XPEL Porter's Five Forces Analysis

From Overview to Strategy Blueprint

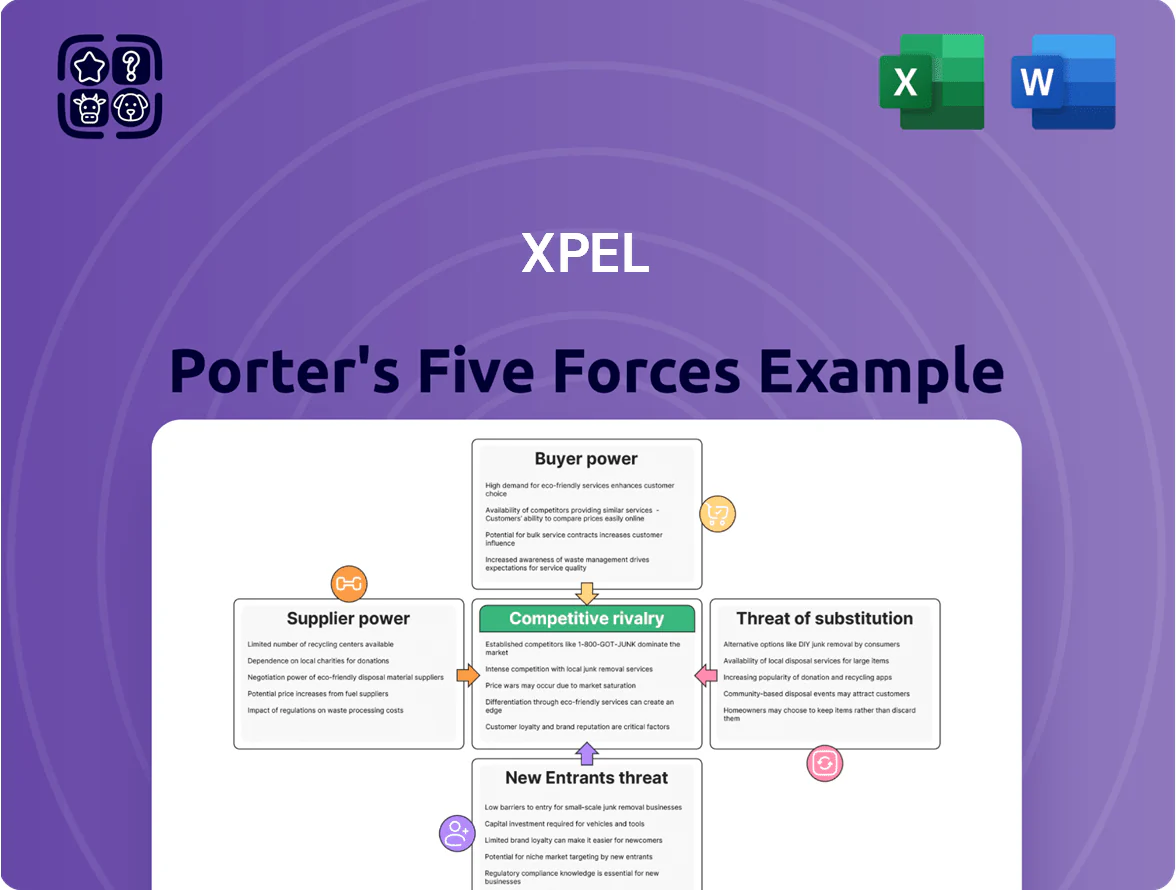

XPEL faces moderate supplier power, evolving buyer expectations, niche substitute threats, and scaling barriers that shape its competitive edge—this snapshot teases the strategic depth available in the full Porter's Five Forces Analysis. Unlock the complete report to see quantified force ratings, visuals, and actionable implications to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentration of specialized film manufacturers

XPEL depends on a small set of specialized film makers for its proprietary aliphatic polyurethane designs; by 2025 it sourced from about 3–5 approved global suppliers, downing single-supplier risk but not eliminating it.

The technical know-how for premium high-performance polymers is concentrated among a few chemical giants (e.g., Covestro, Evonik scale), giving suppliers moderate leverage when demand for such polymers swings.

Supply tightness in 2021–24 raised film input prices ~8–12% annually at peaks; similar volatility could compress XPEL gross margins if suppliers reallocate capacity to industrial or EV sectors.

Reliance on proprietary manufacturing partnerships

XPEL relies on exclusive manufacturing agreements for its paint protection films and window tints, embedding proprietary adhesive and top-coat IP that competitors cannot replicate quickly. Any supplier price hike or disruption directly pressures gross margins—XPEL reported a 2024 gross margin of ~44.5%, so a 200–300 bp supplier cost rise would cut EPS noticeably. Switching vendors needs months of testing and validation, raising operational risk and short-term COGS volatility.

Volatility in petrochemical raw material costs

Primary film resins are petrochemical-derived, so XPEL's COGS tracks crude oil: Brent rose ~38% from Jan 2024 to Dec 2025, lifting resin input costs by an estimated 22% and squeezing gross margin if not passed to buyers.

Suppliers typically pass commodity hikes to distributors; XPEL faces trade-offs between absorbing costs or raising installer prices, risking volume loss—price elasticity for aftermarket films ~ -0.6 in recent studies.

By late 2025, regional geopolitical shifts—notably reduced Middle East exports and higher LNG prices—made input costs a recurring negotiation point, increasing supplier leverage during short supply windows.

Technological exclusivity of chemical components

Suppliers of advanced ceramic particles and UV-resistant resins hold pricing power due to unique performance traits; in 2024, specialty-ceramic markets grew 6.8% to $7.2B, concentrating supply among few chemical giants.

If a supplier patents self-healing or clarity gains, they can charge premiums XPEL must match to stay competitive, raising input costs and margin pressure.

XPEL depends on R&D pipelines of major chemical firms—about 60–70% of high-performance additives come from top 5 suppliers—creating strategic vulnerability.

- Specialty ceramics market $7.2B in 2024, +6.8%

- Top 5 suppliers supply ~60–70% of additives

- Patent breakthroughs enable premium pricing

- Input-concentration raises margin and supply risk

High switching costs for specialized production lines

Transitioning suppliers for XPEL’s large-scale paint protection and window tint films needs 6–18 months and capex often >$2–5M to retool lines to XPEL’s proprietary patterns, creating high switching costs.

Those hurdles reduce supplier churn, giving existing manufacturers steadier volumes and bargaining power, typically managed via 3–5 year contracts that allow price tweaks for CPI-linked inflation.

- 6–18 month lead time

- $2–5M capex per line

- 3–5 year contracts

- Price adjustments tied to CPI

Supplier concentration and resin price surge threaten XPEL’s ~44.5% margin

Suppliers hold moderate-to-high bargaining power: 3–5 approved global film makers and top 5 additive suppliers supply ~60–70% of inputs, creating concentration and 6–18 month switching lead times with $2–5M retooling costs; commodity-linked resin costs rose ~22% after Brent +38% (Jan 2024–Dec 2025), so a 200–300 bp input cost rise would materially cut XPEL’s 2024 gross margin of ~44.5%.

| Metric | Value |

|---|---|

| Approved suppliers | 3–5 |

| Top-5 share (additives) | 60–70% |

| Switch lead time | 6–18 months |

| Retooling capex/line | $2–5M |

| Brent Jan24–Dec25 | +38% |

| Resin cost rise | ~22% |

| 2024 gross margin | ~44.5% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks specific to XPEL, highlighting substitutes, disruptive threats, and strategic levers that affect its pricing, profitability, and competitive positioning.

Condensed Porter's Five Forces for XPEL—one-sheet clarity to quickly gauge competitive pressure and prioritize strategic moves.

Customers Bargaining Power

Fragmentation of the independent installer base

The majority of XPEL’s customers are independent detailers and small shops that individually buy low volumes, so they have limited leverage to demand price cuts or special terms.

These businesses depend on XPEL’s brand to attract consumers—XPEL reported over 3,000 certified installers worldwide by end-2025—keeping installer bargaining power low.

XPEL’s training, technical support, and co-marketing programs increase switching costs and embed the brand into daily operations, reinforcing supplier advantage.

Increasing influence of large dealership groups

As XPEL expands into national dealership networks, large groups wield greater leverage, securing volume discounts and priority logistics that independent shops lack.

By late 2025, consolidation cut dealer count but increased average order size; top 10 dealer groups accounted for ~28% of U.S. new-vehicle retail in 2024, forcing XPEL to trade margin for distribution reach.

Low switching costs for multi-brand installation shops

Many professional installers hold certifications across multiple paint protection film brands, so they can switch recommendations quickly if price or supply shifts; industry surveys in 2024 show ~62% of U.S. installers certify with 2+ brands.

If a rival launches a rebate or integrates with shop management software, installers can pivot with minimal friction—XPEL faced a 4% market-share decline in select U.S. regions in 2023 after competitor promotions.

This low switching cost forces XPEL to invest in service and product reliability; XPEL reported 2024 R&D and support spending of $18.7 million as part of that response.

Consumer brand awareness and pull-through demand

XPEL’s direct-to-consumer spend drove brand pull: by 2024 the company reported 28% CAGR in branded retail leads, and installers increasingly face consumers who request XPEL by name, shifting bargaining power away from shops.

This consumer-driven demand forces installers to stock XPEL to avoid lost jobs, limiting installer price pressure and supporting XPEL’s premium wholesale pricing and higher gross margins (FY2024 gross margin 48.1%).

- 2024: 28% CAGR in branded leads

- FY2024 gross margin 48.1%

- Installer must carry product when end-user requests it

Price transparency and digital comparison tools

By late 2025, online forums and marketplaces let installers and consumers compare paint protection film (PPF) brands and pricing; searches for PPF reviews grew ~38% year-over-year through 2024–25 per Google Trends, increasing buyer price sensitivity.

This transparency lets buyers contest unbacked price hikes; XPEL must prove pricing via measurable gains—e.g., 15%+ durability or 20% faster install times—to avoid churn and maintain dealer margins.

- Comparisons up 38% (Google Trends, 2024–25)

- Install time improvements target: 20% faster

- Durability uplift needed: ≥15%

- Risk: unsubstantiated price rises → higher churn

XPEL: Brand pull and 3,000+ installers counter dealer pricing pressure

Customers mostly small installers with low per-shop volumes, so limited leverage; however dealer consolidation raised group bargaining—top dealer groups drove pricing pressure by 2025. XPEL’s 3,000+ certified installers (end‑2025), DTC branded leads CAGR 28% (to 2024), FY2024 gross margin 48.1%, R&D/support $18.7M (2024) shift power back to XPEL via brand pull.

| Metric | Value |

|---|---|

| Certified installers | 3,000+ |

| Branded leads CAGR | 28% (to 2024) |

| FY2024 gross margin | 48.1% |

| R&D & support (2024) | $18.7M |

Preview the Actual Deliverable

XPEL Porter's Five Forces Analysis

This preview shows the exact XPEL Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full, professionally formatted report you’ll get—ready for download and use the moment you buy.

No mockups or samples: this is the final deliverable and will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

XPEL faces moderate supplier power, evolving buyer expectations, niche substitute threats, and scaling barriers that shape its competitive edge—this snapshot teases the strategic depth available in the full Porter's Five Forces Analysis. Unlock the complete report to see quantified force ratings, visuals, and actionable implications to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentration of specialized film manufacturers

XPEL depends on a small set of specialized film makers for its proprietary aliphatic polyurethane designs; by 2025 it sourced from about 3–5 approved global suppliers, downing single-supplier risk but not eliminating it.

The technical know-how for premium high-performance polymers is concentrated among a few chemical giants (e.g., Covestro, Evonik scale), giving suppliers moderate leverage when demand for such polymers swings.

Supply tightness in 2021–24 raised film input prices ~8–12% annually at peaks; similar volatility could compress XPEL gross margins if suppliers reallocate capacity to industrial or EV sectors.

Reliance on proprietary manufacturing partnerships

XPEL relies on exclusive manufacturing agreements for its paint protection films and window tints, embedding proprietary adhesive and top-coat IP that competitors cannot replicate quickly. Any supplier price hike or disruption directly pressures gross margins—XPEL reported a 2024 gross margin of ~44.5%, so a 200–300 bp supplier cost rise would cut EPS noticeably. Switching vendors needs months of testing and validation, raising operational risk and short-term COGS volatility.

Volatility in petrochemical raw material costs

Primary film resins are petrochemical-derived, so XPEL's COGS tracks crude oil: Brent rose ~38% from Jan 2024 to Dec 2025, lifting resin input costs by an estimated 22% and squeezing gross margin if not passed to buyers.

Suppliers typically pass commodity hikes to distributors; XPEL faces trade-offs between absorbing costs or raising installer prices, risking volume loss—price elasticity for aftermarket films ~ -0.6 in recent studies.

By late 2025, regional geopolitical shifts—notably reduced Middle East exports and higher LNG prices—made input costs a recurring negotiation point, increasing supplier leverage during short supply windows.

Technological exclusivity of chemical components

Suppliers of advanced ceramic particles and UV-resistant resins hold pricing power due to unique performance traits; in 2024, specialty-ceramic markets grew 6.8% to $7.2B, concentrating supply among few chemical giants.

If a supplier patents self-healing or clarity gains, they can charge premiums XPEL must match to stay competitive, raising input costs and margin pressure.

XPEL depends on R&D pipelines of major chemical firms—about 60–70% of high-performance additives come from top 5 suppliers—creating strategic vulnerability.

- Specialty ceramics market $7.2B in 2024, +6.8%

- Top 5 suppliers supply ~60–70% of additives

- Patent breakthroughs enable premium pricing

- Input-concentration raises margin and supply risk

High switching costs for specialized production lines

Transitioning suppliers for XPEL’s large-scale paint protection and window tint films needs 6–18 months and capex often >$2–5M to retool lines to XPEL’s proprietary patterns, creating high switching costs.

Those hurdles reduce supplier churn, giving existing manufacturers steadier volumes and bargaining power, typically managed via 3–5 year contracts that allow price tweaks for CPI-linked inflation.

- 6–18 month lead time

- $2–5M capex per line

- 3–5 year contracts

- Price adjustments tied to CPI

Supplier concentration and resin price surge threaten XPEL’s ~44.5% margin

Suppliers hold moderate-to-high bargaining power: 3–5 approved global film makers and top 5 additive suppliers supply ~60–70% of inputs, creating concentration and 6–18 month switching lead times with $2–5M retooling costs; commodity-linked resin costs rose ~22% after Brent +38% (Jan 2024–Dec 2025), so a 200–300 bp input cost rise would materially cut XPEL’s 2024 gross margin of ~44.5%.

| Metric | Value |

|---|---|

| Approved suppliers | 3–5 |

| Top-5 share (additives) | 60–70% |

| Switch lead time | 6–18 months |

| Retooling capex/line | $2–5M |

| Brent Jan24–Dec25 | +38% |

| Resin cost rise | ~22% |

| 2024 gross margin | ~44.5% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks specific to XPEL, highlighting substitutes, disruptive threats, and strategic levers that affect its pricing, profitability, and competitive positioning.

Condensed Porter's Five Forces for XPEL—one-sheet clarity to quickly gauge competitive pressure and prioritize strategic moves.

Customers Bargaining Power

Fragmentation of the independent installer base

The majority of XPEL’s customers are independent detailers and small shops that individually buy low volumes, so they have limited leverage to demand price cuts or special terms.

These businesses depend on XPEL’s brand to attract consumers—XPEL reported over 3,000 certified installers worldwide by end-2025—keeping installer bargaining power low.

XPEL’s training, technical support, and co-marketing programs increase switching costs and embed the brand into daily operations, reinforcing supplier advantage.

Increasing influence of large dealership groups

As XPEL expands into national dealership networks, large groups wield greater leverage, securing volume discounts and priority logistics that independent shops lack.

By late 2025, consolidation cut dealer count but increased average order size; top 10 dealer groups accounted for ~28% of U.S. new-vehicle retail in 2024, forcing XPEL to trade margin for distribution reach.

Low switching costs for multi-brand installation shops

Many professional installers hold certifications across multiple paint protection film brands, so they can switch recommendations quickly if price or supply shifts; industry surveys in 2024 show ~62% of U.S. installers certify with 2+ brands.

If a rival launches a rebate or integrates with shop management software, installers can pivot with minimal friction—XPEL faced a 4% market-share decline in select U.S. regions in 2023 after competitor promotions.

This low switching cost forces XPEL to invest in service and product reliability; XPEL reported 2024 R&D and support spending of $18.7 million as part of that response.

Consumer brand awareness and pull-through demand

XPEL’s direct-to-consumer spend drove brand pull: by 2024 the company reported 28% CAGR in branded retail leads, and installers increasingly face consumers who request XPEL by name, shifting bargaining power away from shops.

This consumer-driven demand forces installers to stock XPEL to avoid lost jobs, limiting installer price pressure and supporting XPEL’s premium wholesale pricing and higher gross margins (FY2024 gross margin 48.1%).

- 2024: 28% CAGR in branded leads

- FY2024 gross margin 48.1%

- Installer must carry product when end-user requests it

Price transparency and digital comparison tools

By late 2025, online forums and marketplaces let installers and consumers compare paint protection film (PPF) brands and pricing; searches for PPF reviews grew ~38% year-over-year through 2024–25 per Google Trends, increasing buyer price sensitivity.

This transparency lets buyers contest unbacked price hikes; XPEL must prove pricing via measurable gains—e.g., 15%+ durability or 20% faster install times—to avoid churn and maintain dealer margins.

- Comparisons up 38% (Google Trends, 2024–25)

- Install time improvements target: 20% faster

- Durability uplift needed: ≥15%

- Risk: unsubstantiated price rises → higher churn

XPEL: Brand pull and 3,000+ installers counter dealer pricing pressure

Customers mostly small installers with low per-shop volumes, so limited leverage; however dealer consolidation raised group bargaining—top dealer groups drove pricing pressure by 2025. XPEL’s 3,000+ certified installers (end‑2025), DTC branded leads CAGR 28% (to 2024), FY2024 gross margin 48.1%, R&D/support $18.7M (2024) shift power back to XPEL via brand pull.

| Metric | Value |

|---|---|

| Certified installers | 3,000+ |

| Branded leads CAGR | 28% (to 2024) |

| FY2024 gross margin | 48.1% |

| R&D & support (2024) | $18.7M |

Preview the Actual Deliverable

XPEL Porter's Five Forces Analysis

This preview shows the exact XPEL Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full, professionally formatted report you’ll get—ready for download and use the moment you buy.

No mockups or samples: this is the final deliverable and will be available to you instantly after payment.