Guangxi Wuzhou Zhongheng Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

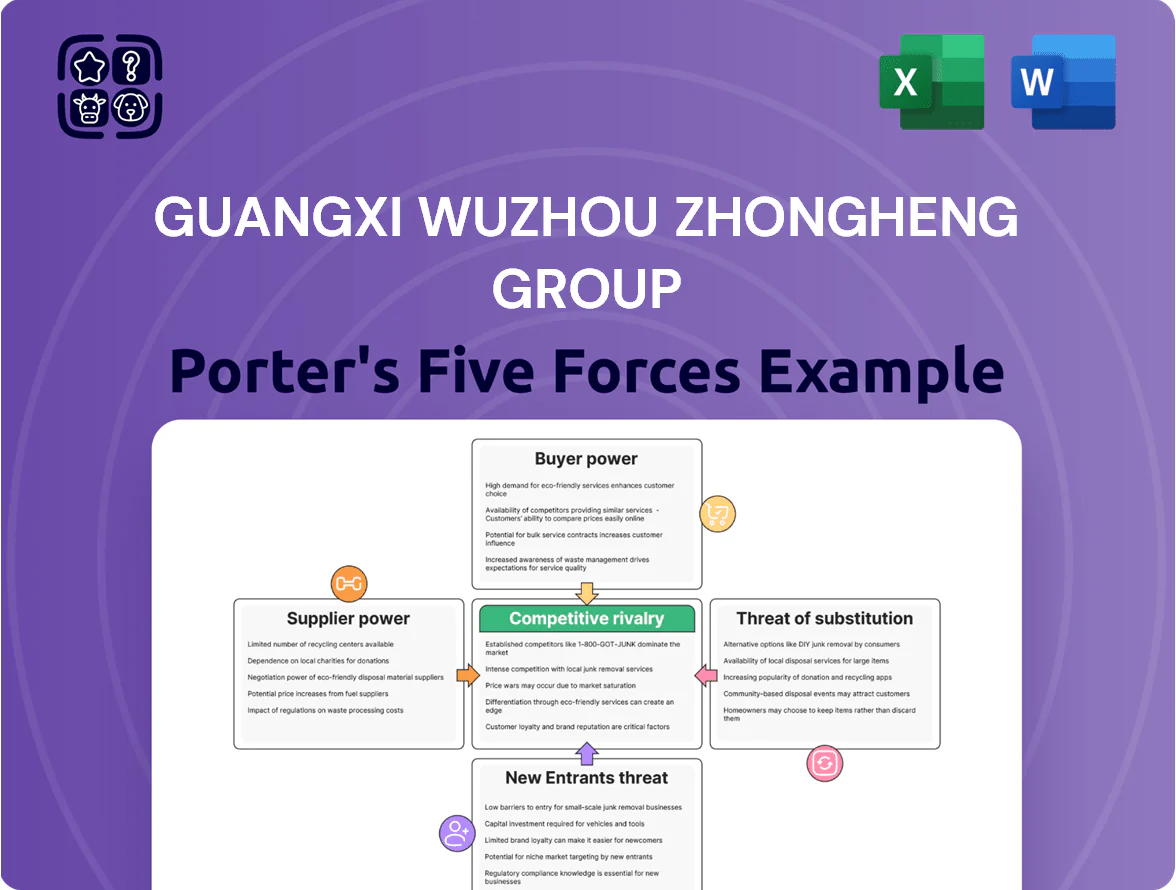

Guangxi Wuzhou Zhongheng Group faces moderate supplier power and intense rivalry in logistics and manufacturing, while barriers to entry and threat of substitutes vary across its port, shipping, and construction segments; regulatory shifts and regional infrastructure investments are key external modifiers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Guangxi Wuzhou Zhongheng Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Scarcity for Traditional Chinese Medicine

Guangxi Wuzhou Zhongheng Group depends on herbs like Panax notoginseng for Xueshuantong injections; high-grade notoginseng prices rose ~28% in 2024 due to poor yields, giving suppliers strong leverage.

Seasonal yields and Guangxi regional limits concentrate supply: top 10 herb suppliers control ~60% of quality-grade supply, so harvest swings or tighter 2023–25 environmental rules cause volatile input costs the company must absorb.

Quality Control and GAP Certification Standards

Suppliers meeting Good Agricultural Practice (GAP) are scarce, giving them strong bargaining power; in China certified GAP suppliers for medicinal plants fell ~18% from 2019–2023, tightening supply. Zhongheng Group depends on high‑purity inputs to keep pharmaceutical certifications and claimed product efficacy, so a switch risks non‑compliance and batch rejection. This reliance on a small pool raises input costs and reduces negotiation leverage, potentially cutting gross margins by several percentage points.

Vertical Integration Strategy

To curb supplier power, Guangxi Wuzhou Zhongheng Group has invested in own cultivation bases, growing its upstream asset base from 18% of raw-material sourcing in 2019 to 46% in 2024, cutting third-party buys by 38% year-on-year. By internalizing cane and herb production, the firm reduced exposure to external price spikes—raw-material cost share fell from 52% of COGS in 2020 to 41% in 2024. This shift lowers reliance on independent farmers and wholesalers and improves margin stability, trimming input-price volatility by an estimated 22% in 2024.

Energy and Packaging Costs

Energy-intensive pharma and health-food production at Guangxi Wuzhou Zhongheng Group relies on electricity, steam, and medical-grade packaging like Type I glass and alu-foil; China industrial electricity rose ~6.2% in 2024, raising utility bill pressure.

Major suppliers—state utilities and global glass/foil makers—use fixed or long-term contracts, so Zhongheng has limited bargaining power, making supplier pressure moderate but material to margins (energy ~8–12% of COGS).

- Energy costs rose ~6.2% in 2024

- Packaging (Type I glass/foil) from few global makers

- Energy ≈8–12% of COGS

- Negotiation room limited → moderate pressure

Specialized Chemical Intermediate Suppliers

For non-herbal pharmaceutical lines, Guangxi Wuzhou Zhongheng needs specialized chemical intermediates and APIs supplied by a global market concentrated among a few high-tech firms with proprietary processes, giving suppliers pricing and delivery leverage.

Supply-chain disruptions and 2024–25 regulatory tightening (e.g., China FDA inspections up 18% in 2024) amplify supplier power, raising input costs and lead-time risk for Zhongheng’s non-herbal products.

- Dependence on few suppliers

- Proprietary processes = switching costs

- 2024 supplier inspections +18% (China FDA)

- Higher input price and lead-time volatility

Zhongheng cuts supplier risk: in‑house rises to 46%, notoginseng prices +28%

Suppliers hold high power: premium Panax notoginseng prices +28% in 2024, top‑10 suppliers ≈60% supply, GAP-certified suppliers down 18% (2019–2023). Zhongheng cut third‑party sourcing from 82% (2019) to 54% (2024), raising in‑house to 46%, trimming raw‑material COGS share 52%→41% and estimated input‑price volatility −22% in 2024.

| Metric | 2019 | 2024 |

|---|---|---|

| In‑house sourcing | 18% | 46% |

| Raw‑material % of COGS | 52% | 41% |

| Notoginseng price change | — | +28% |

What is included in the product

Tailored Porter's Five Forces analysis for Guangxi Wuzhou Zhongheng Group that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market position.

A concise Porter's Five Forces snapshot for Guangxi Wuzhou Zhongheng Group—clear force ratings and action points to quickly relieve strategic uncertainty.

Customers Bargaining Power

Centralized Government Procurement

Concentration of Hospital Networks

Public hospitals and large medical institutions—responsible for roughly 70–80% of inpatient cardiovascular and gynecological procedures in Guangxi in 2024—are the primary end-users of Wuzhou Zhongheng Group’s products.

Many belong to state-owned networks that centrally tender supplies, giving collective bargaining power that compresses supplier margins by an estimated 8–15% in recent bids.

The networks’ ability to switch to generic alternatives or substitute devices strengthens negotiation on price, volume discounts, and payment terms, often extending receivable days beyond 60.

Retail Pharmacy Chain Consolidation

Retail pharmacy chains in China now account for ~48% of OTC and health supplement sales; consolidation among top 3 chains grew market share from 32% (2019) to 46% (2024), letting them demand deeper trade discounts, co-op ad spend, and shelf fees up to 8–12% of invoice value. Zhongheng must cut wholesale prices or raise promo support to retain shelf space across Guangxi’s regions, squeezing gross margins by an estimated 2–4 percentage points.

Patient Loyalty and Brand Awareness

Patient loyalty to Zhongheng’s TCM brands, especially Xueshuantong, reduces customer switching and supports steady demand; Xueshuantong accounted for about 18% of 2024 revenue, per company filings, underscoring brand-driven sales.

This loyalty gives Zhongheng modest pricing power despite generic pressure—average selling price fell just 3% year-on-year in 2024 vs. 8% for peers, per IQVIA regional data.

Brand equity and historical efficacy create repeat prescriptions, insulating margins and lowering acquisition costs.

- Xueshuantong ~18% of 2024 revenue

- ASP decline: Zhongheng -3% vs peers -8% (2024)

- Repeat-prescription share higher by ~12 ppt

Informed Consumer Base in Health Foods

Customers in Guangxi Wuzhou Zhongheng Group’s health-food segment are highly informed and price-sensitive: 72% of Chinese health-product buyers used online comparison tools in 2024, driving demand for ingredient transparency and clinical evidence.

Low switching costs plus frequent promotions and reviews mean consumers often switch brands, pressuring marketing spend and margins; online reviews influence 58% of purchases.

- 72% used online comparison tools (2024)

- 58% influenced by online reviews

- High transparency demand: clinical proof required

- Low switching cost raises marketing/pricing pressure

Zhongheng weathers steep VBP cuts via Xueshuantong brand—ASP resilience amid price pressure

Large public buyers and consolidated pharmacy chains drive down prices—VBP cut prices 20–60% (2021–24) and hospital networks shave supplier margins ~8–15%; Zhongheng relies on low‑margin volume (45% revenue, 2024) but brand Xueshuantong (18% revenue) cushions ASP decline (-3% vs peers -8%, 2024), while informed health‑product consumers (72% compare online) keep marketing pressure high.

| Metric | Value (2024) |

|---|---|

| Revenue from hospitals | 45% |

| Xueshuantong share | 18% |

| ASP change | -3% (Zhongheng) vs -8% peers |

| VBP price cuts | 20–60% |

| Pharmacy consolidation | Top3 share 46% |

| Online comparison | 72% |

Full Version Awaits

Guangxi Wuzhou Zhongheng Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Guangxi Wuzhou Zhongheng Group you’ll receive upon purchase—no placeholders or samples. The document is fully formatted, ready to download and use immediately after payment. It contains supplier and buyer dynamics, competitive rivalry, threat of entrants and substitutes, and strategic implications tailored to the company’s port operations. What you see is the final deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Guangxi Wuzhou Zhongheng Group faces moderate supplier power and intense rivalry in logistics and manufacturing, while barriers to entry and threat of substitutes vary across its port, shipping, and construction segments; regulatory shifts and regional infrastructure investments are key external modifiers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Guangxi Wuzhou Zhongheng Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Scarcity for Traditional Chinese Medicine

Guangxi Wuzhou Zhongheng Group depends on herbs like Panax notoginseng for Xueshuantong injections; high-grade notoginseng prices rose ~28% in 2024 due to poor yields, giving suppliers strong leverage.

Seasonal yields and Guangxi regional limits concentrate supply: top 10 herb suppliers control ~60% of quality-grade supply, so harvest swings or tighter 2023–25 environmental rules cause volatile input costs the company must absorb.

Quality Control and GAP Certification Standards

Suppliers meeting Good Agricultural Practice (GAP) are scarce, giving them strong bargaining power; in China certified GAP suppliers for medicinal plants fell ~18% from 2019–2023, tightening supply. Zhongheng Group depends on high‑purity inputs to keep pharmaceutical certifications and claimed product efficacy, so a switch risks non‑compliance and batch rejection. This reliance on a small pool raises input costs and reduces negotiation leverage, potentially cutting gross margins by several percentage points.

Vertical Integration Strategy

To curb supplier power, Guangxi Wuzhou Zhongheng Group has invested in own cultivation bases, growing its upstream asset base from 18% of raw-material sourcing in 2019 to 46% in 2024, cutting third-party buys by 38% year-on-year. By internalizing cane and herb production, the firm reduced exposure to external price spikes—raw-material cost share fell from 52% of COGS in 2020 to 41% in 2024. This shift lowers reliance on independent farmers and wholesalers and improves margin stability, trimming input-price volatility by an estimated 22% in 2024.

Energy and Packaging Costs

Energy-intensive pharma and health-food production at Guangxi Wuzhou Zhongheng Group relies on electricity, steam, and medical-grade packaging like Type I glass and alu-foil; China industrial electricity rose ~6.2% in 2024, raising utility bill pressure.

Major suppliers—state utilities and global glass/foil makers—use fixed or long-term contracts, so Zhongheng has limited bargaining power, making supplier pressure moderate but material to margins (energy ~8–12% of COGS).

- Energy costs rose ~6.2% in 2024

- Packaging (Type I glass/foil) from few global makers

- Energy ≈8–12% of COGS

- Negotiation room limited → moderate pressure

Specialized Chemical Intermediate Suppliers

For non-herbal pharmaceutical lines, Guangxi Wuzhou Zhongheng needs specialized chemical intermediates and APIs supplied by a global market concentrated among a few high-tech firms with proprietary processes, giving suppliers pricing and delivery leverage.

Supply-chain disruptions and 2024–25 regulatory tightening (e.g., China FDA inspections up 18% in 2024) amplify supplier power, raising input costs and lead-time risk for Zhongheng’s non-herbal products.

- Dependence on few suppliers

- Proprietary processes = switching costs

- 2024 supplier inspections +18% (China FDA)

- Higher input price and lead-time volatility

Zhongheng cuts supplier risk: in‑house rises to 46%, notoginseng prices +28%

Suppliers hold high power: premium Panax notoginseng prices +28% in 2024, top‑10 suppliers ≈60% supply, GAP-certified suppliers down 18% (2019–2023). Zhongheng cut third‑party sourcing from 82% (2019) to 54% (2024), raising in‑house to 46%, trimming raw‑material COGS share 52%→41% and estimated input‑price volatility −22% in 2024.

| Metric | 2019 | 2024 |

|---|---|---|

| In‑house sourcing | 18% | 46% |

| Raw‑material % of COGS | 52% | 41% |

| Notoginseng price change | — | +28% |

What is included in the product

Tailored Porter's Five Forces analysis for Guangxi Wuzhou Zhongheng Group that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market position.

A concise Porter's Five Forces snapshot for Guangxi Wuzhou Zhongheng Group—clear force ratings and action points to quickly relieve strategic uncertainty.

Customers Bargaining Power

Centralized Government Procurement

Concentration of Hospital Networks

Public hospitals and large medical institutions—responsible for roughly 70–80% of inpatient cardiovascular and gynecological procedures in Guangxi in 2024—are the primary end-users of Wuzhou Zhongheng Group’s products.

Many belong to state-owned networks that centrally tender supplies, giving collective bargaining power that compresses supplier margins by an estimated 8–15% in recent bids.

The networks’ ability to switch to generic alternatives or substitute devices strengthens negotiation on price, volume discounts, and payment terms, often extending receivable days beyond 60.

Retail Pharmacy Chain Consolidation

Retail pharmacy chains in China now account for ~48% of OTC and health supplement sales; consolidation among top 3 chains grew market share from 32% (2019) to 46% (2024), letting them demand deeper trade discounts, co-op ad spend, and shelf fees up to 8–12% of invoice value. Zhongheng must cut wholesale prices or raise promo support to retain shelf space across Guangxi’s regions, squeezing gross margins by an estimated 2–4 percentage points.

Patient Loyalty and Brand Awareness

Patient loyalty to Zhongheng’s TCM brands, especially Xueshuantong, reduces customer switching and supports steady demand; Xueshuantong accounted for about 18% of 2024 revenue, per company filings, underscoring brand-driven sales.

This loyalty gives Zhongheng modest pricing power despite generic pressure—average selling price fell just 3% year-on-year in 2024 vs. 8% for peers, per IQVIA regional data.

Brand equity and historical efficacy create repeat prescriptions, insulating margins and lowering acquisition costs.

- Xueshuantong ~18% of 2024 revenue

- ASP decline: Zhongheng -3% vs peers -8% (2024)

- Repeat-prescription share higher by ~12 ppt

Informed Consumer Base in Health Foods

Customers in Guangxi Wuzhou Zhongheng Group’s health-food segment are highly informed and price-sensitive: 72% of Chinese health-product buyers used online comparison tools in 2024, driving demand for ingredient transparency and clinical evidence.

Low switching costs plus frequent promotions and reviews mean consumers often switch brands, pressuring marketing spend and margins; online reviews influence 58% of purchases.

- 72% used online comparison tools (2024)

- 58% influenced by online reviews

- High transparency demand: clinical proof required

- Low switching cost raises marketing/pricing pressure

Zhongheng weathers steep VBP cuts via Xueshuantong brand—ASP resilience amid price pressure

Large public buyers and consolidated pharmacy chains drive down prices—VBP cut prices 20–60% (2021–24) and hospital networks shave supplier margins ~8–15%; Zhongheng relies on low‑margin volume (45% revenue, 2024) but brand Xueshuantong (18% revenue) cushions ASP decline (-3% vs peers -8%, 2024), while informed health‑product consumers (72% compare online) keep marketing pressure high.

| Metric | Value (2024) |

|---|---|

| Revenue from hospitals | 45% |

| Xueshuantong share | 18% |

| ASP change | -3% (Zhongheng) vs -8% peers |

| VBP price cuts | 20–60% |

| Pharmacy consolidation | Top3 share 46% |

| Online comparison | 72% |

Full Version Awaits

Guangxi Wuzhou Zhongheng Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Guangxi Wuzhou Zhongheng Group you’ll receive upon purchase—no placeholders or samples. The document is fully formatted, ready to download and use immediately after payment. It contains supplier and buyer dynamics, competitive rivalry, threat of entrants and substitutes, and strategic implications tailored to the company’s port operations. What you see is the final deliverable.