Yara International Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

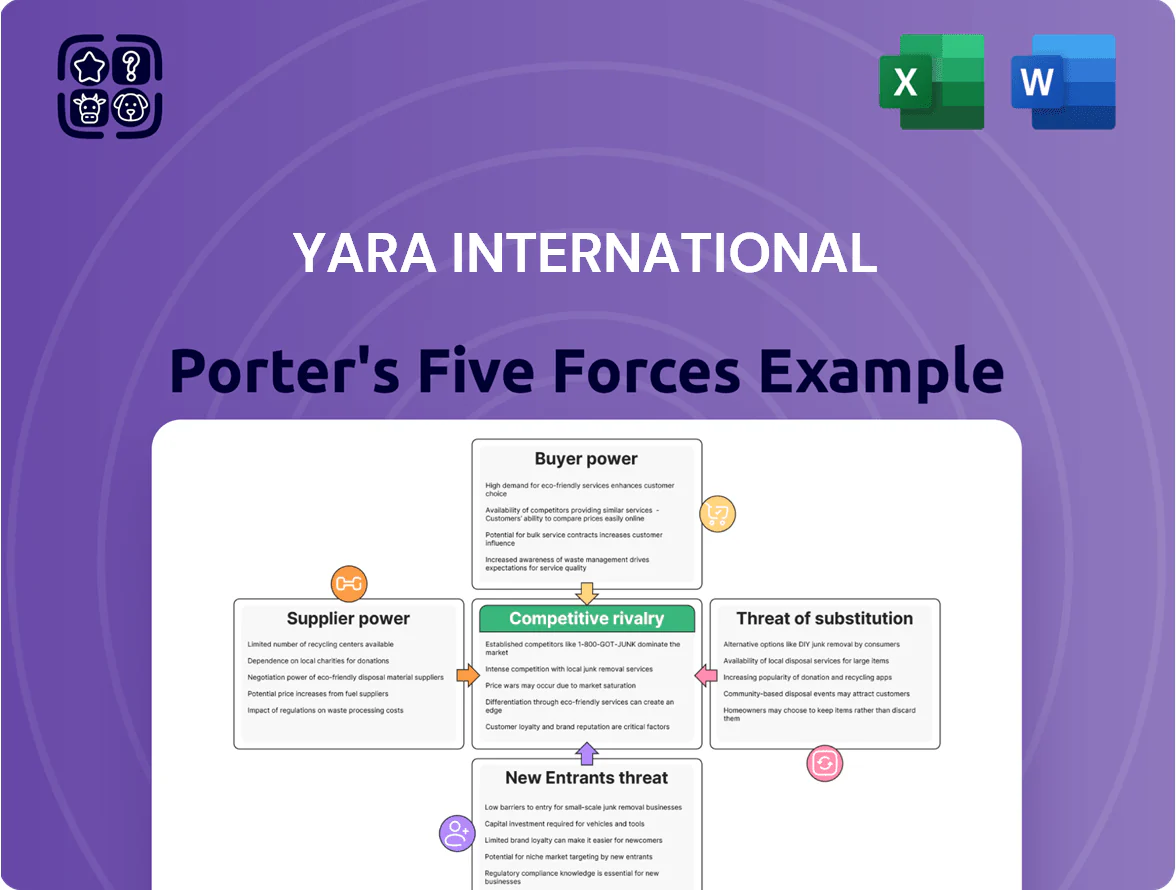

Yara International faces moderate supplier power due to specialized inputs and global sourcing, while buyer power varies across agricultural and industrial clients; rivalry is intense from global fertilizer majors and regional players, and new entrants face high capital and regulatory barriers—substitutes like precision ag and alternative nutrients pose growing but limited threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Yara International’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Natural Gas Feedstock Dependence

Natural gas fuels ~70–80% of ammonia production costs; for Yara International this equated to roughly $1.1–1.4 billion in feedstock spend in 2024, so suppliers hold strong pricing power.

By end-2025 European and North American energy suppliers retain leverage from pipeline constraints and Russia-Ukraine fallout, keeping volatility high and spot prices often 30–60% above long-term averages.

Yara uses multi-year contracts covering ~60% of volumes and is scaling green hydrogen projects targeting 300–500 kt H2 by 2030, but fossil gas still governs near-term margins and cash flow predictability.

Concentration of Mineral Resources

The global supply of phosphate and potash is highly concentrated: in 2024 the top five producers (Morocco/Western Sahara via OCP, Russia, Canada, Belarus, China) accounted for ~70% of exports, letting suppliers push prices—phosphate rock rose ~35% YoY in 2023–24—forcing Yara International to pay higher feedstock costs or reallocate volumes, which raises NPK margins pressure and risks production cuts when geopolitical or export restrictions hit.

Emerging Green Energy Providers

As Yara shifts to decarbonized ammonia, dependency grows on renewable developers and electrolyzer makers; global electrolyzer demand rose 120% in 2024, tightening supply and pricing power. Scarcity of low‑carbon power—IEA estimates 2025 green electricity shortfalls in Europe at 100–150 TWh—lets utilities demand premium contracts. For Yara, securing long‑term, sub‑$40/MWh renewables and reliable 1+ GW electrolyzer deliveries is critical, so suppliers hold strong leverage.

Logistics and Maritime Freight

Global bulk fertilizer distribution depends on specialized shipping and port capacity, with top three maritime logistics firms handling an estimated 60–70% of ammonia/chemical carrier capacity in 2024, raising supplier leverage over Yara International.

Freight-rate swings—Baltic Dirty Tanker Index rose ~45% in 2023–24—and limited ammonia carriers push landed costs up to 15–25% in distant markets, especially during fuel-price spikes.

Supplier bargaining power spikes during port congestion and charter shortages; 2022–24 port delays added ~3–5 days average transit time, increasing inventory and working-capital needs for Yara.

- Top 3 firms control ~60–70% capacity

- Freight volatility raised landed cost 15–25%

- Port delays added 3–5 days (2022–24)

- Fuel spikes magnify supplier leverage

Geopolitical Influence on Raw Materials

Supplier concentration lifts costs: gas, shippers, and exporters drive 15–25% price shocks

Suppliers hold strong power: gas drove $1.1–1.4B feedstock cost in 2024 (~70–80% of ammonia cost), top-5 phosphate/potash exporters supplied ~70% of exports, electrolyzer demand rose 120% in 2024, and top-3 shippers controlled 60–70% capacity—raising landed costs 15–25% and adding 3–5 days transit (2022–24).

| Metric | 2024–25 |

|---|---|

| Gas spend | $1.1–1.4B |

| Top-5 export share | ~70% |

| Electrolyzer demand | +120% |

| Shipper share | 60–70% |

| Landed cost uplift | 15–25% |

| Transit delay | 3–5 days |

What is included in the product

Concise Porter's Five Forces analysis for Yara International highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, plus strategic implications for pricing, margins, and market defense.

A concise Porter's Five Forces snapshot tailored to Yara International—quickly assess supplier, buyer, competitive, substitution, and entrant pressures to guide fertilizer-sector strategy.

Customers Bargaining Power

Consolidation of Agricultural Retailers

In North America and Europe, consolidated agricultural retailers and cooperatives—like CHS Inc. (US) and BayWa AG (Germany)—aggregate demand from thousands of farms, giving them strong volume-based bargaining power versus Yara; top 20 cooperatives account for roughly 35–40% of regional fertilizer purchases as of 2024. They secure steep discounts and extended payment terms, squeezing margins—Yara reported 2024 EBITDA margin pressure in specialty segments. These buyers freely switch global suppliers on price and technical support, raising sales churn risk for Yara and forcing competitive pricing and service investments.

Farmer Price Sensitivity and Income

Farmers are highly price-sensitive: when global crop prices fall, they cut fertilizer spend or shift to cheaper NPK blends; for example, global maize futures dropped ~18% in 2024, and FAO data show fertilizer application rates fell 7% in key producing regions that year, limiting Yara’s ability to pass on higher gas-linked production costs (Yara cites gas cost exposure up to 40%) without risking steep volume declines.

Demand for Low-Carbon Solutions

By late 2025, industrial buyers and food giants are pushing for low-carbon fertilizers to hit their Scope 3 targets, giving large customers stronger leverage to set specs and require certifications; 60% of EU agribusinesses surveyed in 2024 said they'd pay a premium for green inputs, and Yara faces contracts where >30% volume must be certified low-emission. Yara needs major green ammonia capex—estimated $2–3 billion by 2030—to meet demand and retain high-value customers.

Information Transparency and Digital Tools

The rise of digital farming platforms and real-time commodity feeds has cut information asymmetry; by 2025 over 40% of global farmers use precision-agriculture apps, letting buyers compare Yara prices to global ammonia and urea benchmarks instantly, reducing Yara’s regional price premiums.

Smaller farms now demand pricing tied to spot indices; Yara’s margin pressure shows in 2024 clampdown on fertilizer spreads, with global urea FOB volatility ±25% year-on-year, empowering buyers.

- 40%+ farmers use digital ag apps (2025)

- Buyers track ammonia/urea spot indices

- Regional premiums compressed, margins pressured

Switching Costs and Brand Loyalty

Yara’s commodity urea faces low switching costs, but its premium nitrate and tailored NPK products create higher customer stickiness—farmers adapting equipment and soil programs to Yara face measurable yield risk if they switch.

As rivals raised R&D and launched specialty blends in 2024–25, estimated switching propensity rose; industry reports show ~12–18% of large farms trialed alternatives in 2025, lowering barriers.

Yara must expand value-added services—precision agronomy, digital tools, and guaranteed-field trials—to defend retention and justify premium pricing.

- Commodity urea: low switching cost

- Premium nitrate/NPK: higher stickiness, yield risk

- 2025 trials: ~12–18% of large farms

- Action: scale agronomy, digital services, field guarantees

Buyer consolidation, digital adoption and green demand squeeze fertilizer margins

Buyers wield high volume leverage—top 20 co-ops ~35–40% regional purchases (2024)—and switch suppliers on price/service, compressing Yara margins; farmers cut application 7% in 2024 after maize futures fell ~18%, limiting cost pass-through. Demand for low‑carbon fertilizers (60% EU agribusiness willing to pay premium in 2024) forces ~$2–3bn green capex by 2030; digital tools (40%+ farmer adoption by 2025) lower info asymmetry, raising buyer power.

| Metric | Value |

|---|---|

| Top-20 co-op share | 35–40% (2024) |

| Fertilizer application change | -7% (2024) |

| Maize futures move | -18% (2024) |

| Farmers on digital apps | 40%+ (2025) |

| Willing pay premium (EU) | 60% (2024) |

| Green capex need | $2–3bn by 2030 |

Same Document Delivered

Yara International Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Yara International you'll receive upon purchase—no placeholders, no mockups.

The document displayed here is the final, fully formatted file ready for immediate download and use the moment you buy.

You’re previewing the complete deliverable: the same professionally written analysis will be available to you instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Yara International faces moderate supplier power due to specialized inputs and global sourcing, while buyer power varies across agricultural and industrial clients; rivalry is intense from global fertilizer majors and regional players, and new entrants face high capital and regulatory barriers—substitutes like precision ag and alternative nutrients pose growing but limited threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Yara International’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Natural Gas Feedstock Dependence

Natural gas fuels ~70–80% of ammonia production costs; for Yara International this equated to roughly $1.1–1.4 billion in feedstock spend in 2024, so suppliers hold strong pricing power.

By end-2025 European and North American energy suppliers retain leverage from pipeline constraints and Russia-Ukraine fallout, keeping volatility high and spot prices often 30–60% above long-term averages.

Yara uses multi-year contracts covering ~60% of volumes and is scaling green hydrogen projects targeting 300–500 kt H2 by 2030, but fossil gas still governs near-term margins and cash flow predictability.

Concentration of Mineral Resources

The global supply of phosphate and potash is highly concentrated: in 2024 the top five producers (Morocco/Western Sahara via OCP, Russia, Canada, Belarus, China) accounted for ~70% of exports, letting suppliers push prices—phosphate rock rose ~35% YoY in 2023–24—forcing Yara International to pay higher feedstock costs or reallocate volumes, which raises NPK margins pressure and risks production cuts when geopolitical or export restrictions hit.

Emerging Green Energy Providers

As Yara shifts to decarbonized ammonia, dependency grows on renewable developers and electrolyzer makers; global electrolyzer demand rose 120% in 2024, tightening supply and pricing power. Scarcity of low‑carbon power—IEA estimates 2025 green electricity shortfalls in Europe at 100–150 TWh—lets utilities demand premium contracts. For Yara, securing long‑term, sub‑$40/MWh renewables and reliable 1+ GW electrolyzer deliveries is critical, so suppliers hold strong leverage.

Logistics and Maritime Freight

Global bulk fertilizer distribution depends on specialized shipping and port capacity, with top three maritime logistics firms handling an estimated 60–70% of ammonia/chemical carrier capacity in 2024, raising supplier leverage over Yara International.

Freight-rate swings—Baltic Dirty Tanker Index rose ~45% in 2023–24—and limited ammonia carriers push landed costs up to 15–25% in distant markets, especially during fuel-price spikes.

Supplier bargaining power spikes during port congestion and charter shortages; 2022–24 port delays added ~3–5 days average transit time, increasing inventory and working-capital needs for Yara.

- Top 3 firms control ~60–70% capacity

- Freight volatility raised landed cost 15–25%

- Port delays added 3–5 days (2022–24)

- Fuel spikes magnify supplier leverage

Geopolitical Influence on Raw Materials

Supplier concentration lifts costs: gas, shippers, and exporters drive 15–25% price shocks

Suppliers hold strong power: gas drove $1.1–1.4B feedstock cost in 2024 (~70–80% of ammonia cost), top-5 phosphate/potash exporters supplied ~70% of exports, electrolyzer demand rose 120% in 2024, and top-3 shippers controlled 60–70% capacity—raising landed costs 15–25% and adding 3–5 days transit (2022–24).

| Metric | 2024–25 |

|---|---|

| Gas spend | $1.1–1.4B |

| Top-5 export share | ~70% |

| Electrolyzer demand | +120% |

| Shipper share | 60–70% |

| Landed cost uplift | 15–25% |

| Transit delay | 3–5 days |

What is included in the product

Concise Porter's Five Forces analysis for Yara International highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, plus strategic implications for pricing, margins, and market defense.

A concise Porter's Five Forces snapshot tailored to Yara International—quickly assess supplier, buyer, competitive, substitution, and entrant pressures to guide fertilizer-sector strategy.

Customers Bargaining Power

Consolidation of Agricultural Retailers

In North America and Europe, consolidated agricultural retailers and cooperatives—like CHS Inc. (US) and BayWa AG (Germany)—aggregate demand from thousands of farms, giving them strong volume-based bargaining power versus Yara; top 20 cooperatives account for roughly 35–40% of regional fertilizer purchases as of 2024. They secure steep discounts and extended payment terms, squeezing margins—Yara reported 2024 EBITDA margin pressure in specialty segments. These buyers freely switch global suppliers on price and technical support, raising sales churn risk for Yara and forcing competitive pricing and service investments.

Farmer Price Sensitivity and Income

Farmers are highly price-sensitive: when global crop prices fall, they cut fertilizer spend or shift to cheaper NPK blends; for example, global maize futures dropped ~18% in 2024, and FAO data show fertilizer application rates fell 7% in key producing regions that year, limiting Yara’s ability to pass on higher gas-linked production costs (Yara cites gas cost exposure up to 40%) without risking steep volume declines.

Demand for Low-Carbon Solutions

By late 2025, industrial buyers and food giants are pushing for low-carbon fertilizers to hit their Scope 3 targets, giving large customers stronger leverage to set specs and require certifications; 60% of EU agribusinesses surveyed in 2024 said they'd pay a premium for green inputs, and Yara faces contracts where >30% volume must be certified low-emission. Yara needs major green ammonia capex—estimated $2–3 billion by 2030—to meet demand and retain high-value customers.

Information Transparency and Digital Tools

The rise of digital farming platforms and real-time commodity feeds has cut information asymmetry; by 2025 over 40% of global farmers use precision-agriculture apps, letting buyers compare Yara prices to global ammonia and urea benchmarks instantly, reducing Yara’s regional price premiums.

Smaller farms now demand pricing tied to spot indices; Yara’s margin pressure shows in 2024 clampdown on fertilizer spreads, with global urea FOB volatility ±25% year-on-year, empowering buyers.

- 40%+ farmers use digital ag apps (2025)

- Buyers track ammonia/urea spot indices

- Regional premiums compressed, margins pressured

Switching Costs and Brand Loyalty

Yara’s commodity urea faces low switching costs, but its premium nitrate and tailored NPK products create higher customer stickiness—farmers adapting equipment and soil programs to Yara face measurable yield risk if they switch.

As rivals raised R&D and launched specialty blends in 2024–25, estimated switching propensity rose; industry reports show ~12–18% of large farms trialed alternatives in 2025, lowering barriers.

Yara must expand value-added services—precision agronomy, digital tools, and guaranteed-field trials—to defend retention and justify premium pricing.

- Commodity urea: low switching cost

- Premium nitrate/NPK: higher stickiness, yield risk

- 2025 trials: ~12–18% of large farms

- Action: scale agronomy, digital services, field guarantees

Buyer consolidation, digital adoption and green demand squeeze fertilizer margins

Buyers wield high volume leverage—top 20 co-ops ~35–40% regional purchases (2024)—and switch suppliers on price/service, compressing Yara margins; farmers cut application 7% in 2024 after maize futures fell ~18%, limiting cost pass-through. Demand for low‑carbon fertilizers (60% EU agribusiness willing to pay premium in 2024) forces ~$2–3bn green capex by 2030; digital tools (40%+ farmer adoption by 2025) lower info asymmetry, raising buyer power.

| Metric | Value |

|---|---|

| Top-20 co-op share | 35–40% (2024) |

| Fertilizer application change | -7% (2024) |

| Maize futures move | -18% (2024) |

| Farmers on digital apps | 40%+ (2025) |

| Willing pay premium (EU) | 60% (2024) |

| Green capex need | $2–3bn by 2030 |

Same Document Delivered

Yara International Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Yara International you'll receive upon purchase—no placeholders, no mockups.

The document displayed here is the final, fully formatted file ready for immediate download and use the moment you buy.

You’re previewing the complete deliverable: the same professionally written analysis will be available to you instantly after payment.