Xinyuan Real Estate Co. Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

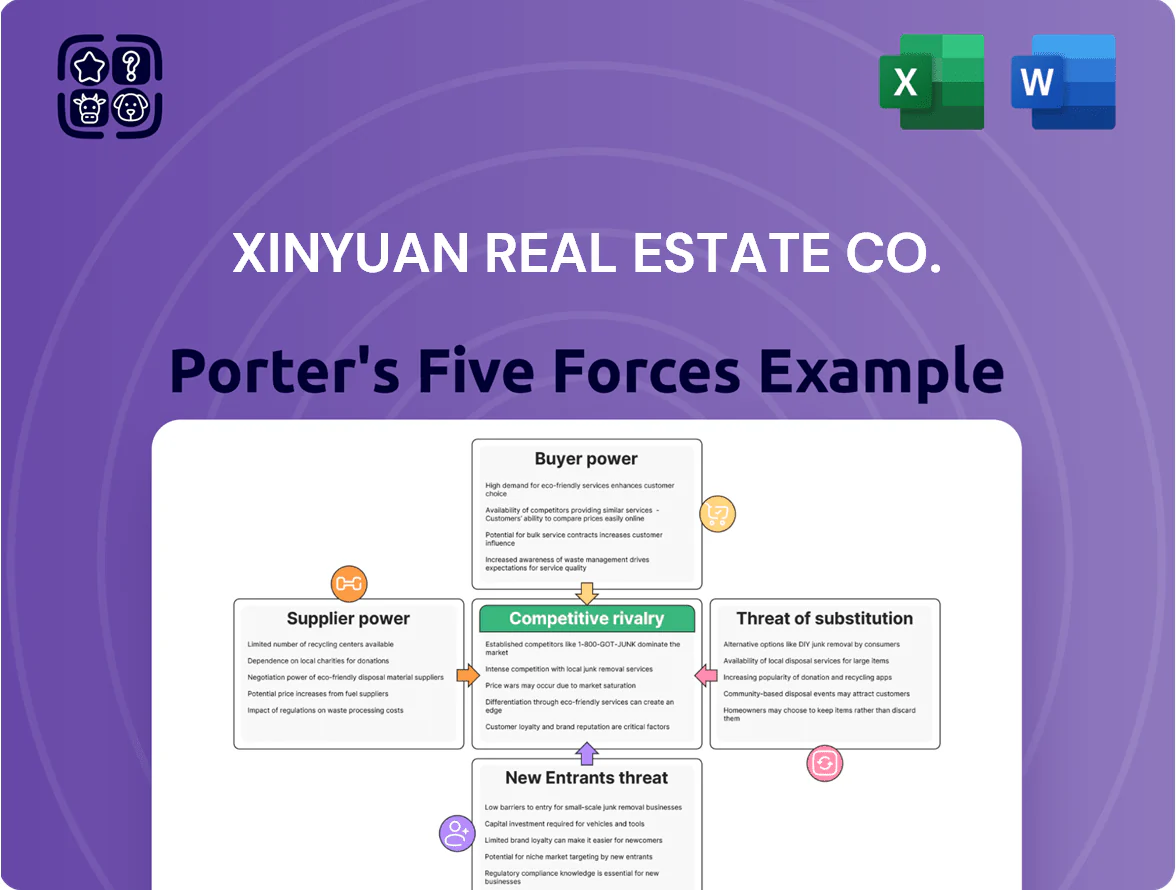

Xinyuan Real Estate faces moderate buyer power and rising competitive rivalry as Chinese developers battle pricing and land constraints, while supplier leverage and regulatory shifts heighten execution risk; substitutes are limited but financing pressures and customer preferences for integrated services pose strategic threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xinyuan Real Estate Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Government Control Over Land Supply

The primary supplier for Xinyuan in China is the government, which holds a land-ownership monopoly and sells parcels via auctions; in 2024 China land-transfer receipts totaled about CNY 6.0 trillion, keeping supplier power high as Xinyuan must accept auction prices and conditions without bargaining.

In the US, land is privately owned but local zoning boards and municipal authorities control land use through permits and density limits; for example New York City’s 2023 zoning approvals tightened FAR rules, constraining project scale and giving local regulators de facto supplier power.

Construction Material Costs and Availability

Xinyuan depends on suppliers for steel, cement and glass, commodities whose prices swung globally; steel rose ~12% in 2024 and cement input inflation averaged 8% Y/Y through 2025. Supply chains stabilized by late 2025, but top 5 material producers control ~60% of supply, giving them pricing leverage. Xinyuan uses long-term contracts to hedge volatility, yet a sudden input-price spike (eg, >10% quarter) would still squeeze margins and delay projects.

Reliance on Specialized Labor and Contractors

The Chinese construction sector faced a 2024 skilled-worker shortfall estimated at 1.2 million workers, raising bargaining power for specialized labor and architectural firms; Xinyuan Real Estate Co. competes with top developers like Country Garden and Evergrande for scarce contractors, which pressures margins.

Access to Financial Capital

Financial institutions and bondholders supply capital to Xinyuan; their leverage rose after 2020–2023 property-sector turmoil and now tracks China policy rates (PBOC cut to 2.5% LPR floor in 2024) and Xinyuan’s junk-ish credit signs—onsite 2024 net debt/EBITDA ~8x—so lenders demand tighter covenants and higher spreads.

Xinyuan must strengthen liquidity and cut leverage to lower borrowing costs and shift covenant terms back in its favor.

- 2024 net debt/EBITDA ≈ 8x

- PBOC LPR policy direction shapes spreads

- Stronger balance sheet → lower spreads, looser covenants

Integration of Smart Home Technology Providers

Xinyuan’s push into high-end mixed-use projects increases reliance on niche smart-home and green-energy suppliers whose proprietary systems raise switching costs; industry reports show smart-home component suppliers capture gross margins of 25–40% and service lock-in averages 5–7 years.

That supplier power forces Xinyuan to form strategic, often multi-year partnerships and joint-spec contracts rather than buy commodities, reducing cost flexibility but raising unit value and customer retention.

- Proprietary tech → high switching cost

- Supplier margins 25–40%

- Service lock-in 5–7 years

- Strategic partnerships > spot purchasing

Suppliers Squeeze Builders: Land, Materials, Labor & Lenders Drive Costs Up

Suppliers hold high power: Chinese land auctions (CNY 6.0tn land receipts in 2024) and municipal zoning in the US constrain project scope; material producers (top 5 ≈60% share) and proprietary smart-home suppliers (margins 25–40%, 5–7yr lock-in) push costs up; skilled-worker shortfall (~1.2m in 2024) and lenders (2024 net debt/EBITDA ≈8x) further strengthen suppliers.

| Item | 2024–25 Metric |

|---|---|

| China land receipts | CNY 6.0tn (2024) |

| Top material producers | ≈60% supply |

| Steel/cement inflation | Steel +12% (2024); cement +8% Y/Y |

| Skilled-worker gap | ≈1.2m short (2024) |

| Net debt/EBITDA | ≈8x (2024) |

| Smart-home supplier margins | 25–40%; lock-in 5–7 yrs |

What is included in the product

Tailored exclusively for Xinyuan Real Estate Co., this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and disruptive market forces shaping its pricing power and profitability.

A concise Porter's Five Forces snapshot for Xinyuan Real Estate—ideal for fast strategic decisions and investor briefs.

Customers Bargaining Power

Availability of Housing Alternatives

Homebuyers in Xinyuan Real Estate Co’s markets face abundant options from local and international developers; China’s residential inventory was estimated at 1.2 trillion RMB unsold value nationwide in 2024, concentrating in provinces like Henan and Sichuan. This surplus gives buyers leverage to demand price cuts or upgraded amenities—average new-home discounts reached 5–12% in 2024 in Tier‑3 cities. Easy switching between projects raises collective bargaining power, pressuring Xinyuan’s margins and sales pace.

Price Sensitivity and Economic Sentiment

By end-2025, consumer confidence in China’s housing market stays tied to GDP growth (projected ~4.5% for 2025) and urban employment; surveys show 38% of potential buyers cite job worry as main deterrent.

Buyers can delay purchases if they expect price drops or if 5-year mortgage rates near 4.5% stay unattractive, raising cancellation risk.

Xinyuan responds with aggressive marketing and flexible financing—extended deposits, lower down-payment pilots and 6–12 month mortgage-rate subsidies—to convert hesitant buyers.

Information Transparency for Buyers

The digital shift has given buyers far more data on Xinyuan Real Estate Co., including third-party valuation sites, sales-trend dashboards and developer-track-record databases; in China online listings grew 18% y/y in 2024, boosting buyer comparison power.

Mortgage Rates and Financing Access

The bargaining power of customers hinges on access to affordable mortgages; China 1-year loan prime rate rose to 3.95% by Dec 2025, tightening real-buyer pools and boosting negotiation leverage for financed buyers.

Tighter bank lending and higher rates force Xinyuan to offer internal subsidies or broker financing; in 2024–25 Xinyuan reported higher sales incentives equal to ~4–6% of contracted sales to sustain velocity.

- Higher LPR (3.95% as of Dec 2025) shrinks qualified buyers

- Qualified buyers gain price leverage

- Xinyuan uses 4–6% subsidy/financing support

- Sales velocity depends on lender openness

Demand for Quality and After-Sales Service

Modern premium buyers insist on high construction standards and full-service property management; in China 2024 surveys show 62% of luxury buyers cite after-sales service as a top purchase driver.

Because Xinyuan (Xinyuan Real Estate Co., listed 2007, ticker XIN) provides property management, customers press for lower fees and higher SLAs, leveraging bundled sales to extract concessions.

Missed expectations risk reputation hit and lower resale values; Xinyuan’s 2023 annual report links customer satisfaction declines to up to 5–8% markdowns on secondary prices.

- 62% of premium buyers prioritize after-sales (China, 2024)

- Xinyuan offers in-house property management—creates buyer leverage

- Service failures can reduce resale value by 5–8% (Xinyuan 2023 data)

China property buyers gain leverage: 1.2tn unsold, 5–12% discounts, service drives value

Buyers wield strong leverage: 1.2tn RMB unsold (2024), 5–12% avg discounts (Tier‑3, 2024), LPR 3.95% (Dec 2025) cuts qualified buyers; Xinyuan’s 4–6% sales subsidies and in‑house property management face 62% premium-buyer service demands; service slips link to 5–8% resale markdowns (Xinyuan 2023).

| Metric | Value |

|---|---|

| Unsold stock (2024) | 1.2tn RMB |

| Avg discounts | 5–12% |

| LPR / 1yr rate (Dec 2025) | 3.95% |

| Xinyuan subsidies | 4–6% sales |

| Premium buyers value service | 62% |

Same Document Delivered

Xinyuan Real Estate Co. Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Xinyuan Real Estate Co. you'll receive immediately after purchase—no surprises, no placeholders. It assesses supplier and buyer power, competitive rivalry, threat of new entrants, and substitution with data-driven observations tied to the China residential and mixed-use property market. The document is fully formatted and ready for download the moment you buy. Use it as-is for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Xinyuan Real Estate faces moderate buyer power and rising competitive rivalry as Chinese developers battle pricing and land constraints, while supplier leverage and regulatory shifts heighten execution risk; substitutes are limited but financing pressures and customer preferences for integrated services pose strategic threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xinyuan Real Estate Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Government Control Over Land Supply

The primary supplier for Xinyuan in China is the government, which holds a land-ownership monopoly and sells parcels via auctions; in 2024 China land-transfer receipts totaled about CNY 6.0 trillion, keeping supplier power high as Xinyuan must accept auction prices and conditions without bargaining.

In the US, land is privately owned but local zoning boards and municipal authorities control land use through permits and density limits; for example New York City’s 2023 zoning approvals tightened FAR rules, constraining project scale and giving local regulators de facto supplier power.

Construction Material Costs and Availability

Xinyuan depends on suppliers for steel, cement and glass, commodities whose prices swung globally; steel rose ~12% in 2024 and cement input inflation averaged 8% Y/Y through 2025. Supply chains stabilized by late 2025, but top 5 material producers control ~60% of supply, giving them pricing leverage. Xinyuan uses long-term contracts to hedge volatility, yet a sudden input-price spike (eg, >10% quarter) would still squeeze margins and delay projects.

Reliance on Specialized Labor and Contractors

The Chinese construction sector faced a 2024 skilled-worker shortfall estimated at 1.2 million workers, raising bargaining power for specialized labor and architectural firms; Xinyuan Real Estate Co. competes with top developers like Country Garden and Evergrande for scarce contractors, which pressures margins.

Access to Financial Capital

Financial institutions and bondholders supply capital to Xinyuan; their leverage rose after 2020–2023 property-sector turmoil and now tracks China policy rates (PBOC cut to 2.5% LPR floor in 2024) and Xinyuan’s junk-ish credit signs—onsite 2024 net debt/EBITDA ~8x—so lenders demand tighter covenants and higher spreads.

Xinyuan must strengthen liquidity and cut leverage to lower borrowing costs and shift covenant terms back in its favor.

- 2024 net debt/EBITDA ≈ 8x

- PBOC LPR policy direction shapes spreads

- Stronger balance sheet → lower spreads, looser covenants

Integration of Smart Home Technology Providers

Xinyuan’s push into high-end mixed-use projects increases reliance on niche smart-home and green-energy suppliers whose proprietary systems raise switching costs; industry reports show smart-home component suppliers capture gross margins of 25–40% and service lock-in averages 5–7 years.

That supplier power forces Xinyuan to form strategic, often multi-year partnerships and joint-spec contracts rather than buy commodities, reducing cost flexibility but raising unit value and customer retention.

- Proprietary tech → high switching cost

- Supplier margins 25–40%

- Service lock-in 5–7 years

- Strategic partnerships > spot purchasing

Suppliers Squeeze Builders: Land, Materials, Labor & Lenders Drive Costs Up

Suppliers hold high power: Chinese land auctions (CNY 6.0tn land receipts in 2024) and municipal zoning in the US constrain project scope; material producers (top 5 ≈60% share) and proprietary smart-home suppliers (margins 25–40%, 5–7yr lock-in) push costs up; skilled-worker shortfall (~1.2m in 2024) and lenders (2024 net debt/EBITDA ≈8x) further strengthen suppliers.

| Item | 2024–25 Metric |

|---|---|

| China land receipts | CNY 6.0tn (2024) |

| Top material producers | ≈60% supply |

| Steel/cement inflation | Steel +12% (2024); cement +8% Y/Y |

| Skilled-worker gap | ≈1.2m short (2024) |

| Net debt/EBITDA | ≈8x (2024) |

| Smart-home supplier margins | 25–40%; lock-in 5–7 yrs |

What is included in the product

Tailored exclusively for Xinyuan Real Estate Co., this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and disruptive market forces shaping its pricing power and profitability.

A concise Porter's Five Forces snapshot for Xinyuan Real Estate—ideal for fast strategic decisions and investor briefs.

Customers Bargaining Power

Availability of Housing Alternatives

Homebuyers in Xinyuan Real Estate Co’s markets face abundant options from local and international developers; China’s residential inventory was estimated at 1.2 trillion RMB unsold value nationwide in 2024, concentrating in provinces like Henan and Sichuan. This surplus gives buyers leverage to demand price cuts or upgraded amenities—average new-home discounts reached 5–12% in 2024 in Tier‑3 cities. Easy switching between projects raises collective bargaining power, pressuring Xinyuan’s margins and sales pace.

Price Sensitivity and Economic Sentiment

By end-2025, consumer confidence in China’s housing market stays tied to GDP growth (projected ~4.5% for 2025) and urban employment; surveys show 38% of potential buyers cite job worry as main deterrent.

Buyers can delay purchases if they expect price drops or if 5-year mortgage rates near 4.5% stay unattractive, raising cancellation risk.

Xinyuan responds with aggressive marketing and flexible financing—extended deposits, lower down-payment pilots and 6–12 month mortgage-rate subsidies—to convert hesitant buyers.

Information Transparency for Buyers

The digital shift has given buyers far more data on Xinyuan Real Estate Co., including third-party valuation sites, sales-trend dashboards and developer-track-record databases; in China online listings grew 18% y/y in 2024, boosting buyer comparison power.

Mortgage Rates and Financing Access

The bargaining power of customers hinges on access to affordable mortgages; China 1-year loan prime rate rose to 3.95% by Dec 2025, tightening real-buyer pools and boosting negotiation leverage for financed buyers.

Tighter bank lending and higher rates force Xinyuan to offer internal subsidies or broker financing; in 2024–25 Xinyuan reported higher sales incentives equal to ~4–6% of contracted sales to sustain velocity.

- Higher LPR (3.95% as of Dec 2025) shrinks qualified buyers

- Qualified buyers gain price leverage

- Xinyuan uses 4–6% subsidy/financing support

- Sales velocity depends on lender openness

Demand for Quality and After-Sales Service

Modern premium buyers insist on high construction standards and full-service property management; in China 2024 surveys show 62% of luxury buyers cite after-sales service as a top purchase driver.

Because Xinyuan (Xinyuan Real Estate Co., listed 2007, ticker XIN) provides property management, customers press for lower fees and higher SLAs, leveraging bundled sales to extract concessions.

Missed expectations risk reputation hit and lower resale values; Xinyuan’s 2023 annual report links customer satisfaction declines to up to 5–8% markdowns on secondary prices.

- 62% of premium buyers prioritize after-sales (China, 2024)

- Xinyuan offers in-house property management—creates buyer leverage

- Service failures can reduce resale value by 5–8% (Xinyuan 2023 data)

China property buyers gain leverage: 1.2tn unsold, 5–12% discounts, service drives value

Buyers wield strong leverage: 1.2tn RMB unsold (2024), 5–12% avg discounts (Tier‑3, 2024), LPR 3.95% (Dec 2025) cuts qualified buyers; Xinyuan’s 4–6% sales subsidies and in‑house property management face 62% premium-buyer service demands; service slips link to 5–8% resale markdowns (Xinyuan 2023).

| Metric | Value |

|---|---|

| Unsold stock (2024) | 1.2tn RMB |

| Avg discounts | 5–12% |

| LPR / 1yr rate (Dec 2025) | 3.95% |

| Xinyuan subsidies | 4–6% sales |

| Premium buyers value service | 62% |

Same Document Delivered

Xinyuan Real Estate Co. Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Xinyuan Real Estate Co. you'll receive immediately after purchase—no surprises, no placeholders. It assesses supplier and buyer power, competitive rivalry, threat of new entrants, and substitution with data-driven observations tied to the China residential and mixed-use property market. The document is fully formatted and ready for download the moment you buy. Use it as-is for strategic or investment decisions.