Wuestenrot & Wuerttembergische Business Model Canvas

W&W Business Model Canvas: Strategic Blueprint for Bancassurance, Digital & Partnerships

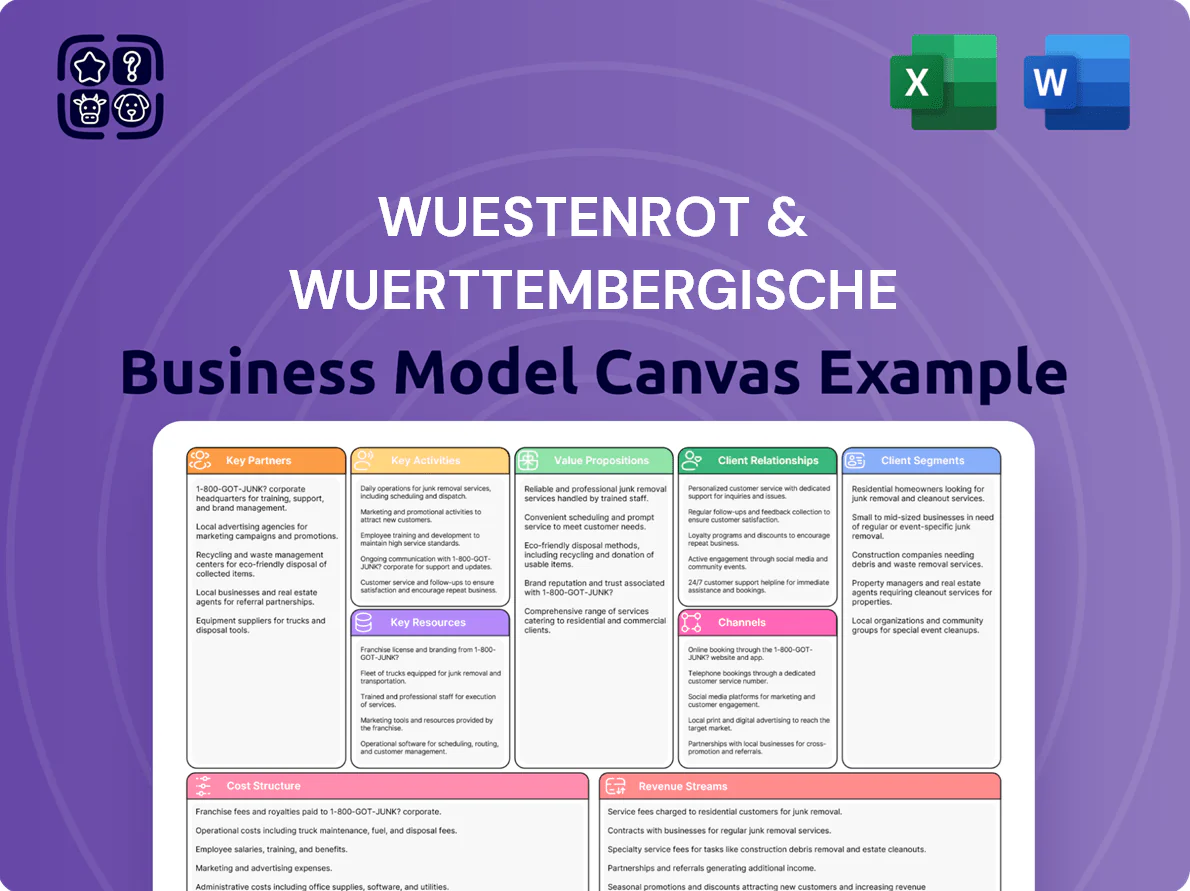

Unlock the full strategic blueprint behind Wuestenrot & Wuerttembergische’s business model — this in-depth Business Model Canvas exposes how the insurer creates customer value, monetizes products, and sustains competitive advantage across bancassurance, digital channels, and partnership ecosystems; ideal for investors, consultants, and founders seeking ready-to-use insights and templates to inform strategy and drive growth.

Partnerships

Strategic Bancassurance Alliances

W&W relies on deep bancassurance integration between Wüstenrot Bank and Württembergische Versicherung to cross-sell mortgages, savings and protection; in 2024 bancassurance sales accounted for about 38% of group new business, boosting fee and commission income by €210m. By partnering with external banks and regional Sparkassen, W&W extends reach across Germany and delivers a seamless home-savings and risk-protection experience.

Independent Sales Agencies

A vast network of ~21,000 independent agents and brokers forms Wüstenrot & Württembergische’s main customer-acquisition channel, offering local advice and long-term client ties; in 2024 these channels accounted for roughly 62% of new life and property policies by volume. W&W backs partners with CRM and mobile quoting tools plus commission models that paid €420m in intermediary commissions in 2024 to drive scale.

Real Estate and Development Partners

Collaborations with property developers and real estate agents drive Wüstenrot’s pipeline: partners referred about 35% of new home-loan leads in 2024, feeding early-stage buyers and renovators into W&W’s product suite. This lets W&W embed financing and building/home insurance during the acquisition process, lifting cross-sell rates—mortgage-to-insurance attach rose to 22% in 2024.

Fintech and Insurtech Collaborators

W&W partners with fintech and insurtech startups to automate claims (cutting average handling time by ~40% in 2024 to under 7 days) and overhaul mobile UX, aiming to lift digital NPS by 12 points and win younger customers by late 2025.

- ~40% faster claims (2024)

- target: digital NPS +12 by 2025

- reduce mobile churn among 25–35s by ~15%

Reinsurance Providers

The Württembergische insurance arm keeps strong ties with global reinsurers, ceding roughly 15–25% of catastrophe-exposed premium to limit volatility; this lets W&W offer high-cover policies while preserving regulatory capital ratios (Solvency II SCR coverage ~190% in FY2024). Effective reinsurance strategy underpins the group’s long-term solvency and calibrated risk appetite.

- 15–25% ceded catastrophe premium

- Solvency II SCR ≈190% (FY2024)

- Supports high-coverage products

W&W 2024: Bancassurance-led growth, €420m commissions, faster claims, SCR ≈190%

W&W’s key partners—bancassurance banks/Sparkassen, ~21,000 agents/brokers, developers/agents, fintechs, and global reinsurers—drove 2024 results: bancassurance = 38% new business (€210m fees), intermediated commissions €420m, 35% mortgage leads from developers, 40% faster claims (avg <7 days), 15–25% catastrophe ceded, Solvency II SCR ≈190%.

| Partner | 2024 metric |

|---|---|

| Bancassurance | 38% new business; €210m fees |

| Agents/Brokers | ~21,000; €420m commissions |

| Developers/Agents | 35% mortgage leads |

| Fintechs | Claims -40% (avg <7 days) |

| Reinsurers | 15–25% ceded; SCR ≈190% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Wüstenrot & Württembergische that maps all nine BMC blocks—customer segments, value propositions, channels, relationships, revenue streams, key resources, activities, partners, and cost structure—reflecting real-world insurance and financial-services operations, competitive strengths and risks, and tailored insights for presentations, funding discussions, and strategic decision-making.

Condenses Wüstenrot & Württembergische’s insurance and financial services strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparisons, team collaboration, and board-ready presentations.

Activities

Integrated Financial Product Development

W&W continuously redesigns its home-savings, insurance and investment lineup, targeting bancassurance bundles that cover life stages; in 2024 W&W Group reported gross premiums of €5.1bn and bancassurance sales grew ~6% YoY, reflecting this focus.

Risk Management and Underwriting

Wüstenrot & Württembergische centers underwriting on precise risk assessment and premium setting; in 2024 the group reported a combined ratio of ~95% and invested in analytics that cut claim variance by 12% year-on-year.

Asset and Wealth Management

Wüstenrot & Württembergische manages ~€60bn in insurance reserves and savings-derived assets (2024), allocating capital across bonds, equities, real estate, and alternatives to meet liabilities and client returns.

By 2025 the firm targets >30% ESG-aligned AUM, embedding ESG screens and engagement in portfolio construction to reduce carbon intensity and meet regulatory and client demand.

Digital Transformation and IT Operations

W&W maintains and upgrades its digital infrastructure to support online banking and insurance portals, spending roughly €120m on IT in 2024 and achieving 98% portal uptime.

They automate back‑office processes (RPA reduced processing time by 45% in 2023) and strengthened cybersecurity—investing €25m in 2024—reducing incidents by 60%.

- €120m IT spend 2024

- 98% portal uptime

- 45% faster processing via RPA

- €25m cybersecurity 2024

- 60% fewer security incidents

Marketing and Multi-Channel Sales

The group centralises brand and sales across branches and digital platforms, training ~4,200 advisors (2024) and running campaigns that drove a 12% YoY digital lead rise in 2024, all to keep the 'The Home Specialist' message consistent.

- 4,200 trained advisors (2024)

- 12% YoY digital lead growth (2024)

- Omnichannel mix: branches, brokers, website, apps

- Focus: consistent home-insurance/mortgage branding

W&W: €5.1bn premiums, €60bn AUM, ~95% combined ratio, scaling ESG & tech

W&W runs product design and bancassurance bundles (2024 gross premiums €5.1bn; bancassurance +6% YoY), precise underwriting (combined ratio ~95%; claim variance -12% YoY), manages ~€60bn AUM, targets >30% ESG AUM by 2025, and spent €120m on IT (98% uptime) plus €25m on cybersecurity in 2024.

| Metric | 2024 / Target |

|---|---|

| Gross premiums | €5.1bn |

| Bancassurance growth | +6% YoY |

| Combined ratio | ~95% |

| AUM | ~€60bn |

| ESG AUM target | >30% by 2025 |

| IT spend | €120m (2024) |

| Portal uptime | 98% |

| Cybersecurity spend | €25m (2024) |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Wüstenrot & Württembergische Business Model Canvas—not a mockup or sample—and it reflects the exact structure, content, and formatting you will receive after purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

W&W Business Model Canvas: Strategic Blueprint for Bancassurance, Digital & Partnerships

Unlock the full strategic blueprint behind Wuestenrot & Wuerttembergische’s business model — this in-depth Business Model Canvas exposes how the insurer creates customer value, monetizes products, and sustains competitive advantage across bancassurance, digital channels, and partnership ecosystems; ideal for investors, consultants, and founders seeking ready-to-use insights and templates to inform strategy and drive growth.

Partnerships

Strategic Bancassurance Alliances

W&W relies on deep bancassurance integration between Wüstenrot Bank and Württembergische Versicherung to cross-sell mortgages, savings and protection; in 2024 bancassurance sales accounted for about 38% of group new business, boosting fee and commission income by €210m. By partnering with external banks and regional Sparkassen, W&W extends reach across Germany and delivers a seamless home-savings and risk-protection experience.

Independent Sales Agencies

A vast network of ~21,000 independent agents and brokers forms Wüstenrot & Württembergische’s main customer-acquisition channel, offering local advice and long-term client ties; in 2024 these channels accounted for roughly 62% of new life and property policies by volume. W&W backs partners with CRM and mobile quoting tools plus commission models that paid €420m in intermediary commissions in 2024 to drive scale.

Real Estate and Development Partners

Collaborations with property developers and real estate agents drive Wüstenrot’s pipeline: partners referred about 35% of new home-loan leads in 2024, feeding early-stage buyers and renovators into W&W’s product suite. This lets W&W embed financing and building/home insurance during the acquisition process, lifting cross-sell rates—mortgage-to-insurance attach rose to 22% in 2024.

Fintech and Insurtech Collaborators

W&W partners with fintech and insurtech startups to automate claims (cutting average handling time by ~40% in 2024 to under 7 days) and overhaul mobile UX, aiming to lift digital NPS by 12 points and win younger customers by late 2025.

- ~40% faster claims (2024)

- target: digital NPS +12 by 2025

- reduce mobile churn among 25–35s by ~15%

Reinsurance Providers

The Württembergische insurance arm keeps strong ties with global reinsurers, ceding roughly 15–25% of catastrophe-exposed premium to limit volatility; this lets W&W offer high-cover policies while preserving regulatory capital ratios (Solvency II SCR coverage ~190% in FY2024). Effective reinsurance strategy underpins the group’s long-term solvency and calibrated risk appetite.

- 15–25% ceded catastrophe premium

- Solvency II SCR ≈190% (FY2024)

- Supports high-coverage products

W&W 2024: Bancassurance-led growth, €420m commissions, faster claims, SCR ≈190%

W&W’s key partners—bancassurance banks/Sparkassen, ~21,000 agents/brokers, developers/agents, fintechs, and global reinsurers—drove 2024 results: bancassurance = 38% new business (€210m fees), intermediated commissions €420m, 35% mortgage leads from developers, 40% faster claims (avg <7 days), 15–25% catastrophe ceded, Solvency II SCR ≈190%.

| Partner | 2024 metric |

|---|---|

| Bancassurance | 38% new business; €210m fees |

| Agents/Brokers | ~21,000; €420m commissions |

| Developers/Agents | 35% mortgage leads |

| Fintechs | Claims -40% (avg <7 days) |

| Reinsurers | 15–25% ceded; SCR ≈190% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Wüstenrot & Württembergische that maps all nine BMC blocks—customer segments, value propositions, channels, relationships, revenue streams, key resources, activities, partners, and cost structure—reflecting real-world insurance and financial-services operations, competitive strengths and risks, and tailored insights for presentations, funding discussions, and strategic decision-making.

Condenses Wüstenrot & Württembergische’s insurance and financial services strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparisons, team collaboration, and board-ready presentations.

Activities

Integrated Financial Product Development

W&W continuously redesigns its home-savings, insurance and investment lineup, targeting bancassurance bundles that cover life stages; in 2024 W&W Group reported gross premiums of €5.1bn and bancassurance sales grew ~6% YoY, reflecting this focus.

Risk Management and Underwriting

Wüstenrot & Württembergische centers underwriting on precise risk assessment and premium setting; in 2024 the group reported a combined ratio of ~95% and invested in analytics that cut claim variance by 12% year-on-year.

Asset and Wealth Management

Wüstenrot & Württembergische manages ~€60bn in insurance reserves and savings-derived assets (2024), allocating capital across bonds, equities, real estate, and alternatives to meet liabilities and client returns.

By 2025 the firm targets >30% ESG-aligned AUM, embedding ESG screens and engagement in portfolio construction to reduce carbon intensity and meet regulatory and client demand.

Digital Transformation and IT Operations

W&W maintains and upgrades its digital infrastructure to support online banking and insurance portals, spending roughly €120m on IT in 2024 and achieving 98% portal uptime.

They automate back‑office processes (RPA reduced processing time by 45% in 2023) and strengthened cybersecurity—investing €25m in 2024—reducing incidents by 60%.

- €120m IT spend 2024

- 98% portal uptime

- 45% faster processing via RPA

- €25m cybersecurity 2024

- 60% fewer security incidents

Marketing and Multi-Channel Sales

The group centralises brand and sales across branches and digital platforms, training ~4,200 advisors (2024) and running campaigns that drove a 12% YoY digital lead rise in 2024, all to keep the 'The Home Specialist' message consistent.

- 4,200 trained advisors (2024)

- 12% YoY digital lead growth (2024)

- Omnichannel mix: branches, brokers, website, apps

- Focus: consistent home-insurance/mortgage branding

W&W: €5.1bn premiums, €60bn AUM, ~95% combined ratio, scaling ESG & tech

W&W runs product design and bancassurance bundles (2024 gross premiums €5.1bn; bancassurance +6% YoY), precise underwriting (combined ratio ~95%; claim variance -12% YoY), manages ~€60bn AUM, targets >30% ESG AUM by 2025, and spent €120m on IT (98% uptime) plus €25m on cybersecurity in 2024.

| Metric | 2024 / Target |

|---|---|

| Gross premiums | €5.1bn |

| Bancassurance growth | +6% YoY |

| Combined ratio | ~95% |

| AUM | ~€60bn |

| ESG AUM target | >30% by 2025 |

| IT spend | €120m (2024) |

| Portal uptime | 98% |

| Cybersecurity spend | €25m (2024) |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Wüstenrot & Württembergische Business Model Canvas—not a mockup or sample—and it reflects the exact structure, content, and formatting you will receive after purchase.