Uxin Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Uxin faces intense buyer bargaining and rising substitute threats as online used-car platforms scale and margins compress, while supplier reliance and regulatory shifts add moderate pressure on growth and pricing power.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Uxin’s competitive dynamics, market pressures, and strategic advantages in detail.

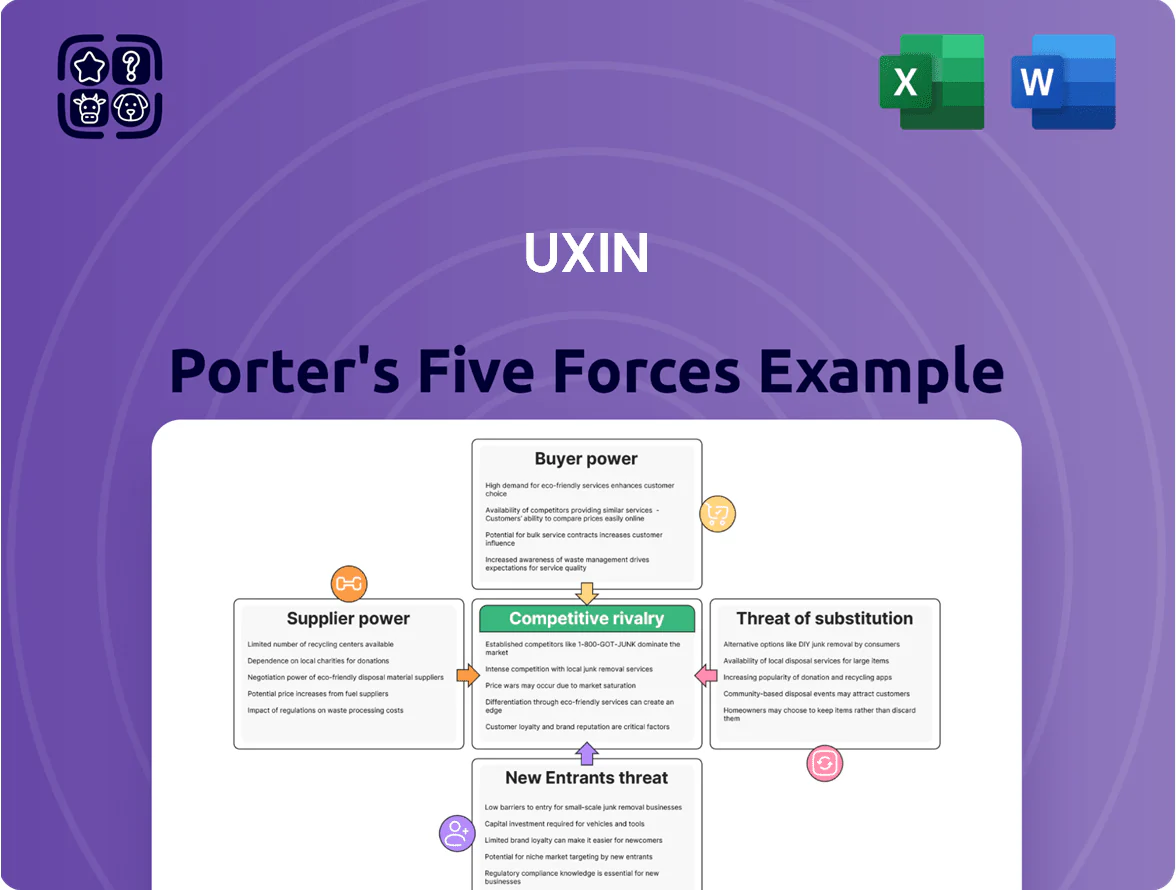

Suppliers Bargaining Power

Fragmented individual car sellers

The primary inventory for Uxin comes from millions of individual car owners selling or trading vehicles; China had about 340 million registered passenger cars by end-2024, many of which turn over each year.

Because suppliers are highly fragmented, no single owner can set prices or terms against Uxin, letting Uxin negotiate competitively for its inventory-ownership model.

Automotive parts and reconditioning vendors

Uxin’s large Inspection and Reconditioning Centers need steady spare parts and workshop equipment; regional vendors are plentiful, but suppliers for EV batteries, advanced driver-assist sensors, and luxury-model components remain concentrated—industry data shows OEM parts for EVs have 2–4 dominant suppliers per major market segment in 2024. Uxin’s 2024 scale—processing ~150,000 used cars—lets it negotiate volume discounts of 8–15% and extended payment terms (30–90 days), reducing supplier leverage.

Institutional financing and insurance partners

Uxin depends on banks and non-bank finance firms to fund consumer auto loans and insurance; in 2024 about 60–70% of its financed transactions used third‑party capital, giving suppliers strong leverage.

These partners set interest spreads and credit terms; a 100 bp rise in funding costs would raise borrower APRs materially and cut Uxin’s margins.

Credit tightening or China regulatory moves (eg 2023–24 shadow‑bank curbs) can cut loan availability and transaction volume quickly, constraining growth.

Logistics and nationwide delivery networks

Uxin’s value hinges on moving cars across China; it runs in-house logistics but relies on third-party carriers for long-distance moves, giving suppliers moderate bargaining power.

Carriers gain leverage during high fuel periods—diesel rose ~25% in 2024 vs 2023—and in regional lockdowns like Guangzhou 2022-style disruptions, raising delivery costs and delays.

- Third-party reliance raises cost exposure

- Fuel +25% in 2024 increased carrier pricing

- Regional lockdowns spike disruption risk

- Moderate supplier power; switchable but costly

Data and technology service providers

Uxin relies on cloud and analytics from large providers (Alibaba Cloud, Tencent Cloud, AWS) to run its valuation algorithms and real-time inventory; switching costs are high—enterprise migrations often exceed $5–10m and 6–18 months. In 2024 Uxin reported over 80% of transactions driven by its online platform, so supplier-backed downtime or price hikes would hit revenue and user experience hard.

- High switching cost: $5–10m, 6–18 months

- 2024: >80% transactions via online platform

- Dependence: real-time inventory, valuation accuracy

- Bargaining power: large cloud firms, limited alternatives

Uxin scale trims parts costs but rising fuel/funding could sharply compress margins

Suppliers have moderate power: fragmented car sellers limit pricing leverage, while concentrated OEM EV/ADAS parts, cloud providers (Alibaba/Tencent/AWS), carriers, and financiers (60–70% third‑party funding in 2024) raise supplier influence; Uxin’s 2024 scale (~150k cars) secures 8–15% parts discounts and 30–90 day terms, but 100bp funding hikes or 25% diesel spikes materially squeeze margins.

| Item | 2024 |

|---|---|

| Cars processed | ~150,000 |

| Third‑party funding | 60–70% |

| Parts discounts | 8–15% |

| Diesel price change | +25% |

What is included in the product

Tailored Porter's Five Forces analysis for Uxin that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its market share, supported by industry context and strategic implications.

Concise Porter's Five Forces summary tailored for Uxin—quickly identify competitive pressures and relief strategies to streamline decision-making and investor briefings.

Customers Bargaining Power

High price transparency and comparison tools

Consumers in China’s used-car market use apps like Uxin, Che168, and Autohome plus 36,000+ offline dealers, so price comparison is near-instant; a 2024 iResearch report found 68% of buyers compare prices across 3+ channels before purchase. This transparency forces Uxin to keep listing and service fees tight—Uxin reported average transaction value of RMB 72,000 in 2024, so a few hundred-yuan fee must be justified. Buyers can walk away if they find a similar car cheaper, raising customer bargaining power and pressuring Uxin’s margins and retention metrics.

Low switching costs between platforms

There are virtually no financial or technical barriers stopping buyers from switching from Uxin to rivals like Guazi or local dealers, so customer bargaining power is high; surveys in 2024 showed 62% of Chinese used-car buyers cited platform choice as interchangeable.

This low stickiness forces Uxin to spend heavily on marketing and service—Uxin's 2024 S&M rose 18% to RMB 1.2 billion—while competing on vehicle quality and post-sale guarantees to prevent churn.

Demand for comprehensive warranties and quality assurance

Used-car buyers in China now expect full transparency on vehicle history and condition; a 2024 iResearch survey found 62% would pay more for comprehensive warranties and 48% reject sellers lacking clear provenance.

Uxin’s 2C model uses standardized inspections and a 7- to 30-day return policy, yet customers still push for longer warranties and escrow-style payments.

If Uxin’s reliability metrics slip—its 2024 buyer satisfaction was 78%—buyers will shift quickly to rivals like Guazi or Carvana-style entrants seen as more trustworthy.

Availability of new energy vehicle alternatives

The fast expansion of China’s new energy vehicle (NEV) market—sales hit 8.1 million units in 2024, up 48% year-on-year—creates a strong substitute to buying used ICE cars, eroding Uxin’s pricing power.

As BYD, Tesla, and others cut entry prices (BYD Qin at ~RMB 110,000 in 2024) and offer financing incentives, used-car buyers gain negotiation leverage, forcing Uxin to accept lower margins.

- NEV sales 2024: 8.1M (+48%)

- BYD entry price ≈ RMB 110,000 (2024)

- Result: downward pressure on Uxin margins

Influence of social media and online reviews

In China’s digital market, one bad experience can go viral on WeChat, Douyin, or Xiaohongshu, and 72% of Chinese car buyers consult social reviews before purchase (2024 JD Power China auto survey), so Uxin’s reputation directly affects lead conversion and resale margins.

Customers wield collective bargaining power: negative UGC (user‑generated content) can cut platform GMV and increase CAC; Uxin needs continuous reputation spend—reviews, after‑sales service—to keep retention and referrals high.

- 72% of Chinese car buyers check social reviews (JD Power China, 2024)

- Douyin user reach ~700M monthly (ByteDance reported 2024)

- Higher negative UGC correlates with 10–15% drop in conversion in auto e‑commerce (industry analyses, 2023–24)

High buyer power and NEV price pressure squeeze Uxin margins

Buyers in China’s used‑car market have high bargaining power: 68% compare 3+ channels (iResearch 2024), 62% view platforms as interchangeable (2024 survey), and 72% check social reviews (JD Power China 2024), forcing Uxin to keep fees low, raise S&M (RMB 1.2bn in 2024) and offer warranties to prevent churn; NEV surge (8.1M sales, +48% 2024) and BYD entry pricing (~RMB 110,000) further squeeze margins.

| Metric | 2024 |

|---|---|

| Buyers comparing 3+ channels | 68% |

| Platform interchangeability | 62% |

| Check social reviews | 72% |

| Uxin S&M | RMB 1.2bn |

| NEV sales | 8.1M (+48%) |

| BYD entry price | ≈RMB 110,000 |

Preview Before You Purchase

Uxin Porter's Five Forces Analysis

This preview shows the exact Uxin Porter’s Five Forces analysis you'll receive after purchase—no placeholders, no samples.

The document displayed here is the full, professionally formatted file you’ll get instantly—ready for download and use.

You're viewing the final deliverable: the same comprehensive analysis available immediately upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Uxin faces intense buyer bargaining and rising substitute threats as online used-car platforms scale and margins compress, while supplier reliance and regulatory shifts add moderate pressure on growth and pricing power.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Uxin’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented individual car sellers

The primary inventory for Uxin comes from millions of individual car owners selling or trading vehicles; China had about 340 million registered passenger cars by end-2024, many of which turn over each year.

Because suppliers are highly fragmented, no single owner can set prices or terms against Uxin, letting Uxin negotiate competitively for its inventory-ownership model.

Automotive parts and reconditioning vendors

Uxin’s large Inspection and Reconditioning Centers need steady spare parts and workshop equipment; regional vendors are plentiful, but suppliers for EV batteries, advanced driver-assist sensors, and luxury-model components remain concentrated—industry data shows OEM parts for EVs have 2–4 dominant suppliers per major market segment in 2024. Uxin’s 2024 scale—processing ~150,000 used cars—lets it negotiate volume discounts of 8–15% and extended payment terms (30–90 days), reducing supplier leverage.

Institutional financing and insurance partners

Uxin depends on banks and non-bank finance firms to fund consumer auto loans and insurance; in 2024 about 60–70% of its financed transactions used third‑party capital, giving suppliers strong leverage.

These partners set interest spreads and credit terms; a 100 bp rise in funding costs would raise borrower APRs materially and cut Uxin’s margins.

Credit tightening or China regulatory moves (eg 2023–24 shadow‑bank curbs) can cut loan availability and transaction volume quickly, constraining growth.

Logistics and nationwide delivery networks

Uxin’s value hinges on moving cars across China; it runs in-house logistics but relies on third-party carriers for long-distance moves, giving suppliers moderate bargaining power.

Carriers gain leverage during high fuel periods—diesel rose ~25% in 2024 vs 2023—and in regional lockdowns like Guangzhou 2022-style disruptions, raising delivery costs and delays.

- Third-party reliance raises cost exposure

- Fuel +25% in 2024 increased carrier pricing

- Regional lockdowns spike disruption risk

- Moderate supplier power; switchable but costly

Data and technology service providers

Uxin relies on cloud and analytics from large providers (Alibaba Cloud, Tencent Cloud, AWS) to run its valuation algorithms and real-time inventory; switching costs are high—enterprise migrations often exceed $5–10m and 6–18 months. In 2024 Uxin reported over 80% of transactions driven by its online platform, so supplier-backed downtime or price hikes would hit revenue and user experience hard.

- High switching cost: $5–10m, 6–18 months

- 2024: >80% transactions via online platform

- Dependence: real-time inventory, valuation accuracy

- Bargaining power: large cloud firms, limited alternatives

Uxin scale trims parts costs but rising fuel/funding could sharply compress margins

Suppliers have moderate power: fragmented car sellers limit pricing leverage, while concentrated OEM EV/ADAS parts, cloud providers (Alibaba/Tencent/AWS), carriers, and financiers (60–70% third‑party funding in 2024) raise supplier influence; Uxin’s 2024 scale (~150k cars) secures 8–15% parts discounts and 30–90 day terms, but 100bp funding hikes or 25% diesel spikes materially squeeze margins.

| Item | 2024 |

|---|---|

| Cars processed | ~150,000 |

| Third‑party funding | 60–70% |

| Parts discounts | 8–15% |

| Diesel price change | +25% |

What is included in the product

Tailored Porter's Five Forces analysis for Uxin that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its market share, supported by industry context and strategic implications.

Concise Porter's Five Forces summary tailored for Uxin—quickly identify competitive pressures and relief strategies to streamline decision-making and investor briefings.

Customers Bargaining Power

High price transparency and comparison tools

Consumers in China’s used-car market use apps like Uxin, Che168, and Autohome plus 36,000+ offline dealers, so price comparison is near-instant; a 2024 iResearch report found 68% of buyers compare prices across 3+ channels before purchase. This transparency forces Uxin to keep listing and service fees tight—Uxin reported average transaction value of RMB 72,000 in 2024, so a few hundred-yuan fee must be justified. Buyers can walk away if they find a similar car cheaper, raising customer bargaining power and pressuring Uxin’s margins and retention metrics.

Low switching costs between platforms

There are virtually no financial or technical barriers stopping buyers from switching from Uxin to rivals like Guazi or local dealers, so customer bargaining power is high; surveys in 2024 showed 62% of Chinese used-car buyers cited platform choice as interchangeable.

This low stickiness forces Uxin to spend heavily on marketing and service—Uxin's 2024 S&M rose 18% to RMB 1.2 billion—while competing on vehicle quality and post-sale guarantees to prevent churn.

Demand for comprehensive warranties and quality assurance

Used-car buyers in China now expect full transparency on vehicle history and condition; a 2024 iResearch survey found 62% would pay more for comprehensive warranties and 48% reject sellers lacking clear provenance.

Uxin’s 2C model uses standardized inspections and a 7- to 30-day return policy, yet customers still push for longer warranties and escrow-style payments.

If Uxin’s reliability metrics slip—its 2024 buyer satisfaction was 78%—buyers will shift quickly to rivals like Guazi or Carvana-style entrants seen as more trustworthy.

Availability of new energy vehicle alternatives

The fast expansion of China’s new energy vehicle (NEV) market—sales hit 8.1 million units in 2024, up 48% year-on-year—creates a strong substitute to buying used ICE cars, eroding Uxin’s pricing power.

As BYD, Tesla, and others cut entry prices (BYD Qin at ~RMB 110,000 in 2024) and offer financing incentives, used-car buyers gain negotiation leverage, forcing Uxin to accept lower margins.

- NEV sales 2024: 8.1M (+48%)

- BYD entry price ≈ RMB 110,000 (2024)

- Result: downward pressure on Uxin margins

Influence of social media and online reviews

In China’s digital market, one bad experience can go viral on WeChat, Douyin, or Xiaohongshu, and 72% of Chinese car buyers consult social reviews before purchase (2024 JD Power China auto survey), so Uxin’s reputation directly affects lead conversion and resale margins.

Customers wield collective bargaining power: negative UGC (user‑generated content) can cut platform GMV and increase CAC; Uxin needs continuous reputation spend—reviews, after‑sales service—to keep retention and referrals high.

- 72% of Chinese car buyers check social reviews (JD Power China, 2024)

- Douyin user reach ~700M monthly (ByteDance reported 2024)

- Higher negative UGC correlates with 10–15% drop in conversion in auto e‑commerce (industry analyses, 2023–24)

High buyer power and NEV price pressure squeeze Uxin margins

Buyers in China’s used‑car market have high bargaining power: 68% compare 3+ channels (iResearch 2024), 62% view platforms as interchangeable (2024 survey), and 72% check social reviews (JD Power China 2024), forcing Uxin to keep fees low, raise S&M (RMB 1.2bn in 2024) and offer warranties to prevent churn; NEV surge (8.1M sales, +48% 2024) and BYD entry pricing (~RMB 110,000) further squeeze margins.

| Metric | 2024 |

|---|---|

| Buyers comparing 3+ channels | 68% |

| Platform interchangeability | 62% |

| Check social reviews | 72% |

| Uxin S&M | RMB 1.2bn |

| NEV sales | 8.1M (+48%) |

| BYD entry price | ≈RMB 110,000 |

Preview Before You Purchase

Uxin Porter's Five Forces Analysis

This preview shows the exact Uxin Porter’s Five Forces analysis you'll receive after purchase—no placeholders, no samples.

The document displayed here is the full, professionally formatted file you’ll get instantly—ready for download and use.

You're viewing the final deliverable: the same comprehensive analysis available immediately upon payment.