Wuxi Apptec Boston Consulting Group Matrix

Actionable Strategy Starts Here

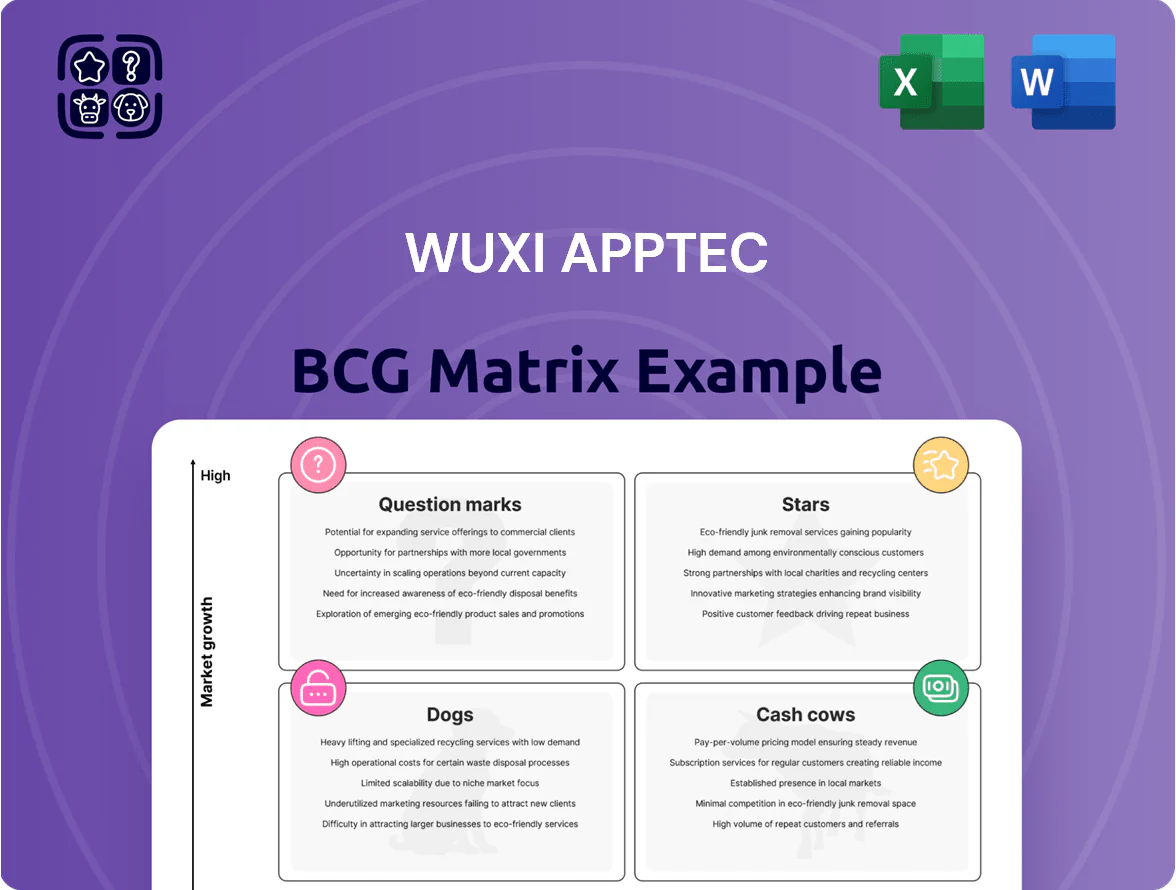

Wuxi AppTec’s preliminary BCG Matrix snapshot highlights strong Stars in high-growth biologics services, steady Cash Cows in mature CRO segments, and select Question Marks in emerging cell & gene therapy support—indicating where investment can fuel market leadership or where divestment may be prudent. This preview scratches the surface; purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use strategic report in Word + Excel to guide confident investment and portfolio decisions.

Stars

TIDES Oligonucleotide and Peptide Services

The TIDES Oligonucleotide and Peptide Services unit sits in the BCG Matrix as a star: booming peptide demand—GLP-1 agonist sales grew ~85% yoy globally in 2024 to ~$60bn—drives rapid revenue expansion for WuXi AppTec’s TIDES, which saw segment revenue rise ~72% in 2024 to an estimated $1.1bn.

WuXi AppTec has added ~40% more peptide GMP capacity between 2023–2025, investing over $600m by Q3 2025 to secure ~18% global market share in contract peptide manufacture.

High ongoing capex needs persist—management signaled another $300–450m planned for 2026—to defend margins and scale versus Catalent, Lonza and Samsung Biologics, keeping TIDES capital-intensive but growth-driving.

Integrated CRDMO Business Model

WuXi AppTec’s integrated CRDMO (contract research, development, and manufacturing organization) model captures value from discovery to commercial manufacturing, driving a reported 28% global market share in biologics outsourcing by 2024 and enabling ~20% faster time-to-market for clients per company disclosures.

That end-to-end offering secured Stars positioning in the BCG matrix, but sustaining it needs ongoing capex—WuXi invested $1.2bn in 2023–24 across biologics, cell therapy, and gene therapy platforms—to outpace niche specialists.

The vertical synergy creates a durable competitive moat: cross-selling lifted 2024 service revenues to $3.6bn, with integrated clients showing 30% higher lifetime value versus single-service customers.

AI-Driven Drug Discovery Platforms

By integrating generative AI into its chemistry and biology platforms, WuXi AppTec became a first-to-market innovator, launching AI-drug pipelines that cut lead discovery times by up to 60% in pilot projects in 2024.

Demand for AI-accelerated research is rising fast—global AI drug discovery investment hit about $7.4 billion in 2024, and clients are seeking lower R&D costs and higher success rates.

These digital platforms need heavy cash for R&D and cloud/data infrastructure—WuXi reported roughly RMB 1.1 billion in AI-related capex and data spend in 2024—but they sit in a high-growth segment where WuXi holds a dominant partner position.

The segment is key for attracting tech-forward biotech startups and big pharma, fueling service deals and long-term partnerships that bolster WuXi’s pipeline and recurring revenue streams.

High-Potency API Manufacturing

WuXi AppTec’s high-potency API (HPAPI) unit is a Star: specialized containment, advanced facilities, and strict safety protocols support a leading market share in a fast-growing oncology and targeted-therapy niche; global HPAPI CDMO demand grew ~12% CAGR to 2024, and WuXi reported >20% share in select HPAPI services in 2024.

These services command premium pricing—typical HPAPI contract margins 25–35%—but need steady reinvestment in containment tech and compliance; WuXi’s 2024 capital expenditures for advanced chemistry and containment exceeded $200M.

As targeted-medicine adoption matures, this Star should shift to a cash cow with sustained high margins and lower growth, assuming continued regulatory alignment and capacity optimization.

- Specialized containment, advanced facilities

- Leading market share; ~20%+ in select HPAPI services (2024)

- Premium margins: ~25–35%

- 2024 CAPEX on containment/chemistry >$200M

- Expected transition to cash cow as market matures

Advanced Biology and Oncology Services

WuXi AppTec leads in advanced biology and oncology services, capturing roughly 18% of the global CRO market for preclinical oncology by 2025 and benefiting from a 9% CAGR in cancer research funding (2020–2025).

The firm invests in specialized mouse models and high-content screening, adding ~$120M CAPEX in 2024 to expand in vivo and immuno-oncology platforms.

These high-end services drive premium pricing, long-term client ties, and preserve WuXi AppTec’s reputation as a top-tier scientific partner.

- ~18% preclinical oncology CRO share (2025)

- 9% CAGR in cancer research funding (2020–2025)

- $120M CAPEX for in vivo/IO in 2024

- Focus: mouse models, high-content screening

TIDES & HPAPI Surge: $1.1B TIDES, +40% peptide capacity, HPAPI >20% share

TIDES and HPAPI are Stars: TIDES revenue ~ $1.1bn (2024), 72% yoy; peptide GMP capacity +40% (2023–25); WuXi capex $1.2bn (2023–24), +$300–450m planned (2026). HPAPI >20% share in select services, margins 25–35%, CAPEX >$200m (2024).

| Metric | 2024/2025 |

|---|---|

| TIDES rev | $1.1bn |

| Peptide capacity | +40% |

| HPAPI share | >20% |

| 2023–24 capex | $1.2bn |

What is included in the product

In-depth BCG review of Wuxi AppTec: strategic moves for Stars, Cash Cows, Question Marks, and Dogs with investment, hold, divest guidance.

One-page BCG Matrix for Wuxi AppTec placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

Small Molecule Discovery Chemistry

Small Molecule Discovery Chemistry is Wuxi AppTec’s foundational business, holding roughly 30–35% global market share in discovery services as of 2025 and delivering steady revenue of about RMB 7.2 billion in 2024.

It generates strong cash flow with low incremental marketing or capex needs versus cell/gene units, returning ~18% operating margin in 2024 and funding R&D elsewhere.

The scale and efficiency in this mature segment financed ~RMB 1.6 billion of investments into cell and gene programs in 2024 and remains the main source for dividends and debt service.

Laboratory Testing and Analytical Services

WuXi Testing delivers regulatory safety and analytical services essential for every drug candidate, spanning all therapeutic areas; in 2025 the CRO/CDMO testing market was ~US$45bn and WuXi holds a leading share, driving steady, high-margin revenue.

The segment’s mature demand yields stable mid-single-digit organic growth and gross margins often above 40%, creating predictable cash flow.

Existing lab infrastructure keeps capital intensity low and operating efficiency high, with utilization rates typically 70–85%.

Cash from this business is routinely redeployed to fund WuXi’s high-growth R&D and cell/gene therapy question marks.

DMPK and ADME Research Services

The DMPK and ADME unit at WuXi AppTec is a global leader, providing standardized preclinical DMPK testing required for IND filings; it reported ~18% of 2024 revenue (~$1.05B of $5.8B) and >30% EBITDA margin, reflecting high market share in a stable market.

Competition centers on track record and reliability, not rapid innovation, so the unit acts as a cash cow: low promotional spend, predictable demand, and steady cash flow supporting R&D-intensive client relationships.

Commercial Scale Small Molecule Manufacturing

Once a drug reaches commercial stage, WuXi AppTec’s small-molecule manufacturing becomes a high-volume, high-margin cash cow, with FY2024 GMP API sales contributing roughly US$1.1bn of the company’s total revenue and gross margins near 35% on this segment.

The company’s 20+ facilities in China and 6 overseas plants handled multi-ton production runs for several top-50 global small-molecule drugs in 2024, securing long-term supply contracts that sustain steady cash inflows despite lower growth versus biologics.

Economies of scale give WuXi AppTec 20–30% lower per-unit costs versus mid-sized CDMOs, locking in market share and free cash flow that funds R&D and capacity expansion.

- FY2024 small-molecule/API revenue ~US$1.1bn

- Gross margin ~35% for commercial small molecules

- 20+ China sites, 6 overseas plants

- Per-unit cost 20–30% below mid-sized CDMOs

Biosafety Testing Services

Biosafety testing is a mature, highly regulated market where WuXi AppTec holds a dominant position via 2025 global lab network; these services underpin product release, creating steady revenue less tied to drug-discovery cycles—WuXi reported testing & services revenue of RMB 18.2bn in FY2024, ~22% of total.

The segment needs periodic tech upgrades, not blockbuster R&D spend, providing predictable margins (mid-20s percent EBITDA in 2024) and acting as a cash cow funding growth areas.

- Established market position via global labs

- Essential for product release → steady demand

- Lower R&D intensity; periodic capital upgrades

- FY2024 testing/services revenue RMB 18.2bn; EBITDA ~25%

WuXi’s high‑margin cash engines fund cell/gene R&D: Discovery, DMPK, API, Testing

WuXi’s cash cows: Small-molecule discovery (30–35% share; RMB 7.2bn revenue 2024; ~18% op margin), DMPK/ADME (~US$1.05bn 2024; >30% EBITDA), commercial API (~US$1.1bn 2024; ~35% gross margin; 20+ China, 6 overseas plants), and testing/biosafety (RMB 18.2bn 2024; ~25% EBITDA); together produce stable, high-margin cash funding cell/gene R&D.

| Unit | 2024 rev | Margin | Notes |

|---|---|---|---|

| Discovery | RMB 7.2bn | 18% op | 30–35% market |

| DMPK | US$1.05bn | >30% EBITDA | IND testing |

| API | US$1.1bn | 35% gross | 26 plants |

| Testing | RMB 18.2bn | ~25% EBITDA | Global labs |

Preview = Final Product

Wuxi Apptec BCG Matrix

The file you're previewing on this page is the final Wuxi AppTec BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report designed for clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Wuxi AppTec’s preliminary BCG Matrix snapshot highlights strong Stars in high-growth biologics services, steady Cash Cows in mature CRO segments, and select Question Marks in emerging cell & gene therapy support—indicating where investment can fuel market leadership or where divestment may be prudent. This preview scratches the surface; purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use strategic report in Word + Excel to guide confident investment and portfolio decisions.

Stars

TIDES Oligonucleotide and Peptide Services

The TIDES Oligonucleotide and Peptide Services unit sits in the BCG Matrix as a star: booming peptide demand—GLP-1 agonist sales grew ~85% yoy globally in 2024 to ~$60bn—drives rapid revenue expansion for WuXi AppTec’s TIDES, which saw segment revenue rise ~72% in 2024 to an estimated $1.1bn.

WuXi AppTec has added ~40% more peptide GMP capacity between 2023–2025, investing over $600m by Q3 2025 to secure ~18% global market share in contract peptide manufacture.

High ongoing capex needs persist—management signaled another $300–450m planned for 2026—to defend margins and scale versus Catalent, Lonza and Samsung Biologics, keeping TIDES capital-intensive but growth-driving.

Integrated CRDMO Business Model

WuXi AppTec’s integrated CRDMO (contract research, development, and manufacturing organization) model captures value from discovery to commercial manufacturing, driving a reported 28% global market share in biologics outsourcing by 2024 and enabling ~20% faster time-to-market for clients per company disclosures.

That end-to-end offering secured Stars positioning in the BCG matrix, but sustaining it needs ongoing capex—WuXi invested $1.2bn in 2023–24 across biologics, cell therapy, and gene therapy platforms—to outpace niche specialists.

The vertical synergy creates a durable competitive moat: cross-selling lifted 2024 service revenues to $3.6bn, with integrated clients showing 30% higher lifetime value versus single-service customers.

AI-Driven Drug Discovery Platforms

By integrating generative AI into its chemistry and biology platforms, WuXi AppTec became a first-to-market innovator, launching AI-drug pipelines that cut lead discovery times by up to 60% in pilot projects in 2024.

Demand for AI-accelerated research is rising fast—global AI drug discovery investment hit about $7.4 billion in 2024, and clients are seeking lower R&D costs and higher success rates.

These digital platforms need heavy cash for R&D and cloud/data infrastructure—WuXi reported roughly RMB 1.1 billion in AI-related capex and data spend in 2024—but they sit in a high-growth segment where WuXi holds a dominant partner position.

The segment is key for attracting tech-forward biotech startups and big pharma, fueling service deals and long-term partnerships that bolster WuXi’s pipeline and recurring revenue streams.

High-Potency API Manufacturing

WuXi AppTec’s high-potency API (HPAPI) unit is a Star: specialized containment, advanced facilities, and strict safety protocols support a leading market share in a fast-growing oncology and targeted-therapy niche; global HPAPI CDMO demand grew ~12% CAGR to 2024, and WuXi reported >20% share in select HPAPI services in 2024.

These services command premium pricing—typical HPAPI contract margins 25–35%—but need steady reinvestment in containment tech and compliance; WuXi’s 2024 capital expenditures for advanced chemistry and containment exceeded $200M.

As targeted-medicine adoption matures, this Star should shift to a cash cow with sustained high margins and lower growth, assuming continued regulatory alignment and capacity optimization.

- Specialized containment, advanced facilities

- Leading market share; ~20%+ in select HPAPI services (2024)

- Premium margins: ~25–35%

- 2024 CAPEX on containment/chemistry >$200M

- Expected transition to cash cow as market matures

Advanced Biology and Oncology Services

WuXi AppTec leads in advanced biology and oncology services, capturing roughly 18% of the global CRO market for preclinical oncology by 2025 and benefiting from a 9% CAGR in cancer research funding (2020–2025).

The firm invests in specialized mouse models and high-content screening, adding ~$120M CAPEX in 2024 to expand in vivo and immuno-oncology platforms.

These high-end services drive premium pricing, long-term client ties, and preserve WuXi AppTec’s reputation as a top-tier scientific partner.

- ~18% preclinical oncology CRO share (2025)

- 9% CAGR in cancer research funding (2020–2025)

- $120M CAPEX for in vivo/IO in 2024

- Focus: mouse models, high-content screening

TIDES & HPAPI Surge: $1.1B TIDES, +40% peptide capacity, HPAPI >20% share

TIDES and HPAPI are Stars: TIDES revenue ~ $1.1bn (2024), 72% yoy; peptide GMP capacity +40% (2023–25); WuXi capex $1.2bn (2023–24), +$300–450m planned (2026). HPAPI >20% share in select services, margins 25–35%, CAPEX >$200m (2024).

| Metric | 2024/2025 |

|---|---|

| TIDES rev | $1.1bn |

| Peptide capacity | +40% |

| HPAPI share | >20% |

| 2023–24 capex | $1.2bn |

What is included in the product

In-depth BCG review of Wuxi AppTec: strategic moves for Stars, Cash Cows, Question Marks, and Dogs with investment, hold, divest guidance.

One-page BCG Matrix for Wuxi AppTec placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

Small Molecule Discovery Chemistry

Small Molecule Discovery Chemistry is Wuxi AppTec’s foundational business, holding roughly 30–35% global market share in discovery services as of 2025 and delivering steady revenue of about RMB 7.2 billion in 2024.

It generates strong cash flow with low incremental marketing or capex needs versus cell/gene units, returning ~18% operating margin in 2024 and funding R&D elsewhere.

The scale and efficiency in this mature segment financed ~RMB 1.6 billion of investments into cell and gene programs in 2024 and remains the main source for dividends and debt service.

Laboratory Testing and Analytical Services

WuXi Testing delivers regulatory safety and analytical services essential for every drug candidate, spanning all therapeutic areas; in 2025 the CRO/CDMO testing market was ~US$45bn and WuXi holds a leading share, driving steady, high-margin revenue.

The segment’s mature demand yields stable mid-single-digit organic growth and gross margins often above 40%, creating predictable cash flow.

Existing lab infrastructure keeps capital intensity low and operating efficiency high, with utilization rates typically 70–85%.

Cash from this business is routinely redeployed to fund WuXi’s high-growth R&D and cell/gene therapy question marks.

DMPK and ADME Research Services

The DMPK and ADME unit at WuXi AppTec is a global leader, providing standardized preclinical DMPK testing required for IND filings; it reported ~18% of 2024 revenue (~$1.05B of $5.8B) and >30% EBITDA margin, reflecting high market share in a stable market.

Competition centers on track record and reliability, not rapid innovation, so the unit acts as a cash cow: low promotional spend, predictable demand, and steady cash flow supporting R&D-intensive client relationships.

Commercial Scale Small Molecule Manufacturing

Once a drug reaches commercial stage, WuXi AppTec’s small-molecule manufacturing becomes a high-volume, high-margin cash cow, with FY2024 GMP API sales contributing roughly US$1.1bn of the company’s total revenue and gross margins near 35% on this segment.

The company’s 20+ facilities in China and 6 overseas plants handled multi-ton production runs for several top-50 global small-molecule drugs in 2024, securing long-term supply contracts that sustain steady cash inflows despite lower growth versus biologics.

Economies of scale give WuXi AppTec 20–30% lower per-unit costs versus mid-sized CDMOs, locking in market share and free cash flow that funds R&D and capacity expansion.

- FY2024 small-molecule/API revenue ~US$1.1bn

- Gross margin ~35% for commercial small molecules

- 20+ China sites, 6 overseas plants

- Per-unit cost 20–30% below mid-sized CDMOs

Biosafety Testing Services

Biosafety testing is a mature, highly regulated market where WuXi AppTec holds a dominant position via 2025 global lab network; these services underpin product release, creating steady revenue less tied to drug-discovery cycles—WuXi reported testing & services revenue of RMB 18.2bn in FY2024, ~22% of total.

The segment needs periodic tech upgrades, not blockbuster R&D spend, providing predictable margins (mid-20s percent EBITDA in 2024) and acting as a cash cow funding growth areas.

- Established market position via global labs

- Essential for product release → steady demand

- Lower R&D intensity; periodic capital upgrades

- FY2024 testing/services revenue RMB 18.2bn; EBITDA ~25%

WuXi’s high‑margin cash engines fund cell/gene R&D: Discovery, DMPK, API, Testing

WuXi’s cash cows: Small-molecule discovery (30–35% share; RMB 7.2bn revenue 2024; ~18% op margin), DMPK/ADME (~US$1.05bn 2024; >30% EBITDA), commercial API (~US$1.1bn 2024; ~35% gross margin; 20+ China, 6 overseas plants), and testing/biosafety (RMB 18.2bn 2024; ~25% EBITDA); together produce stable, high-margin cash funding cell/gene R&D.

| Unit | 2024 rev | Margin | Notes |

|---|---|---|---|

| Discovery | RMB 7.2bn | 18% op | 30–35% market |

| DMPK | US$1.05bn | >30% EBITDA | IND testing |

| API | US$1.1bn | 35% gross | 26 plants |

| Testing | RMB 18.2bn | ~25% EBITDA | Global labs |

Preview = Final Product

Wuxi Apptec BCG Matrix

The file you're previewing on this page is the final Wuxi AppTec BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report designed for clarity and professional presentation.