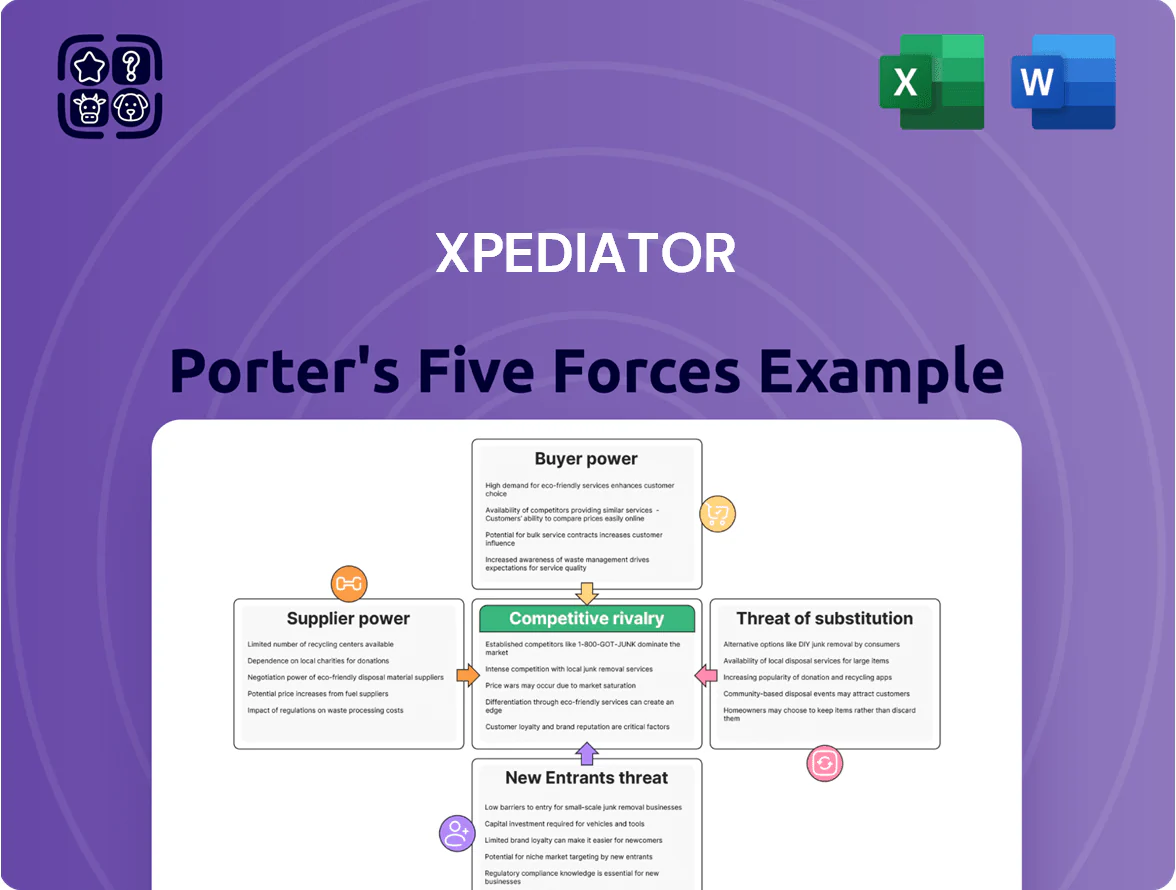

Xpediator Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Xpediator operates in a fragmented logistics market where bargaining power of buyers and threat of new entrants weigh heavily against margin compression and route specialization advantages.

Supplier dependency, regulatory shifts, and technological disruption shape competitive intensity—creating both operational risks and opportunities for differentiation through digital freight and niche services.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xpediator’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of haulage providers

The market for sub-contracted road transport in Central and Eastern Europe remains highly fragmented, with over 300,000 small hauliers in Poland and Romania in 2024, limiting individual supplier leverage.

Xpediator uses its scale—handling ~£420m revenue in 2024—to secure volume discounts and stable rates by offering consistent work to these smaller operators.

Still, rising consolidation—M&A activity up 22% in regional trucking in 2023—could increase suppliers' bargaining power over time.

Dominance of global shipping lines and airlines

Impact of specialized labor shortages

Persistent shortages of HGV drivers and warehouse staff across the UK and EU boost labor’s bargaining power; UK driver vacancies hit ~100,000 in 2024 (Road Haulage Association) and EU transport employment tightened 6.2% YoY in 2024, pushing average sector wages up 7–9% and raising Xpediator’s unit labour costs and recruitment spend. Xpediator must raise pay, invest in retention and training—else service continuity and margins suffer in this tight market.

Volatility in energy and fuel costs

Fuel is a critical input for Xpediator’s road and rail logistics, and global oil prices—Brent averaging about 88 USD/barrel in 2025—set fuel cost swings beyond supplier negotiation.

Fuel and energy suppliers hold high leverage since long‑haul heavy transport lacks scalable low‑carbon alternatives; this raises operating-cost sensitivity and margin risk.

Xpediator uses contractual fuel surcharge mechanisms to pass costs to customers, but contract caps and spot business limit full passthrough and create residual margin exposure.

- Brent ~88 USD/barrel (2025)

- Fuel surcharge common, but caps exist

- Limited large-scale alternatives for heavy transport

- Residual margin risk when passthrough restricted

Reliance on strategic infrastructure and ports

Access to key UK ports, EU gateways, and major rail terminals is concentrated among a few authorities and private operators (e.g., DP World, Associated British Ports), giving them leverage over Xpediator’s routing and costs.

These operators set fees and congestion surcharges; a 10–15% port fee hike or daily congestion surcharges (recent UK peak surcharge ~25 GBP/day in 2024) directly raise Xpediator’s unit costs and compress margins.

Limited alternative hubs mean service delays translate to inventory and detention costs for clients, reducing Xpediator’s pricing flexibility and increasing supplier bargaining power.

- Concentration: few operators control major hubs

- Fee risk: port surcharges rose ~10–15% in 2023–24

- Direct cost pass-through limited by competition

- Congestion adds daily surcharges (~25 GBP/day in 2024)

Consolidation vs fragmentation: carriers and fuel squeeze margins amid driver shortages

Supplier power is mixed: fragmented small hauliers limit leverage, but consolidation (M&A +22% in 2023) and concentrated ocean/air carriers (Maersk, MSC, CMA CGM; Emirates, Lufthansa Cargo, Qatar) raise pricing power; fuel (Brent ~88 USD/bbl in 2025), port operators (DP World, ABP) and HGV driver shortages (UK ~100,000 vacancies in 2024) create material cost and margin exposure.

| Factor | Key metric (latest) |

|---|---|

| Haulier fragmentation | ~300,000 small hauliers (PL/RO, 2024) |

| Consolidation | M&A +22% (2023) |

| Ocean carriers | Top 3 concentrate >50% capacity (2024) |

| Fuel | Brent ~88 USD/bbl (2025) |

| Driver shortage | UK ~100,000 vacancies (2024) |

| Port surcharges | Peak ~25 GBP/day (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Xpediator that uncovers competitive drivers, assesses supplier and buyer power, identifies substitutes and entry barriers, and highlights disruptive threats with strategic commentary for investor and management use.

Clear one-sheet Porter's Five Forces summary for Xpediator—ideal for fast strategic decisions and slide-ready reporting.

Customers Bargaining Power

Low switching costs for standard freight services

Low switching costs make freight forwarding and road haulage a commodity for many shippers, so buyers can move volumes to cheaper carriers quickly; industry surveys in 2024 show 62% of SMEs change providers at least annually. This forces Xpediator to prove value via on-time performance (aiming for >95% delivery reliability) or tech like real-time tracking to protect margin. The absence of long-term route lock-ins keeps pricing pressure high and buyer leverage strong.

Demand for integrated digital supply chain solutions

Volume-based negotiation leverage

Large retail and manufacturing clients drive capacity use at Xpediator, with top 10 customers historically accounting for about 45% of revenues in 2024, so they command volume discounts and extended payment terms; contracts often cut gross margins by 3–6 percentage points. Losing one major account can slash regional operating profit by double digits—Xpediator reported a 12% regional EBIT swing in 2023 after a key client exit—giving buyers clear leverage.

Sensitivity to macroeconomic fluctuations

During downturns buyers push for price cuts; UK retail spending fell 0.6% in Q4 2024, making clients more price-sensitive and likely to renegotiate Xpediator contracts.

Xpediator’s mix of e-commerce and essential-goods clients (about 44% of 2024 revenue from UK/EU retail and food logistics) cushions demand dips but industry-wide supply-chain cost-cutting still pressures margins.

Customers run competitive bids—spot rates fell ~8% YoY in European last-mile in 2024—forcing logistics providers to trim margins.

- UK retail spend −0.6% Q4 2024

- Xpediator ~44% 2024 revenue from retail/food

- European last-mile spot rates −8% YoY 2024

Expansion of in-house logistics capabilities

Large e-commerce and retail firms are insourcing logistics—Amazon, Walmart, and Alibaba expanded in-house warehousing, cutting third-party demand by an estimated 5–10% of global contracted freight volume in 2024, which shrinks Xpediator’s addressable market and raises customer bargaining power.

When these clients still outsource overflow or specialty flows, they demand lower margins and tighter SLAs; Xpediator must defend pricing by offering niche skills like complex customs brokerage, duty optimization, and tariff classification to stay indispensable.

- Insourcing cut ~5–10% contracted freight (2024 estimate)

- Overflow work drives price pressure, tighter SLAs

- Specialized customs brokerage and tariff services = key differentiator

Buyers Wield Control: Low Switching Costs, High SME Churn, Pressure on Xpediator Margins

Buyers hold strong leverage: low switching costs, 62% SME annual churn (2024), and top 10 clients = ~45% revenue (2024) force price/term pressure; 72% prioritise visibility and last-mile spot rates fell ~8% YoY (2024). Xpediator’s £86.2m 2024 revenue and 44% retail/food mix raise dependence on few large buyers, so digital features and niche customs services are critical to defend margins.

| Metric | 2024 |

|---|---|

| Revenue | £86.2m |

| Top-10 rev share | ~45% |

| Retail/food mix | 44% |

| SME churn | 62% |

| Last-mile spot rates | −8% YoY |

What You See Is What You Get

Xpediator Porter's Five Forces Analysis

This preview shows the exact Xpediator Porter's Five Forces analysis you'll receive immediately after purchase—no samples or placeholders; the full, professionally formatted document is ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Xpediator operates in a fragmented logistics market where bargaining power of buyers and threat of new entrants weigh heavily against margin compression and route specialization advantages.

Supplier dependency, regulatory shifts, and technological disruption shape competitive intensity—creating both operational risks and opportunities for differentiation through digital freight and niche services.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xpediator’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of haulage providers

The market for sub-contracted road transport in Central and Eastern Europe remains highly fragmented, with over 300,000 small hauliers in Poland and Romania in 2024, limiting individual supplier leverage.

Xpediator uses its scale—handling ~£420m revenue in 2024—to secure volume discounts and stable rates by offering consistent work to these smaller operators.

Still, rising consolidation—M&A activity up 22% in regional trucking in 2023—could increase suppliers' bargaining power over time.

Dominance of global shipping lines and airlines

Impact of specialized labor shortages

Persistent shortages of HGV drivers and warehouse staff across the UK and EU boost labor’s bargaining power; UK driver vacancies hit ~100,000 in 2024 (Road Haulage Association) and EU transport employment tightened 6.2% YoY in 2024, pushing average sector wages up 7–9% and raising Xpediator’s unit labour costs and recruitment spend. Xpediator must raise pay, invest in retention and training—else service continuity and margins suffer in this tight market.

Volatility in energy and fuel costs

Fuel is a critical input for Xpediator’s road and rail logistics, and global oil prices—Brent averaging about 88 USD/barrel in 2025—set fuel cost swings beyond supplier negotiation.

Fuel and energy suppliers hold high leverage since long‑haul heavy transport lacks scalable low‑carbon alternatives; this raises operating-cost sensitivity and margin risk.

Xpediator uses contractual fuel surcharge mechanisms to pass costs to customers, but contract caps and spot business limit full passthrough and create residual margin exposure.

- Brent ~88 USD/barrel (2025)

- Fuel surcharge common, but caps exist

- Limited large-scale alternatives for heavy transport

- Residual margin risk when passthrough restricted

Reliance on strategic infrastructure and ports

Access to key UK ports, EU gateways, and major rail terminals is concentrated among a few authorities and private operators (e.g., DP World, Associated British Ports), giving them leverage over Xpediator’s routing and costs.

These operators set fees and congestion surcharges; a 10–15% port fee hike or daily congestion surcharges (recent UK peak surcharge ~25 GBP/day in 2024) directly raise Xpediator’s unit costs and compress margins.

Limited alternative hubs mean service delays translate to inventory and detention costs for clients, reducing Xpediator’s pricing flexibility and increasing supplier bargaining power.

- Concentration: few operators control major hubs

- Fee risk: port surcharges rose ~10–15% in 2023–24

- Direct cost pass-through limited by competition

- Congestion adds daily surcharges (~25 GBP/day in 2024)

Consolidation vs fragmentation: carriers and fuel squeeze margins amid driver shortages

Supplier power is mixed: fragmented small hauliers limit leverage, but consolidation (M&A +22% in 2023) and concentrated ocean/air carriers (Maersk, MSC, CMA CGM; Emirates, Lufthansa Cargo, Qatar) raise pricing power; fuel (Brent ~88 USD/bbl in 2025), port operators (DP World, ABP) and HGV driver shortages (UK ~100,000 vacancies in 2024) create material cost and margin exposure.

| Factor | Key metric (latest) |

|---|---|

| Haulier fragmentation | ~300,000 small hauliers (PL/RO, 2024) |

| Consolidation | M&A +22% (2023) |

| Ocean carriers | Top 3 concentrate >50% capacity (2024) |

| Fuel | Brent ~88 USD/bbl (2025) |

| Driver shortage | UK ~100,000 vacancies (2024) |

| Port surcharges | Peak ~25 GBP/day (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Xpediator that uncovers competitive drivers, assesses supplier and buyer power, identifies substitutes and entry barriers, and highlights disruptive threats with strategic commentary for investor and management use.

Clear one-sheet Porter's Five Forces summary for Xpediator—ideal for fast strategic decisions and slide-ready reporting.

Customers Bargaining Power

Low switching costs for standard freight services

Low switching costs make freight forwarding and road haulage a commodity for many shippers, so buyers can move volumes to cheaper carriers quickly; industry surveys in 2024 show 62% of SMEs change providers at least annually. This forces Xpediator to prove value via on-time performance (aiming for >95% delivery reliability) or tech like real-time tracking to protect margin. The absence of long-term route lock-ins keeps pricing pressure high and buyer leverage strong.

Demand for integrated digital supply chain solutions

Volume-based negotiation leverage

Large retail and manufacturing clients drive capacity use at Xpediator, with top 10 customers historically accounting for about 45% of revenues in 2024, so they command volume discounts and extended payment terms; contracts often cut gross margins by 3–6 percentage points. Losing one major account can slash regional operating profit by double digits—Xpediator reported a 12% regional EBIT swing in 2023 after a key client exit—giving buyers clear leverage.

Sensitivity to macroeconomic fluctuations

During downturns buyers push for price cuts; UK retail spending fell 0.6% in Q4 2024, making clients more price-sensitive and likely to renegotiate Xpediator contracts.

Xpediator’s mix of e-commerce and essential-goods clients (about 44% of 2024 revenue from UK/EU retail and food logistics) cushions demand dips but industry-wide supply-chain cost-cutting still pressures margins.

Customers run competitive bids—spot rates fell ~8% YoY in European last-mile in 2024—forcing logistics providers to trim margins.

- UK retail spend −0.6% Q4 2024

- Xpediator ~44% 2024 revenue from retail/food

- European last-mile spot rates −8% YoY 2024

Expansion of in-house logistics capabilities

Large e-commerce and retail firms are insourcing logistics—Amazon, Walmart, and Alibaba expanded in-house warehousing, cutting third-party demand by an estimated 5–10% of global contracted freight volume in 2024, which shrinks Xpediator’s addressable market and raises customer bargaining power.

When these clients still outsource overflow or specialty flows, they demand lower margins and tighter SLAs; Xpediator must defend pricing by offering niche skills like complex customs brokerage, duty optimization, and tariff classification to stay indispensable.

- Insourcing cut ~5–10% contracted freight (2024 estimate)

- Overflow work drives price pressure, tighter SLAs

- Specialized customs brokerage and tariff services = key differentiator

Buyers Wield Control: Low Switching Costs, High SME Churn, Pressure on Xpediator Margins

Buyers hold strong leverage: low switching costs, 62% SME annual churn (2024), and top 10 clients = ~45% revenue (2024) force price/term pressure; 72% prioritise visibility and last-mile spot rates fell ~8% YoY (2024). Xpediator’s £86.2m 2024 revenue and 44% retail/food mix raise dependence on few large buyers, so digital features and niche customs services are critical to defend margins.

| Metric | 2024 |

|---|---|

| Revenue | £86.2m |

| Top-10 rev share | ~45% |

| Retail/food mix | 44% |

| SME churn | 62% |

| Last-mile spot rates | −8% YoY |

What You See Is What You Get

Xpediator Porter's Five Forces Analysis

This preview shows the exact Xpediator Porter's Five Forces analysis you'll receive immediately after purchase—no samples or placeholders; the full, professionally formatted document is ready for download and use the moment you buy.