XPeng PESTLE Analysis

Your Competitive Advantage Starts with This Report

Navigate XPeng’s future with our concise PESTLE snapshot—spot regulatory, economic, and tech forces shaping its roadmap and valuation; ideal for investors and strategists seeking fast, actionable context. Purchase the full PESTLE for a detailed, editable report with risk assessments and strategic implications you can apply immediately.

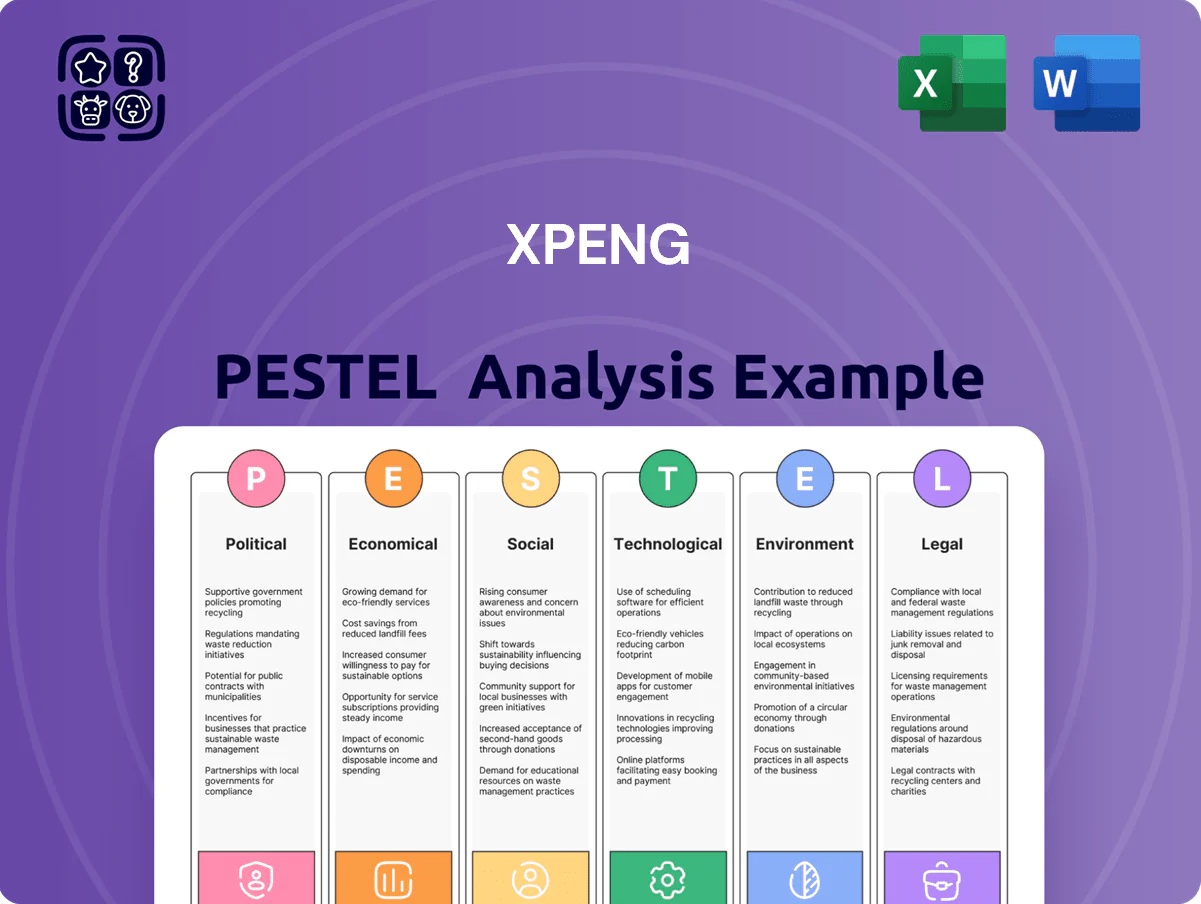

Political factors

Geopolitical trade barriers

As of late 2025, XPeng faces higher barriers as the US and EU imposed tariffs up to 25% and 20% respectively on Chinese-made EVs, aiming to protect domestic makers and raising XPeng's landed costs materially.

These protectionist levies force XPeng to revise pricing and distribution; company guidance showed international ASP pressure and potential margin contraction of 3–5 percentage points in 2025.

XPeng is exploring localized assembly and joint ventures in Europe and Southeast Asia to offset tariffs and preserve share, with two pilot partner talks reported in 2024–25.

Domestic policy support

The Chinese government lists New Energy Vehicles as a strategic pillar through 2025, targeting EV penetration rising to ~20% of new car sales by 2025; XPeng gains from R&D grants and high-tech enterprise tax preferences, which reduced effective tax rates and supported 2024 R&D spend (~RMB 8.9bn).

Global supply chain security

Political instability in lithium- and cobalt-producing regions (DRC accounts for ~70% of global cobalt refining) threatens XPeng’s production continuity, requiring inventory buffers and long-term contracts.

Western export controls on advanced semiconductors—US tightening since 2022—push XPeng toward domestic chip sourcing and suppliers in China and Taiwan to reduce supply risk.

XPeng must navigate diplomatic shifts and sanctions to protect smart-driving hardware supply chains; in 2024 the company increased local supplier spend to mitigate export-related disruptions.

Regulatory alignment on AI

The Chinese political landscape is tightening AI regulations; new rules (2023–2025 drafts and 2024 personal data law updates) require in-country storage and strict processing controls for autonomous driving data, directly affecting XPeng’s XNGP.

XPeng must certify XNGP under state security protocols and possibly localize servers; noncompliance risks delayed OTA rollouts—XPeng reported 2024 revenue RMB 22.7bn, so slowed feature deployment could hit software monetization.

- Must align XNGP with national data sovereignty and security certification

- In-country storage and processing mandates increase infrastructure costs

- Regulatory checks can delay OTA updates and time-to-market for AD features

- 2024 revenue RMB 22.7bn—software rollout delays could affect recurring revenue

Local government partnerships

XPeng maintains deep ties with local governments in Zhaoqing and Guangzhou, securing favorable land use and infrastructure support that underpinned the 2024 expansion of its Zhaoqing plant increasing capacity by ~25,000 units annually.

These partnerships were instrumental in obtaining permits for road and airborne autonomous testing, supporting R&D spend of RMB 9.3 billion in 2024.

Reliance on local authorities, however, exposes XPeng to political shifts and regional GDP targets—Guangdong provincial growth guidance of ~5% for 2025 could realign incentives and permit timelines.

- Local partnerships enabled ~25k unit capacity expansion (Zhaoqing)

- R&D investment RMB 9.3bn in 2024 supported testing approvals

- Exposure to Guangdong 2025 growth target ~5% may affect incentives

Tariffs, supply risks and China support squeeze XPeng — margins hit, localization ramps

Tariffs (US 25%, EU 20%) raised landed costs, pressuring 2025 margins by ~3–5 pts; localized assembly JV talks ongoing (2024–25). Strategic support from China (NEV target ~20% by 2025) delivered R&D tax breaks and grants—R&D spend ~RMB 9.3bn (2024). Supply risks: DRC cobalt concentration (~70% refining) and semiconductor export controls pushed XPeng to localize suppliers and servers for XNGP, raising capex and infra costs.

| Metric | Value |

|---|---|

| 2024 Revenue | RMB 22.7bn |

| 2024 R&D Spend | RMB 9.3bn |

| Zhaoqing Capacity Add | ~25,000 units |

| US/EU Tariffs | 25% / 20% |

| Cobalt Refining (DRC) | ~70% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect XPeng, with data-driven trends and region-specific context to identify risks and opportunities.

Condensed PESTLE highlights for XPeng that can be dropped into presentations or planning decks to quickly align teams on regulatory, economic, technological, social, and environmental risks and opportunities.

Economic factors

Intense market price competition

The Chinese EV market remained in a price war through 2025, pushing average selling prices down ~8% year-on-year and compressing industry gross margins to ~12% on average; XPeng cut prices on key models in 2024–25 to sustain deliveries but reported a 2025 H1 gross margin of about 10–11%. XPeng must trade off aggressive pricing to protect volume against investor pressure for a clear path to profitability after cumulative losses through 2024. The environment favors automakers with lower unit costs—BYD and Tesla's China operations showed 15–20% higher operating leverage—making efficient manufacturing and vertical integration strategic priorities for XPeng.

Cost volatility of raw materials

Fluctuations in battery-grade lithium carbonate and rare earths directly affect XPeng’s COGS; lithium carbonate rose about 40% in 2021–22 then eased, but prices spiked 25% in late 2023 amid supply tightness, complicating margins.

While battery pack costs fell roughly 15–25% from 2020–2024, sudden supply shocks or speculative moves can trigger sharp short-term increases, disrupting XPeng’s forecasts.

XPeng mitigates risk via multi-year supply contracts covering a significant portion of needs and pilots alternative chemistries (e.g., LFP and silicon-anode blends) to reduce exposure to lithium and rare-earth volatility.

Global interest rate environment

Higher global interest rates—US Fed funds at 5.25–5.50% and ECB refinancing near 4.0% in 2024—raise consumer financing costs, likely dampening demand for premium EVs and pressuring XPeng sales volumes. This trend reduces attractiveness of XPeng’s leasing and financial services, squeezing margins as monthly payments rise. XPeng’s cost of capital is sensitive to central bank policy; a 100-bp rise can materially increase future debt servicing and capex costs.

Consumer purchasing power

The broader economic recovery in China affects disposable income for XPeng’s middle-class and affluent targets; household consumption grew 4.1% year-on-year in 2024 through Q3, supporting EV demand but uneven across regions.

Slower GDP growth—China’s 2024 GDP expanded ~4.5% vs prior targets—can delay high-ticket buys, reducing sales velocity for models like G6 and X9.

XPeng tracks consumer confidence and adjusted marketing and inventory after 2024 consumer confidence dips; it links spend to monthly sales and retail inventory days.

- Household consumption +4.1% y/y (2024 Q1–Q3)

- China GDP ~4.5% (2024)

- XPeng ties marketing to consumer confidence metrics and inventory days

Currency exchange fluctuations

As XPeng grows in Europe and Southeast Asia, Renminbi volatility versus the euro, rupiah and baht affects export pricing and reported overseas revenue; 2024 FX swings saw RMB move about 3-4% vs EUR and 5-7% vs several SE Asian currencies, impacting margins on cross-border sales.

XPeng consolidates foreign revenue and uses hedging—forward contracts and currency options—to limit translation losses; in 2024 management disclosed FX hedges covering a portion of expected FX exposure to stabilize EBIT.

- RMB vs EUR volatility ~3-4% in 2024

- RMB vs select SE Asian currencies moved 5-7% in 2024

- Hedging via forwards/options used to protect margins and translated revenue

EV price war trims ASP -8% to 2025; margins squeeze as lithium spikes, consumption steadies

Price war cut ASP ~8% y/y to 2025; industry gross margin ~12%, XPeng H1 2025 ~10–11%; lithium carbonate spikes +25% late 2023; battery pack costs down 15–25% (2020–24); China consumption +4.1% (2024 Q1–Q3), GDP ~4.5% (2024); RMB vs EUR ±3–4% (2024), vs SE Asia ±5–7%; hedges via forwards/options cover part of exposure.

| Metric | Value |

|---|---|

| ASP change | -8% (to 2025) |

| XPeng GM H1 2025 | 10–11% |

| Lithium spike | +25% (late 2023) |

| China consumption | +4.1% (2024 Q1–Q3) |

Full Version Awaits

XPeng PESTLE Analysis

The preview shown here is the exact XPeng PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

The content, layout, and analysis visible in this preview are the final file you’ll download immediately after payment—no placeholders, no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Navigate XPeng’s future with our concise PESTLE snapshot—spot regulatory, economic, and tech forces shaping its roadmap and valuation; ideal for investors and strategists seeking fast, actionable context. Purchase the full PESTLE for a detailed, editable report with risk assessments and strategic implications you can apply immediately.

Political factors

Geopolitical trade barriers

As of late 2025, XPeng faces higher barriers as the US and EU imposed tariffs up to 25% and 20% respectively on Chinese-made EVs, aiming to protect domestic makers and raising XPeng's landed costs materially.

These protectionist levies force XPeng to revise pricing and distribution; company guidance showed international ASP pressure and potential margin contraction of 3–5 percentage points in 2025.

XPeng is exploring localized assembly and joint ventures in Europe and Southeast Asia to offset tariffs and preserve share, with two pilot partner talks reported in 2024–25.

Domestic policy support

The Chinese government lists New Energy Vehicles as a strategic pillar through 2025, targeting EV penetration rising to ~20% of new car sales by 2025; XPeng gains from R&D grants and high-tech enterprise tax preferences, which reduced effective tax rates and supported 2024 R&D spend (~RMB 8.9bn).

Global supply chain security

Political instability in lithium- and cobalt-producing regions (DRC accounts for ~70% of global cobalt refining) threatens XPeng’s production continuity, requiring inventory buffers and long-term contracts.

Western export controls on advanced semiconductors—US tightening since 2022—push XPeng toward domestic chip sourcing and suppliers in China and Taiwan to reduce supply risk.

XPeng must navigate diplomatic shifts and sanctions to protect smart-driving hardware supply chains; in 2024 the company increased local supplier spend to mitigate export-related disruptions.

Regulatory alignment on AI

The Chinese political landscape is tightening AI regulations; new rules (2023–2025 drafts and 2024 personal data law updates) require in-country storage and strict processing controls for autonomous driving data, directly affecting XPeng’s XNGP.

XPeng must certify XNGP under state security protocols and possibly localize servers; noncompliance risks delayed OTA rollouts—XPeng reported 2024 revenue RMB 22.7bn, so slowed feature deployment could hit software monetization.

- Must align XNGP with national data sovereignty and security certification

- In-country storage and processing mandates increase infrastructure costs

- Regulatory checks can delay OTA updates and time-to-market for AD features

- 2024 revenue RMB 22.7bn—software rollout delays could affect recurring revenue

Local government partnerships

XPeng maintains deep ties with local governments in Zhaoqing and Guangzhou, securing favorable land use and infrastructure support that underpinned the 2024 expansion of its Zhaoqing plant increasing capacity by ~25,000 units annually.

These partnerships were instrumental in obtaining permits for road and airborne autonomous testing, supporting R&D spend of RMB 9.3 billion in 2024.

Reliance on local authorities, however, exposes XPeng to political shifts and regional GDP targets—Guangdong provincial growth guidance of ~5% for 2025 could realign incentives and permit timelines.

- Local partnerships enabled ~25k unit capacity expansion (Zhaoqing)

- R&D investment RMB 9.3bn in 2024 supported testing approvals

- Exposure to Guangdong 2025 growth target ~5% may affect incentives

Tariffs, supply risks and China support squeeze XPeng — margins hit, localization ramps

Tariffs (US 25%, EU 20%) raised landed costs, pressuring 2025 margins by ~3–5 pts; localized assembly JV talks ongoing (2024–25). Strategic support from China (NEV target ~20% by 2025) delivered R&D tax breaks and grants—R&D spend ~RMB 9.3bn (2024). Supply risks: DRC cobalt concentration (~70% refining) and semiconductor export controls pushed XPeng to localize suppliers and servers for XNGP, raising capex and infra costs.

| Metric | Value |

|---|---|

| 2024 Revenue | RMB 22.7bn |

| 2024 R&D Spend | RMB 9.3bn |

| Zhaoqing Capacity Add | ~25,000 units |

| US/EU Tariffs | 25% / 20% |

| Cobalt Refining (DRC) | ~70% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect XPeng, with data-driven trends and region-specific context to identify risks and opportunities.

Condensed PESTLE highlights for XPeng that can be dropped into presentations or planning decks to quickly align teams on regulatory, economic, technological, social, and environmental risks and opportunities.

Economic factors

Intense market price competition

The Chinese EV market remained in a price war through 2025, pushing average selling prices down ~8% year-on-year and compressing industry gross margins to ~12% on average; XPeng cut prices on key models in 2024–25 to sustain deliveries but reported a 2025 H1 gross margin of about 10–11%. XPeng must trade off aggressive pricing to protect volume against investor pressure for a clear path to profitability after cumulative losses through 2024. The environment favors automakers with lower unit costs—BYD and Tesla's China operations showed 15–20% higher operating leverage—making efficient manufacturing and vertical integration strategic priorities for XPeng.

Cost volatility of raw materials

Fluctuations in battery-grade lithium carbonate and rare earths directly affect XPeng’s COGS; lithium carbonate rose about 40% in 2021–22 then eased, but prices spiked 25% in late 2023 amid supply tightness, complicating margins.

While battery pack costs fell roughly 15–25% from 2020–2024, sudden supply shocks or speculative moves can trigger sharp short-term increases, disrupting XPeng’s forecasts.

XPeng mitigates risk via multi-year supply contracts covering a significant portion of needs and pilots alternative chemistries (e.g., LFP and silicon-anode blends) to reduce exposure to lithium and rare-earth volatility.

Global interest rate environment

Higher global interest rates—US Fed funds at 5.25–5.50% and ECB refinancing near 4.0% in 2024—raise consumer financing costs, likely dampening demand for premium EVs and pressuring XPeng sales volumes. This trend reduces attractiveness of XPeng’s leasing and financial services, squeezing margins as monthly payments rise. XPeng’s cost of capital is sensitive to central bank policy; a 100-bp rise can materially increase future debt servicing and capex costs.

Consumer purchasing power

The broader economic recovery in China affects disposable income for XPeng’s middle-class and affluent targets; household consumption grew 4.1% year-on-year in 2024 through Q3, supporting EV demand but uneven across regions.

Slower GDP growth—China’s 2024 GDP expanded ~4.5% vs prior targets—can delay high-ticket buys, reducing sales velocity for models like G6 and X9.

XPeng tracks consumer confidence and adjusted marketing and inventory after 2024 consumer confidence dips; it links spend to monthly sales and retail inventory days.

- Household consumption +4.1% y/y (2024 Q1–Q3)

- China GDP ~4.5% (2024)

- XPeng ties marketing to consumer confidence metrics and inventory days

Currency exchange fluctuations

As XPeng grows in Europe and Southeast Asia, Renminbi volatility versus the euro, rupiah and baht affects export pricing and reported overseas revenue; 2024 FX swings saw RMB move about 3-4% vs EUR and 5-7% vs several SE Asian currencies, impacting margins on cross-border sales.

XPeng consolidates foreign revenue and uses hedging—forward contracts and currency options—to limit translation losses; in 2024 management disclosed FX hedges covering a portion of expected FX exposure to stabilize EBIT.

- RMB vs EUR volatility ~3-4% in 2024

- RMB vs select SE Asian currencies moved 5-7% in 2024

- Hedging via forwards/options used to protect margins and translated revenue

EV price war trims ASP -8% to 2025; margins squeeze as lithium spikes, consumption steadies

Price war cut ASP ~8% y/y to 2025; industry gross margin ~12%, XPeng H1 2025 ~10–11%; lithium carbonate spikes +25% late 2023; battery pack costs down 15–25% (2020–24); China consumption +4.1% (2024 Q1–Q3), GDP ~4.5% (2024); RMB vs EUR ±3–4% (2024), vs SE Asia ±5–7%; hedges via forwards/options cover part of exposure.

| Metric | Value |

|---|---|

| ASP change | -8% (to 2025) |

| XPeng GM H1 2025 | 10–11% |

| Lithium spike | +25% (late 2023) |

| China consumption | +4.1% (2024 Q1–Q3) |

Full Version Awaits

XPeng PESTLE Analysis

The preview shown here is the exact XPeng PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

The content, layout, and analysis visible in this preview are the final file you’ll download immediately after payment—no placeholders, no surprises.