XPeng Boston Consulting Group Matrix

See the Bigger Picture

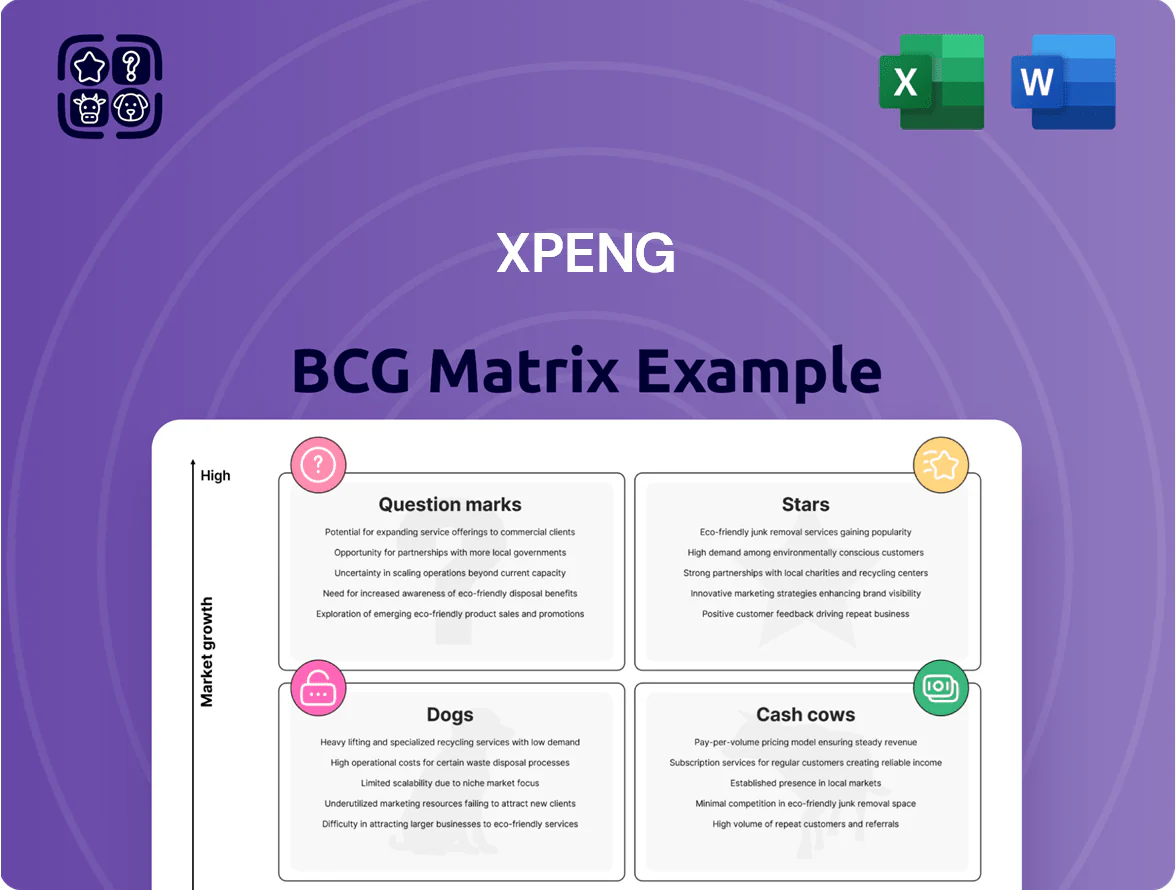

XPeng’s BCG Matrix preview highlights how its EV models and software services stack up amid rapid market shifts—identifying potential Stars in smart EV tech, Question Marks among emerging markets, and Cash Cows in established segments. This snapshot points to where XPeng should invest or divest, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable strategies, and clear capital-allocation guidance. Purchase the complete report to get an editable Word analysis plus an Excel summary for immediate use and confident decision-making.

Stars

P7+ AI Sedan

By end-2025 the P7+ AI Sedan reached ~18% share of China’s mid-to-premium smart sedan market and drove XPeng’s vehicle revenue to RMB 9.2 billion (Q4 2025 run-rate) via end-to-end AI large models enabling executive-level autonomous features.

It sits as a BCG Star: high market share and high growth—global deliveries grew 42% YoY in 2025—but escalating software R&D and annual OTA update costs near RMB 1.1 billion keep consumption high.

MONA M03 Series

As Xpeng’s mass-market push, the MONA M03 captured ~28% of China’s sub-200k EV buyers aged 22–35 by Q4 2025, selling 142,000 units in 2025 and driving 19% of Xpeng’s revenue (RMB 8.4bn) that year.

Growth was fueled by a 12.3% year-on-year rise in smart-cockpit software subscriptions and a NPS of 71; rivals BYD and Geely pressured margins, so Xpeng increased capex to RMB 6.1bn for 2026 to scale production and expand distribution to 220 cities.

G6 Ultra Smart SUV

The G6 Ultra Smart SUV remains a market leader in the global mid-size SUV segment, leveraging XPeng’s 800V silicon-carbide (SiC) platform for 10–20 minute 10–80% charging, helping lift its China and Europe market share to an estimated 6.8% in 2025 mid-size EVs. As a Star in the BCG matrix, it drives high revenue—XPeng reported G6-related line growth contributing to a 2025 H1 vehicle revenue increase of ~28%—and needs sustained capital for international logistics and 120+ localized service centers planned through 2026 to outpace legacy automakers.

XNGP Autonomous Driving Software

XNGP Autonomous Driving Software is XPeng’s proprietary ADAS platform and a prime differentiator that boosts revenue across models by attracting higher-value buyers; paid upgrades and subscriptions drove software revenue to an estimated RMB 3.2 billion in 2025 YTD, up ~65% year-over-year.

As a Star in the BCG Matrix, XNGP leads urban navigation performance but requires continuous R&D investment—XPeng spent RMB 1.1 billion on AD/AI R&D in 2024 to defend its moat and accelerate feature rollouts.

- Rapid SaaS growth: +65% YoY to ~RMB 3.2B (2025 YTD)

- R&D intensity: ~34% of software revenue reinvested (RMB 1.1B in 2024)

- Market position: top-tier urban navigation, high attachment rate across models

European Market Expansion

XPeng’s push into Northern and Western Europe drove 2024 unit sales up 85% YoY, capturing about 6% of the premium EV import segment in Norway and 3% in Germany, positioning the brand as a high-tech alternative to Audi/BMW and fueling strong volume growth.

XPeng is investing roughly €420M through 2024–25 to open 40 showrooms and meet EU safety/CO2 regulations, diverting cash but aiming to convert early adopters into stable market share.

- 85% YoY sales growth (2024)

- ~6% premium EV import share Norway, ~3% Germany

- €420M capex for 40 showrooms + compliance (2024–25)

XPeng Stars: RMB21B 2025 revenue mix; needs RMB7.2B capex + RMB1.1B/yr AD R&D

XPeng’s Stars (P7+, MONA M03, G6, XNGP) drove 2025 vehicle revenue ~RMB 17.6B and software revenue ~RMB 3.2B (+65% YoY); Stars show high share/growth but need ~RMB 7.2B capex/OTAs (2024–26) and RMB 1.1B annual AD R&D to sustain edge.

| Asset | 2025 KPI | Key Spend |

|---|---|---|

| P7+ AI Sedan | 18% mid-prem share; RMB 9.2B rev | AD R&D/OTA |

| MONA M03 | 142k units; RMB 8.4B rev | Capex RMB 6.1B |

| G6 SUV | 6.8% mid-size share; 28% line growth | Intl logistics, service centers |

| XNGP | RMB 3.2B software rev | RMB 1.1B AD R&D |

What is included in the product

BCG Matrix for XPeng: quadrant-by-quadrant strategic review highlighting Stars, Cash Cows, Question Marks, Dogs, investment/ divestment guidance and trend impacts.

One-page XPeng BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

P7 Standard Platform

The P7 Standard platform has entered maturity, holding a high market share among loyal XPeng buyers—about 18% of XPeng sales in 2024 (≈12,000 units) —so revenue is stable and predictable.

With R&D and tooling costs fully amortized by 2023, unit gross margins run near 28% and operating cash flow from the model exceeded ¥1.2 billion in 2024, funding new projects.

Marketing spend is low—roughly 40% less per unit than newer EV lines—making P7 a steady cash cow that underwrites XPeng’s next-gen investments.

Supercharging Infrastructure Network

By end-2025 XPeng’s S4/S5 supercharger network in China reached ~3,200 stations, generating stable recurring revenue—estimated CNY 1.1 billion in 2025 charging fees, with ~22% from third-party EVs and the rest from XPeng owners.

Opex for maintenance and grid costs remained ~18% of revenue, leaving high free cash flow; new capex was ~CNY 120 million in 2025, small versus revenue.

The unit now functions as a cash cow: mature demand, predictable utilization ~46% nationwide, and pricing yield supporting margin expansion and cross-sell of services.

Financial and Insurance Services

XPeng’s Financial and Insurance Services supplies auto loans, leasing, and insurance to about 35–40% of its buyers, giving it a dominant share inside the XPeng ecosystem and classification as a Cash Cow in the BCG matrix.

Operating in China’s mature auto-finance market, the unit generated roughly CNY 1.2 billion in net interest and fee income in 2024, supplying steady liquidity to service corporate debt and fund R&D.

Smart Cockpit Ecosystem

The Smart Cockpit Ecosystem in XPeng cars delivers high-margin digital revenue from third-party app integrations and paid content; XPeng reported 2024 in-car software ARPU around RMB 380 per active vehicle annually, converting hundreds of thousands of deployed units into recurring income.

With hardware already in ~300,000+ vehicles by end-2024, incremental cost to roll out services is near zero, so margins stay high and cash flows steady enough to cover corporate admin and ops.

- High-margin digital sales: ~RMB 380 ARPU (2024)

- Deployed base: ~300,000 vehicles (end-2024)

- Low incremental cost: near-zero delivery

- Provides steady cash for admin/ops

After-Sales and Maintenance Operations

As of Q4 2025, XPeng’s after-sales and maintenance, supported by a fleet exceeding 400,000 vehicles, has become a high-margin cash cow, delivering service gross margins near 35% and recurring revenue from 3-5 year service contracts covering ~28% of active owners.

These localized, essential services create a captive market with low demand elasticity, generating steady cash flows that reduced XPeng’s operating cash volatility and improved free cash flow by ~12% in 2025.

- Fleet size: >400,000 vehicles (Q4 2025)

- Service gross margin: ~35%

- Owners on service contracts: ~28%

- Contribution to FCF improvement: ~+12% (2025)

XPeng’s P7, finance & services: ~CNY3.7b cash, high margins, >400k base, funds R&D

P7, finance, in-car services, and after-sales are XPeng cash cows: combined they delivered ~CNY 3.7b operating cash in 2024–25, high margins (P7: ~28%, services: ~35%), ARPU RMB 380 (2024), deployed base >400k (Q4 2025), and low incremental capex (~CNY 120m in 2025), funding R&D and capex.

| Unit | 2024–25 |

|---|---|

| P7 sales | ~12,000 units (2024) |

| Operating cash | ~CNY 3.7b (2024–25) |

| Margins | P7 28% / Services 35% |

| ARPU | RMB 380 (2024) |

| Deployed base | >400,000 vehicles (Q4 2025) |

| Capex | ~CNY 120m (2025) |

What You’re Viewing Is Included

XPeng BCG Matrix

The file you're previewing is the exact BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document tailored for strategic use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

XPeng’s BCG Matrix preview highlights how its EV models and software services stack up amid rapid market shifts—identifying potential Stars in smart EV tech, Question Marks among emerging markets, and Cash Cows in established segments. This snapshot points to where XPeng should invest or divest, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable strategies, and clear capital-allocation guidance. Purchase the complete report to get an editable Word analysis plus an Excel summary for immediate use and confident decision-making.

Stars

P7+ AI Sedan

By end-2025 the P7+ AI Sedan reached ~18% share of China’s mid-to-premium smart sedan market and drove XPeng’s vehicle revenue to RMB 9.2 billion (Q4 2025 run-rate) via end-to-end AI large models enabling executive-level autonomous features.

It sits as a BCG Star: high market share and high growth—global deliveries grew 42% YoY in 2025—but escalating software R&D and annual OTA update costs near RMB 1.1 billion keep consumption high.

MONA M03 Series

As Xpeng’s mass-market push, the MONA M03 captured ~28% of China’s sub-200k EV buyers aged 22–35 by Q4 2025, selling 142,000 units in 2025 and driving 19% of Xpeng’s revenue (RMB 8.4bn) that year.

Growth was fueled by a 12.3% year-on-year rise in smart-cockpit software subscriptions and a NPS of 71; rivals BYD and Geely pressured margins, so Xpeng increased capex to RMB 6.1bn for 2026 to scale production and expand distribution to 220 cities.

G6 Ultra Smart SUV

The G6 Ultra Smart SUV remains a market leader in the global mid-size SUV segment, leveraging XPeng’s 800V silicon-carbide (SiC) platform for 10–20 minute 10–80% charging, helping lift its China and Europe market share to an estimated 6.8% in 2025 mid-size EVs. As a Star in the BCG matrix, it drives high revenue—XPeng reported G6-related line growth contributing to a 2025 H1 vehicle revenue increase of ~28%—and needs sustained capital for international logistics and 120+ localized service centers planned through 2026 to outpace legacy automakers.

XNGP Autonomous Driving Software

XNGP Autonomous Driving Software is XPeng’s proprietary ADAS platform and a prime differentiator that boosts revenue across models by attracting higher-value buyers; paid upgrades and subscriptions drove software revenue to an estimated RMB 3.2 billion in 2025 YTD, up ~65% year-over-year.

As a Star in the BCG Matrix, XNGP leads urban navigation performance but requires continuous R&D investment—XPeng spent RMB 1.1 billion on AD/AI R&D in 2024 to defend its moat and accelerate feature rollouts.

- Rapid SaaS growth: +65% YoY to ~RMB 3.2B (2025 YTD)

- R&D intensity: ~34% of software revenue reinvested (RMB 1.1B in 2024)

- Market position: top-tier urban navigation, high attachment rate across models

European Market Expansion

XPeng’s push into Northern and Western Europe drove 2024 unit sales up 85% YoY, capturing about 6% of the premium EV import segment in Norway and 3% in Germany, positioning the brand as a high-tech alternative to Audi/BMW and fueling strong volume growth.

XPeng is investing roughly €420M through 2024–25 to open 40 showrooms and meet EU safety/CO2 regulations, diverting cash but aiming to convert early adopters into stable market share.

- 85% YoY sales growth (2024)

- ~6% premium EV import share Norway, ~3% Germany

- €420M capex for 40 showrooms + compliance (2024–25)

XPeng Stars: RMB21B 2025 revenue mix; needs RMB7.2B capex + RMB1.1B/yr AD R&D

XPeng’s Stars (P7+, MONA M03, G6, XNGP) drove 2025 vehicle revenue ~RMB 17.6B and software revenue ~RMB 3.2B (+65% YoY); Stars show high share/growth but need ~RMB 7.2B capex/OTAs (2024–26) and RMB 1.1B annual AD R&D to sustain edge.

| Asset | 2025 KPI | Key Spend |

|---|---|---|

| P7+ AI Sedan | 18% mid-prem share; RMB 9.2B rev | AD R&D/OTA |

| MONA M03 | 142k units; RMB 8.4B rev | Capex RMB 6.1B |

| G6 SUV | 6.8% mid-size share; 28% line growth | Intl logistics, service centers |

| XNGP | RMB 3.2B software rev | RMB 1.1B AD R&D |

What is included in the product

BCG Matrix for XPeng: quadrant-by-quadrant strategic review highlighting Stars, Cash Cows, Question Marks, Dogs, investment/ divestment guidance and trend impacts.

One-page XPeng BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

P7 Standard Platform

The P7 Standard platform has entered maturity, holding a high market share among loyal XPeng buyers—about 18% of XPeng sales in 2024 (≈12,000 units) —so revenue is stable and predictable.

With R&D and tooling costs fully amortized by 2023, unit gross margins run near 28% and operating cash flow from the model exceeded ¥1.2 billion in 2024, funding new projects.

Marketing spend is low—roughly 40% less per unit than newer EV lines—making P7 a steady cash cow that underwrites XPeng’s next-gen investments.

Supercharging Infrastructure Network

By end-2025 XPeng’s S4/S5 supercharger network in China reached ~3,200 stations, generating stable recurring revenue—estimated CNY 1.1 billion in 2025 charging fees, with ~22% from third-party EVs and the rest from XPeng owners.

Opex for maintenance and grid costs remained ~18% of revenue, leaving high free cash flow; new capex was ~CNY 120 million in 2025, small versus revenue.

The unit now functions as a cash cow: mature demand, predictable utilization ~46% nationwide, and pricing yield supporting margin expansion and cross-sell of services.

Financial and Insurance Services

XPeng’s Financial and Insurance Services supplies auto loans, leasing, and insurance to about 35–40% of its buyers, giving it a dominant share inside the XPeng ecosystem and classification as a Cash Cow in the BCG matrix.

Operating in China’s mature auto-finance market, the unit generated roughly CNY 1.2 billion in net interest and fee income in 2024, supplying steady liquidity to service corporate debt and fund R&D.

Smart Cockpit Ecosystem

The Smart Cockpit Ecosystem in XPeng cars delivers high-margin digital revenue from third-party app integrations and paid content; XPeng reported 2024 in-car software ARPU around RMB 380 per active vehicle annually, converting hundreds of thousands of deployed units into recurring income.

With hardware already in ~300,000+ vehicles by end-2024, incremental cost to roll out services is near zero, so margins stay high and cash flows steady enough to cover corporate admin and ops.

- High-margin digital sales: ~RMB 380 ARPU (2024)

- Deployed base: ~300,000 vehicles (end-2024)

- Low incremental cost: near-zero delivery

- Provides steady cash for admin/ops

After-Sales and Maintenance Operations

As of Q4 2025, XPeng’s after-sales and maintenance, supported by a fleet exceeding 400,000 vehicles, has become a high-margin cash cow, delivering service gross margins near 35% and recurring revenue from 3-5 year service contracts covering ~28% of active owners.

These localized, essential services create a captive market with low demand elasticity, generating steady cash flows that reduced XPeng’s operating cash volatility and improved free cash flow by ~12% in 2025.

- Fleet size: >400,000 vehicles (Q4 2025)

- Service gross margin: ~35%

- Owners on service contracts: ~28%

- Contribution to FCF improvement: ~+12% (2025)

XPeng’s P7, finance & services: ~CNY3.7b cash, high margins, >400k base, funds R&D

P7, finance, in-car services, and after-sales are XPeng cash cows: combined they delivered ~CNY 3.7b operating cash in 2024–25, high margins (P7: ~28%, services: ~35%), ARPU RMB 380 (2024), deployed base >400k (Q4 2025), and low incremental capex (~CNY 120m in 2025), funding R&D and capex.

| Unit | 2024–25 |

|---|---|

| P7 sales | ~12,000 units (2024) |

| Operating cash | ~CNY 3.7b (2024–25) |

| Margins | P7 28% / Services 35% |

| ARPU | RMB 380 (2024) |

| Deployed base | >400,000 vehicles (Q4 2025) |

| Capex | ~CNY 120m (2025) |

What You’re Viewing Is Included

XPeng BCG Matrix

The file you're previewing is the exact BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document tailored for strategic use.