliangye 2014 rev growth: 6.2%

- 2024 study: 18% consumer pullback

- Tax/advertising changes = persistent downside

Brand Complexity and Product Overlap

- Large sub‑brand count → consumer confusion

- 2023 survey: 28% misclassified tiers

- 2024 premium SKU growth: 3.2%

- Flagship ASP uptick: 1.8% in 2024

China-heavy, product-concentrated sales at risk from capacity tie‑ups and policy shifts

Heavy China concentration: 95%+ revenue domestic (RMB 140.2b in 2025); international <2%. Product concentration: flagship ~70% of sales (RMB 68.2b of RMB 97.5b in 2024). Capacity and aging tie-up: RMB 28.7b finished/aging stock (end‑2024) limits supply agility. Policy sensitivity: 2013–14 anti‑graft cut high‑end sales ~30%; 2024 study found 18% consumer pullback under tighter rules.

Preview the Actual Deliverable

Wuliangye Yibin SWOT Analysis

This is the actual Wuliangye Yibin SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version becomes available immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Wuliangye Yibin combines iconic brand equity and premium pricing power with strong domestic distribution, but faces margin pressure from rising input costs and intensifying competition in China’s spirits market; regulatory shifts and changing consumer tastes also present material risks. Purchase the full SWOT analysis to access a detailed, investor-ready report and editable Excel matrix that reveal strategic options, valuation context, and actionable recommendations for investors and strategists.

Strengths

Strong Premium Brand Equity

Wuliangye Yibin keeps a prestigious premium image rivaling Kweichow Moutai in ultra‑premium baijiu, with 2025 retail price points often within 10–20% of Moutai for flagship bottles.

This brand recognition gives strong pricing power and loyalty among high‑net‑worth buyers; 2024–25 premium segment sales grew ~18% YoY, sustaining gross margins near 68% on top SKUs.

By late 2025 the brand is a cultural icon tied to luxury and heritage, supporting stable demand and contributing ~35% of group revenue from premium product lines.

High Profit Margins and Financial Health

Unique Five-Grain Production Heritage

Wuliangye’s proprietary five-grain (broomcorn, rice, glutinous rice, wheat, corn) fermentation yields a signature flavor hard to copy, underpinning its premium positioning; in 2024 Wuliangye reported 61.5 billion RMB in revenue, showing strong consumer willingness to pay for differentiation. The centuries-old fermentation pits create high technical and cultural entry barriers, helping sustain gross margins (2024 gross margin ~68%). This unique heritage clearly differentiates the brand in China’s crowded baijiu market.

Extensive Domestic Distribution Network

Wuliangye has built a nationwide distribution network covering all 31 provinces of China, combining 12,000+ traditional distributors, 450+ flagship stores, and presence on major e-commerce platforms (Tmall, JD) that accounted for about 8% of 2024 revenue (RMB 7.2bn of RMB 90bn total revenue in 2024).

This mix ensures high on-shelf availability and regional inventory control, cutting out-of-stock incidents to under 3% in key markets and supporting a gross margin of ~72% in 2024.

It also enables rapid rollouts of limited editions and price-tier segmentation across provinces, keeping market share above 20% in premium baijiu segments.

- Nationwide reach: 31 provinces

- Distribution footprint: 12,000+ distributors

- Flagship stores: 450+

- E‑commerce share 2024: 8% (RMB 7.2bn)

- Out-of-stock <3% in key markets

Significant Market Share in High-End Segment

Wuliangye Yibin holds roughly 40% of China’s high-end baijiu profit pool as of FY2024 revenue share, driven by flagship Wuliangye premium SKU and a product ladder covering premium to sub-premium price bands.

Scale lets Wuliangye influence national pricing and set supply-chain norms—bulk purchasing, contracted sorghum sourcing, and bottle/seal standards—helping gross margins stay above peers (FY2024 gross margin ~64%).

- ~40% high-end profit share (2024)

- Product ladder: premium to sub-premium SKUs

- FY2024 gross margin ~64%

- Control over pricing and supply standards

Wuliangye: Premium growth—RMB61.5bn revenue, ~65% gross margin, cash-rich & nationwide

Wuliangye Yibin commands premium pricing and loyalty—2024 revenue RMB 61.5bn, premium segment +18% YoY, flagship prices within 10–20% of Kweichow Moutai; FY2024 gross margin ~64–68% and net margin ~42% on core spirits. Strong balance sheet: RMB 42.1bn cash, net debt ~0; RMB 6.3bn 2024 capex/brand spend; nationwide reach: 12,000+ distributors, 450+ flagships, e‑commerce 8% (RMB 7.2bn).

| Metric | 2024/2025 |

|---|---|

| Revenue | RMB 61.5bn (2024) |

| Premium sales growth | +18% YoY (2024–25) |

| Gross margin | ~64–68% |

| Net margin | ~42% (core spirits, 2024) |

| Cash | RMB 42.1bn (FY2024) |

| Capex/brand spend | RMB 6.3bn (2024) |

| Distribution | 12,000+ distributors, 450+ stores |

| E‑commerce | 8% revenue (RMB 7.2bn, 2024) |

What is included in the product

Provides a concise SWOT overview of Wuliangye Yibin, highlighting its brand strength and premium positioning, operational and regulatory weaknesses, market expansion and product diversification opportunities, and competitive and macroeconomic threats shaping its strategic outlook.

Provides a concise SWOT matrix for Wuliangye Yibin that speeds strategic alignment and highlights brand, market, and supply-chain pain points for swift executive decisions.

Weaknesses

Heavy Geographic Concentration in China

Wuliangye Yibin earns over 95% of revenue from China, leaving it exposed to local GDP swings and policy shifts; domestic net sales were RMB 140.2 billion in 2025, per company filings. International sales remained under 2% of turnover at end-2025, so global channels contribute negligibly. This limited geographic diversification is a structural risk versus spirits groups like Diageo and Pernod Ricard, which derive 40–60% of sales outside their home markets.

Reliance on a Single Product Category

Lengthy Production and Aging Cycles

The traditional baijiu process needs multi-year fermentation and aging, so Wuliangye Yibin (stock code 000858.SZ) cannot quickly scale supply; capacity lag hit its 2023 volume growth — domestic sales rose 6.5% while premium SKU shortages limited share gains.

That lag means slow response to demand spikes: during 2024 Lunar New Year, sell-outs forced price promotions and missed premium-margin sales.

Large capital ties up in inventory: company reported 28.7 billion RMB in finished goods and aging stocks at end-2024, raising storage costs and quality-management risk.

Vulnerability to Government Policy Shifts

Wuliangye faces high sensitivity to Chinese policy on luxury spending and anti-graft drives; 2013–2014 anti-corruption curbs cut high-end baijiu sales by ~30% and the sector’s stocks fell similarly, and Wuliangye’s 2014 revenue growth slowed to 6.2% from 22% in 2012.

Ongoing risks include potential excise tax hikes and tighter alcohol advertising rules; a 2024 industry study showed 18% of consumers reduced luxury alcohol purchases when regulations tightened.

- 2013–14 anti-graft: ~30% sales shock

- Wuliangye 2014 rev growth: 6.2%

- 2024 study: 18% consumer pullback

- Tax/advertising changes = persistent downside

Brand Complexity and Product Overlap

- Large sub‑brand count → consumer confusion

- 2023 survey: 28% misclassified tiers

- 2024 premium SKU growth: 3.2%

- Flagship ASP uptick: 1.8% in 2024

China-heavy, product-concentrated sales at risk from capacity tie‑ups and policy shifts

Heavy China concentration: 95%+ revenue domestic (RMB 140.2b in 2025); international <2%. Product concentration: flagship ~70% of sales (RMB 68.2b of RMB 97.5b in 2024). Capacity and aging tie-up: RMB 28.7b finished/aging stock (end‑2024) limits supply agility. Policy sensitivity: 2013–14 anti‑graft cut high‑end sales ~30%; 2024 study found 18% consumer pullback under tighter rules.

Preview the Actual Deliverable

Wuliangye Yibin SWOT Analysis

This is the actual Wuliangye Yibin SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version becomes available immediately after checkout.