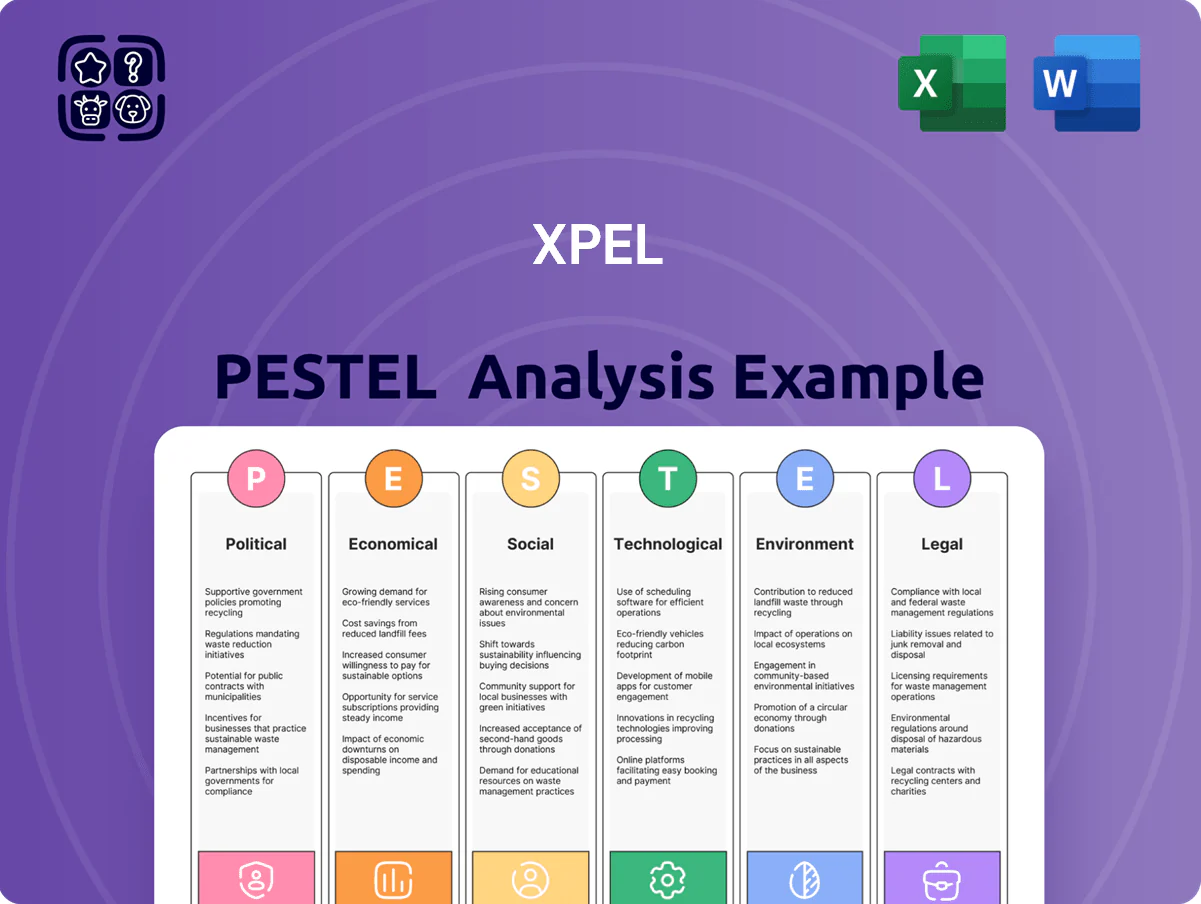

XPEL PESTLE Analysis

Your Competitive Advantage Starts with This Report

Uncover how political shifts, economic trends, and rapid tech advances are reshaping XPEL’s market position with our concise PESTLE Analysis—designed for investors and strategists who need actionable external insights. Buy the full report for a complete breakdown of risks, opportunities, and strategic implications, ready to download and use in pitches or planning.

Political factors

Global Trade Policy and Tariffs

Changes in trade agreements and tariffs on PET film and finished paint protection products can raise XPEL's COGS; 2024 US tariffs on Chinese chemical imports rose effective rates by ~5-10%, potentially adding millions in input costs given XPEL's $1.16B 2024 revenue and ~35% gross margin.

Geopolitical Stability in Key Markets

Government Incentives for Electric Vehicles

Government incentives for electric vehicles, such as US federal tax credits up to $7,500 and EU subsidies covering up to 30% of purchase price, expand XPEL’s core customer base by boosting EV sales—global EV sales reached 14 million in 2023, a 35% rise YoY—driving demand for PPF and ceramic coatings as EV owners pay 10–20% more for aftermarket protection to preserve resale value.

Regulatory Standards for Window Tinting

State and national bodies regularly revise visible light transmission (VLT) limits—for example, over 20 US states modified tint laws between 2019–2024 and EU member states enforce 70% VLT for front side windows; noncompliance risks fines up to $500 per vehicle or product seizures. XPEL must adapt coatings and certification to jurisdictional VLTs to avoid bans and preserve revenue (2024 global aftermarket tint market ~USD 2.1bn). Staying proactive lets XPEL supply compliant films to its ~2,000 global installers.

- Over 20 US states changed tint laws 2019–2024

- EU common front-side VLT ~70%

- Noncompliance fines up to $500 per vehicle

- 2024 aftermarket tint market ≈ USD 2.1bn; XPEL serves ~2,000 installers

Corporate Tax Reform and Fiscal Policy

Changes in domestic and international tax laws can materially affect XPEL's profitability and cash flow; a 5.0% effective tax-rate change on 2025 projected pre-tax income of $120M would alter net income by ~$6M.

Fiscal incentives like R&D tax credits and bonus depreciation (e.g., U.S. R&D credit reducing costs by up to 10–20%) support XPEL's product innovation and facility investment plans.

Analysts track policy shifts to revise DCF inputs and long-term growth, with tax-rate assumptions driving valuation swings of 3–7% in comparable automotive-tech peers.

- 5% tax-rate change ≈ $6M impact on $120M pre-tax

- R&D credits can lower R&D expense by ~10–20%

- Tax assumption shifts can move valuations 3–7%

Geopolitics, tariffs and tax shifts threaten XPEL’s margins and revenue stability

Trade tariffs, sanctions and regional instability can swing XPEL’s COGS and revenues—2024 US tariff hikes added ~5–10% input cost risk to a $1.16B revenue base; political events drove ~7% quarterly revenue swings in affected markets. Tax-rate moves (~5% change ≈ $6M on $120M pre-tax) and VLT/tint law variations (20+ US states 2019–2024; EU ~70% VLT) affect compliance costs and market access.

| Metric | Value |

|---|---|

| 2024 Revenue | $1.16B |

| Gross margin | ~35% |

| Tariff impact | +5–10% input cost |

| EV sales 2023 | 14M (+35% YoY) |

| Tax sensitivity | 5% ≈ $6M |

What is included in the product

Explores how external macro-environmental factors uniquely affect XPEL across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Concise PESTLE summary tailored for XPEL that highlights regulatory, technological, and market risks in plain language, ideal for quick insertion into presentations or sharing across teams to align strategy and de-risk decision-making.

Economic factors

Consumer Discretionary Spending Trends

XPEL’s revenue is highly correlated with disposable income among car enthusiasts and luxury buyers; U.S. personal disposable income rose 3.4% in 2024 y/y, supporting demand for premium services like ceramic coatings and PPF, which represented ~60% of XPEL’s 2024 product revenue. During expansions, ASPs and installation volumes climb, while downturns—e.g., 2023 GDP slowdown—suppress high-end upgrades, forcing defensive pricing and channel diversification.

Interest Rates and Auto Financing

Higher interest rates reduce new vehicle sales—US auto loan rates averaged ~10.5% in 2024 versus ~6% in 2021—dampening demand for XPEL's PPF as new-vehicle installations drive ~60% of aftermarket revenue.

More expensive financing particularly slows high-end vehicle transactions, shrinking the immediate addressable market for premium PPF; luxury segment sales fell ~8% YoY in 2024 in several markets.

XPEL monitors central bank policy closely—Fed rate decisions and ECB/BoE moves directly influence vehicle credit conditions and dealer inventories, linking monetary policy to aftermarket growth prospects.

Fluctuations in Raw Material Costs

Fluctuations in thermoplastic polyurethane and related chemicals, tied to oil-derived feedstocks, exposed XPEL to raw-material price swings—TPU prices rose ~12% in 2023 and global chemical input inflation averaged 9% in 2024, risking margin compression if costs cannot be passed to consumers or installers.

XPEL reported gross margin of 41.8% in FY2024, reflecting some absorption of higher input costs; inability to transfer prices could materially reduce margins given materials share of COGS.

To mitigate volatility, XPEL employs strategic sourcing, multi-supplier contracts and inventory layering; management noted inventory increased 18% year-over-year at end-FY2024 to hedge against supply shocks and price spikes.

Currency Exchange Rate Volatility

As a global entity, XPEL faces transaction and translation risks from USD fluctuations; in 2024 approximately 28% of revenue was generated outside the US, exposing consolidated results to currency moves.

Dollar strength in 2024 raised local prices, contributing to slower growth in Europe and Asia where FX-adjusted sales growth lagged reported growth by about 3–5 percentage points.

XPEL’s finance team uses hedging—forward contracts and net exposure management—reducing quarterly earnings volatility; in FY2024 hedges covered an estimated 60–70% of near-term net exposure.

- ~28% revenue ex-US (2024)

- FX-adjusted sales growth ~3–5 ppt below reported in Europe/Asia (2024)

- Hedges cover ~60–70% of near-term exposure (FY2024)

Labor Market Conditions and Installer Availability

The growth of XPEL depends on skilled labor in its third-party installer network; U.S. auto aftermarket employment rose 2.1% in 2024, but technician shortages persist, pressuring lead times and capacity.

Labor shortages and rising wage demands—wages in auto repair increased ~4.5% YoY in 2024—can raise installation costs for consumers and compress XPEL margins.

XPEL's training programs (XPEL Academy) aim to pipeline certified installers; the company reported training over 5,000 technicians globally through 2024 to support product adoption.

- Installer shortages risk higher end-user prices and longer lead times

- Wage inflation (~4–5% in 2024) pressures margins

- XPEL trained 5,000+ technicians by 2024 to secure capacity

Premium PPF demand lifted by rising PDI but margin and volume risks loom

Economic factors: consumer disposable income gains (US PDI +3.4% in 2024) support premium PPF/ceramic demand (~60% revenue); higher auto loan rates (~10.5% avg 2024) and luxury sales down ~8% pressure volumes; TPU/chemical input inflation (~9% in 2024) risks margins (gross margin FY2024 41.8%); FX and hedging (28% revenue ex-US; 60–70% hedged) and installer labor constraints (5,000 trained) shape growth.

| Metric | 2024 |

|---|---|

| US PDI change | +3.4% |

| Auto loan rate | ~10.5% |

| TPU/inputs | +9% |

| Gross margin | 41.8% |

| Revenue ex‑US | ~28% |

Same Document Delivered

XPEL PESTLE Analysis

The preview shown here is the exact XPEL PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Uncover how political shifts, economic trends, and rapid tech advances are reshaping XPEL’s market position with our concise PESTLE Analysis—designed for investors and strategists who need actionable external insights. Buy the full report for a complete breakdown of risks, opportunities, and strategic implications, ready to download and use in pitches or planning.

Political factors

Global Trade Policy and Tariffs

Changes in trade agreements and tariffs on PET film and finished paint protection products can raise XPEL's COGS; 2024 US tariffs on Chinese chemical imports rose effective rates by ~5-10%, potentially adding millions in input costs given XPEL's $1.16B 2024 revenue and ~35% gross margin.

Geopolitical Stability in Key Markets

Government Incentives for Electric Vehicles

Government incentives for electric vehicles, such as US federal tax credits up to $7,500 and EU subsidies covering up to 30% of purchase price, expand XPEL’s core customer base by boosting EV sales—global EV sales reached 14 million in 2023, a 35% rise YoY—driving demand for PPF and ceramic coatings as EV owners pay 10–20% more for aftermarket protection to preserve resale value.

Regulatory Standards for Window Tinting

State and national bodies regularly revise visible light transmission (VLT) limits—for example, over 20 US states modified tint laws between 2019–2024 and EU member states enforce 70% VLT for front side windows; noncompliance risks fines up to $500 per vehicle or product seizures. XPEL must adapt coatings and certification to jurisdictional VLTs to avoid bans and preserve revenue (2024 global aftermarket tint market ~USD 2.1bn). Staying proactive lets XPEL supply compliant films to its ~2,000 global installers.

- Over 20 US states changed tint laws 2019–2024

- EU common front-side VLT ~70%

- Noncompliance fines up to $500 per vehicle

- 2024 aftermarket tint market ≈ USD 2.1bn; XPEL serves ~2,000 installers

Corporate Tax Reform and Fiscal Policy

Changes in domestic and international tax laws can materially affect XPEL's profitability and cash flow; a 5.0% effective tax-rate change on 2025 projected pre-tax income of $120M would alter net income by ~$6M.

Fiscal incentives like R&D tax credits and bonus depreciation (e.g., U.S. R&D credit reducing costs by up to 10–20%) support XPEL's product innovation and facility investment plans.

Analysts track policy shifts to revise DCF inputs and long-term growth, with tax-rate assumptions driving valuation swings of 3–7% in comparable automotive-tech peers.

- 5% tax-rate change ≈ $6M impact on $120M pre-tax

- R&D credits can lower R&D expense by ~10–20%

- Tax assumption shifts can move valuations 3–7%

Geopolitics, tariffs and tax shifts threaten XPEL’s margins and revenue stability

Trade tariffs, sanctions and regional instability can swing XPEL’s COGS and revenues—2024 US tariff hikes added ~5–10% input cost risk to a $1.16B revenue base; political events drove ~7% quarterly revenue swings in affected markets. Tax-rate moves (~5% change ≈ $6M on $120M pre-tax) and VLT/tint law variations (20+ US states 2019–2024; EU ~70% VLT) affect compliance costs and market access.

| Metric | Value |

|---|---|

| 2024 Revenue | $1.16B |

| Gross margin | ~35% |

| Tariff impact | +5–10% input cost |

| EV sales 2023 | 14M (+35% YoY) |

| Tax sensitivity | 5% ≈ $6M |

What is included in the product

Explores how external macro-environmental factors uniquely affect XPEL across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Concise PESTLE summary tailored for XPEL that highlights regulatory, technological, and market risks in plain language, ideal for quick insertion into presentations or sharing across teams to align strategy and de-risk decision-making.

Economic factors

Consumer Discretionary Spending Trends

XPEL’s revenue is highly correlated with disposable income among car enthusiasts and luxury buyers; U.S. personal disposable income rose 3.4% in 2024 y/y, supporting demand for premium services like ceramic coatings and PPF, which represented ~60% of XPEL’s 2024 product revenue. During expansions, ASPs and installation volumes climb, while downturns—e.g., 2023 GDP slowdown—suppress high-end upgrades, forcing defensive pricing and channel diversification.

Interest Rates and Auto Financing

Higher interest rates reduce new vehicle sales—US auto loan rates averaged ~10.5% in 2024 versus ~6% in 2021—dampening demand for XPEL's PPF as new-vehicle installations drive ~60% of aftermarket revenue.

More expensive financing particularly slows high-end vehicle transactions, shrinking the immediate addressable market for premium PPF; luxury segment sales fell ~8% YoY in 2024 in several markets.

XPEL monitors central bank policy closely—Fed rate decisions and ECB/BoE moves directly influence vehicle credit conditions and dealer inventories, linking monetary policy to aftermarket growth prospects.

Fluctuations in Raw Material Costs

Fluctuations in thermoplastic polyurethane and related chemicals, tied to oil-derived feedstocks, exposed XPEL to raw-material price swings—TPU prices rose ~12% in 2023 and global chemical input inflation averaged 9% in 2024, risking margin compression if costs cannot be passed to consumers or installers.

XPEL reported gross margin of 41.8% in FY2024, reflecting some absorption of higher input costs; inability to transfer prices could materially reduce margins given materials share of COGS.

To mitigate volatility, XPEL employs strategic sourcing, multi-supplier contracts and inventory layering; management noted inventory increased 18% year-over-year at end-FY2024 to hedge against supply shocks and price spikes.

Currency Exchange Rate Volatility

As a global entity, XPEL faces transaction and translation risks from USD fluctuations; in 2024 approximately 28% of revenue was generated outside the US, exposing consolidated results to currency moves.

Dollar strength in 2024 raised local prices, contributing to slower growth in Europe and Asia where FX-adjusted sales growth lagged reported growth by about 3–5 percentage points.

XPEL’s finance team uses hedging—forward contracts and net exposure management—reducing quarterly earnings volatility; in FY2024 hedges covered an estimated 60–70% of near-term net exposure.

- ~28% revenue ex-US (2024)

- FX-adjusted sales growth ~3–5 ppt below reported in Europe/Asia (2024)

- Hedges cover ~60–70% of near-term exposure (FY2024)

Labor Market Conditions and Installer Availability

The growth of XPEL depends on skilled labor in its third-party installer network; U.S. auto aftermarket employment rose 2.1% in 2024, but technician shortages persist, pressuring lead times and capacity.

Labor shortages and rising wage demands—wages in auto repair increased ~4.5% YoY in 2024—can raise installation costs for consumers and compress XPEL margins.

XPEL's training programs (XPEL Academy) aim to pipeline certified installers; the company reported training over 5,000 technicians globally through 2024 to support product adoption.

- Installer shortages risk higher end-user prices and longer lead times

- Wage inflation (~4–5% in 2024) pressures margins

- XPEL trained 5,000+ technicians by 2024 to secure capacity

Premium PPF demand lifted by rising PDI but margin and volume risks loom

Economic factors: consumer disposable income gains (US PDI +3.4% in 2024) support premium PPF/ceramic demand (~60% revenue); higher auto loan rates (~10.5% avg 2024) and luxury sales down ~8% pressure volumes; TPU/chemical input inflation (~9% in 2024) risks margins (gross margin FY2024 41.8%); FX and hedging (28% revenue ex-US; 60–70% hedged) and installer labor constraints (5,000 trained) shape growth.

| Metric | 2024 |

|---|---|

| US PDI change | +3.4% |

| Auto loan rate | ~10.5% |

| TPU/inputs | +9% |

| Gross margin | 41.8% |

| Revenue ex‑US | ~28% |

Same Document Delivered

XPEL PESTLE Analysis

The preview shown here is the exact XPEL PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.