Beijing Yanjing Brewery Co. Porter's Five Forces Analysis

From Overview to Strategy Blueprint

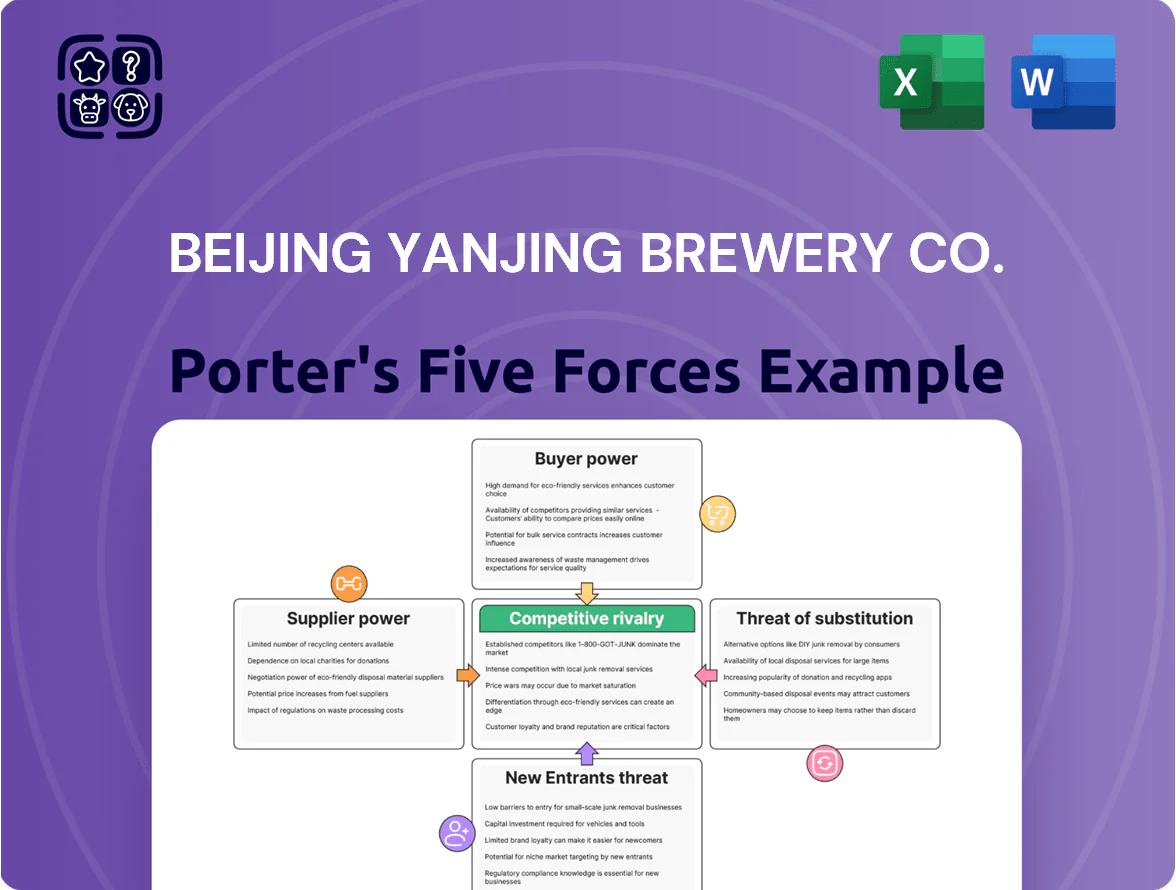

Beijing Yanjing Brewery faces moderate rivalry—strong domestic brands and regional brewers pressure margins, while its scale and distribution in Beijing provide durable advantages.

Supplier power is limited by commodity sourcing, but fluctuating grain costs and packaging inputs raise operational risk; buyer power grows as retail chains consolidate.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Beijing Yanjing Brewery Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material commodity price volatility

Beijing Yanjing Brewery depends on barley, hops and rice, commodities whose global prices rose ~18% year-on-year in 2024 due to weather shocks, raising input costs materially for brewers.

By late 2025 Yanjing had signed multi-year purchase contracts covering roughly 60% of its needs with local farms and overseas maltsters to stabilize prices and secure supply.

Still, fewer than five high-quality malt providers in China give those suppliers moderate bargaining power; during the 2023–24 poor harvests, supplier-driven price spikes added about CNY 0.12 per litre to production cost.

Packaging material cost fluctuations

Packaging accounts for roughly 15–20% of Yanjing’s production cost, covering glass bottles, aluminum cans, and cardboard; global aluminum prices rose 12% in 2024, pushing can costs higher. Suppliers hold moderate bargaining power since their margins track commodity and energy prices—aluminum and oil shocks raise input costs across the sector. Yanjing reduces supplier risk by sourcing from multiple manufacturers and keeping 30% of purchases on short-term contracts, but it still faces industry-wide price hikes that squeeze margins.

Energy and utility requirements

Brewing uses heavy water, electricity and steam; Yanjing consumed about 120 million m3 of water and 1.8 TWh of energy in 2024, so utilities are critical cost drivers.

China’s 2025 environmental rules force cleaner energy and emission controls, raising capex and OPEX; utility providers thus gain leverage during the green transition.

State-owned utility monopolies set prices and emission benchmarks; Yanjing faces limited bargaining room—energy spend accounted for ~8–10% of COGS in 2024.

Dependence on specialized brewing equipment

Dependence on specialized brewing equipment concentrates supplier power: a handful of global engineering firms supply mash tuns, centrifuges, and control systems, making switching costly and technically risky for Beijing Yanjing Brewery Co. (Yanjing).

Technical complexity plus high capex means suppliers can demand premium terms; industry reports show aftermarket service margins of 20–30% and lead times of 6–18 months for major components.

Yanjing signs long-term service agreements and spare-parts contracts—tying operational uptime to specific vendors and raising effective switching costs while securing predictable maintenance spend.

- High supplier concentration

- Switching costs: multi-million CNY, 6–18 month lead times

- Aftermarket margins ~20–30%

- Long-term service contracts reduce flexibility

Logistics and transportation providers

Yanjing’s vast China distribution makes it sensitive to third-party logistics and fuel pricing; fuel volatility pushed diesel retail prices up ~18% YoY in 2025, raising transport costs by an estimated 6–9% for CPG firms.

Rising logistics wages (+7% nationwide in 2025) increased carriers’ leverage, so Yanjing expanded in-house freight capacity and regional depots but still pays premiums to external carriers for remote western provinces.

- Fuel prices +18% YoY (2025)

- Logistics wages +7% (2025)

- Transport cost rise est. 6–9%

- Internal logistics expanded; external use for remote markets

Suppliers Tighten Grip: Commodities, Aluminum and Utilities Drive Yanjing COGS Higher

Suppliers hold moderate-to-high power: commodity inputs and packaging pushed Yanjing’s COGS up via 18% barley/hop/rice price rise in 2024 and 12% aluminum rise; energy/water and specialized equipment add concentration and switching costs. Yanjing hedges ~60% via multi-year buys, keeps 30% short-term, expanded in-house logistics; nevertheless utility monopolies, 6–18 month equipment lead times, and 20–30% aftermarket margins sustain supplier leverage.

| Metric | Value |

|---|---|

| Commodity price change (2024) | ~+18% |

| Aluminum price change (2024) | +12% |

| Multi-year cover (2025) | ~60% |

| Short-term purchases | ~30% |

| Equipment lead times | 6–18 months |

| Aftermarket margins | 20–30% |

| Energy use (2024) | 1.8 TWh |

| Water use (2024) | 120M m3 |

What is included in the product

Tailored Porter's Five Forces analysis for Beijing Yanjing Brewery Co. uncovering competitive intensity, buyer/supplier power, threat of substitutes and new entrants, plus disruptive trends and strategic levers influencing its pricing, margins, and market resilience.

A one-sheet Porter’s Five Forces summary for Beijing Yanjing Brewery—quickly spot supplier, buyer, and competitive pressures to guide pricing and distribution strategy.

Customers Bargaining Power

Dominance of large-scale retail chains

Low switching costs for end consumers

Individual consumers face virtually zero switching costs between Yanjing and rivals like Tsingtao or Snow, so brand substitutability is high; NielsenIQ reported Chinese beer market share: Snow 21.5%, Tsingtao 9.8%, Yanjing 6.1% in 2024, showing tight competition.

This forces Yanjing to spend on loyalty and marketing—2023 capex and SGA trends show Chinese brewers often allocate 3–5% of revenue to marketing; Yanjing’s price moves risk immediate churn in the mass market where price elasticity is high.

Influence of the Horeca sector

The Horeca channel exerts high bargaining power for Yanjing; in Beijing 2024 horeca accounted for ~28% of on-trade beer volume, concentrating spend among chains. Large groups secure exclusive pouring rights, forcing brewers to offer discounts up to 12–18% and marketing support. Yanjing must deliver tailored pricing, inventory guarantees and promo spends—often 5–8% of net sales—to win high-volume urban accounts.

Growth of e-commerce and digital platforms

The rise of online grocery and food-delivery apps gives shoppers instant price comparison, increasing customer bargaining power and pressuring margins—China internet grocery GMV hit CNY 1.2 trillion in 2024, up 18% year-over-year.

Platforms push deep discounts during festivals (e.g., Singles Day) that can cut manufacturer margins; marketplace promo fees average 4–8% in 2024.

Yanjing built direct-to-consumer channels in 2023–24, capturing first-party data and raising direct sales to ~6% of revenue by 2025 to better control pricing.

- Online grocery GMV CNY 1.2T (2024)

- Marketplace promo fees 4–8% (2024)

- Yanjing DTC ≈6% revenue (2025)

Increasing demand for premium and craft options

Rising Chinese demand for premium beer shifts indirect bargaining power to consumers, forcing Beijing Yanjing Brewery Co. to reorient from low-cost mass production toward higher-margin specialty brews; premium beer value in China grew ~12% CAGR 2019–2024, reaching ~CNY 120 billion in 2024.

Yanjing must speed product development and small-batch capacity to match tastes or cede share to niche craft labels, which grew volume share from ~3% in 2018 to ~7% in 2024.

Retailers and platforms squeeze Yanjing margins as DTC rises to regain pricing power

| Metric | Value |

|---|---|

| Top‑10 chains share (2025) | >40% |

| Marketplace promo fees (2024) | 4–8% |

| Yanjing market share (2024) | 6.1% |

| Snow market share (2024) | 21.5% |

| Online grocery GMV (2024) | CNY 1.2T |

| Yanjing DTC revenue (2025) | ≈6% |

Preview Before You Purchase

Beijing Yanjing Brewery Co. Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Beijing Yanjing Brewery you’ll receive—no samples or placeholders; the full, professionally formatted document is ready for instant download after purchase.

The analysis covers competitive rivalry, threat of new entrants, supplier and buyer power, and substitution risk, and the file you see here is the same complete deliverable available immediately upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Beijing Yanjing Brewery faces moderate rivalry—strong domestic brands and regional brewers pressure margins, while its scale and distribution in Beijing provide durable advantages.

Supplier power is limited by commodity sourcing, but fluctuating grain costs and packaging inputs raise operational risk; buyer power grows as retail chains consolidate.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Beijing Yanjing Brewery Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material commodity price volatility

Beijing Yanjing Brewery depends on barley, hops and rice, commodities whose global prices rose ~18% year-on-year in 2024 due to weather shocks, raising input costs materially for brewers.

By late 2025 Yanjing had signed multi-year purchase contracts covering roughly 60% of its needs with local farms and overseas maltsters to stabilize prices and secure supply.

Still, fewer than five high-quality malt providers in China give those suppliers moderate bargaining power; during the 2023–24 poor harvests, supplier-driven price spikes added about CNY 0.12 per litre to production cost.

Packaging material cost fluctuations

Packaging accounts for roughly 15–20% of Yanjing’s production cost, covering glass bottles, aluminum cans, and cardboard; global aluminum prices rose 12% in 2024, pushing can costs higher. Suppliers hold moderate bargaining power since their margins track commodity and energy prices—aluminum and oil shocks raise input costs across the sector. Yanjing reduces supplier risk by sourcing from multiple manufacturers and keeping 30% of purchases on short-term contracts, but it still faces industry-wide price hikes that squeeze margins.

Energy and utility requirements

Brewing uses heavy water, electricity and steam; Yanjing consumed about 120 million m3 of water and 1.8 TWh of energy in 2024, so utilities are critical cost drivers.

China’s 2025 environmental rules force cleaner energy and emission controls, raising capex and OPEX; utility providers thus gain leverage during the green transition.

State-owned utility monopolies set prices and emission benchmarks; Yanjing faces limited bargaining room—energy spend accounted for ~8–10% of COGS in 2024.

Dependence on specialized brewing equipment

Dependence on specialized brewing equipment concentrates supplier power: a handful of global engineering firms supply mash tuns, centrifuges, and control systems, making switching costly and technically risky for Beijing Yanjing Brewery Co. (Yanjing).

Technical complexity plus high capex means suppliers can demand premium terms; industry reports show aftermarket service margins of 20–30% and lead times of 6–18 months for major components.

Yanjing signs long-term service agreements and spare-parts contracts—tying operational uptime to specific vendors and raising effective switching costs while securing predictable maintenance spend.

- High supplier concentration

- Switching costs: multi-million CNY, 6–18 month lead times

- Aftermarket margins ~20–30%

- Long-term service contracts reduce flexibility

Logistics and transportation providers

Yanjing’s vast China distribution makes it sensitive to third-party logistics and fuel pricing; fuel volatility pushed diesel retail prices up ~18% YoY in 2025, raising transport costs by an estimated 6–9% for CPG firms.

Rising logistics wages (+7% nationwide in 2025) increased carriers’ leverage, so Yanjing expanded in-house freight capacity and regional depots but still pays premiums to external carriers for remote western provinces.

- Fuel prices +18% YoY (2025)

- Logistics wages +7% (2025)

- Transport cost rise est. 6–9%

- Internal logistics expanded; external use for remote markets

Suppliers Tighten Grip: Commodities, Aluminum and Utilities Drive Yanjing COGS Higher

Suppliers hold moderate-to-high power: commodity inputs and packaging pushed Yanjing’s COGS up via 18% barley/hop/rice price rise in 2024 and 12% aluminum rise; energy/water and specialized equipment add concentration and switching costs. Yanjing hedges ~60% via multi-year buys, keeps 30% short-term, expanded in-house logistics; nevertheless utility monopolies, 6–18 month equipment lead times, and 20–30% aftermarket margins sustain supplier leverage.

| Metric | Value |

|---|---|

| Commodity price change (2024) | ~+18% |

| Aluminum price change (2024) | +12% |

| Multi-year cover (2025) | ~60% |

| Short-term purchases | ~30% |

| Equipment lead times | 6–18 months |

| Aftermarket margins | 20–30% |

| Energy use (2024) | 1.8 TWh |

| Water use (2024) | 120M m3 |

What is included in the product

Tailored Porter's Five Forces analysis for Beijing Yanjing Brewery Co. uncovering competitive intensity, buyer/supplier power, threat of substitutes and new entrants, plus disruptive trends and strategic levers influencing its pricing, margins, and market resilience.

A one-sheet Porter’s Five Forces summary for Beijing Yanjing Brewery—quickly spot supplier, buyer, and competitive pressures to guide pricing and distribution strategy.

Customers Bargaining Power

Dominance of large-scale retail chains

Low switching costs for end consumers

Individual consumers face virtually zero switching costs between Yanjing and rivals like Tsingtao or Snow, so brand substitutability is high; NielsenIQ reported Chinese beer market share: Snow 21.5%, Tsingtao 9.8%, Yanjing 6.1% in 2024, showing tight competition.

This forces Yanjing to spend on loyalty and marketing—2023 capex and SGA trends show Chinese brewers often allocate 3–5% of revenue to marketing; Yanjing’s price moves risk immediate churn in the mass market where price elasticity is high.

Influence of the Horeca sector

The Horeca channel exerts high bargaining power for Yanjing; in Beijing 2024 horeca accounted for ~28% of on-trade beer volume, concentrating spend among chains. Large groups secure exclusive pouring rights, forcing brewers to offer discounts up to 12–18% and marketing support. Yanjing must deliver tailored pricing, inventory guarantees and promo spends—often 5–8% of net sales—to win high-volume urban accounts.

Growth of e-commerce and digital platforms

The rise of online grocery and food-delivery apps gives shoppers instant price comparison, increasing customer bargaining power and pressuring margins—China internet grocery GMV hit CNY 1.2 trillion in 2024, up 18% year-over-year.

Platforms push deep discounts during festivals (e.g., Singles Day) that can cut manufacturer margins; marketplace promo fees average 4–8% in 2024.

Yanjing built direct-to-consumer channels in 2023–24, capturing first-party data and raising direct sales to ~6% of revenue by 2025 to better control pricing.

- Online grocery GMV CNY 1.2T (2024)

- Marketplace promo fees 4–8% (2024)

- Yanjing DTC ≈6% revenue (2025)

Increasing demand for premium and craft options

Rising Chinese demand for premium beer shifts indirect bargaining power to consumers, forcing Beijing Yanjing Brewery Co. to reorient from low-cost mass production toward higher-margin specialty brews; premium beer value in China grew ~12% CAGR 2019–2024, reaching ~CNY 120 billion in 2024.

Yanjing must speed product development and small-batch capacity to match tastes or cede share to niche craft labels, which grew volume share from ~3% in 2018 to ~7% in 2024.

Retailers and platforms squeeze Yanjing margins as DTC rises to regain pricing power

| Metric | Value |

|---|---|

| Top‑10 chains share (2025) | >40% |

| Marketplace promo fees (2024) | 4–8% |

| Yanjing market share (2024) | 6.1% |

| Snow market share (2024) | 21.5% |

| Online grocery GMV (2024) | CNY 1.2T |

| Yanjing DTC revenue (2025) | ≈6% |

Preview Before You Purchase

Beijing Yanjing Brewery Co. Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Beijing Yanjing Brewery you’ll receive—no samples or placeholders; the full, professionally formatted document is ready for instant download after purchase.

The analysis covers competitive rivalry, threat of new entrants, supplier and buyer power, and substitution risk, and the file you see here is the same complete deliverable available immediately upon payment.