Yeahka Porter's Five Forces Analysis

From Overview to Strategy Blueprint

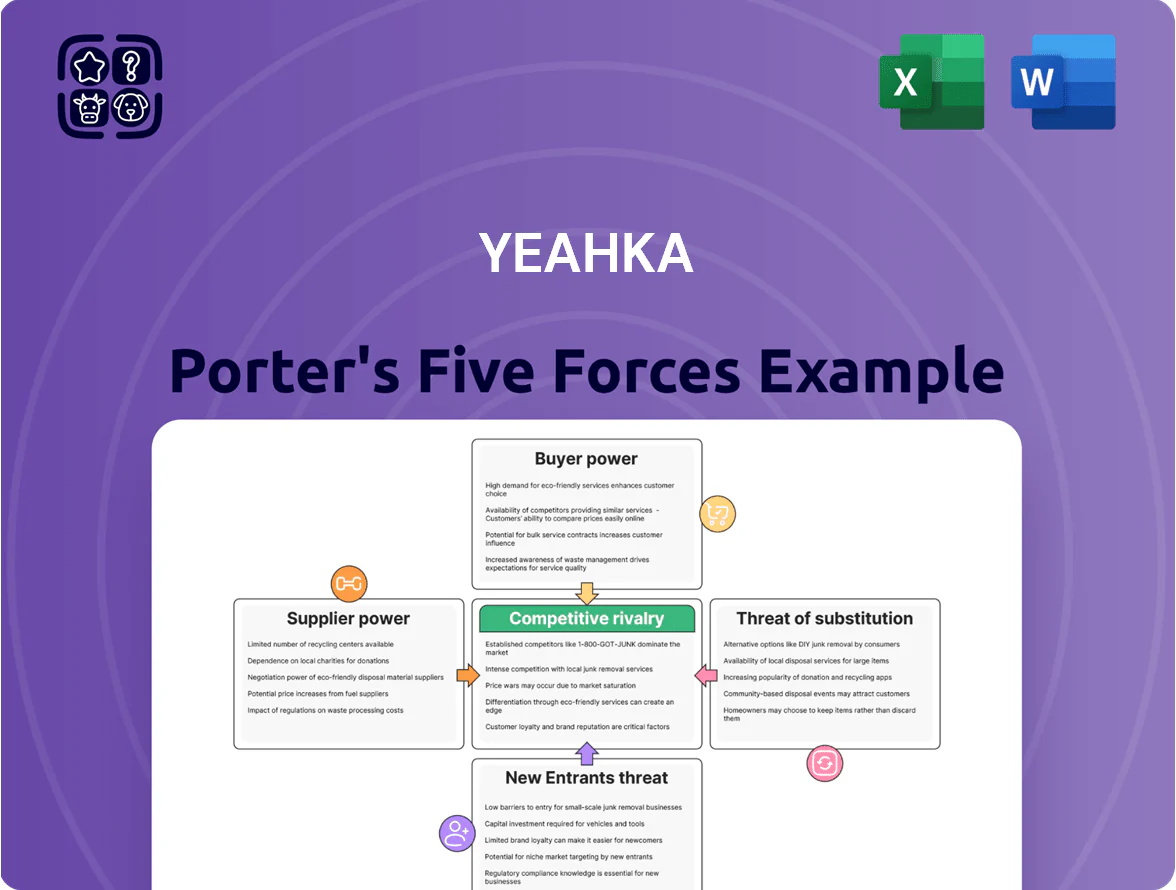

Yeahka faces intense buyer price sensitivity, rising threat from fintech entrants, and moderate supplier leverage due to platform partnerships; this snapshot highlights key strategic pressures but only scratches the surface.

Suppliers Bargaining Power

Dependence on major clearing houses and banks

Yeahka depends on China UnionPay and NetsUnion Clearing Corporation for core settlement; in 2024 UnionPay handled ~75% of China card transactions and NetsUnion processed the majority of QR/payments, so these platforms set protocols and fees that define Yeahka’s unit costs.

Both are centralized and state-linked, giving Yeahka little bargaining power to cut processing fees or alter technical standards; this concentration likely keeps Yeahka’s gross margin on payment services constrained—card fees in China averaged ~0.4–0.6% in 2024.

Reliance on dominant mobile wallet platforms

Yeahka depends on Alipay and WeChat Pay for merchant reach; together they held about 92% of China’s mobile payments volume in 2024, so their platform rules shape aggregator access and pricing.

Their control lets them change partner terms or commission splits—Alipay/Tencent fee moves of even 1–2 percentage points could cut Yeahka’s gross margin materially given Yeahka’s 2024 net transaction revenue of RMB 2.1 billion.

Influence of technology and cloud infrastructure providers

Yeahka’s SaaS and payment services rely on external cloud giants—Alibaba Cloud, Huawei Cloud—so migrating petabyte-scale merchant data and real-time processing stacks carries high switching costs, giving suppliers moderate bargaining power; in 2024 China cloud revenue grew 26% to about CNY 360bn, so tiered pricing and SLAs can materially affect Yeahka’s cost of goods sold and margins (for example, a 5–10% price uplift would raise infrastructure spend notably).

Sourcing of payment hardware and POS terminals

Yeahka needs steady supply of smart POS terminals and QR scanners to onboard brick‑and‑mortar merchants, but security and encryption specs shrink qualified Chinese vendors to a few certified makers.

Global semiconductor price volatility and 2024–25 supply constraints raised component costs ~15–30%, risking higher unit costs and slower rollout for Yeahka’s hardware-dependent merchant acquisition.

Regulatory compliance and licensing authorities

The People’s Bank of China and other regulators are effectively suppliers of Yeahka’s legal right to operate, controlling payment licenses, data privacy rules, and cross-border approvals; non-compliance can stop services.

In 2023 China tightened payment and data rules—fines up to RMB 1 million and license revocations—so a regulatory pivot could force Yeahka to rework products, incurring multimillion-yuan costs and revenue hits.

- Regulators = legal gatekeepers

- Controls: licenses, data, cross-border

- Non-compliance: fines, revocation

- 2023 rule shifts raised compliance costs

Dominant platforms and cost shocks squeeze Yeahka margins and raise compliance risk

Suppliers hold strong power: UnionPay/NetsUnion (≈75% card share; QR dominance) and Alipay+WeChat (≈92% mobile volume in 2024) set fees and rules that constrain Yeahka’s margins; card fees averaged 0.4–0.6% in 2024 and Yeahka’s 2024 net transaction revenue was RMB 2.1bn. Cloud and certified POS vendors raise switching costs; 2024–25 component cost shocks (+15–30%) and tighter 2023 regs (fines, license risk) add material supply-side risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| UnionPay/NetsUnion | ≈75% card; QR majority | Controls fees/protocols |

| Alipay+WeChat | ≈92% mobile vol | Platform rules, commission risk |

| Cloud vendors | China cloud rev CNY360bn (2024) | Switching cost, pricing pressure |

| Hardware suppliers | Component costs +15–30% (2024–25) | Higher unit costs, slower rollout |

| Regulators | 2023 tightened rules | License/compliance risk, fines |

What is included in the product

Tailored Porter's Five Forces for Yeahka, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and strategic risks to its market share and profitability.

Concise Porter's Five Forces summary for Yeahka—spot competitive pressures and relief strategies at a glance to speed boardroom decisions.

Customers Bargaining Power

Low switching costs for small and medium merchants

The primary customers for Yeahka are SMEs with low switching costs—industry surveys show 62% of Chinese small merchants used multiple payment providers in 2024—so similar core features and a 0.2–0.6% fee sensitivity push merchants to choose ease of setup and price; this forces Yeahka to iterate product features quarterly and maintain higher support spend (customer service costs rose 14% in 2024) to retain merchant loyalty.

High price sensitivity regarding transaction fees

In China’s cutthroat payments market, merchants shift over fee gaps as small as 0.1 percentage point; a 2024 iResearch report found 38% of SMEs switched providers for lower rates. Merchants treat card and QR payments as a utility and press for discounts or promotional pricing, limiting Yeahka’s pricing power. Yeahka risks a sharp drop in active merchants—its merchant churn rose to 12% in FY2024 when average take-rate climbed 0.15ppt.

Demand for integrated value-added services

Modern merchants want more than payments; 72% of Chinese SMBs in a 2024 IDC survey said they prefer bundled SaaS for POS, CRM, and inventory, giving buyers pricing leverage as they demand integrated, discountable packages.

As merchants grow sophisticated, Yeahka (NYSE: YEAH) faces churn risk if its ecosystem lags—2023 merchant ARPU fell 6% at some Chinese rivals when add-on services were missing, so expanding SaaS offerings is critical to retain volume and margin.

Fragmented nature of the merchant base

Individual small merchants hold little bargaining clout, but Yeahka faces a fragmented merchant base exceeding 8 million active POS merchants across China (2024), forcing management of vast low-value accounts and high service overhead.

No single customer can push prices, yet high churn (industry ~25% annual for micro-merchants) forces heavy marketing and acquisition spend, so the aggregate market effectively controls Yeahka’s customer acquisition cost (CAC).

- ~8M active merchants (2024)

- Industry micro-merchant churn ~25%/yr

- High CAC driven by volume replacement

- No single-customer pricing pressure

Availability of transparent market information

Digital platforms and industry forums let merchants compare payment rates and service quality for providers like Yeahka, Lakala, and Huifu; a 2024 China fintech survey found 62% of SMEs used online comparison tools when choosing payment partners.

High transparency means merchants can cite competitor offers to negotiate lower transaction fees—average card-acquiring fees in 2024 ranged 0.38%–0.8%—shrinking Yeahka’s room for hidden charges.

Information symmetry cuts Yeahka’s opportunistic pricing and raises churn risk if terms aren’t competitive; merchant switching costs are estimated under CNY 1,500 for typical SMB setups.

- 62% of SMEs use online comparison tools (2024)

- Typical card fees 0.38%–0.8% (2024)

- SMB switching cost ≈ CNY 1,500

SME Bargaining Bite: Low Costs, High Comparison Use Drive 12% Yeahka Churn

SME customers wield strong aggregate bargaining power: low switching costs (~CNY1,500), high price sensitivity (card fees 0.38%–0.8% in 2024), and heavy use of comparison tools (62% of SMEs) drive churn (~25% for micro-merchants) and force Yeahka to invest in product, support, and promotions (support costs +14% in 2024; merchant churn 12% at Yeahka in FY2024).

| Metric | 2024 |

|---|---|

| Active merchants | ~8M |

| SME comparison use | 62% |

| Card fee range | 0.38%–0.8% |

| Micro-merchant churn | ~25%/yr |

| Yeahka churn | 12% (FY2024) |

Full Version Awaits

Yeahka Porter's Five Forces Analysis

This preview shows the exact Yeahka Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples; it’s the final, professionally formatted document ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Yeahka faces intense buyer price sensitivity, rising threat from fintech entrants, and moderate supplier leverage due to platform partnerships; this snapshot highlights key strategic pressures but only scratches the surface.

Suppliers Bargaining Power

Dependence on major clearing houses and banks

Yeahka depends on China UnionPay and NetsUnion Clearing Corporation for core settlement; in 2024 UnionPay handled ~75% of China card transactions and NetsUnion processed the majority of QR/payments, so these platforms set protocols and fees that define Yeahka’s unit costs.

Both are centralized and state-linked, giving Yeahka little bargaining power to cut processing fees or alter technical standards; this concentration likely keeps Yeahka’s gross margin on payment services constrained—card fees in China averaged ~0.4–0.6% in 2024.

Reliance on dominant mobile wallet platforms

Yeahka depends on Alipay and WeChat Pay for merchant reach; together they held about 92% of China’s mobile payments volume in 2024, so their platform rules shape aggregator access and pricing.

Their control lets them change partner terms or commission splits—Alipay/Tencent fee moves of even 1–2 percentage points could cut Yeahka’s gross margin materially given Yeahka’s 2024 net transaction revenue of RMB 2.1 billion.

Influence of technology and cloud infrastructure providers

Yeahka’s SaaS and payment services rely on external cloud giants—Alibaba Cloud, Huawei Cloud—so migrating petabyte-scale merchant data and real-time processing stacks carries high switching costs, giving suppliers moderate bargaining power; in 2024 China cloud revenue grew 26% to about CNY 360bn, so tiered pricing and SLAs can materially affect Yeahka’s cost of goods sold and margins (for example, a 5–10% price uplift would raise infrastructure spend notably).

Sourcing of payment hardware and POS terminals

Yeahka needs steady supply of smart POS terminals and QR scanners to onboard brick‑and‑mortar merchants, but security and encryption specs shrink qualified Chinese vendors to a few certified makers.

Global semiconductor price volatility and 2024–25 supply constraints raised component costs ~15–30%, risking higher unit costs and slower rollout for Yeahka’s hardware-dependent merchant acquisition.

Regulatory compliance and licensing authorities

The People’s Bank of China and other regulators are effectively suppliers of Yeahka’s legal right to operate, controlling payment licenses, data privacy rules, and cross-border approvals; non-compliance can stop services.

In 2023 China tightened payment and data rules—fines up to RMB 1 million and license revocations—so a regulatory pivot could force Yeahka to rework products, incurring multimillion-yuan costs and revenue hits.

- Regulators = legal gatekeepers

- Controls: licenses, data, cross-border

- Non-compliance: fines, revocation

- 2023 rule shifts raised compliance costs

Dominant platforms and cost shocks squeeze Yeahka margins and raise compliance risk

Suppliers hold strong power: UnionPay/NetsUnion (≈75% card share; QR dominance) and Alipay+WeChat (≈92% mobile volume in 2024) set fees and rules that constrain Yeahka’s margins; card fees averaged 0.4–0.6% in 2024 and Yeahka’s 2024 net transaction revenue was RMB 2.1bn. Cloud and certified POS vendors raise switching costs; 2024–25 component cost shocks (+15–30%) and tighter 2023 regs (fines, license risk) add material supply-side risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| UnionPay/NetsUnion | ≈75% card; QR majority | Controls fees/protocols |

| Alipay+WeChat | ≈92% mobile vol | Platform rules, commission risk |

| Cloud vendors | China cloud rev CNY360bn (2024) | Switching cost, pricing pressure |

| Hardware suppliers | Component costs +15–30% (2024–25) | Higher unit costs, slower rollout |

| Regulators | 2023 tightened rules | License/compliance risk, fines |

What is included in the product

Tailored Porter's Five Forces for Yeahka, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and strategic risks to its market share and profitability.

Concise Porter's Five Forces summary for Yeahka—spot competitive pressures and relief strategies at a glance to speed boardroom decisions.

Customers Bargaining Power

Low switching costs for small and medium merchants

The primary customers for Yeahka are SMEs with low switching costs—industry surveys show 62% of Chinese small merchants used multiple payment providers in 2024—so similar core features and a 0.2–0.6% fee sensitivity push merchants to choose ease of setup and price; this forces Yeahka to iterate product features quarterly and maintain higher support spend (customer service costs rose 14% in 2024) to retain merchant loyalty.

High price sensitivity regarding transaction fees

In China’s cutthroat payments market, merchants shift over fee gaps as small as 0.1 percentage point; a 2024 iResearch report found 38% of SMEs switched providers for lower rates. Merchants treat card and QR payments as a utility and press for discounts or promotional pricing, limiting Yeahka’s pricing power. Yeahka risks a sharp drop in active merchants—its merchant churn rose to 12% in FY2024 when average take-rate climbed 0.15ppt.

Demand for integrated value-added services

Modern merchants want more than payments; 72% of Chinese SMBs in a 2024 IDC survey said they prefer bundled SaaS for POS, CRM, and inventory, giving buyers pricing leverage as they demand integrated, discountable packages.

As merchants grow sophisticated, Yeahka (NYSE: YEAH) faces churn risk if its ecosystem lags—2023 merchant ARPU fell 6% at some Chinese rivals when add-on services were missing, so expanding SaaS offerings is critical to retain volume and margin.

Fragmented nature of the merchant base

Individual small merchants hold little bargaining clout, but Yeahka faces a fragmented merchant base exceeding 8 million active POS merchants across China (2024), forcing management of vast low-value accounts and high service overhead.

No single customer can push prices, yet high churn (industry ~25% annual for micro-merchants) forces heavy marketing and acquisition spend, so the aggregate market effectively controls Yeahka’s customer acquisition cost (CAC).

- ~8M active merchants (2024)

- Industry micro-merchant churn ~25%/yr

- High CAC driven by volume replacement

- No single-customer pricing pressure

Availability of transparent market information

Digital platforms and industry forums let merchants compare payment rates and service quality for providers like Yeahka, Lakala, and Huifu; a 2024 China fintech survey found 62% of SMEs used online comparison tools when choosing payment partners.

High transparency means merchants can cite competitor offers to negotiate lower transaction fees—average card-acquiring fees in 2024 ranged 0.38%–0.8%—shrinking Yeahka’s room for hidden charges.

Information symmetry cuts Yeahka’s opportunistic pricing and raises churn risk if terms aren’t competitive; merchant switching costs are estimated under CNY 1,500 for typical SMB setups.

- 62% of SMEs use online comparison tools (2024)

- Typical card fees 0.38%–0.8% (2024)

- SMB switching cost ≈ CNY 1,500

SME Bargaining Bite: Low Costs, High Comparison Use Drive 12% Yeahka Churn

SME customers wield strong aggregate bargaining power: low switching costs (~CNY1,500), high price sensitivity (card fees 0.38%–0.8% in 2024), and heavy use of comparison tools (62% of SMEs) drive churn (~25% for micro-merchants) and force Yeahka to invest in product, support, and promotions (support costs +14% in 2024; merchant churn 12% at Yeahka in FY2024).

| Metric | 2024 |

|---|---|

| Active merchants | ~8M |

| SME comparison use | 62% |

| Card fee range | 0.38%–0.8% |

| Micro-merchant churn | ~25%/yr |

| Yeahka churn | 12% (FY2024) |

Full Version Awaits

Yeahka Porter's Five Forces Analysis

This preview shows the exact Yeahka Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples; it’s the final, professionally formatted document ready for immediate download and use.