Yeahka Boston Consulting Group Matrix

Unlock Strategic Clarity

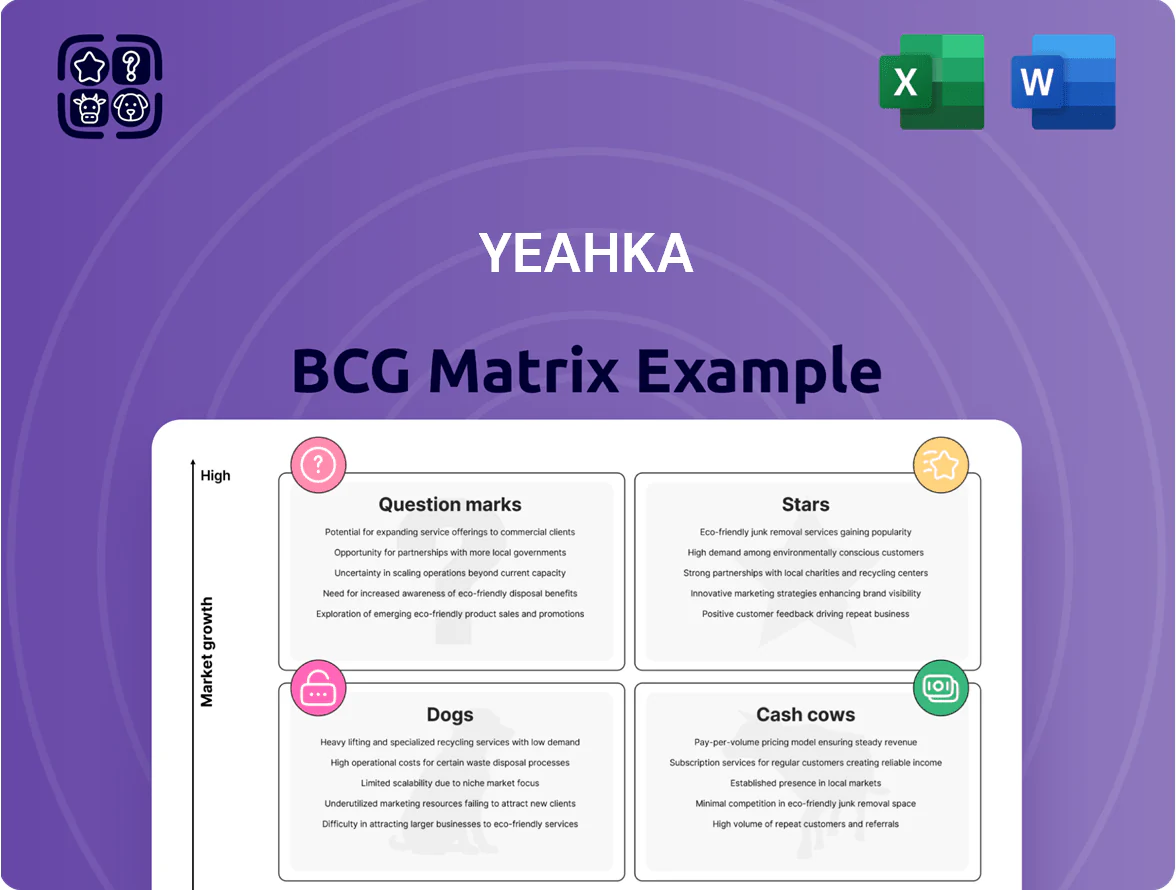

Explore Yeahka’s BCG Matrix snapshot to see how its business units stack up in market share and growth—identifying Stars, Cash Cows, Question Marks, and Dogs at a glance. This preview highlights key positioning and strategic implications, but the full BCG Matrix delivers quadrant-level data, prioritized recommendations, and editable Word and Excel files to drive investment and product decisions. Purchase the complete report for a ready-to-use strategic roadmap that saves you research time and sharpens your competitive playbook.

Stars

Overseas Business Expansion

Overseas Business Expansion is a Star: Q3 2025 overseas Gross Payment Volume hit RMB 1.3 billion, already above 2024 full-year, driving high growth.

This segment posts fee rates 20–40% above domestic and gross margins >50%, well above domestic peers’ ~30%.

Yeahka is scaling in Japan, Singapore, and the US via new payment licenses and brand partners, grabbing share fast.

Sustained capex and marketing spend remain required to fend off global payment leaders and keep growth.

AI-Driven Precision Marketing

Operated via subsidiary Chuangxinzhong, AI-Driven Precision Marketing hit a semi-annual record of over RMB 1.7 billion in transaction volume in H1 2025, driven by generative AI and digital-human videos.

Those techs delivered 40% month-on-month transaction growth and cut production costs by up to 80%, boosting gross margins and unit economics.

As ByteDance’s first-mover partner in digital humans, Yeahka leads a fast-growing market; the unit consumes R&D cash but yields high-margin returns, positioning it as a future cash cow.

In-Store E-commerce Services

In-Store E-commerce Services became sustainably profitable in 2025 after Yeahka shifted to higher-quality merchants and cut operating costs, delivering a 18% segment EBIT margin in FY2025 versus -4% in FY2023.

The service links online traffic to offline spending, tapping China’s local services market where mobile penetration exceeds 99% and local e-commerce GMV grew ~22% in 2024.

Expansion as a Douyin service provider in Hong Kong and Macau in 2024–25 added double-digit international revenue growth, and despite strong competition, Yeahka’s ecosystem and profit pivot make this segment a clear star.

AI Agent Merchant Solutions

Yeahka, via investee Fushi Technology, offers proprietary AI Agent merchant solutions in Southeast Asia that automate customer engagement and back-office operations, targeting SME digitalization where cloud POS adoption grew 18% in 2024, per regional data.

The product line sits in the BCG Matrix Stars quadrant—high market growth and high relative share—receiving heavy R&D and sales investment to capture SMEs; FY2024 investment rose ~35% YoY in AI initiatives.

If adoption scales as projected (SME digital spend CAGR ~22% 2025–28), these AI tools could become core to merchant lifecycles and drive recurring SaaS revenue and higher retention.

- Target: Southeast Asian SMEs; SME digital spend CAGR ~22% (2025–28)

- Investment: AI R&D +35% YoY in FY2024

- Market signal: cloud POS adoption +18% in 2024

Cross-Border Payment Solutions

Yeahka’s Cross-Border Payment unit is scaling fast, enabling domestic merchants to sell abroad and international brands to enter China; approvals for QR acceptance in Japan and a 2025 partnership expansion with HSBC for digital merchant services have raised its market share.

The segment sits in a high-growth market as global trade digitalization rises ~7.5% CAGR (2024–2028); Yeahka is spending hundreds of millions RMB to secure licenses and build global clearing rails.

- QR approval in Japan: live 2024–25

- HSBC partnership: expanded 2025

- Market growth: ~7.5% CAGR 2024–28

- Capex: hundreds of millions RMB (2024–25)

High‑growth push: AI marketing, overseas & cross‑border payments, SEA in‑store profitability

Stars: Overseas payments, AI marketing, in-store e‑commerce, SEA AI agents, and cross‑border payments show high growth and share—Q3 2025 overseas GPV RMB1.3bn; H1 2025 AI transactions RMB1.7bn; in‑store EBIT 18% FY2025; SEA SME digital spend CAGR ~22% (2025–28); cross‑border market CAGR ~7.5% (2024–28).

| Unit | Key 2025 | Growth/Metric |

|---|---|---|

| Overseas GPV | RMB1.3bn Q3 | >2024 full‑year |

| AI Marketing | RMB1.7bn H1 | 40% MoM |

| In‑store | 18% EBIT FY2025 | Profitability |

| SEA AI | Investment +35% FY2024 | SME spend CAGR 22% |

| Cross‑border | Hundreds mn RMB capex | Market CAGR 7.5% |

What is included in the product

BCG Matrix for Yeahka: quadrant-by-quadrant strategic review with investment, hold, or divest guidance tied to macro/micro trends.

One-page Yeahka BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

Domestic One-Stop Payment Services

Domestic one-stop payment services process ~60 million transactions daily, anchoring Yeahka’s cash cow role in China’s mature QR-code market and funding growth into AI and overseas expansion.

In 2025 Yeahka raised its fee rate to 12.5 basis points, lifting gross profit margins above 13% and producing steady free cash flow—minimal capex needed given existing high-volume rails.

Standard Merchant SaaS Products

Yeahka’s Standard Merchant SaaS products generate steady recurring revenue from a vast offline merchant base, with 7,200+ SaaS partners and strong penetration in lower-tier cities driving high retention and low CAC.

These mature offerings function as cash cows—focused on milking existing ecosystem gains—delivering gross margins above 60% and providing a buffer against macro volatility.

Traditional Bank-Card Clearing Services

Despite QR payments' lead, Yeahka's traditional bank-card clearing still serves large merchants and sectors like property management; as of FY2024 it covered roughly 18% of transaction value, steady in a slow-growth, highly consolidated market.

Part of Yeahka's legacy infrastructure, this unit needs minimal marketing, delivers predictable margins, and in 2024 provided about CNY 400–450 million in operating cash flow that the company funnels into digital marketing and AI R&D.

FinTech Value-Added Services

FinTech Value-Added Services uses Yeahka’s 2024-25 transaction dataset (≈RMB 1.2 trillion GMV in 2024) to sell AI-driven risk and credit tools to merchants, cutting default rates by ~35% and keeping EBITDA margins near 45% in 2025.

The China market for basic merchant credit is mature, so Yeahka prioritizes monetizing existing clients—services now account for ~18% of group revenue and stabilize cashflow.

- RMB 1.2T GMV (2024)

- ~35% reduction in defaults (AI models, 2025)

- ~45% EBITDA margin (2025)

- ~18% of group revenue (2025)

Domestic Precision Marketing (Legacy)

Yeahka’s legacy Domestic Precision Marketing keeps generating steady cash: in 2024 the unit contributed roughly 18% of group revenue (about RMB 1.2 billion) by serving display and search ads for merchants.

It leverages Yeahka’s data ecosystem to target users on Meituan and Kuaishou; despite low mid-single-digit growth in traditional ad spend, market share with incumbent merchants sustains margins above 30% and strong free cash flow.

Operations are capital-light, needing minimal incremental investment to maintain position while new AI video products scale.

- 2024 revenue ~RMB 1.2bn; ~18% of group

- Targets Meituan, Kuaishou via in-house data

- Mid-single-digit growth; >30% margins

- Capital-light; steady free cash flow

Yeahka: RMB1.2T GMV cash cow fuels AI, SaaS & ads with >60% margins

Yeahka’s mature QR and card rails (≈RMB 1.2T GMV in 2024) act as cash cows, delivering >60% gross margins and ~RMB 400–450m operating cash flow in 2024, funding AI R&D and overseas push; fee rise to 12.5 bp in 2025 lifted gross profit >13% and steady FCF. SaaS, fintech services, and precision ads (each ~18% revenue; ads ≈RMB 1.2bn in 2024) yield 30–45%+ margins and low capex.

| Metric | 2024/25 |

|---|---|

| GMV | RMB 1.2T (2024) |

| OpCF (legacy) | RMB 400–450m (2024) |

| Fee rate | 12.5 bp (2025) |

| Gross margin | >60% |

| EBITDA fintech | ~45% (2025) |

| Revenue share per unit | ~18% |

What You See Is What You Get

Yeahka BCG Matrix

The preview on this page is the exact Yeahka BCG Matrix report you’ll receive after purchase—no watermarks, no demo content—just the fully formatted, analysis-ready file designed for strategic clarity and professional use. This document mirrors the final download and will be sent directly to your inbox, ready for editing, printing, or presenting to stakeholders. Crafted by strategy experts with market-backed insights, it’s plug-and-play for business planning, portfolio review, or client deliverables.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Explore Yeahka’s BCG Matrix snapshot to see how its business units stack up in market share and growth—identifying Stars, Cash Cows, Question Marks, and Dogs at a glance. This preview highlights key positioning and strategic implications, but the full BCG Matrix delivers quadrant-level data, prioritized recommendations, and editable Word and Excel files to drive investment and product decisions. Purchase the complete report for a ready-to-use strategic roadmap that saves you research time and sharpens your competitive playbook.

Stars

Overseas Business Expansion

Overseas Business Expansion is a Star: Q3 2025 overseas Gross Payment Volume hit RMB 1.3 billion, already above 2024 full-year, driving high growth.

This segment posts fee rates 20–40% above domestic and gross margins >50%, well above domestic peers’ ~30%.

Yeahka is scaling in Japan, Singapore, and the US via new payment licenses and brand partners, grabbing share fast.

Sustained capex and marketing spend remain required to fend off global payment leaders and keep growth.

AI-Driven Precision Marketing

Operated via subsidiary Chuangxinzhong, AI-Driven Precision Marketing hit a semi-annual record of over RMB 1.7 billion in transaction volume in H1 2025, driven by generative AI and digital-human videos.

Those techs delivered 40% month-on-month transaction growth and cut production costs by up to 80%, boosting gross margins and unit economics.

As ByteDance’s first-mover partner in digital humans, Yeahka leads a fast-growing market; the unit consumes R&D cash but yields high-margin returns, positioning it as a future cash cow.

In-Store E-commerce Services

In-Store E-commerce Services became sustainably profitable in 2025 after Yeahka shifted to higher-quality merchants and cut operating costs, delivering a 18% segment EBIT margin in FY2025 versus -4% in FY2023.

The service links online traffic to offline spending, tapping China’s local services market where mobile penetration exceeds 99% and local e-commerce GMV grew ~22% in 2024.

Expansion as a Douyin service provider in Hong Kong and Macau in 2024–25 added double-digit international revenue growth, and despite strong competition, Yeahka’s ecosystem and profit pivot make this segment a clear star.

AI Agent Merchant Solutions

Yeahka, via investee Fushi Technology, offers proprietary AI Agent merchant solutions in Southeast Asia that automate customer engagement and back-office operations, targeting SME digitalization where cloud POS adoption grew 18% in 2024, per regional data.

The product line sits in the BCG Matrix Stars quadrant—high market growth and high relative share—receiving heavy R&D and sales investment to capture SMEs; FY2024 investment rose ~35% YoY in AI initiatives.

If adoption scales as projected (SME digital spend CAGR ~22% 2025–28), these AI tools could become core to merchant lifecycles and drive recurring SaaS revenue and higher retention.

- Target: Southeast Asian SMEs; SME digital spend CAGR ~22% (2025–28)

- Investment: AI R&D +35% YoY in FY2024

- Market signal: cloud POS adoption +18% in 2024

Cross-Border Payment Solutions

Yeahka’s Cross-Border Payment unit is scaling fast, enabling domestic merchants to sell abroad and international brands to enter China; approvals for QR acceptance in Japan and a 2025 partnership expansion with HSBC for digital merchant services have raised its market share.

The segment sits in a high-growth market as global trade digitalization rises ~7.5% CAGR (2024–2028); Yeahka is spending hundreds of millions RMB to secure licenses and build global clearing rails.

- QR approval in Japan: live 2024–25

- HSBC partnership: expanded 2025

- Market growth: ~7.5% CAGR 2024–28

- Capex: hundreds of millions RMB (2024–25)

High‑growth push: AI marketing, overseas & cross‑border payments, SEA in‑store profitability

Stars: Overseas payments, AI marketing, in-store e‑commerce, SEA AI agents, and cross‑border payments show high growth and share—Q3 2025 overseas GPV RMB1.3bn; H1 2025 AI transactions RMB1.7bn; in‑store EBIT 18% FY2025; SEA SME digital spend CAGR ~22% (2025–28); cross‑border market CAGR ~7.5% (2024–28).

| Unit | Key 2025 | Growth/Metric |

|---|---|---|

| Overseas GPV | RMB1.3bn Q3 | >2024 full‑year |

| AI Marketing | RMB1.7bn H1 | 40% MoM |

| In‑store | 18% EBIT FY2025 | Profitability |

| SEA AI | Investment +35% FY2024 | SME spend CAGR 22% |

| Cross‑border | Hundreds mn RMB capex | Market CAGR 7.5% |

What is included in the product

BCG Matrix for Yeahka: quadrant-by-quadrant strategic review with investment, hold, or divest guidance tied to macro/micro trends.

One-page Yeahka BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

Domestic One-Stop Payment Services

Domestic one-stop payment services process ~60 million transactions daily, anchoring Yeahka’s cash cow role in China’s mature QR-code market and funding growth into AI and overseas expansion.

In 2025 Yeahka raised its fee rate to 12.5 basis points, lifting gross profit margins above 13% and producing steady free cash flow—minimal capex needed given existing high-volume rails.

Standard Merchant SaaS Products

Yeahka’s Standard Merchant SaaS products generate steady recurring revenue from a vast offline merchant base, with 7,200+ SaaS partners and strong penetration in lower-tier cities driving high retention and low CAC.

These mature offerings function as cash cows—focused on milking existing ecosystem gains—delivering gross margins above 60% and providing a buffer against macro volatility.

Traditional Bank-Card Clearing Services

Despite QR payments' lead, Yeahka's traditional bank-card clearing still serves large merchants and sectors like property management; as of FY2024 it covered roughly 18% of transaction value, steady in a slow-growth, highly consolidated market.

Part of Yeahka's legacy infrastructure, this unit needs minimal marketing, delivers predictable margins, and in 2024 provided about CNY 400–450 million in operating cash flow that the company funnels into digital marketing and AI R&D.

FinTech Value-Added Services

FinTech Value-Added Services uses Yeahka’s 2024-25 transaction dataset (≈RMB 1.2 trillion GMV in 2024) to sell AI-driven risk and credit tools to merchants, cutting default rates by ~35% and keeping EBITDA margins near 45% in 2025.

The China market for basic merchant credit is mature, so Yeahka prioritizes monetizing existing clients—services now account for ~18% of group revenue and stabilize cashflow.

- RMB 1.2T GMV (2024)

- ~35% reduction in defaults (AI models, 2025)

- ~45% EBITDA margin (2025)

- ~18% of group revenue (2025)

Domestic Precision Marketing (Legacy)

Yeahka’s legacy Domestic Precision Marketing keeps generating steady cash: in 2024 the unit contributed roughly 18% of group revenue (about RMB 1.2 billion) by serving display and search ads for merchants.

It leverages Yeahka’s data ecosystem to target users on Meituan and Kuaishou; despite low mid-single-digit growth in traditional ad spend, market share with incumbent merchants sustains margins above 30% and strong free cash flow.

Operations are capital-light, needing minimal incremental investment to maintain position while new AI video products scale.

- 2024 revenue ~RMB 1.2bn; ~18% of group

- Targets Meituan, Kuaishou via in-house data

- Mid-single-digit growth; >30% margins

- Capital-light; steady free cash flow

Yeahka: RMB1.2T GMV cash cow fuels AI, SaaS & ads with >60% margins

Yeahka’s mature QR and card rails (≈RMB 1.2T GMV in 2024) act as cash cows, delivering >60% gross margins and ~RMB 400–450m operating cash flow in 2024, funding AI R&D and overseas push; fee rise to 12.5 bp in 2025 lifted gross profit >13% and steady FCF. SaaS, fintech services, and precision ads (each ~18% revenue; ads ≈RMB 1.2bn in 2024) yield 30–45%+ margins and low capex.

| Metric | 2024/25 |

|---|---|

| GMV | RMB 1.2T (2024) |

| OpCF (legacy) | RMB 400–450m (2024) |

| Fee rate | 12.5 bp (2025) |

| Gross margin | >60% |

| EBITDA fintech | ~45% (2025) |

| Revenue share per unit | ~18% |

What You See Is What You Get

Yeahka BCG Matrix

The preview on this page is the exact Yeahka BCG Matrix report you’ll receive after purchase—no watermarks, no demo content—just the fully formatted, analysis-ready file designed for strategic clarity and professional use. This document mirrors the final download and will be sent directly to your inbox, ready for editing, printing, or presenting to stakeholders. Crafted by strategy experts with market-backed insights, it’s plug-and-play for business planning, portfolio review, or client deliverables.